Lumber has long been known as a quite illiquid futures market. We talked about it on the RCM blog here, on the Hedged Edge podcast here, and Derivative podcast here.

But changes are afoot which may solve the main issues that lead to the illiquid nature of lumber futures, with the CME Group getting ready to launch a new lumber futures and options contract that will be smaller and have more delivery options, which we believe will allow for more effective risk management. The CME said it plans to launch the new contract early in August. The current contract that expires in May 2023 will be the last month under current specifications. This has caused some buzz in the industry, so let’s take some time to check it out.

The two big new key features as far as we’re concerns are:

• Small contract size for precise hedging

• Participation from throughout the lumber supply chain

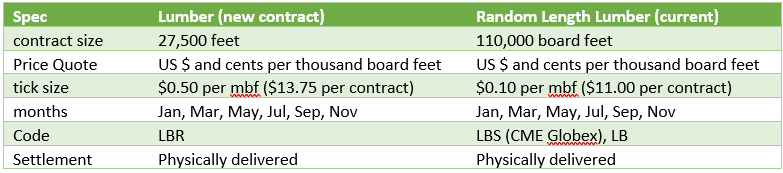

The smaller contract size is very welcome in the industry as the current lumber contract is for 110,000 board feet (1 rail carload), whereas the new contract will trade in lengths of 27,500 feet (1 truckload). This will allow for more precise and accurate hedging while allowing for more participation in the market from smaller traders. Smaller traders had been pushed out in the past with the requirements and contracts not fitting their needs. This will allow for greater liquidity in the market that currently only sees a couple hundred contracts traded a day.

The new contract also allows eastern mills to deliver, where the current contract only allowed western mill delivery. This expands the accessibility to producers to accommodate the changing landscape and needs of the market. Delivery will now be in Chicago and allow for eastern species of spruce, pine and fir, instead of just species grown in the west (southern yellow pine is still not a deliverable species). This will make the market more accessible and will increase participation and provide more risk management options.

Now, the CME is a publicly traded company and they’re doing this to generate more volumes and interest in this market. But that doesn’t mean it’s not a good thing. We think it will definitely create better liquidity for the lumber market, by both increasing volumes from current market participants and bringing new participants to the market.

By making deliverable contracts for both east and west mills while lowering the contract size, you attract new participants from all along the supply chain from producers of wood, to mills, on through to home builders. And as those commercial groups increase their footprint, the hope is that speculative trade flow (i.e hedge funds, ETF’s, and retail traders) also begin to increase interest in the market; creating a flywheel effect adding to the liquidity for the physical market participants.

The contract is ¼ the size of the old one meaning if you want to hedge or trade the same amount of board feet it will require 4 contracts instead of 1, creating more contracts to trade across the market (more liquid). The length also allows for more accurate hedging needs by making it easier to accurately manage your risk (think now you can protect 165,000 board feet vs either 110,000 or 220,000 feet). Traders will also be able to spread across the two markets for a short time creating new trade/arbitrage opportunities as they are not the same contract and specs, so they will not trade perfectly in tandem.

Ultimately homebuilders and speculators will be welcomed back into the market with these contracts being much more friendly. Builders will be able to hedge the price of lumber on a couple houses (or one large one) instead of having to hedge several at once that may not be under contract.

Our team as well as many others in the lumber industry are fired up after years of wanting a better lumber contract…LETS DO THIS!

Big changes to #lumber happening allowing broader participation for the industry to offset risk. @SherwoodLumber #guaranteedforwardprice https://t.co/sijrYkwLVU

— Kyle Little (@lumberlittle) July 5, 2022

🚨 🚨 🚨 NEW LUMBER FUTURES CONTRACT LAUNCHING AUGUST 8TH 🚨 🚨 🚨

This is great news and a culmination of a few years worth of hard work by the CME and industry participants.

The old contract will continue to trade as normal. https://t.co/xM0GNM5aQg

— Stinson Dean🌲 (@LumberTrading) July 5, 2022

As the contract progresses and ultimately receives approval, we will update this article to reflect new information provided from the CME and CFTC.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact RCM Ag Services today for more information on how this new contract could fit your business.

agsupport@rcmam.com