Recap:

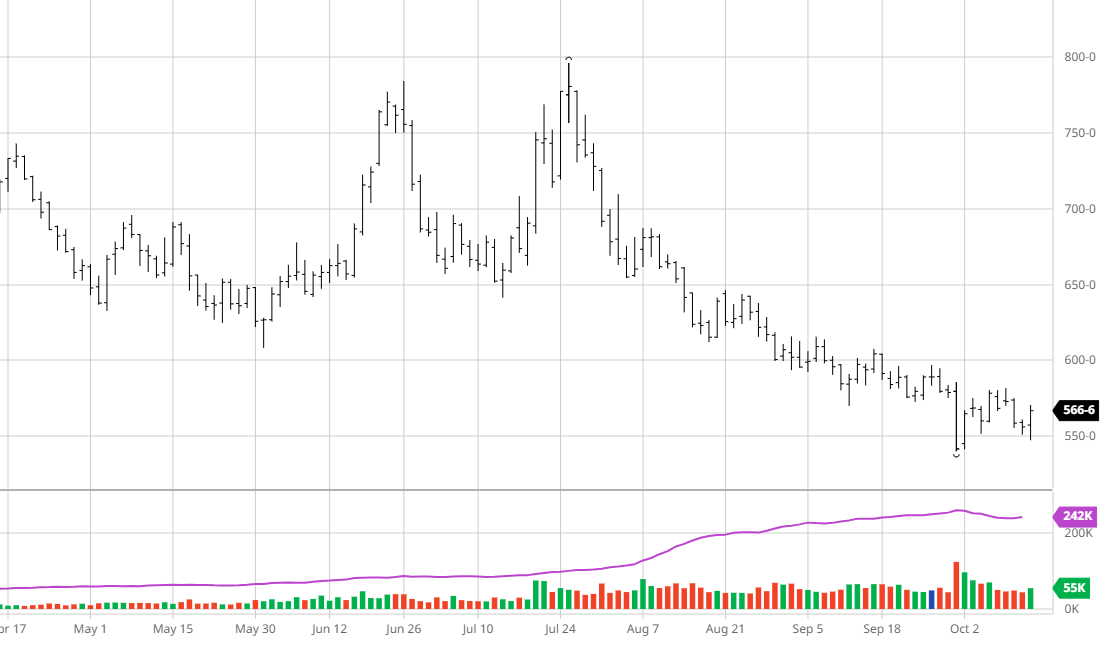

The immense tension in the lumber industry is lower mill costs and less demand versus a new face of the pent-up market. No better example of what lies ahead from this tension is the way futures traded on Thursday. A pattern of voids is developing that will cause higher prices as the industry now gets long futures and is no longer hedging. In the short run, the industry’s one-sidedness will continue to create downward pressure. The makeup will look like an overbought condition, with prices going lower.

Time has been good to the mills. We are going on 20 months of a bear market. At the beginning of the cycle, production costs were estimated to be around $600. One year later they were down to $500. And today they are closer to $400. We can argue about the exact cost, but the net end result is that time has lower production costs. Time has not lowered the pent-up demand.

The trend of owning a home started to pick up around 2017. Home buyer confidence soared. By 2019, the employment of many minority groups had hit records. With low rates and consumer confidence in all groups throughout the US, the hope for a home was high. Then Covid hit. My point is that the pent-up players are still around. Higher rates have slowed but not reduced the need. The home builders know that at a price point, there is good demand. They are going into 2024 with the same strategy and 2023 and that is to wait and see. Statistically, they are carrying the same high inventory of what is called undesignated starts on the books as last year. They can turn the building spigot back on quickly if the economics warrant it.

The macro picture projects the lumber market to the bottom and moves out of the bearish cycle. The norm is to have a few big buy rounds that go south. It will take time. The micro picture is to put all the chips on black. Vegas is beautiful this time of year.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636