Note:

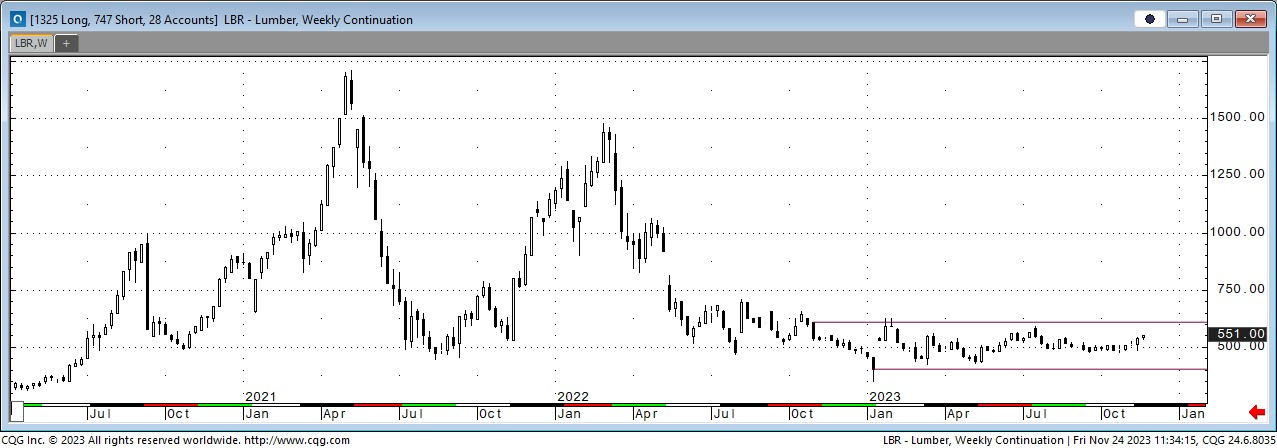

The futures market continues to drift toward the 200-day average. If the market is lower, it drifts up to it; if the market is higher, it drifts down. That average has been flat for months, and the market looks to be near fair value whenever it is close. This is not a buyer or seller manipulation. It is fair value for the current supply and demand. This simplifies the game. If you stay within the goalposts, you make money. Those goalposts are $20 under and $30 over. That was the proper strategy in 2023 and continues into 2024. Can this market stay perfectly balanced for the long term? Most likely not, but the reasons for imbalance take time to materialize. The risk in 2024 is that demand will outpace supply at certain points. The upside risk is real and should be mitigated. After 2017 and 2021, no one can tell me things will be normal again. You need to protect yourself if you have 2nd, third, and fourth-quarter risks. If supply becomes an issue, you are protected. If not, a yearend loss in futures will dwarf the cash gains.

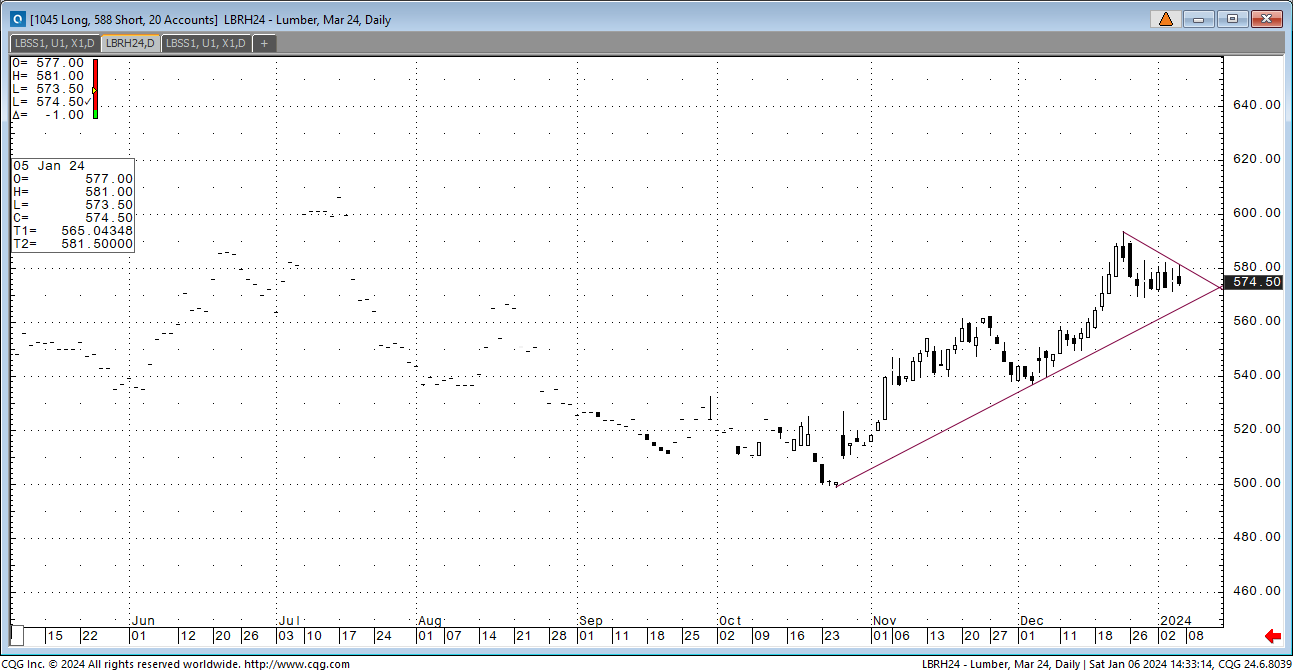

In the short run, this market continues in a wave pattern with higher highs and higher lows. While marginal, it does offer a playbook of sorts as to when to enter the market. The December low was 537.00. The January low was 542.50. With the 200-day at 548.40, I would set that as the objective right now. The funds are buying, making it a slog. There was a jump in the industry shorts. If the mills are selling, the spring rally will start early.

Flounder to flat this week??

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636