Recap:

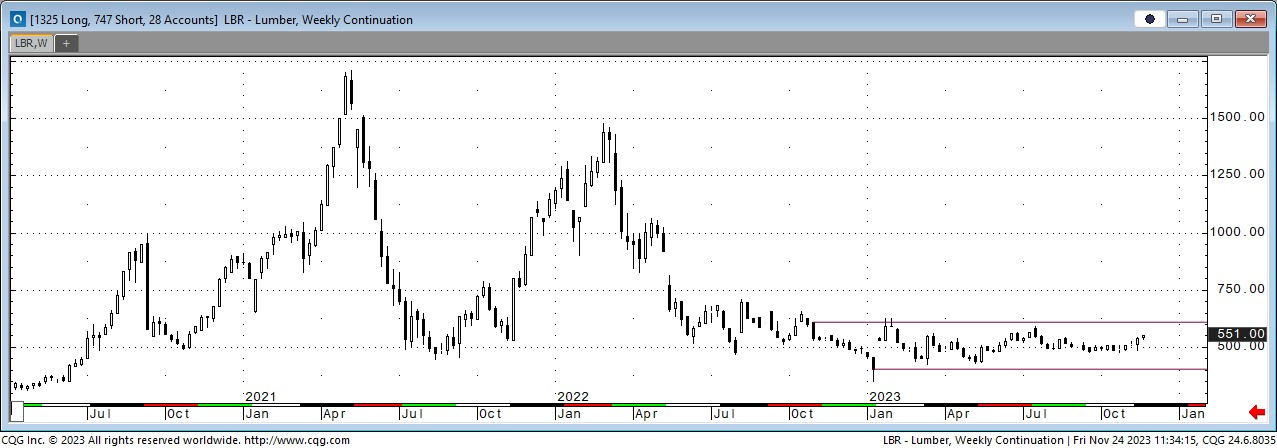

On the surface, the futures trade last week looked flat. The net change for the week was up $2. In fact, the last seven sessions have seen closes within a $4 range. A digestion phase after the run-up? Underneath the surface, things are changing. We have shifted the fund shorts over to the industry. Wood is now hedged. We have also shifted some of the industry longs over to new fund longs. The makeup of the futures market today is friendly. It is not a signal to buy, but it could generate higher prices on its own.

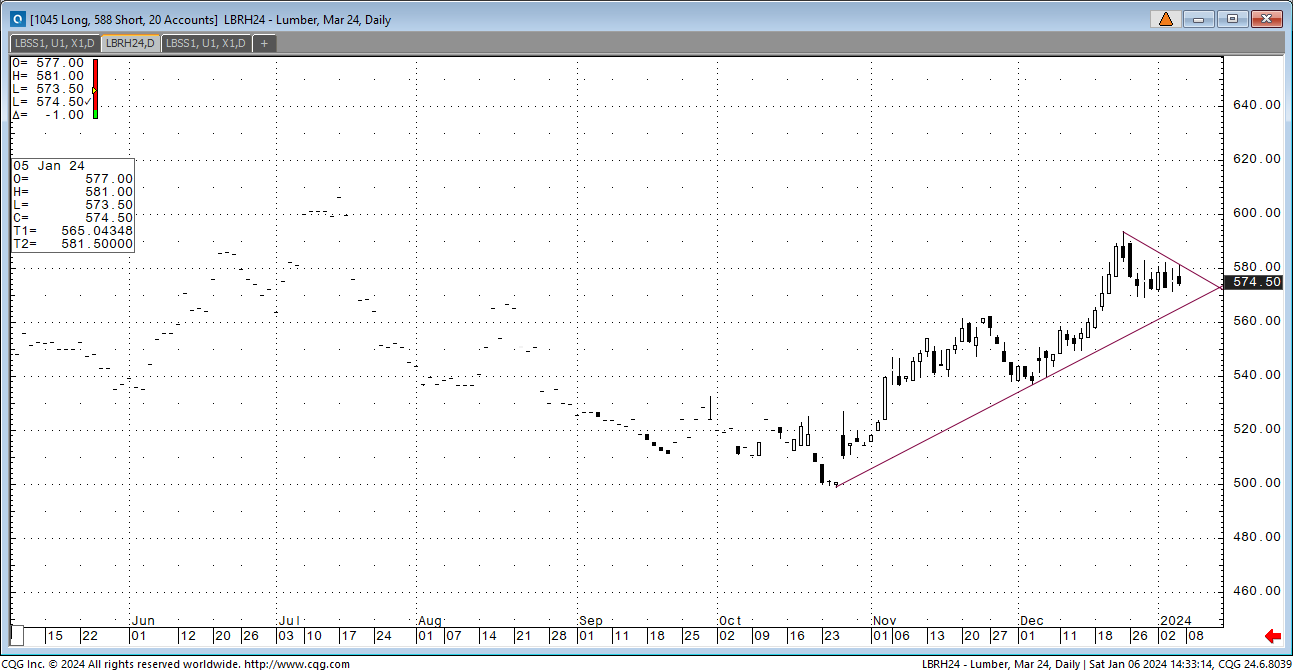

The futures market is closed on Monday the 15th, so January expires on Friday. The current open interest is normal for five sessions to go. With the growing industry’s short number, we may see some upward pressure again. We could see a shift to expirations now having an upward bias.

As far as the cash market goes, it remains fluid. That has been the case for months now. It has the feel of the covid slowdown that never occurred. This time, we spent a year expecting a recession and higher unemployment. What we found was steady business.

With mills coming back online and wholesalers owning wood, it could be sloppy for a while. The funds are the key.

This recent sideways trade is nearing an end…….

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636