Recap:

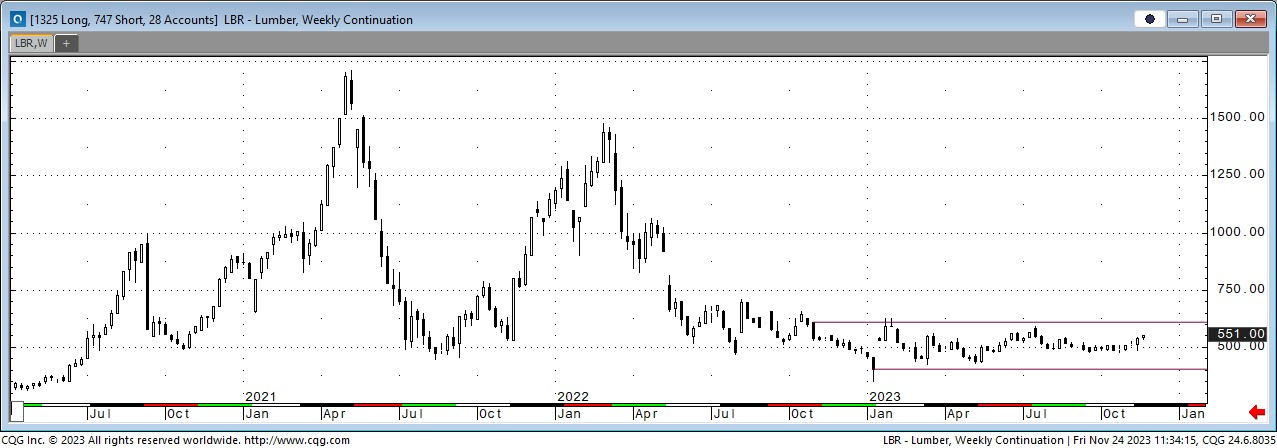

The lumber market today has three defined pillars. The first is supply and demand. The other is rates, and then there is inventory management attitudes. All are currently indicating more of the same for 2024. What could be different is inventory management.

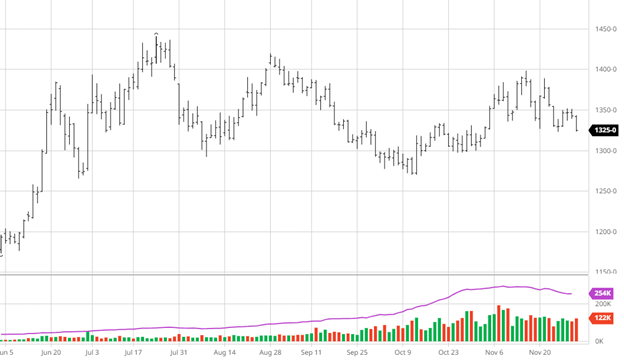

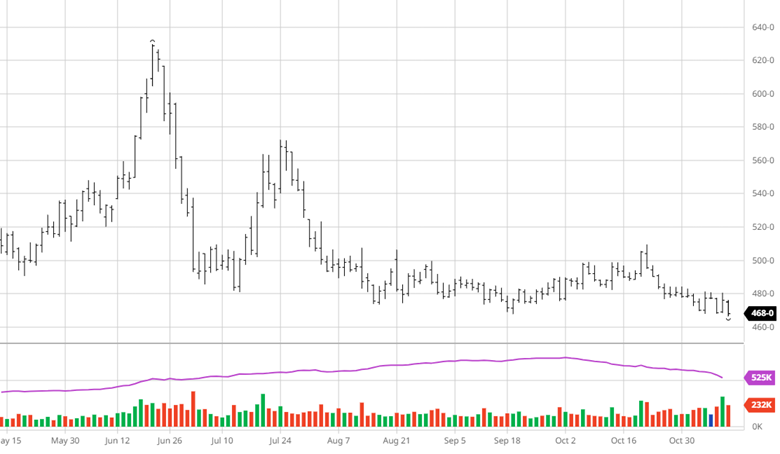

This past month we saw a much more robust buy round. There was a genuine attitude that buying cash at $370 or $375 held a low risk. We saw that again with the lack of hedging after a $50 run in futures. Most believed that inventory management was sufficient. Distribution and wholesalers want to hold more product. Contracts and VMI limit the availability of wood at any given time. The fact that the industry was able to have a good buy round indicates a shift at the mills to hold more wood. That is good for prices in a flat market. A Weyerhaeuser guy (Jay) always said that it is bullish when the mills control the wood. When they ship it to others it is bearish. Let’s see if that is the case next year.

Last week’s negative trade reflected the lack of hedging by the industry. The end-of-the-year timeframe is rough for those holding inventories. Another sloppy week is expected. The massive liquidation in the futures market takes it out of the game to help at this point.

Technical:

The futures market retraced 38% of the move last week. The 50% mark is 518.00 and the 61% is 509.70. All are in reach. What is a little more bullish is the fact that the lower Bollinger band sits at 520.50. It would take time and work to get that band to turn down. I am looking for a lower trade in January, but the timing may be closer to expiration.

Note: fund managers point to a possible shift in the fund makeup in lumber from short to long. Rates will control that conversation.

Note: the sleeper in this market is the monthly inventory of new homes available. This last number of 7.8 months is the highest we have seen in three years.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636

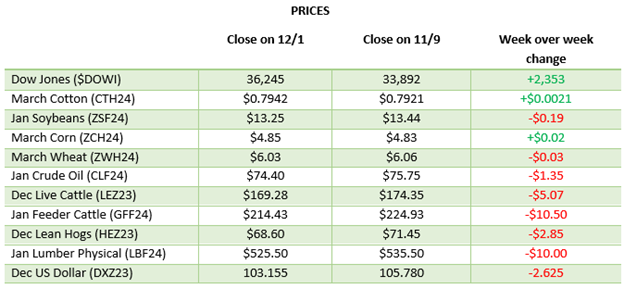

Soybeans have fallen over the last couple of weeks but is in a sideways trade in the big picture. Exports were not as strong as corn but better than expected. Brazil’s weather is the main focus for beans right now as the north is drier than normal and the south is still wet. The bean demand from China is welcome, as always, but sustained demand and not just demand while Brazil is having logistic issues will be important. The amount of rain in Brazil next week will be the main market mover until the report on Friday if we get some surprises.

Soybeans have fallen over the last couple of weeks but is in a sideways trade in the big picture. Exports were not as strong as corn but better than expected. Brazil’s weather is the main focus for beans right now as the north is drier than normal and the south is still wet. The bean demand from China is welcome, as always, but sustained demand and not just demand while Brazil is having logistic issues will be important. The amount of rain in Brazil next week will be the main market mover until the report on Friday if we get some surprises.