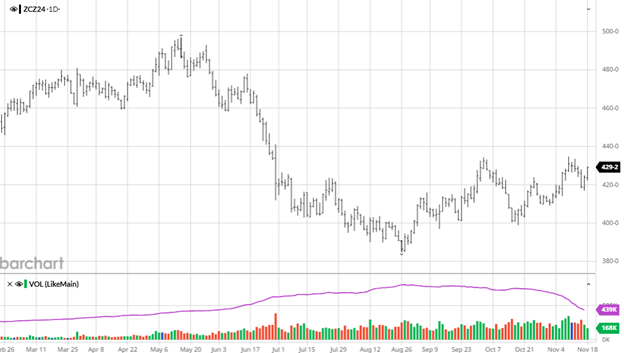

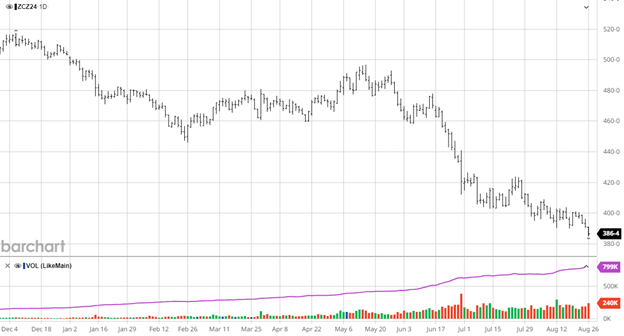

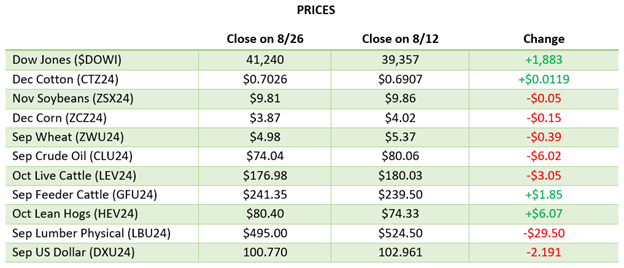

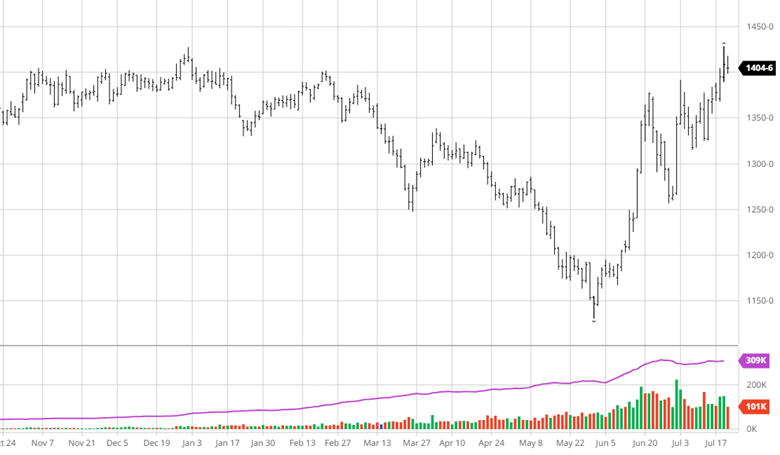

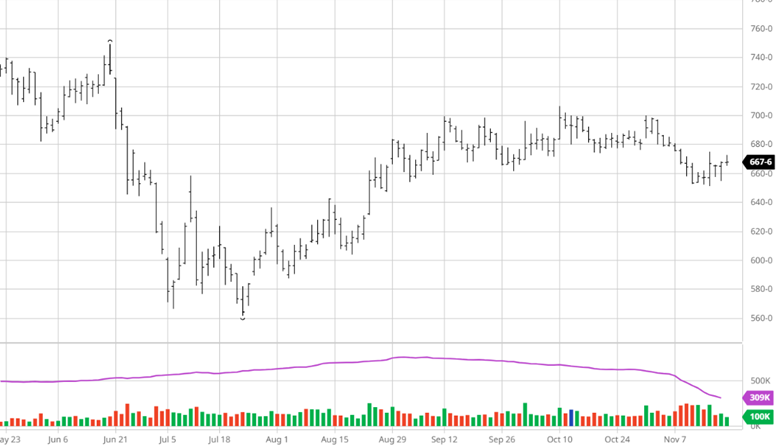

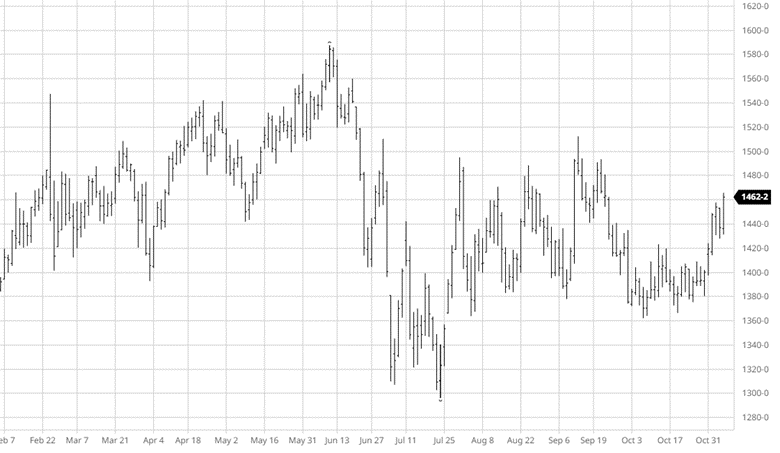

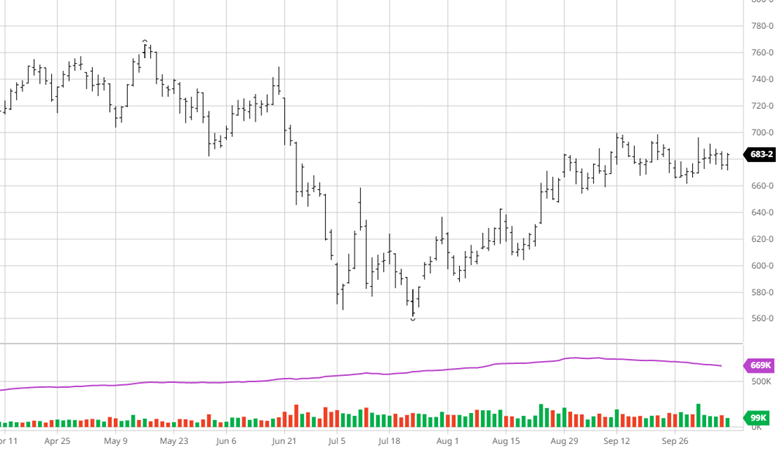

Corn prices have drifted lower since Mid-July with no major weather issues and no major trade deal news. The corn crop ratings remain strong with about 73% of the US crop rated good/excellent and slking and dough formation ahead of average. Exports have slowed and funds have kept their short position about even last week. With the recent heat dissipating giving way to a cooler week, this crop has not been made yet but has not faced any prolonged growth challenges which continues to fuel the estimates into the 184-185 bu/acre. While this will be an impressive crop, from talking to growers across the country there are trouble spots due to disease and timing of rains which would help us get back to the low 180s which would give the market a bump. The market has been limping lower and will likely continue until something in the news cycle changes.

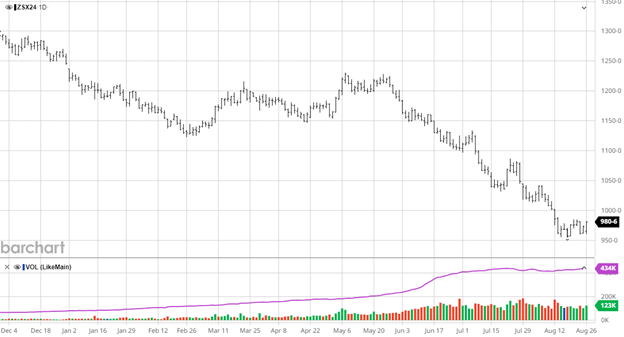

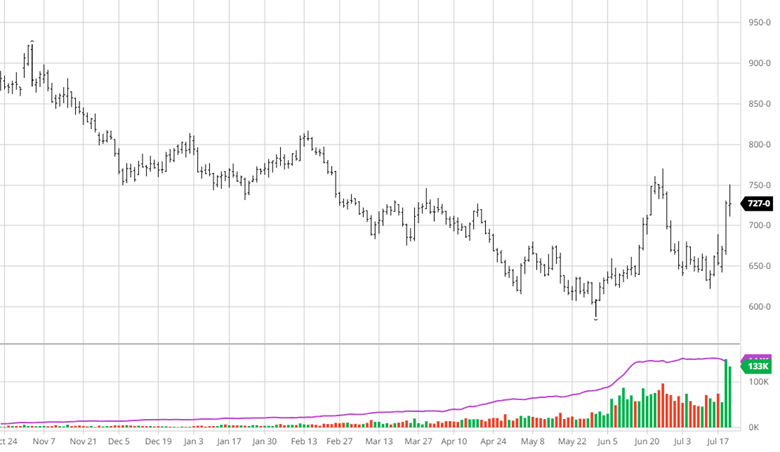

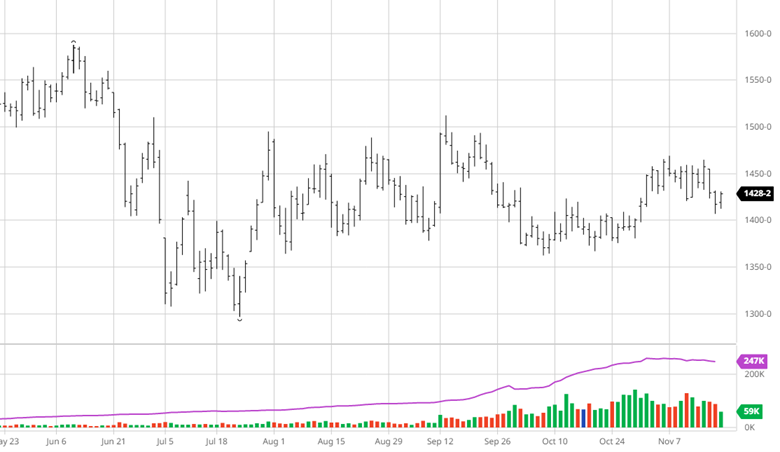

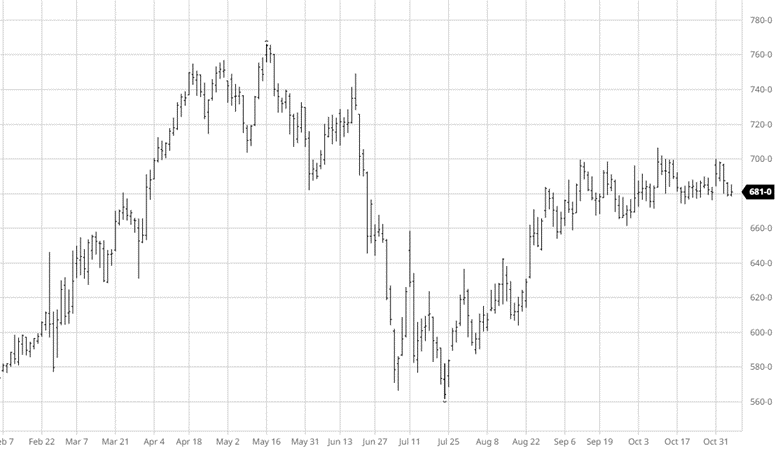

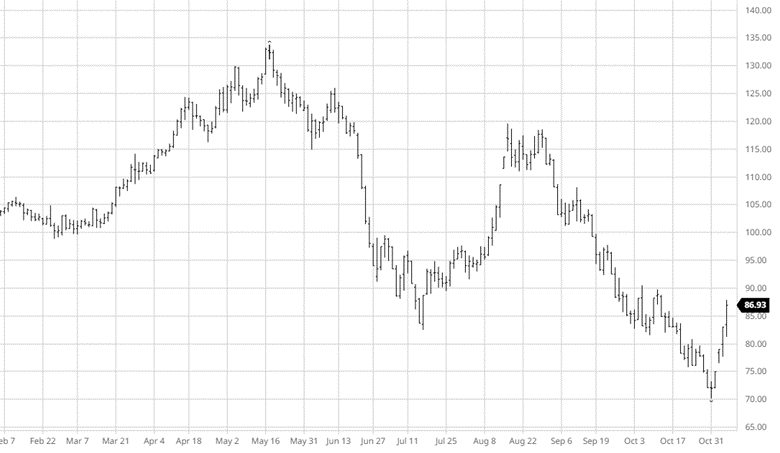

Soybeans have struggled lately as there has not been any news to boost the market. Exports this week were better but until China shows up as a buyer the demand for US beans is struggling on the global market. South America had a strong crop giving China more supply to buy so China may not show up until they have to unless prices fall enough to make them step in. Crop ratings remain strong, but the next month of rain will be important for pod filling and to get the crop across the finish line.

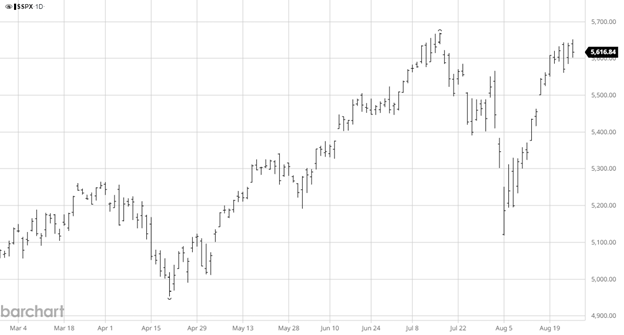

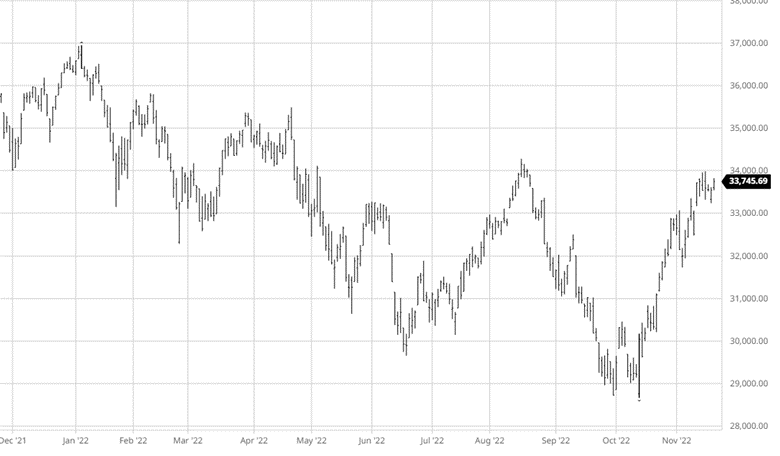

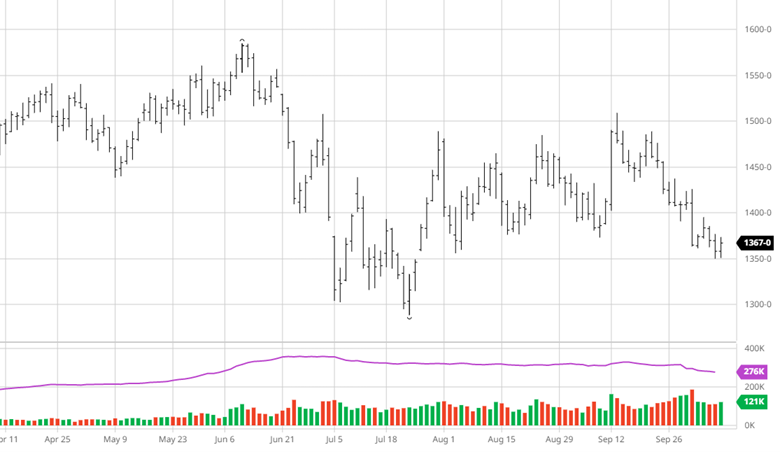

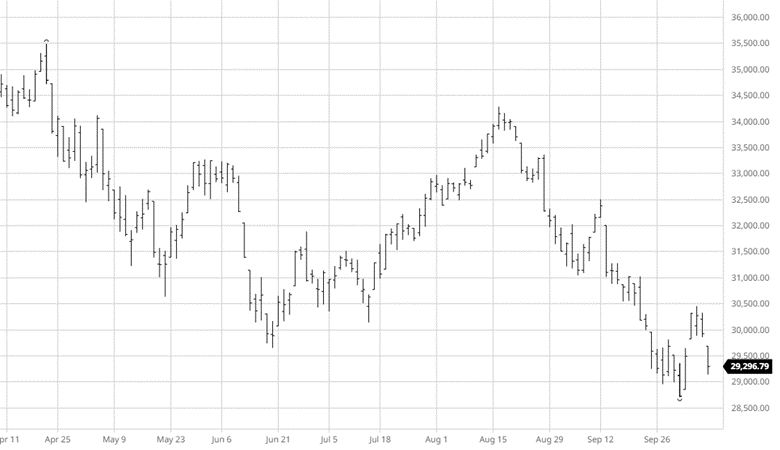

Equity Markets

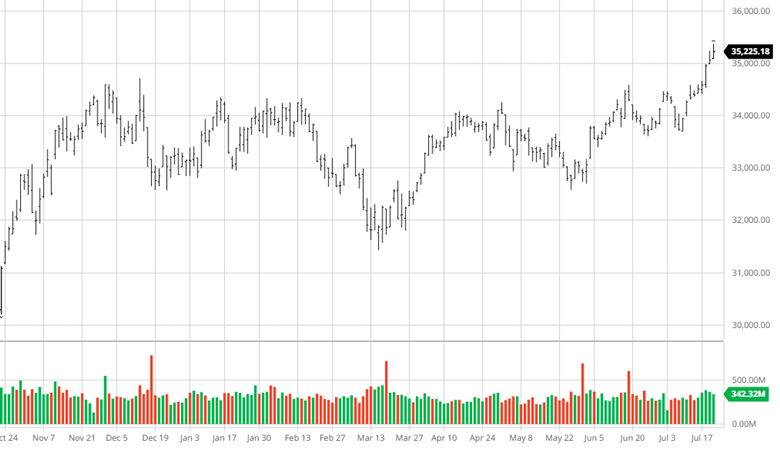

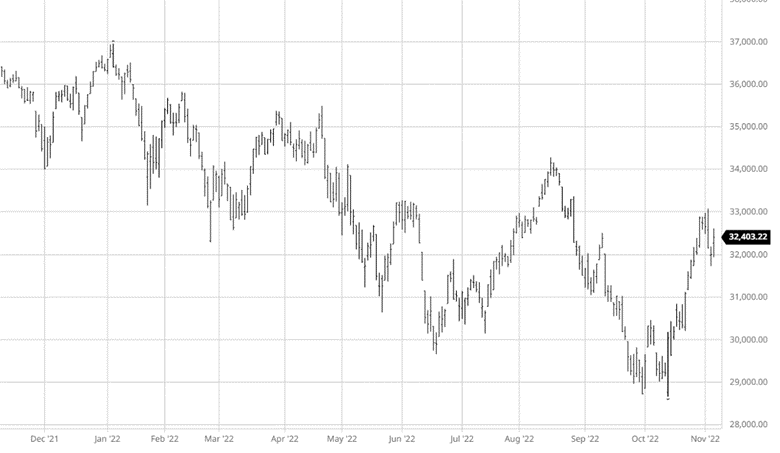

Equity markets continued to reach new highs before a sizeable pullback to end last week with the news of Trump firing the head of the BLS. AI and tech names continue to lead the way. Magnificent 7 stocks have had mixed reactions to earnings but nobody is sounding the alarm yet about tariffs as guidance remains steady.

Other News

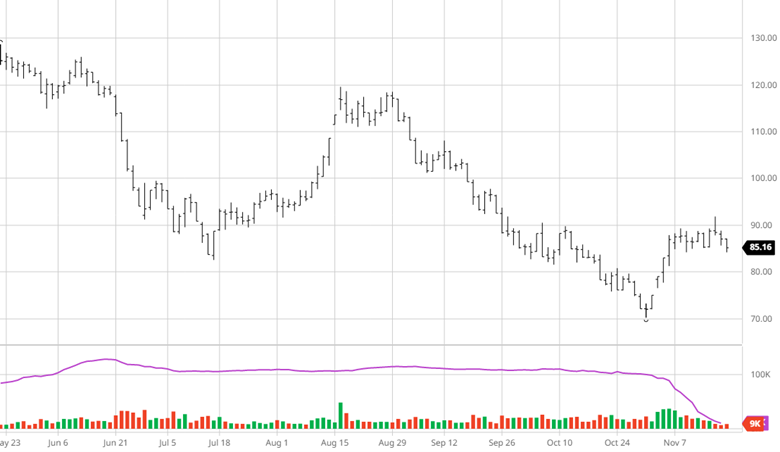

- Wheat has limped lower with corn and beans but saw good exports this week amid Ukraine’s sluggish exports.

- The USD has strengthened in the last week but is still well below its year high. Historically this would have been supportive of agriculture exports but there are other factors in play this year.

- The August WASDE report should provide some clarity and at least provide some new news for the market to digest and trade on for a bit.

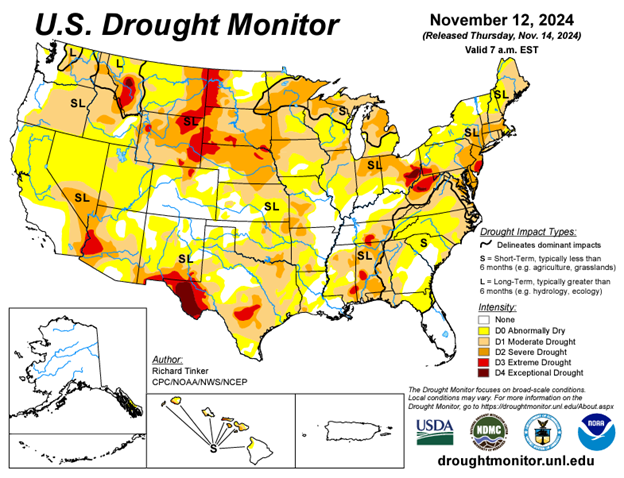

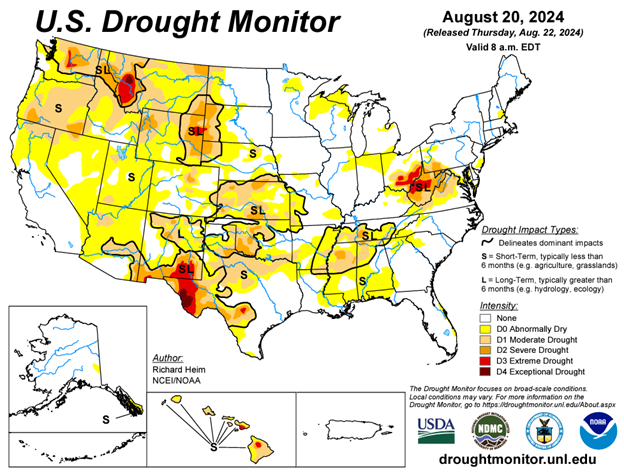

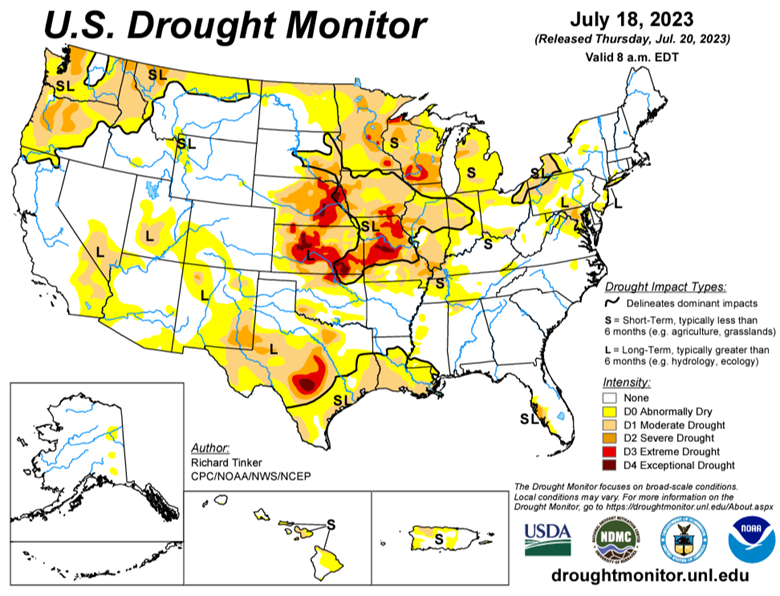

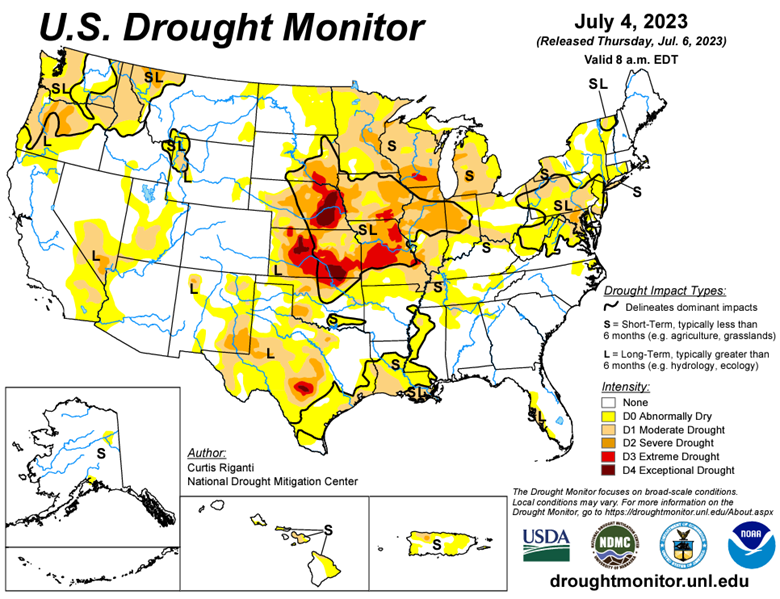

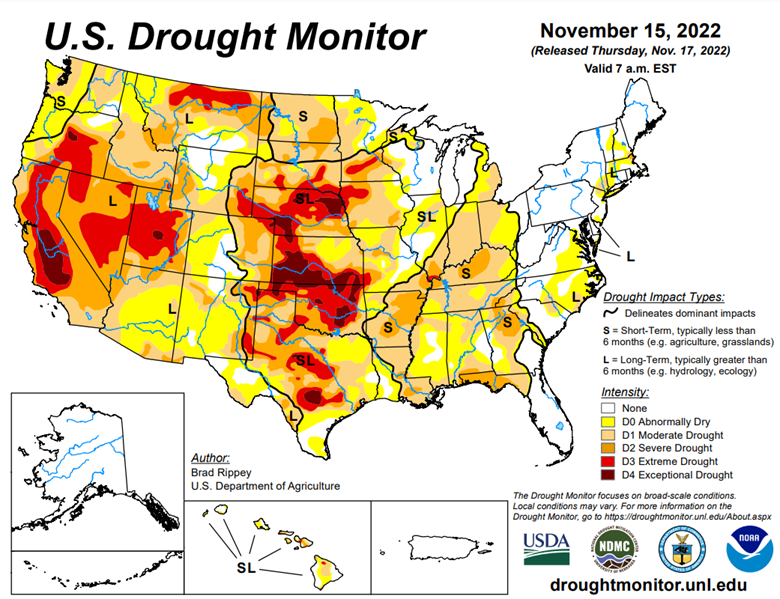

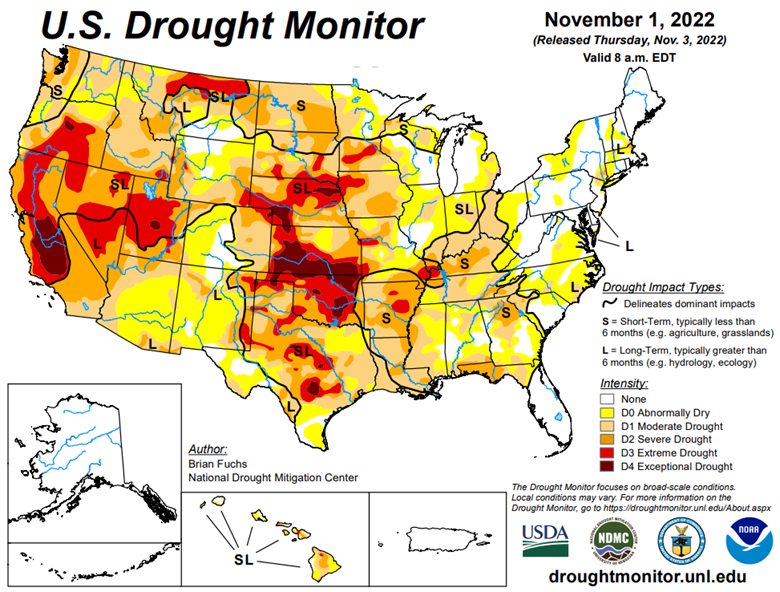

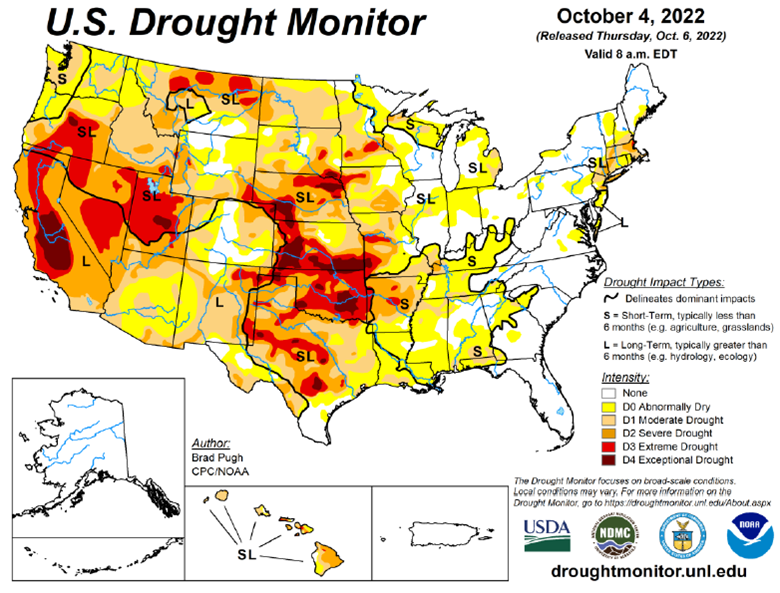

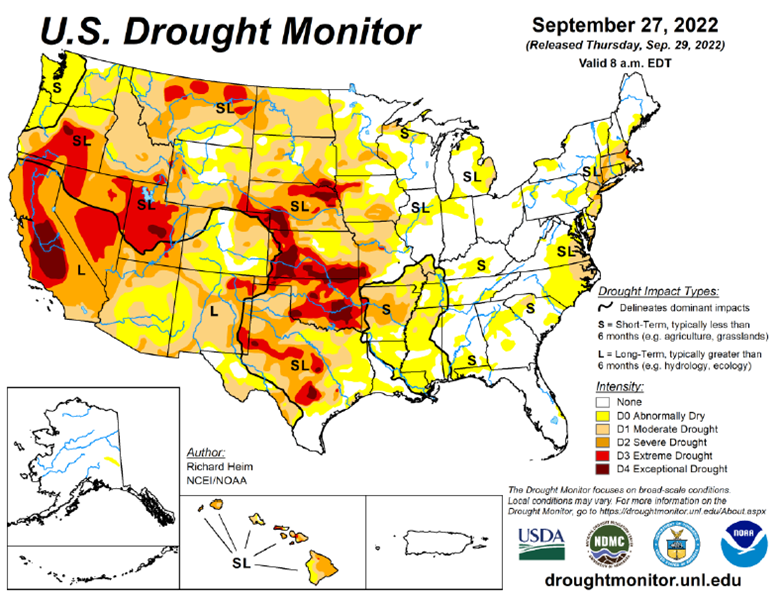

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.