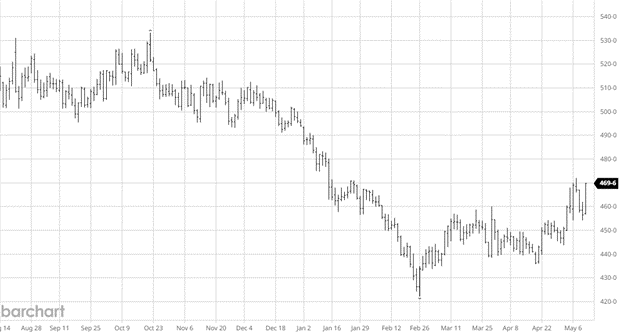

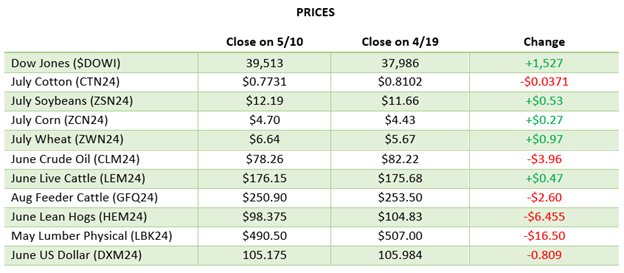

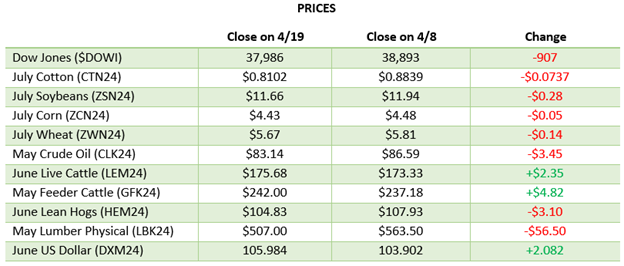

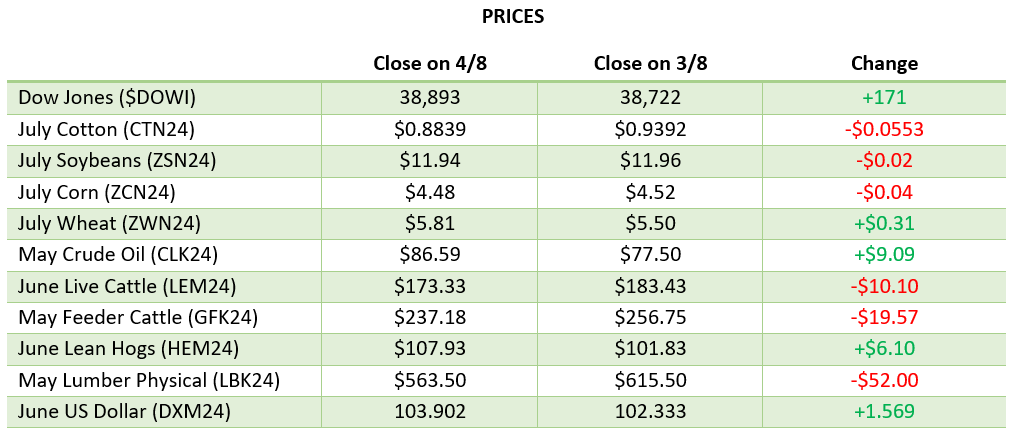

Corn had a rough week as planting is nearly wrapped up and the expectation of high initial US crop ratings put pressure on the market. The forecast for June turned slightly wetter but will not have any material impact on planting finishing up. The Black Sea yields continue to be pressured due to their weather with no immediate relief apparent. The USDA Crop Production report on June 12 will be watched closely as we get updates for the US including acreage, area harvested, and yield. The market will be looking for any good news before then to help support a weakening market.

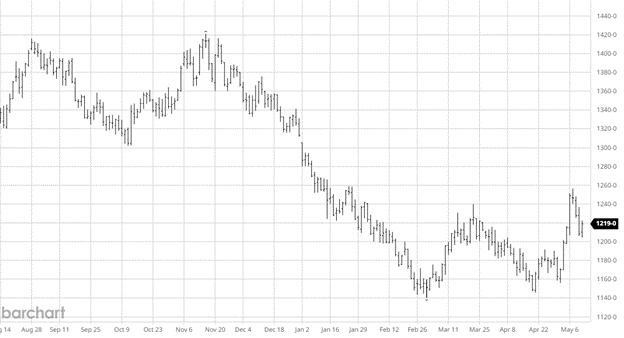

Beans fell on the week as planting advances despite some slowdowns in some areas due to weather. Currently only 3% of soybean production comes from areas experiencing drought. Rio Grande do Sul is turning warmer and drier after weeks of issues with flooding. Morgan Stanley estimates 5 million tonnes of soybeans were lost to the flooding in the region. Beans, like corn, have no bullish weather to help the market as it looks like normal planting progress should be made and no major weather issues in the forecast.

Beans fell on the week as planting advances despite some slowdowns in some areas due to weather. Currently only 3% of soybean production comes from areas experiencing drought. Rio Grande do Sul is turning warmer and drier after weeks of issues with flooding. Morgan Stanley estimates 5 million tonnes of soybeans were lost to the flooding in the region. Beans, like corn, have no bullish weather to help the market as it looks like normal planting progress should be made and no major weather issues in the forecast.

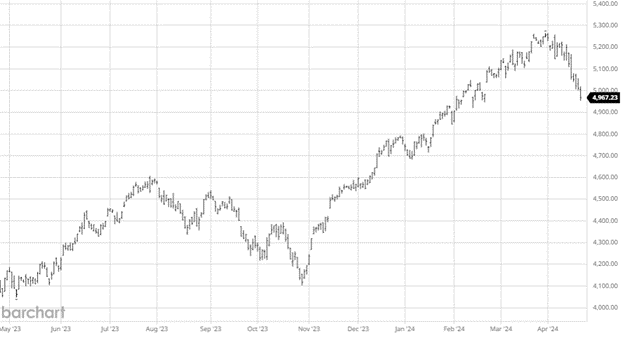

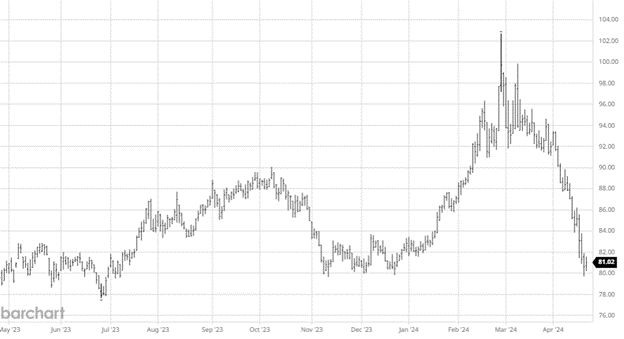

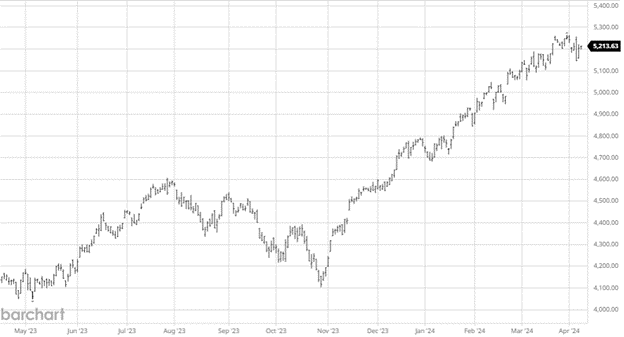

Equity Markets

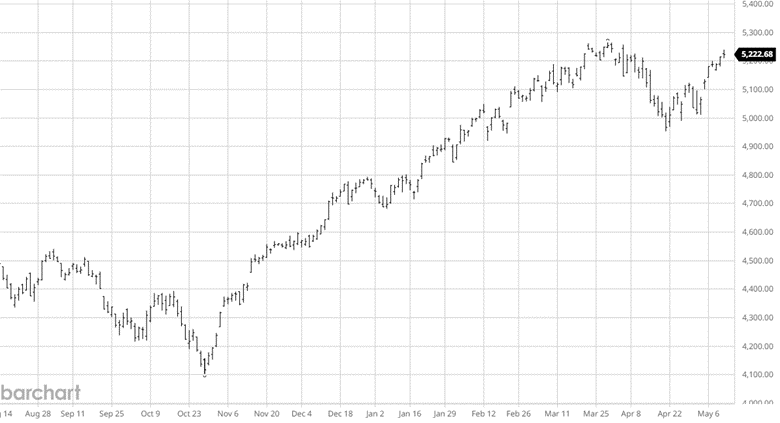

The equity markets have had a rough go lately with all major indexes falling well off recent highs. Several earnings misses and growing belief that “higher for longer” could last through the summer has people raising questions about the market.

Other News

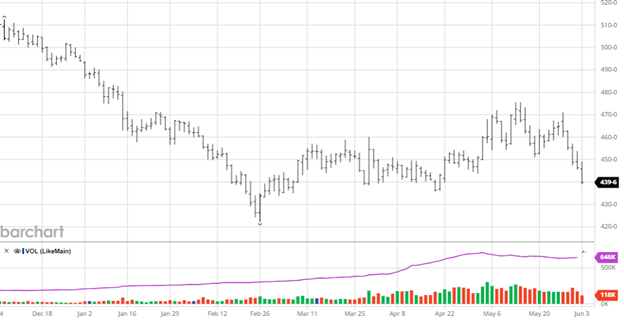

- The Black Sea weather forecast has improved for next week as rain has been added to the forecast.

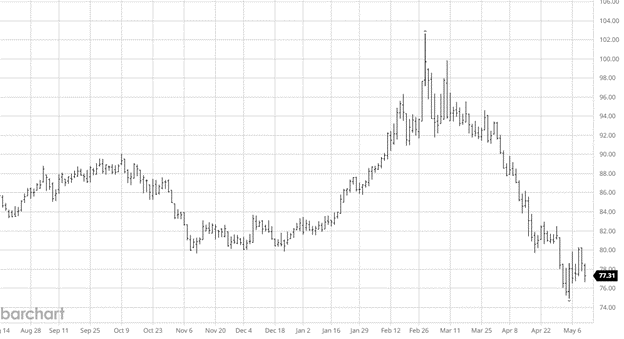

- Wheat has seen a strong rally since mid-April seeing a $1.50+ rally at one point with possible production issues in the Black Sea even with the small pullback to end the week.

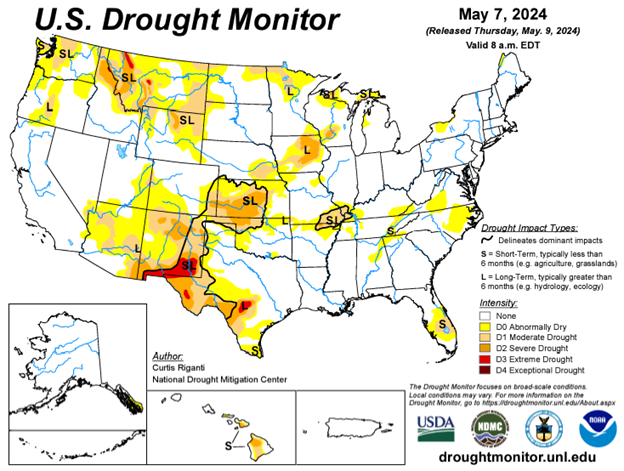

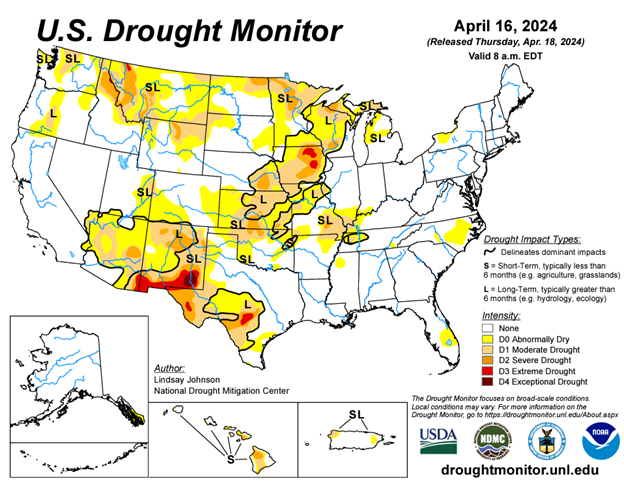

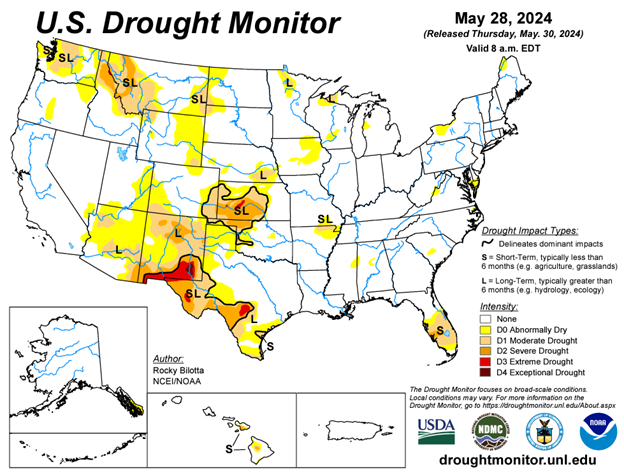

Drought Monitor

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.