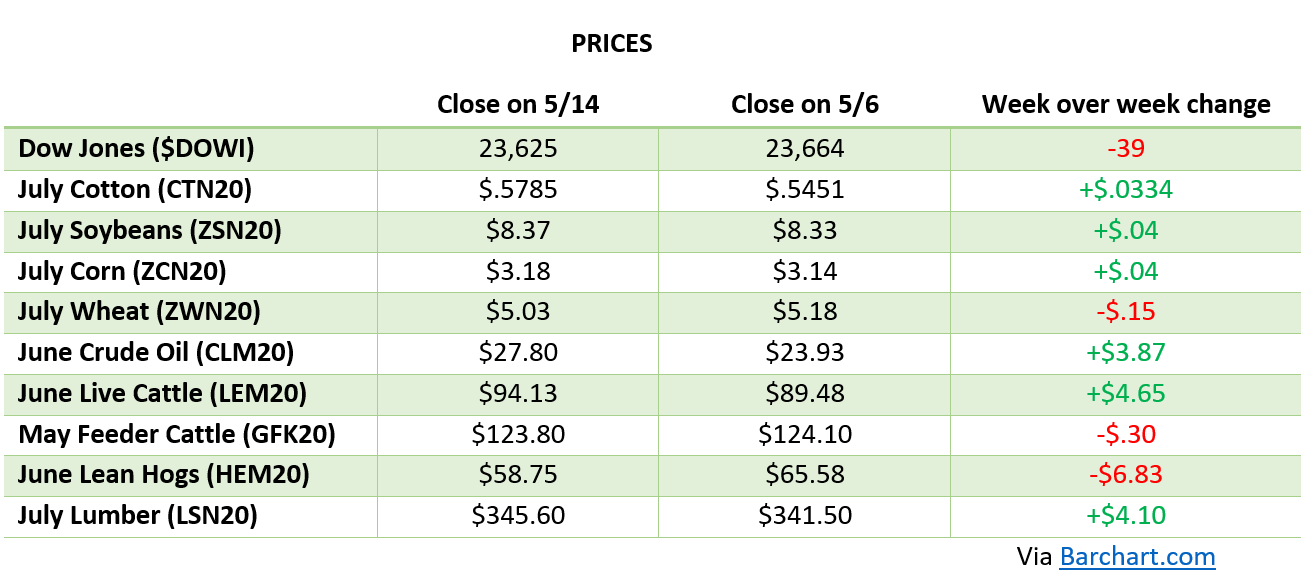

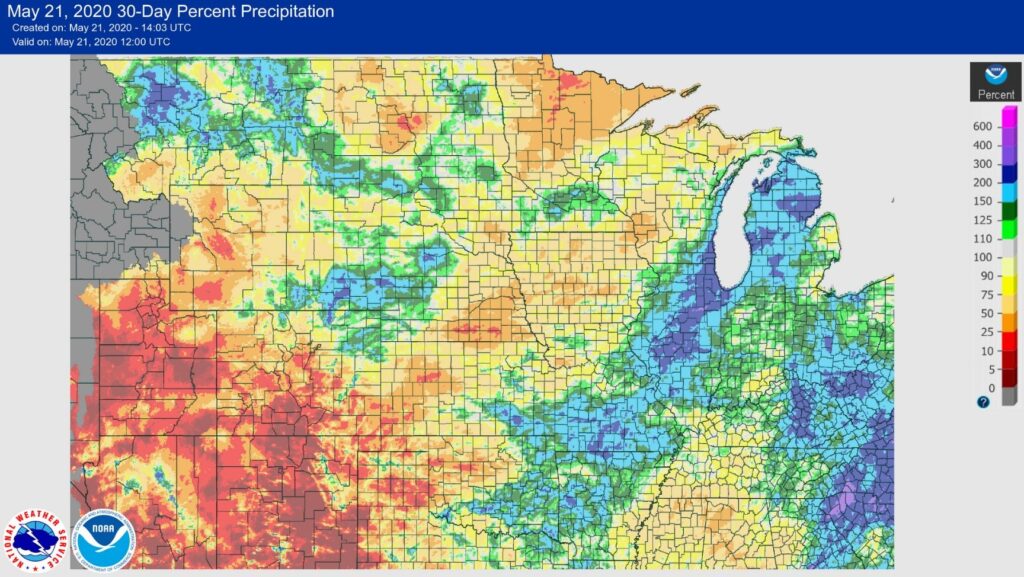

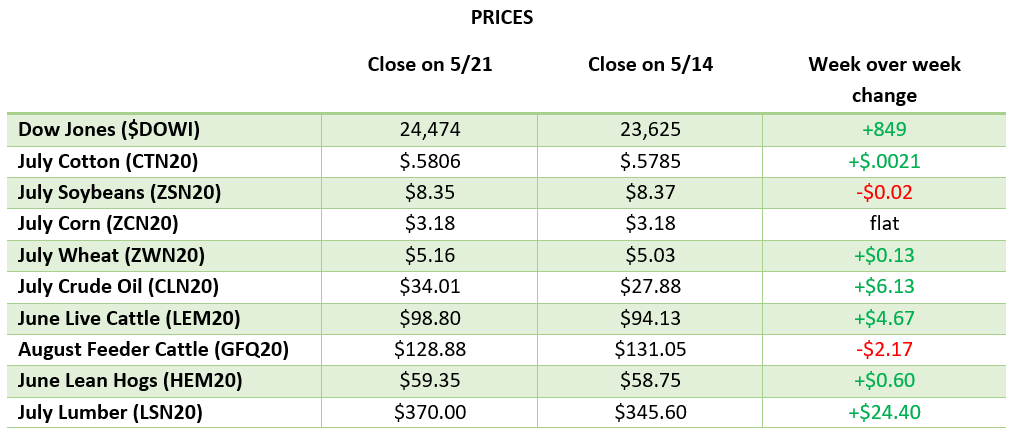

Farmers in the Midwest are saying what we’re all thinking – “enough of the rain already!” There has been major rainfall, and even flooding, across most of the Midwest including Michigan, Illinois, and Southern Ohio over the past month, and without a drier outlook over the next week, there’s the potential for planting to be pushed back up against the “prevent plant deadline” in those states. Across the rest of the country, planting is still on a good pace and flat prices week-over-week show little news in the markets. Ethanol production ticked up last week but will need a much larger demand to use up the massive amounts in storage. With exports falling within expectations trade looks to remain calm as we head into Memorial Day weekend and the start of summer.

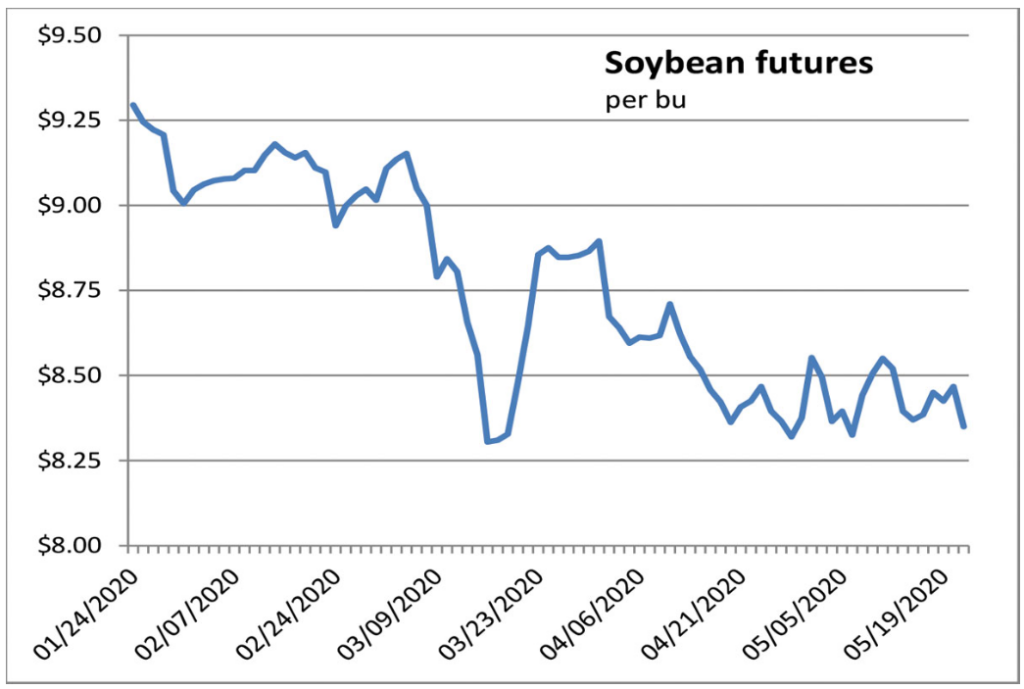

U.S. Soybean planting, like corn, has continued its good start in most areas except for North Dakota. Bean prices took a big hit on Thursday despite a 22-week high in sales of 1.205 MMT with 738k tonnes going to China. The possibility of increased political tensions as President Trump fired off more tweets criticizing China pulled the markets lower after a good week. Along with Australia’s wanting the WHO to investigate the origins of the coronavirus outbreak, Trump’s tweets are another thing in a long line of issues that could come between the U.S. and China’s phase 1 trade agreement.

Wheat has seen a boost this week as the Russian wheat crop yield appears similar to last year. The excess rain in parts of the US with SRW has lead to some worries about the crop and the possibility of worsening conditions. There has been a pickup in domestic demand as mills around the country are opening back up and demand ramps up. Keep an eye on Russian Wheat as another big cut to their yield would be supportive of U.S. wheat prices along with further weather problems domestically.

There’s been a lot going on in the meats sector – specifically when it comes to COVD-19 impacting American production plants.

COVID-19 has infiltrated America’s meatpacking plants causing them to slow processing speeds, or close all-together… Converting livestock into the cuts that get to your plate requires massive facilities, intensive labor, and working in tight quarters which makes it difficult, if not impossible, to control the spread of a contagious disease. Without the ability to “socially distance”, thousands of plant workers have become ill, some have died, while many others are too afraid to go to work. The repercussions of the Covid-19-related plant disruptions will impact our food system for years to come. Once the smoke clears, owners of large meat packing plants may look to create smaller, regional facilities meaning consumers can expect higher prices, and fewer choices in the coming weeks and months.

Check out more short-term and long-term repercussions in the rest of our blog here.

CFAP Relief Package

The USDA came out with more information this week about the CFAP Relief Package. The CFAP had scheduled payment of 32 cents per bushel from the original CARES Act and a CCC payment of 35 cents per bushel on the lower of 50% of last year’s production or 50% of your unpriced corn on January 15th. That works out to potentially receiving 67 cents on half of last year’s corn crop. The soybeans payment works the same with payments of 45 cents and 50 cents for a potential payment of 95 cents per bushel on 50% of last year’s bean crop. The math is not clear nor why January 15th was chosen, but those are the guidelines. Livestock is also covered in the payment and information on that from the USDA website can be found here. Sign up starts next Tuesday the 26th at your local FSA office. For more information on how to sign up, check out this video.

Via Barchart.com