In this episode of The Hedged Edge, hosts Jeff Eizenberg and Ben Hetzel dive deep into the heart of agricultural markets with special guest Fred Seamon from CME Group. As harvest challenges mount with record-breaking rainfall across the Midwest, the conversation spans centuries of market innovation—from the early days of Chicago’s grain trade to cutting-edge futures contracts. Fred shares fascinating insights into the historical development of commodity exchanges, explaining how farmers went from local merchants to global market participants.

The discussion explores critical topics including harvest logistics, railroad transportation, the evolving role of the USDA, and emerging market tools like the new fertilizer futures contract. Listeners will gain a rich understanding of how technological advances and market innovations continue to transform risk management for producers. Whether you’re a farmer, trader, or agricultural enthusiast, this episode offers a comprehensive look at the complex ecosystem of agricultural markets, blending historical perspective with forward-looking analysis.

Packed with expert commentary, practical insights, and a touch of humor, this episode is a must-listen for anyone interested in understanding the intricate world of commodity trading and agricultural economics.

_____________________________________

_____________________________________

Listen on the radio at KNDC Radio https://www.kndcradio.com/

and KBJM Radio https://kbjm.com/

Check out the complete Transcript from our latest podcast below:

Harvest, Hedging, and History: Navigating Agricultural Markets from Grain Elevators to Futures Contracts

Jeff Eizenberg 00:57

Welcome to the next episode of The hedged edge. I’m your host, Jeff Eisenberg, and I’m here with my co host, Ben Hetzel. Ben, it’s almost big game season, and we’re talking waterfowl. What’s been going on? You get out any hunting yet?

Ben Hetzel 01:12

No, I haven’t. My my boys like to shoot some birds. I don’t mind going out a little bit. I much prefer to shoot the clay version, because I don’t know, I just, for some reason, I’ve always kind of grown up with the idea that if you’re gonna hunt

Speaker 1 01:28

wildlife, you have to be willing to eat the wild game that you hunt.

Ben Hetzel 01:33

And I’ve never been a real big fan of game bird, so I didn’t, we didn’t shoot a lot of them when I was a kid. So, but my boys like to hunt, and it’s a lot of our family hunts, so it’s, it’s just good to get out. But yeah, we’re coming up on, there’s, there’s tons of people out there along the roads, and sometimes not the safest practices going on with vehicles on these country roads. But definitely got bird season going on and and big games coming right around the corner, and that’s kind of what we do. We we enjoy that a little more, I’d say. So we’re excited.

Jeff Eizenberg 02:12

That’s good. Now, with all the weather we’ve had all the wet, rain and whatnot, that’s good for birds. Yeah,

Ben Hetzel 02:19

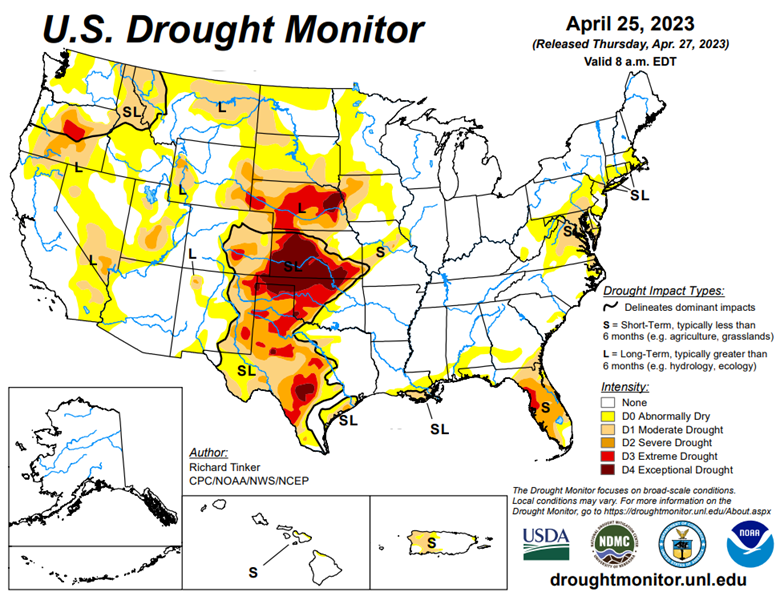

I mean, it’s, probably all right. In general, it’s good to have moisture versus drought, obviously, and it’s been crazy. I’d say this year has got to be right up there with a record for a lot of places. I hear producers talk across the trade area that they are at record levels. And when you have thunderstorms, they vary and that sort of thing. But it’s been an unbelievably wet year for this trade area, Southwest, North Dakota, Northwest South Dakota. I seen a visual on kind of the percentile, and we’re at like 150% to normal, is what our little area of the world showed, particularly right around where I live, near London, and so yeah, it’s, it’s good, but yet challenging at times. Harvest is slow to come off. These row crops are ready in a lot of areas, and harvest is definitely moving forward, but we see fields that are ready to be cut, fields that are cut. So it’s, we’re in the midst, and I know a lot of guys are anxious to get get everything out of those fields, especially when you got you know, we’ve had some high winds, 60 mile an hour us, and so guys are nervous about some of these row crops starting fall down or whatever it is. But again, the wildlife sure enjoy that cover. So more harvest that gets done makes it easier on the deer and antelope hunters, but it’s that season. Yep.

Jeff Eizenberg 03:52

And speaking of harvest, where, where are we in the process now, from the elevators perspective, you guys filling up, starting to put up any grain piles? What’s it look like as you’re driving around?

Ben Hetzel 04:04

I don’t see too many piles. You know, out here, we do a lot of grain bagging, past how that’s managed. Wildlife can be a challenge, especially in a wet year. No, you were curious of how that all kind of works. But for the most part, the bags are fine, unless wildlife get on them and start popping holes in them and then have some serious problems. But a lot of people manage them real close. Now, you know, there’s been some train wrecks on bags, but, yeah, it’s, there’s a there’s a fair amount of bags around, and guys were moving a little bit of small grain. A lot of canola has been moved. So I think there’s places to go with some of this row crop harvest, but we’re getting pressure all the time to continue to make space, pretty hard to keep the flax and the peas and the canola and the wheat, all that stuff moving because they want to try to market their corn and. And some fires as well. And so it’s been a real battle. Railroads kind of slipped a little bit. It’s gotten a little bit late on placements, so that’s a challenge as well. But it hadn’t been too bad, and I wouldn’t say we’re way behind. You know, seasonally, it’s not uncommon to expect some delays, but it’s it’s starting to show up a little bit more now, as corn harvest is ramping up in the east and and on the railroads defense, this soybean crop didn’t move like normal it was a non traditional flow for them, and so that they actually, I think, adjusted about as well as you could ever expect a large organization to shift their assets, and fortunately, it’s a smooth move to the Gulf. It’s not quite as smooth for us up here as going to the P and W, but that flow isn’t a bad flow, and so the railroad can do it fairly efficiently. And so that’s a positive. Unlike the Mexico market, where we can bottleneck the border and some of that stuff, and there is, there’s some congestion going on there. We’re hearing trains are getting held up across the border, slow to come back out, and so that is affecting some of this. But that’s just a volume issue, which is good. I mean, Mexico has been a great trade partner. We’ve talked about it on our podcast. People that tuned in to one of our earlier shows learned a lot about what’s going on with US and Mexico, and I think that’s key going forward still. But, you know, maybe we’ll get into a little bit of it today, on the rest of the world and what’s going on. There’s lots of news this last week that kind of rocked the market. China’s still obviously a big topic. So if

Speaker 2 06:52

you want to listen back to this episode or find past episodes of The hedged edge, visit kbjm.com or kndc radio.com under Listen Live and podcast options, or either station’s free mobile app under podcasts.

Jeff Eizenberg 07:08

Yeah, that’s a great segue. And yeah, I’m excited here today, we’re going to bring on a special guest that’s got a ton of history and experience in the markets, and take a look back in memory lane and understand what the importance is of the exchange, is how the exchange ultimately helps us to manage risk, and a lot of that comes down to understanding the history and how things flow, how trade flows, and how traders are able to manage some of the things you just talked about, people Bringing more crop to town than possibly in years past. How the rail systems could potentially slow down movement of grain from Southwest North Dakota down through to the Gulf, etc. So with that, we’ll take a minute here and introduce our guests. We have Fred Seaman joining us from the CME Group. Fred is with us, right out of Chicago, been part of the exchange for the last nearly 25 years. So welcome Fred.

Fred Seamon 08:08

Thank you, Jeff. Much appreciated. Really glad to be here.

Jeff Eizenberg 08:13

No thanks for jumping on this exciting for me, you and I basically have been involved in Chicago markets about the same amount of time you’re saying 2001 for you, I started out working at the Board of Trade, and in 2000 you know, our paths have kind of meandered, but we’ve never crossed until today. So this is exciting.

Fred Seamon 08:35

It’s amazing that we haven’t, but I did. I started in late 2001 and had been teaching at the University of Wyoming, so it was quite a change for me and my wife, but definitely haven’t looked back. It’s been the best job I’ve ever had by far.

Jeff Eizenberg 08:53

Yeah, you can’t beat the exchanges. The history goes back over. I think, I believe, 150 years, you know, the way in which they started out being Chicago, the center of the agricultural world, and the river and the rail all coming in, and now, now today, to be the place where innovation is happening, left and right. You know, the the thing that stands out to me, I think people miss and I always ask farmers that I meet, I ask elevator operators that I meet. Have you been to Chicago and have you seen the exchanges? And unfortunately, they transitioned away in our career, time from the pit traded. But I would love for you to help everyone remember the the training coats, the greens, the yellows, the blues, kind of the vibe that Chicago used to have.

Fred Seamon 09:46

I’m so glad that I got to witness peak four before, you know, it started to decline. And you know that did occur during my my tenure at the exchange. I. And, you know, it’s, it’s, it’s all electronic now, but you know that was, we got into a commodity boom in the, you know, early and mid, 2000s and you know, you would get really, really busy days. And I would hear from merchandisers, you know that, you know, they would, it would take some period of time before they would get confirmation on fills. So as efficient as the floor was, and it was extremely efficient, there’s a lot of things the floor did really, really well, but the markets had just grown to a point where, you know, the electronic screen just became, you know, the choice when, when we did start having daytime, electronic trade, the choice of most agricultural traders, and it started to to evolve away from the floor. But, you know, a lot of what happened on that floor is still relevant today. It’s just how we manage, you know, and how people enter and execute trades has changed. That’s all. But the underlying reason for them, the markets are still the same.

Jeff Eizenberg 11:10

Yeah, that’s That’s right. It’s a place to discover price and also manage risk. And the reality that the hedging community is what the exchanges were built for. Is so important for people understand it was built for hedgers, the speculators came in to provide liquidity. And today it’s a global marketplace that trades 24, six, effective, yeah. Well,

Fred Seamon 11:37

you know, it started as a spot market. If you go back into the 1840s you know what happened is, you know, everyone knows the US started 13 original colonies on the east coast. But as it started to expand westward, it didn’t take farmers long to recognize that they would rather farm ground in places like Ohio and Indiana and Illinois than they would Massachusetts and New York. So agricultural production moved westward, but most of the people were still in the east. So at harvest, you know, you’d have all these farmers bringing all of this grain into the major cities, Chicago, being one of them. And you know, they would try to find a merchant who was willing to buy their grain to, you know, arrange for it to be shipped back to the east where it would be consumed. And you know, some of those merchants were legitimate, some probably not. And you know, the the idea, did all producers get equal treatment? Well, probably not. So the exchange actually started. Well, there’s a few things. You know, the Board of Trade was a an organization that was started to promote commerce in the city of Chicago, and grain trade was one of those things. So, you know, their their first idea was just, let’s have merchant members, and let’s have them congregate in one place, and then, you know, a farmer can come to that one place, the members have been vetted, so, you know, hopefully they’re all legitimate, and something that we take for granted, but was real powerful at the time, was every time there was a transaction, they would post the price, so that the next farmer that came along probably wouldn’t receive the Same price, but would get an idea of the value of what they were, you know, selling, and that was the start of the exchange. It was just a spot market. Need to fall from there, eventually becoming forward contracts, and ultimately futures contracts in the 1860s that didn’t ultimately succeed, but corn, wheat and oak futures all launched on January 2. 1877 have existed continually since. It’s

Jeff Eizenberg 14:17

quite the history it is.

Ben Hetzel 14:19

It’s really kind of wild when you think about farmers and ranchers moving their goods far as they did. You know, I’ve got my aunt was going through the attic of the farmhouse where my grandparents lived for all my life anyway, and most of my mom and her siblings, but they found boxes of old receipts or tickets from when they would haul calves down to Sioux Falls, South Dakota. And mean to drive that today is a trek. I mean, it’s a six and a half hour drive. And to think back then they loaded their calves up and. The wagons and shipped them down there, or they took them in when the railroad came through, they took them in and put them on the rail and down there and sold them. And it’s just crazy to think of the dollars that they were transacting compared to what we’re transacting today. And of course, was cattle at all time highs. It’s just unbelievable. That journey that them, people went on to move that grain or those cattle was remarkable,

Fred Seamon 15:28

absolutely remarkable. And one of the things, Jeff, I think you, you mentioned, was about innovation and the farmers, indeed, the effort that they took to bring grain into the city, and then, you know, you got the railroads and so forth. And that certainly evolved. But, you know, transportation into the major merchandising points. But a couple of the innovations that occurred at the exchange early that we again take for granted, but it just completely revolutionized how grain was traded. Two of them were a system of grades and sampling. There wasn’t a USDA then, so a way to be able to differentiate grain so that it could be commingled in a grain elevator. And the first grain elevator in Chicago was was built in the late 1830s so the ability to commingle grain, and then the idea of receding grain within a facility, so that you could trade grain among multiple parties without it having to move to the multiple parties. It could just sit in one location, and you could just trade ownership of it. And that really revolutionized grain trade. And actually the center of grain trade in the Midwest. US moved from St Louis to Chicago because of those, those innovations, I

Jeff Eizenberg 17:08

think that’s really important for people to understand, is that the exchange has continued to evolve to support the farming community. It’s something that has been exciting the whole way through that, the point then became the delivery mechanism, right? Because that, I also believe is important to have multiple delivery points, of which the grade and quality is standardized. Was that the exchange that drove that? Or how did that come about?

Fred Seamon 17:35

They did and of course, there’s some great stories of shenanigans that went on along with that. But, yeah, a system of grades and a system of grading as well. But as you can imagine, when you know the Registrar of the exchange, the person that’s signing their checks, is a member of the change that also runs a grain elevator at the same time. There could be, from time to time, pressure on that exchange staff member to, you know, look one way or another when it came to grading grain. So at some point, the state of Illinois stepped in and said, enough of the shenanigans. We’re taking over. And those processes have existed at the government level, rather than the exchange level, for most of our existence. But did start at the exchange that’s

Ben Hetzel 18:39

kind of wild, because you’re talking like 1830 in the USDA started 1860 or Yeah?

Fred Seamon 18:47

Is that? Yeah? I think, I think that’s right. And it’s interesting. It was the 1860s when the state of Illinois took over inspection. So that was part of the learning process as things move from exchange regulated to state regulation and making it sound like the board was the Wild West. In some ways it was. But what they did and how, you know, they brought about organized trade. It definitely was a positive. You just anytime you have human beings and trade, there’s always going to be those few that are going to be looking for ways to benefit. So there definitely were some shenanigans.

Speaker 2 19:40

Want more agricultural market expertise. Listen to full episodes of the hedge edge podcast wherever you get your podcasts, or visit RCM, ag services.com get the complete market analysis and strategies you need to succeed.

Ben Hetzel 19:57

You can a wild west. Jeff, you’re I know you’re. Dying to jump on this. We have no government. USDA is not giving out reports.

Jeff Eizenberg 20:05

That’s right, that’s right. Ben, and that’s the part that he’s mentioned, the USDA didn’t exist back when the exchange started. The USDA effectively doesn’t exist today, because we don’t have a government operationally. And so you start to ask yourselves, the question is, how are we going to advance the needs that we have today for information without the USDA? And I’m going to go ahead and pose the question, do we even need the USDA anymore? After you know the innovation that could potentially happen as a

Fred Seamon 20:39

result. As of right now, we do, especially on the livestock side, feeder cattle is settled to our feeder cattle index, which is all based on USDA reported feeder cattle sales in the country and direct reports. We also use USDA reports for doing differentials in live cattle deliveries and lean hogs and pork cut out is all under mandatory price reporting. So one of the big things when you see a government shutdown coming, you know we always want to know is, is AMS market reporting going to be affected or not? And some of this, the shutdowns, they’ve been considered non essential, and those reports didn’t come out, and the exchange had nothing to to settle against. And other times they were deemed essential, and the reports continued to flow. Luckily, this time, the reports continued to flow at this point, so we haven’t had an adverse effect. And then on the grain side, you know, just having USDA price reporting adds additional trans transparency in the countryside relative to Chicago. So I think, you know, that’s a benefit to all. But, yeah, I mean that it’s we still rely pretty heavily on USDA, whether it’s for livestock settlements or for transparency when it comes to grains and oil seeds, and I should mention dairy too, that all is USDA based reporting as well. So we’d hate to see USDA go

Jeff Eizenberg 22:37

anywhere. Okay, so we’ll give them a break. They need to exist. Let’s get this government shut down, taken care of, and get these people back to work. Shifting gears a little bit, though, but similar topic, I do want to ask the question is from a research perspective, and as you start to think forward about news and information, you know, we’re having so many new private companies that have entered the market. We have private companies like stone X and many others that have existed over the years, and new ones are entering the marketplace for research yield updates, and we’re getting information from China and from Brazil, and you get all these questions of, How reliable is that data? How reliable is our own data? Are we going to eventually transition to a spot, kind of like when you and I were at the exchanges and the pit trade had existed, it was kind of slow. You mentioned it. People didn’t always get reported their trades in a timely manner to now it’s microseconds. Do you feel that perhaps, maybe even this government shutdown accelerates this but that we get to a point where the information is more real time and we rely on, call it an exchange of information, to truly understand where we are with yields and stocks and other things like that. Oh, I

Fred Seamon 24:04

feel for certain that we’re going to see incredible amounts of change going forward. The technology is just improving every day, right? And satellites, cameras, the I’m not one of these people that, oh my god, AI is going to replace people. I don’t believe that, but I think AI is going to be a good kind of first step for analyzing all of these data, and then people will ultimately, but it’ll be a massive amount of data that will come in, and the AI will make it manageable for a person to evaluate. So I think, yes, we will continue to see evolution, both in private companies, but also, I think at the USDA as well. We were just at an event at West Texas and a live cattle event. And, you know, some of the interesting things that they’re working on from that front. So I think there will be that, that evolution, and you will see a lot more data available in more real time or near real time, as we go forward. And that’s important. You know, one of my jobs at the exchange is new agricultural products. You know, me and my team are responsible for designing new agricultural futures contracts. And, you know, back in the floor days, and historically, that always meant physically delivered, right, you know, and that’s still the gold standard, don’t get me wrong. But bringing a physically delivered contract to market, you know, designing a delivery mechanism, getting firm signed up for, you know, participating in that. And, you know, it takes a lot of time and a lot of effort to do that, so the cost to bring a physically delivered contract to market is pretty high. So, you know, you’ve got to have, and again, it’s the gold standard. You would still do those, but you’ve got to have a lot of really strong supporting economics for the exchange to make that investment. But you have a lot of these, you know, firms, USDA data, but also, you know, price reporting agencies that are assessing, not just reporting markets, but assessing markets. And one of the areas that you know, we’ve had growth is the ability to bring cash settled contracts, based on these assessments, to market, and they’re a lot cheaper to bring to market. So things that historically probably would have never seen the light of day of a futures contract. The calculus is different just because the cost and the effort to bringing it is is there. So you know, that’s another area where we see a lot of evolution.

Speaker 2 27:10

If you’re enjoying today’s show, check us out on Facebook. Just search RCM, ag services for market updates and tips. Find us on Facebook today.

Ben Hetzel 27:22

Yeah, and I think one, one to call out that I recently learned about is the new fertilizer contract, the 10 ton, yeah, you know, I think that could be valuable. And there’s tons of arguments about size and and what the perfect fit would be, and is it more of a producer contract, or can commercials utilize it effectively and but I think it speaks to the innovation and some of what you’ve you’ve touched on today, and I think part of the challenges is promoting it and getting it utilized so that there’s plenty of liquidity and and and again, being cash settled makes that a more appealing situation.

Fred Seamon 28:05

Yeah, that’s been, you know, we’ve had fertilizer contracts for a long period of time, but they’re more wholesale directed contracts. And the idea was, hey, you know, could we package one of these and aim it more at the producer level. And that’s where the 10 ton came from. You know, the 10 ton urea. Let’s get some market makers involved. So there’s a good two sided market. And, you know, let’s put it out there. You know, that’s a major cost point for so many producers. And you know, a real inability to, you know, other than forward contracting. And then, you know, the elevators being able to have a tool to use. What could make better forward contracts to producers as well. But why can’t we do something at the producer level with respect to fertilizer, and this has been our first test case, and, you know, we’ve seen some uptake to it, so we’re still optimistic about it, but, you know, an idea that can certainly expand, you know, as we go kind of down from the wholesale level To the actual producer level with respect to fertilizer,

Ben Hetzel 29:22

I think every producer that that I deal with out here really recognizes the benefit of having a futures backed commodity with, you know, contract, because you take sunflowers and peas and and some of those type of products. A lot of the pulses are all the pulses, basically. And, you know, sunflowers can be really challenging to market, because there’s really no that gold standard you talked about having that backed by those contracts and and so thin markets. Obviously, the volumes dictate what, what? Makes sense to bring to market, but I think we all can really step back and realize that there’s a ton of value in and what’s what your company, the CME Group, and others, are doing, to bring these contracts to to the producers, or to the commercial side, or investors. And so I really, I think that’s a take home for people listening. Is this, this is a valid tool, and it’s been around a long, long time. It’s, it’s battle tested, it’s, it’s evolving still, and, and those are all great things, but really appreciate your insights. That’s that’s been fun to listen to that history, too.

Fred Seamon 30:40

Oh yeah, no, glad to share those things. And you know, that’s, that’s why we’re here. And, you know, I spend I’ve been here, you know, coming up on 24 years, and one of the big things for me is, you know, just because something didn’t work in the past does not mean that it won’t work in the future. So, you know, at least I, and I encourage my team to also not put on blinders. And, you know, it’s okay to evaluate something that maybe we tried, you know, a decade ago, 15 years ago, maybe the timings right now. So we work really hard to be non biased, and we are definitely customer driven, that’s for sure.

Jeff Eizenberg 31:29

Yeah, and we appreciate that tremendously, Fred. And you know the people that are listening here today, you recall the reason we brought this podcast on the radio and into the community and are taking taking your time and creating your time to listen is we want to focus on the importance of risk management and around producing crops, whether it’s corn, soybeans, wheat, you name it, trying to focus on helping people make the right decisions, forward thinking on how they actually are planning to sell and market their grain. And none of that exists without the exchange. And the exchange, again, the word innovation and willingness to continue to support the local communities. So for those that are that are listening, if you, if you have ideas of products that you’d love to hear or see. You can call us, you can text us, you can email us, and we’ll we’ll send it right out to chain to Fred. So the other way is obviously check in with Ben over at Scranton equity Co Op, and you know he’ll be able to explain all the different products that they use today, futures, options, some of the OTC solutions. And again, reminder, as we wrap up harvest and head out into the cold months that none of us want to talk about, that you still have grain in the bins, and we need to figure out the best timing to sell that, of course, but always think there’s opportunities to hedge manage risk and just put an offer out there to see if you can get something done. So thanks again to everyone who’s been listening and sharing their inputs, and thanks to Fred and Ben dear for all your time. It’s been a great it’s been a great week.

Ben Hetzel 33:19

Yeah, thanks Jeff, and thanks again, Fred, for bringing those insights. Good visit.

Fred Seamon 33:24

Yeah, thanks guys. Appreciate you having me.

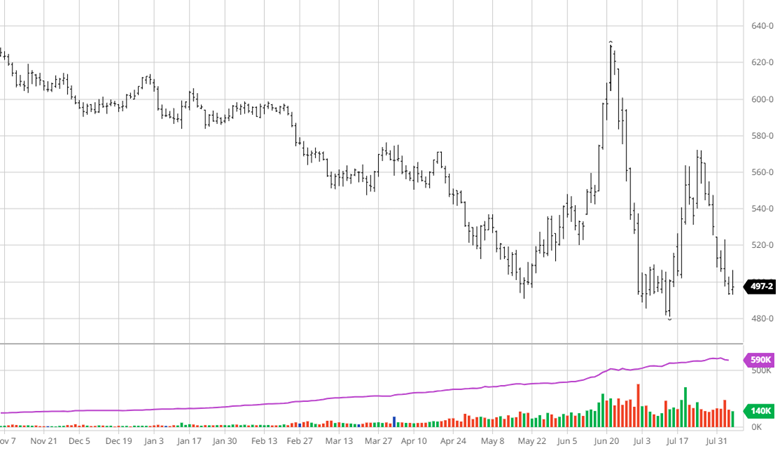

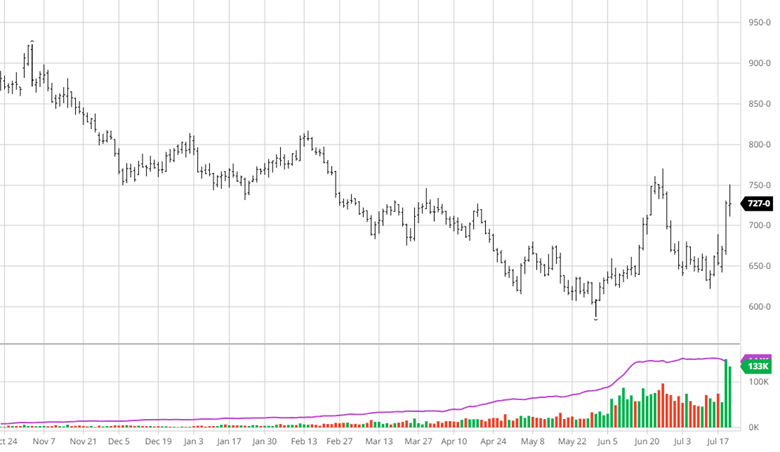

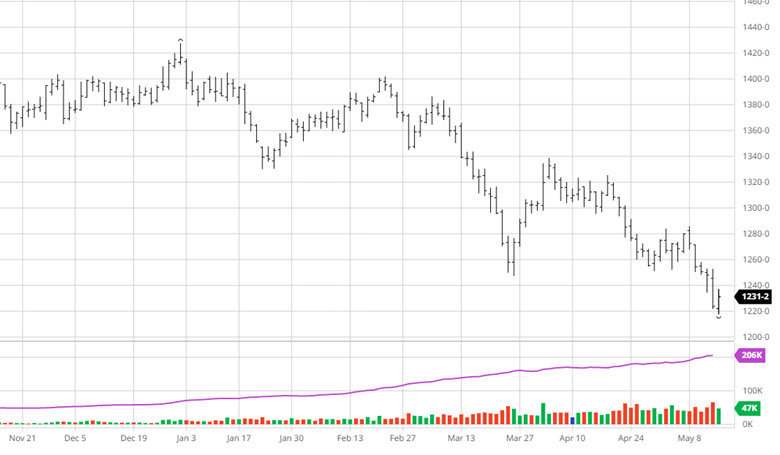

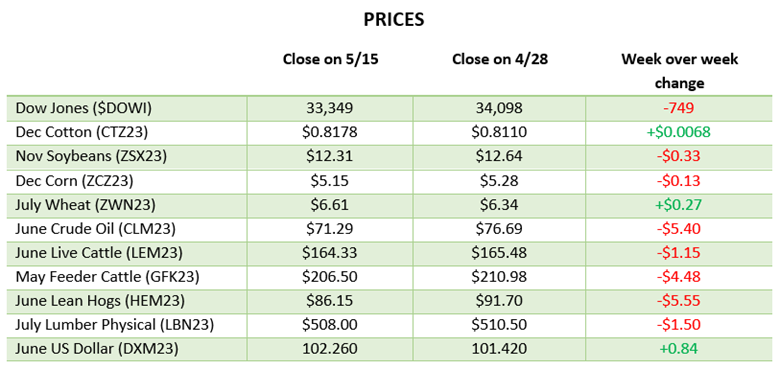

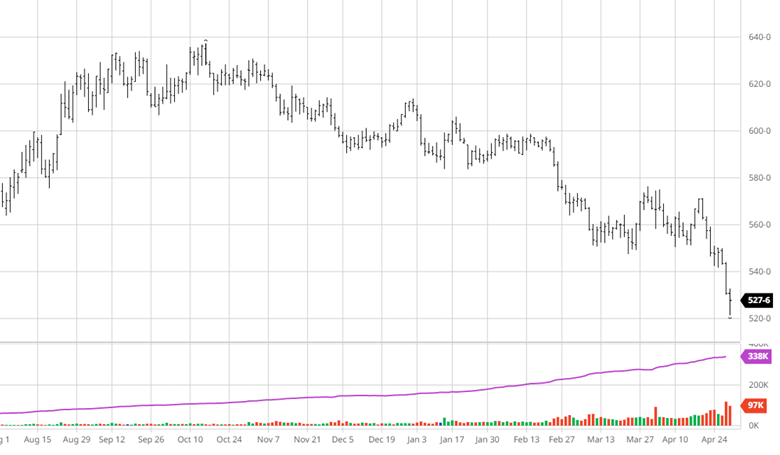

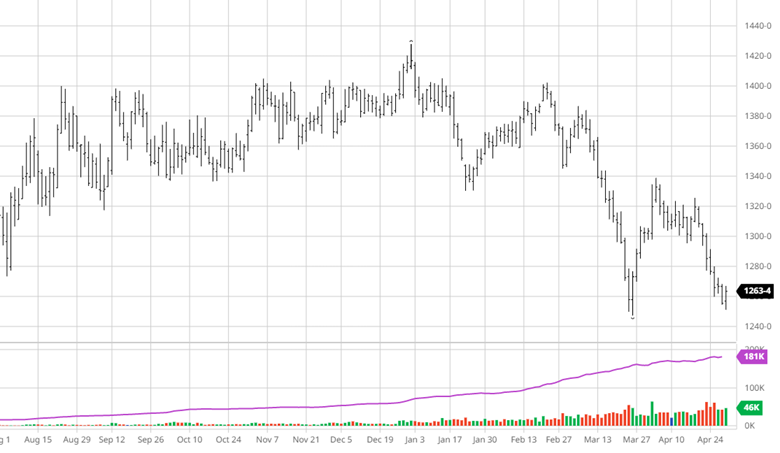

Beans were lower post USDA report as well despite the report being neutral continuing their recent downtrend. The biggest hit to beans in the past couple weeks came when President Trump and President Xi had a call and no announcement of Ag purchases were made around it. Without China buying US beans there is no major upside currently, except for potentially lower yields. South America’s crop has been able to satisfy China’s needs as that trend will continue moving forward until they run out of supply.

Beans were lower post USDA report as well despite the report being neutral continuing their recent downtrend. The biggest hit to beans in the past couple weeks came when President Trump and President Xi had a call and no announcement of Ag purchases were made around it. Without China buying US beans there is no major upside currently, except for potentially lower yields. South America’s crop has been able to satisfy China’s needs as that trend will continue moving forward until they run out of supply.