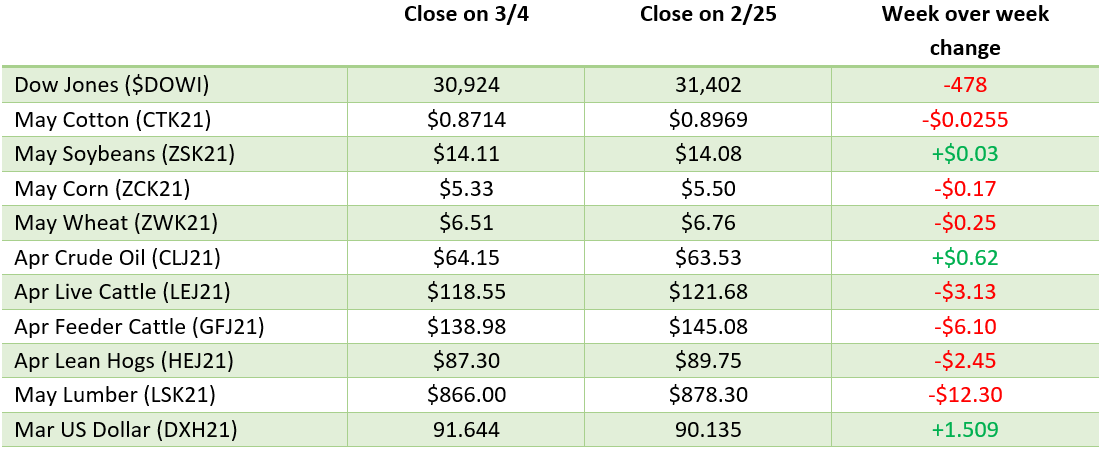

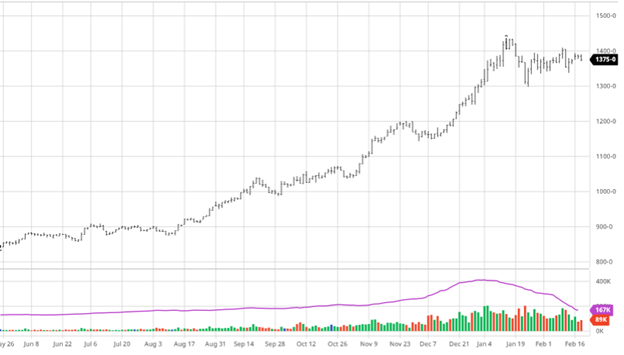

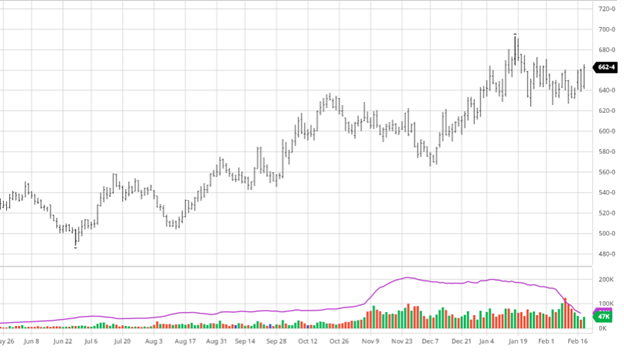

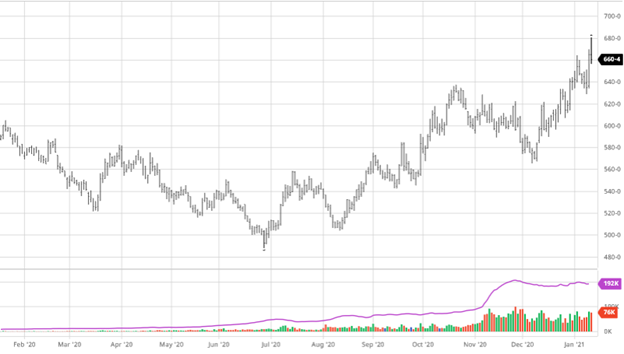

Corn had small gains on the week after continuing to trade in the recent range since leveling off at the start of February. Corn had strong exports and CONAB’s crop were both bullish factors supporting the market on Thursday. Rain expectations were added to later in March for Argentina but also added to northern Brazil in the short run. These expectations are continuing to put pressure on an already delayed harvest. Throughout the current bull run, Corn has managed to bounce when it tests the low end of its technical range. This is nice to see the support kicking in when there is both bearish and bullish news in the market. The March 31st Acreage and Stocks Report will have updates on every category and will set the stage for the trade’s expectations into the US growing season. The USDA will need to update their stocks in this report as exports have been ahead of their predicted pace for the year-to-date.

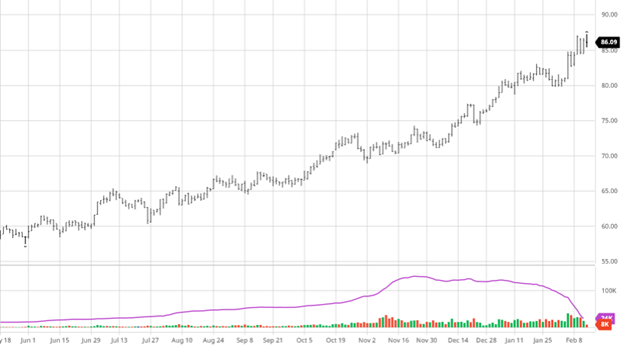

Via Barchart

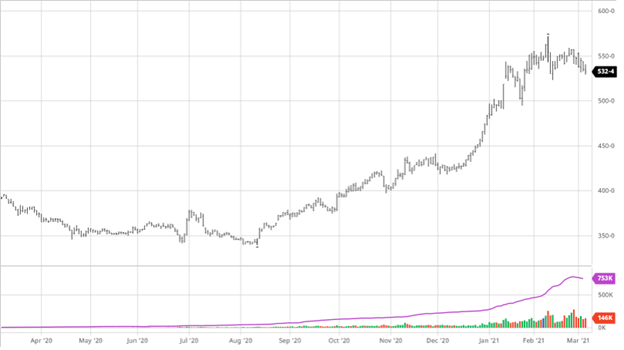

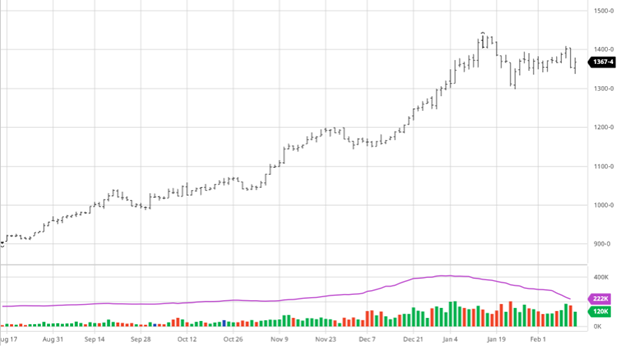

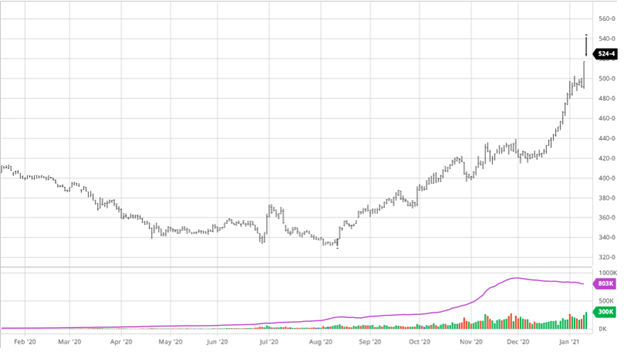

Soybeans made small gains on the week; albeit volatile, after falling from their contract highs at the start of the week. The continued ASF questions in China will hang around the market as bearish news until we get more concrete answers. South America has continued to struggle with its bean harvest and with more rain in the forecast for northern part of Brazil the struggles look to continue. Friday’s early pullback pushed beans below $14.00 on fund selling despite South America continuing to trim their expected yield. Beans are still trading within a wide range but still have a bullish chart even with the small pullback from contract highs this week. Continue to keep an eye on South American weather, exports, and ASF news as those will be the movers going into the March 31st acreage and stocks report.

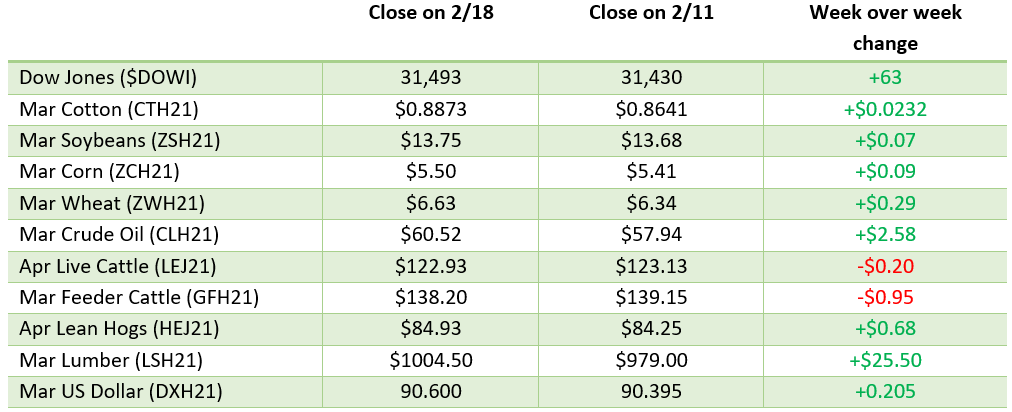

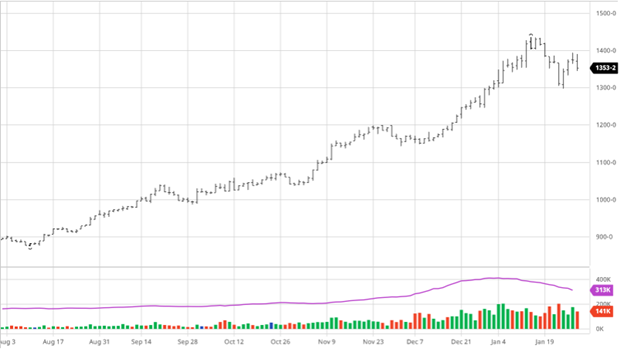

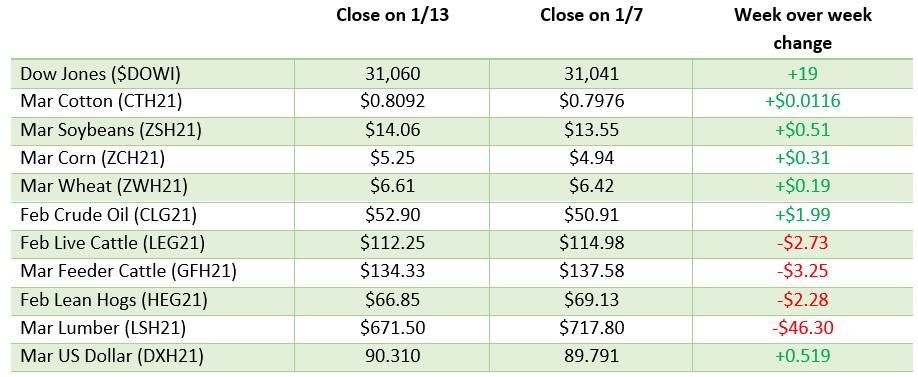

Dow Jones

The Dow had a strong bounce back week as President Biden and the Democrats passed a $1.9 trillion dollar stimulus bill and the continued news of states opening fully back up. Covid-19 vaccines continue to rollout and case numbers also continue to trend in the right direction which is positive for the economy and reopening efforts. The Nasdaq has also bounced back some this week after getting killed last week on rising interest rates as investors cycled out of tech.

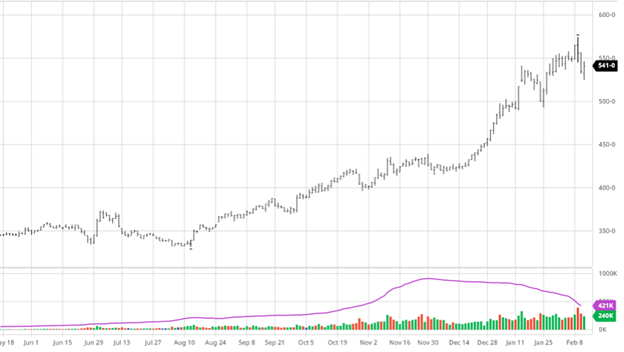

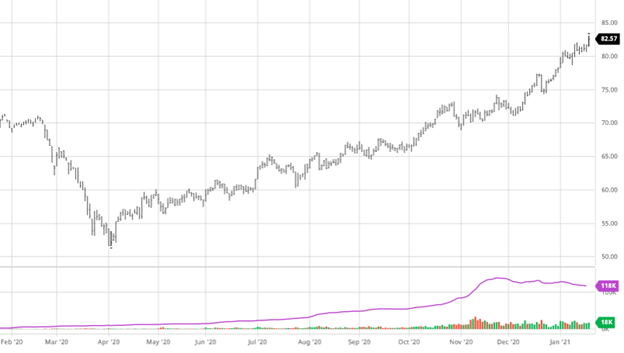

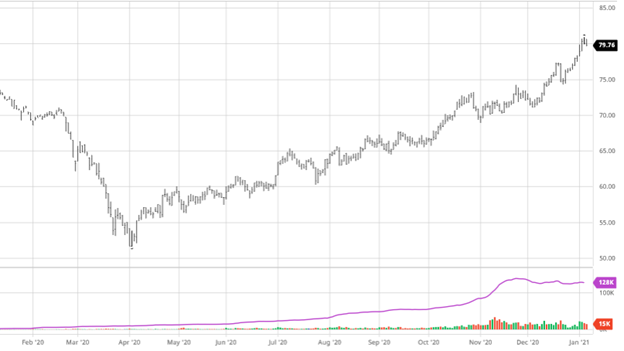

Cotton

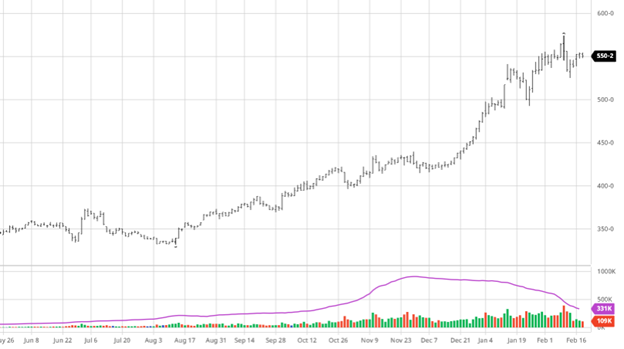

After falling hard last week cotton has been bouncing around making small gains on the week. Cotton, like other commodities, are being bought in greater quantities at higher prices which are signs of inflation starting at the start of the consumer cycle. Cotton demand around the world has slowly been rising as the world re-opens and consumers cant wear the same pair of sweatpants all week long everywhere.

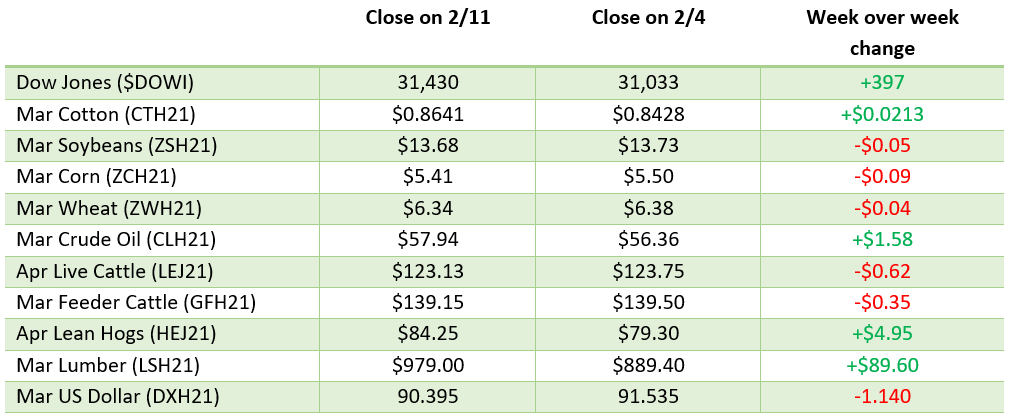

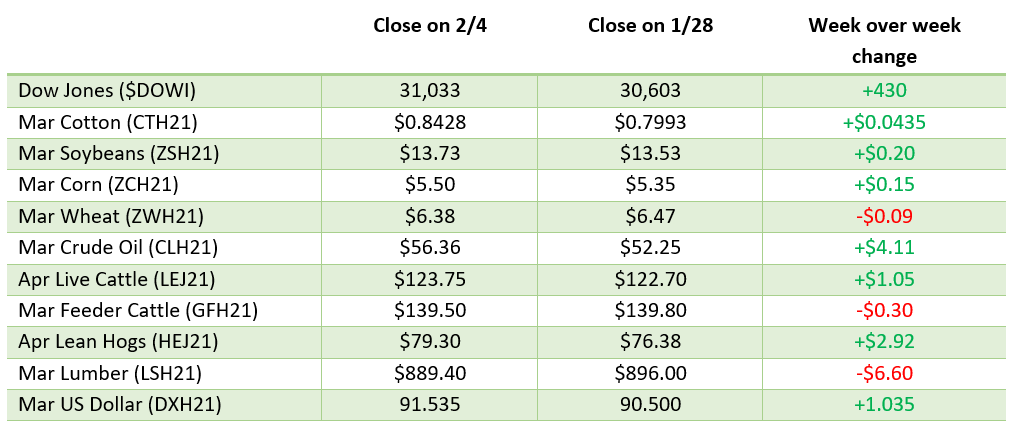

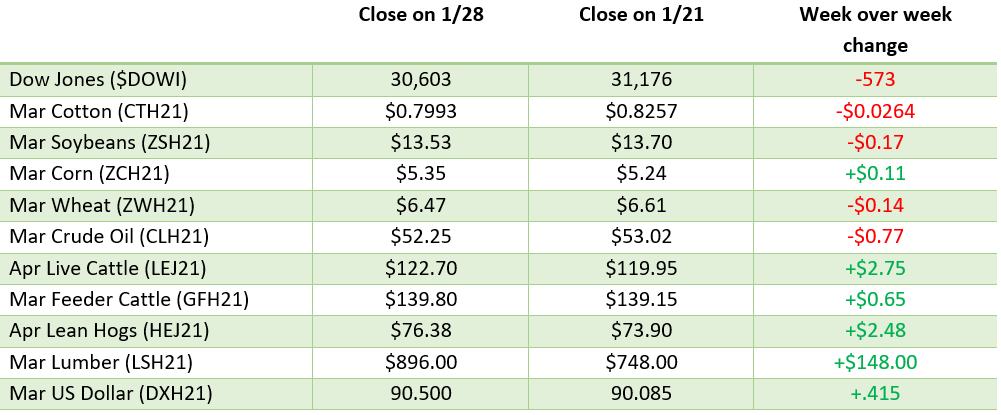

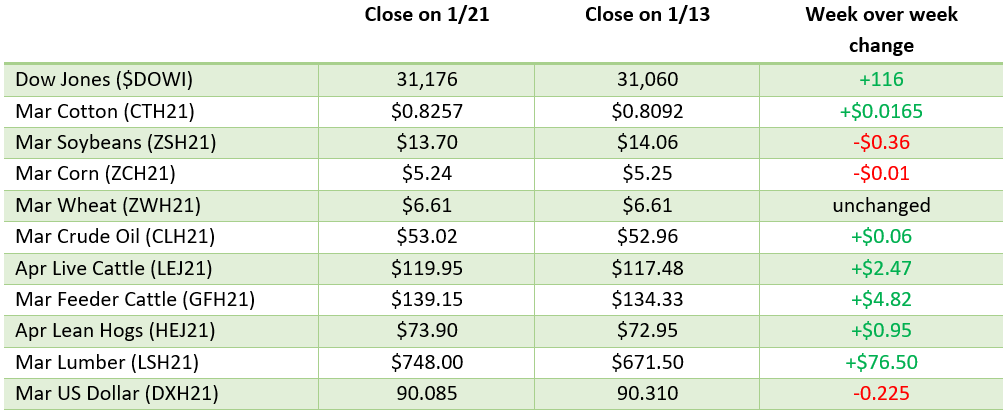

Weekly Prices

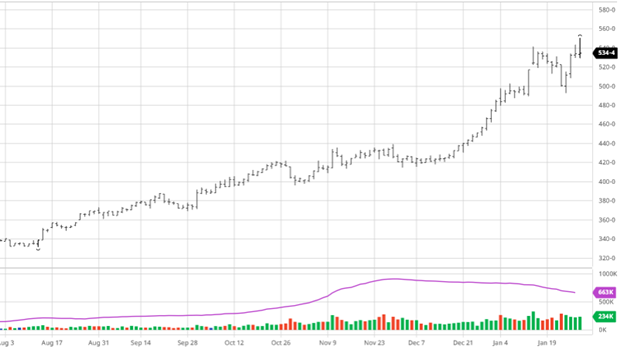

Via Barchart.com