Note:

It is still February. I have to remind most traders of that. Most are trying to accelerate the cycle up a few months, looking for all the issues to hit. In reality, the market is trading at an average February pace. What is unusual is the added buying in the last few weeks. Most are trying to hold a consistent inventory level into the spring buy. The previous two weeks’ business was not an inventory build but a fill-in. That is mildly friendly.

It is a challenging environment to navigate. For every negative data point, there is a positive one. You can’t get pessimistic about the housing industry. 2024 will be steady. The difference between 2023 and 2024 was that the lumber market was demand-driven. There could be a pivot coming to a supply-driven market. That is when the volatility starts. Last year, the cheapest, most abundant wood in the world was sitting at Port Canaveral. That is different this year.

Technical:

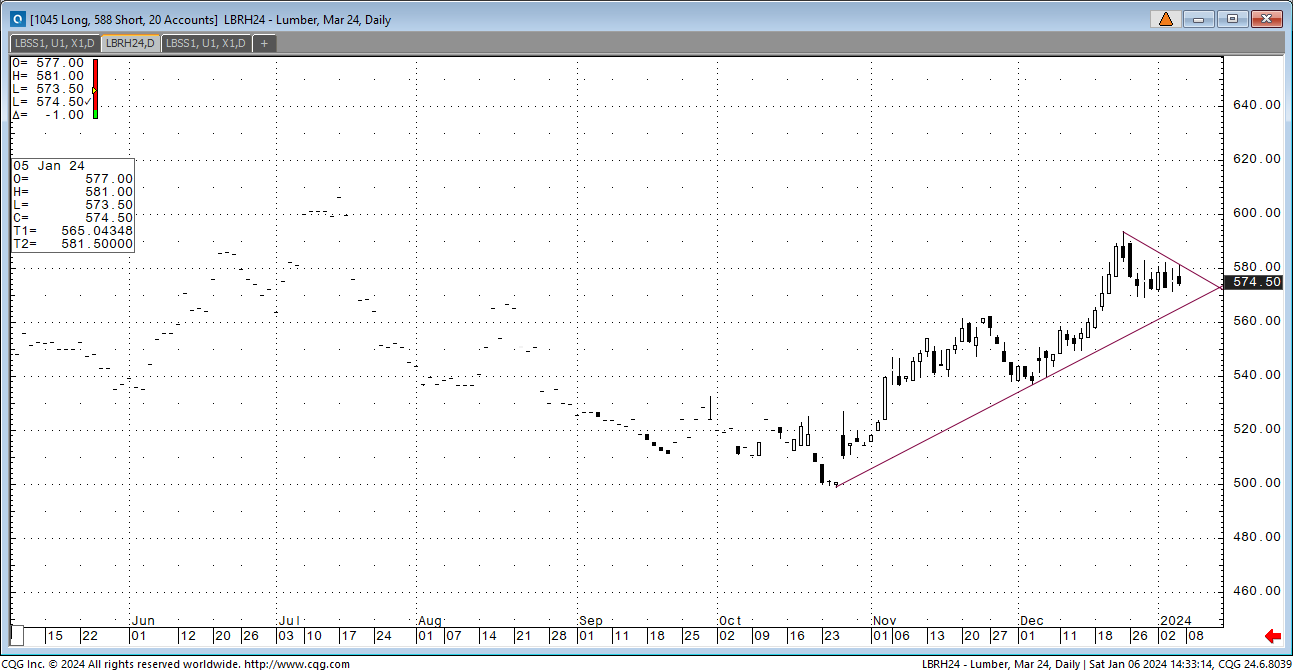

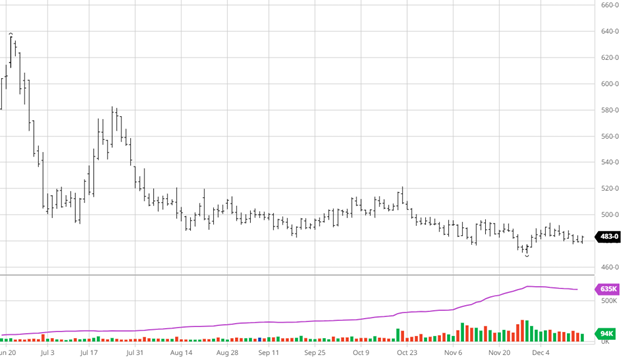

I am switching to the May futures contract for the tech read. Now is a good time to mention the significant gap from 572.00 to 566.00 under the market. For now, we aren’t going to worry about it. The RSI is 62%, with most momentum indicators pointing up. You can build a case that May has been a more volatile trade. That may indicate more volatility to come. A few extra cars with futures $30 over is a win/win.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636