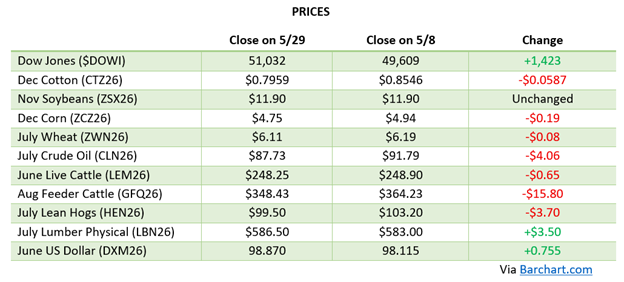

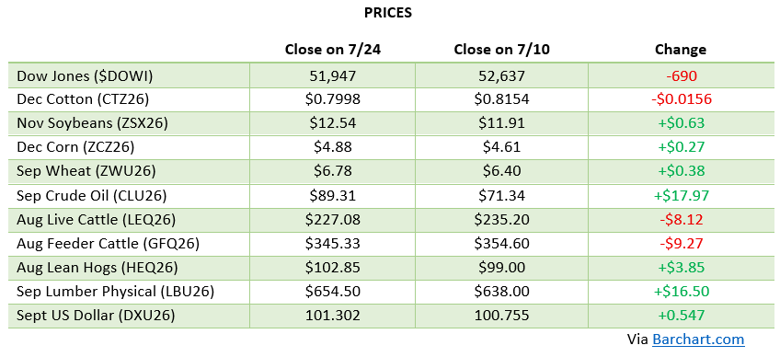

Corn caught a boost from the July 10th WASDE report, which cut 2026/27 ending stocks to 1.79 billion bushels, 200 million lower than June, on stronger-than-expected old-crop demand that trimmed 2025/26 carryout by 125 million bushels to 2.02 billion. Even with production pegged at a record 16.0 billion bushels, the tighter carryout was enough to spark buying, and December corn settled the WASDE session at $4.60. The rally extended over the following two weeks as a hot, dry pattern settled over the Corn Belt right through pollination, the most critical stretch for yield determination, with December corn touching $4.92 on July 24th, its highest intraday level since May 21st, before fading back into the $4.80s. Export demand has been the other pillar of support: 2025/26 corn sales commitments have already topped 3.41 billion bushels, up nearly 24% from a year ago and above USDA’s full-year forecast of 3.325 billion bushels, while 2026/27 bookings are running 12% ahead of last year’s pace. With the crop pushing through its most sensitive growth stage under some stress, and NASS heading into the field July 25th through August 5th for the first survey-based yield numbers of the season, weather will remain the dominant driver into the August 12th WASDE. Prices are lower to start the week of July 27th.

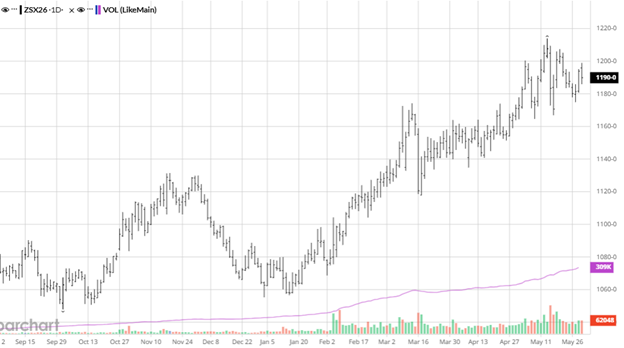

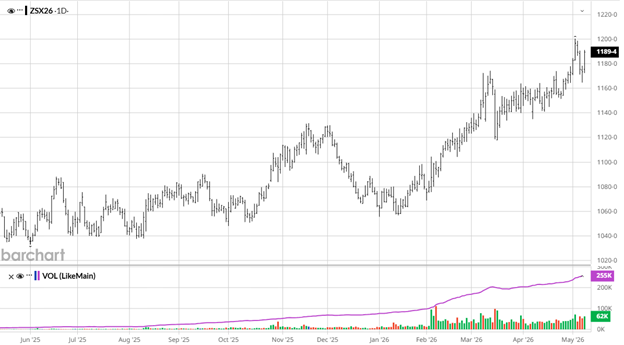

Soybeans got a mixed signal from the July WASDE: USDA raised 2026/27 production 40 million bushels to a record 4.475 billion on higher harvested acres, but a matching bump in exports left new-crop ending stocks unchanged at 310 million bushels, while old-crop 2025/26 carryout actually tightened another 10 million to 330 million bushels. Crush held steady at a record 2.75 billion bushels. New-crop November futures have been the standout performer of the period, climbing from the low-$12 area into the $12.40s-$12.50s by July 23rd-24th, territory not seen in a new-crop contract since December 2023, as the same hot, dry forecast pressuring corn is raising concerns about pod-setting and seed fill during this critical stretch. Chinese demand has quietly turned into a real tailwind rather than just a headline, China has been a steady buyer of new-crop beans in recent weeks, and traders are increasingly optimistic that the long-delayed Trump-Xi meeting, now being framed as a late-September event, could bring another leg of purchases. We are close to the point where it wouldn’t take much more than a one-bushel-per-acre yield hit to make U.S. supplies uncomfortably tight, so August weather is squarely in the driver’s seat.

Soybeans got a mixed signal from the July WASDE: USDA raised 2026/27 production 40 million bushels to a record 4.475 billion on higher harvested acres, but a matching bump in exports left new-crop ending stocks unchanged at 310 million bushels, while old-crop 2025/26 carryout actually tightened another 10 million to 330 million bushels. Crush held steady at a record 2.75 billion bushels. New-crop November futures have been the standout performer of the period, climbing from the low-$12 area into the $12.40s-$12.50s by July 23rd-24th, territory not seen in a new-crop contract since December 2023, as the same hot, dry forecast pressuring corn is raising concerns about pod-setting and seed fill during this critical stretch. Chinese demand has quietly turned into a real tailwind rather than just a headline, China has been a steady buyer of new-crop beans in recent weeks, and traders are increasingly optimistic that the long-delayed Trump-Xi meeting, now being framed as a late-September event, could bring another leg of purchases. We are close to the point where it wouldn’t take much more than a one-bushel-per-acre yield hit to make U.S. supplies uncomfortably tight, so August weather is squarely in the driver’s seat.

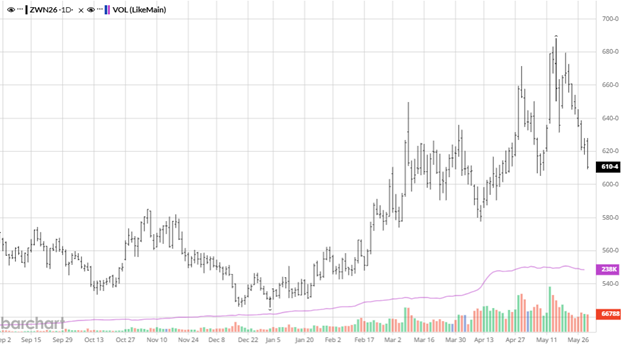

Wheat also caught a bid off the July 10th report, with USDA trimming its wheat production estimate again on continued winter wheat losses, winter wheat production is now seen at just 990.5 million bushels, a 29% drop from a year ago, while spring wheat is projected 4% lower at 475 million bushels, keeping this year’s crop firmly on track to be one of the smallest in decades. Ending stocks fell another 22 million bushels to 722 million on the news, and Chicago wheat jumped over 20 cents to settle at $6.40 that session. The complex has since given back some of those gains as harvest wraps up across the Southern Plains and the market digests early results from this year’s spring wheat crop tour, which came in below both last year’s yield and USDA’s most recent guess, though a bit better than the trade feared. Black Sea supply risk remains part of the backdrop, with Russian consultancy IKAR now pegging Russia’s 2026 crop at 90 million tonnes and export potential at 44.5 million tonnes, keeping traders wary of pricing U.S. wheat too far above what the world actually needs. Export demand has been unremarkable, with last week’s sales total of 10.7 million bushels falling below the four-week average, and the wheat market looks a bit overbought technically after its recent run.

Equity Markets

Equity markets pushed to fresh records early in the period, with the Dow topping 53,000 for the first time on July 6th and closing at 52,637 on July 10th, before the reignited Iran conflict and a wave of chip-sector weakness took some wind out of the rally. The Dow closed the week of July 24th at 51,947, still up more than 16% year-over-year, as investors weighed strong Big Tech earnings and continued AI-driven enthusiasm against renewed Middle East headline risk. Volatility has picked up as the market digests a heavy earnings calendar alongside the prospect that persistent inflation could push the Fed toward holding rates steady, or even hiking, rather than cutting further this year.

Energy Markets

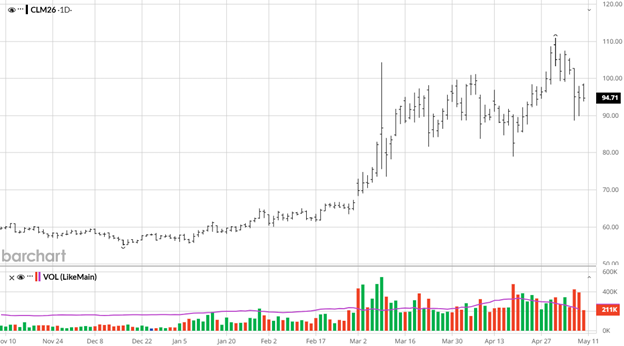

Energy markets were the most volatile corner of the entire complex over the past two weeks as the U.S.-Iran ceasefire that had briefly calmed prices in June completely unraveled. Iran’s attack on a tanker near the Strait of Hormuz on July 7th sent crude sharply higher, and the conflict escalated from there: U.S. forces have carried out repeated rounds of strikes on Iranian targets, Washington reinstated its naval blockade of Iranian ports, and Iran’s Houthi allies in Yemen declared a maritime embargo against Saudi Arabia. WTI crude has been on a wild ride as a result, swinging from the $70 handle in early July to the low-to-mid $80s at points last week, before easing modestly to close out the week as markets try to gauge whether the fighting stays contained. Some analysts now warn Brent could threaten its 2022 high near $128, or even the 2008 peak above $146, in a worst-case escalation scenario. For producers, this is the same fertilizer and diesel cost risk that flared up earlier this year resurfacing, and it is worth watching closely before locking in fall input needs.

Other News

– Cotton remains a standout, with December cotton settling above 81 cents on July 10th, continuing its run to multi-year highs as elevated crude prices keep synthetic fiber costs up and support natural fiber demand.

– China has been a consistent buyer of new-crop soybeans in recent weeks, and unknown-destination purchases announced late in the period are widely believed to be Chinese business ahead of the Trump-Xi meeting now being targeted for late September.

– USDA’s NASS will be in farmers’ fields conducting the first survey-based yield interviews of the season from July 25th through August 5th, setting up the August 12th WASDE as the next major acreage and yield-driven catalyst.

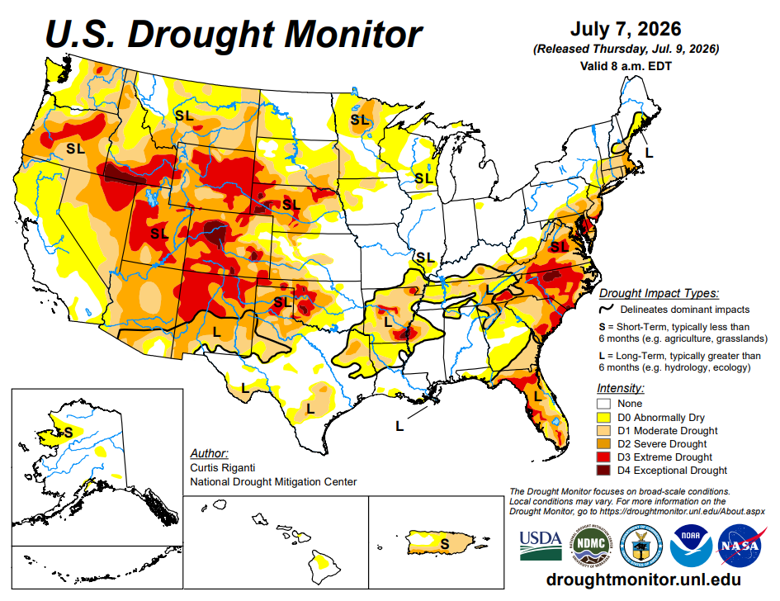

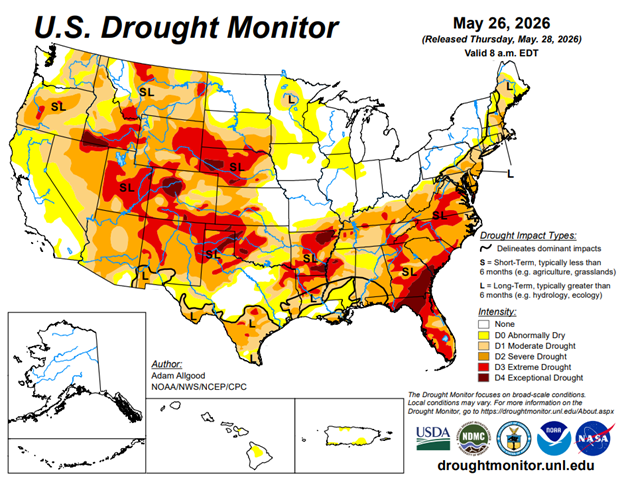

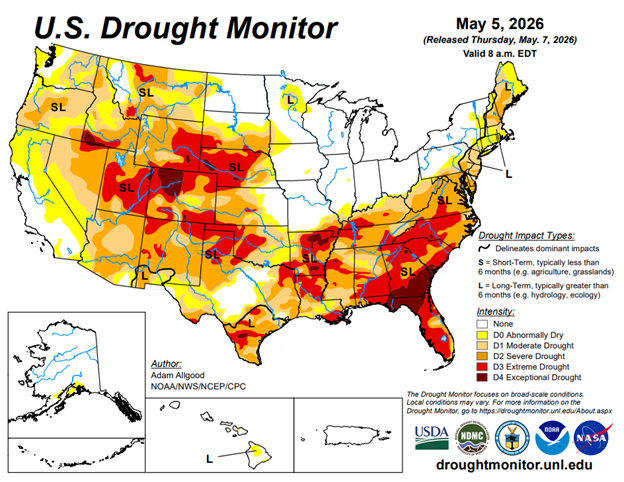

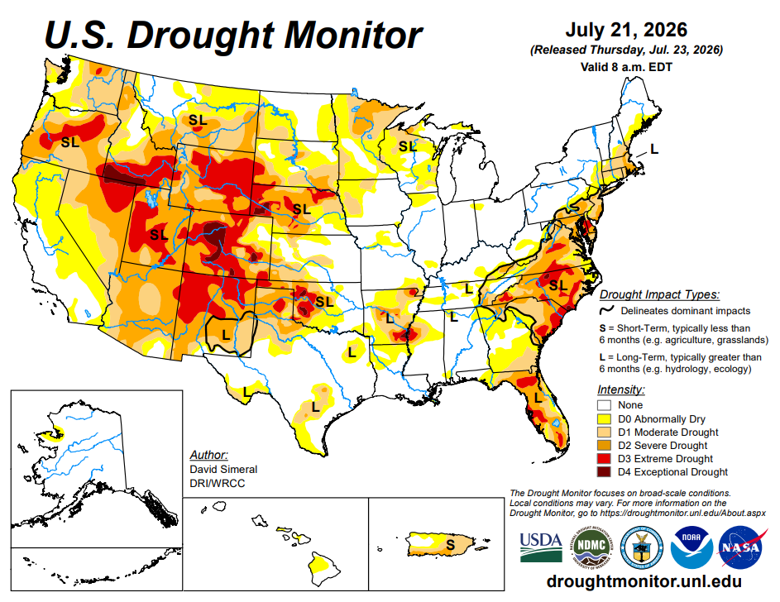

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers- Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.