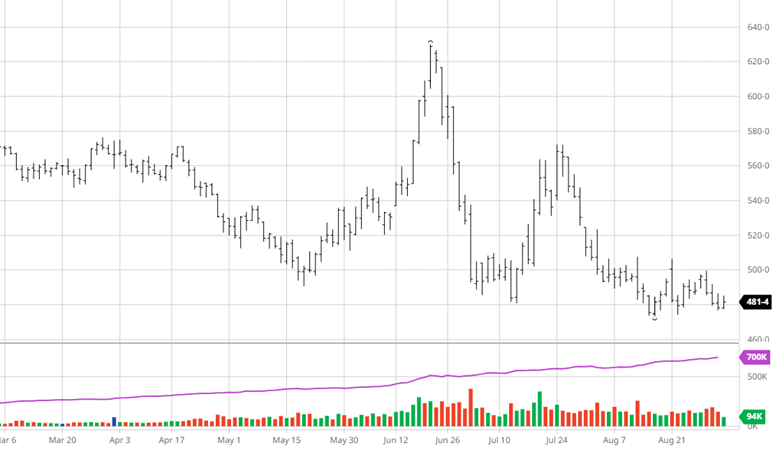

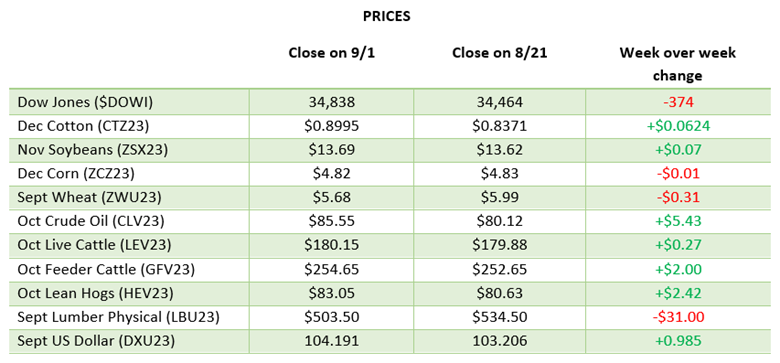

Lumber Weekly

Last Week:

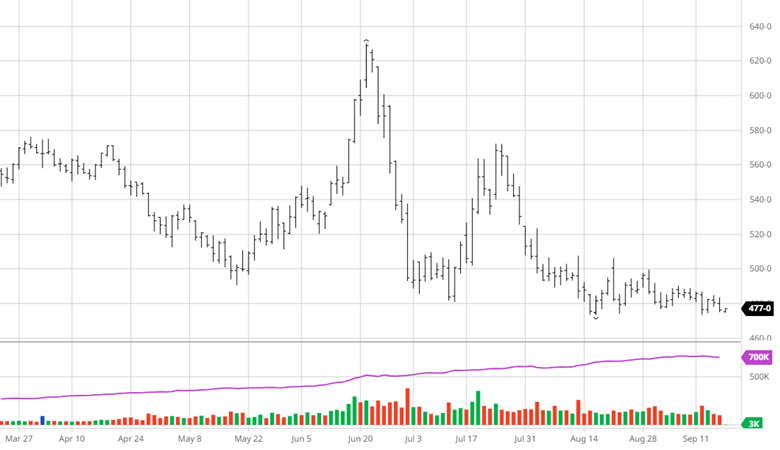

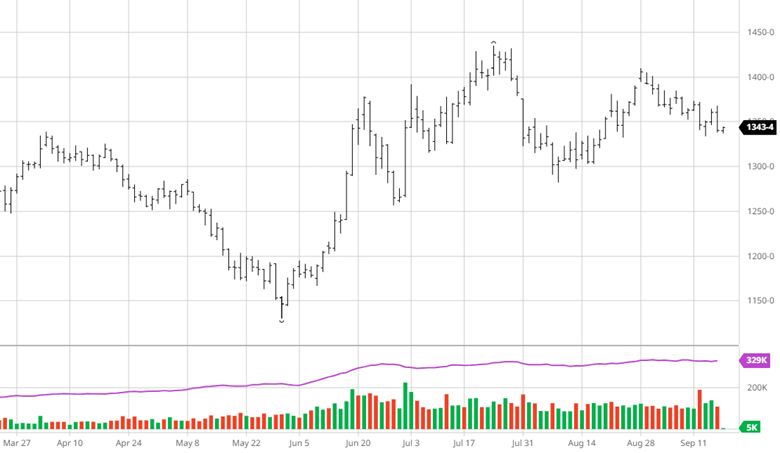

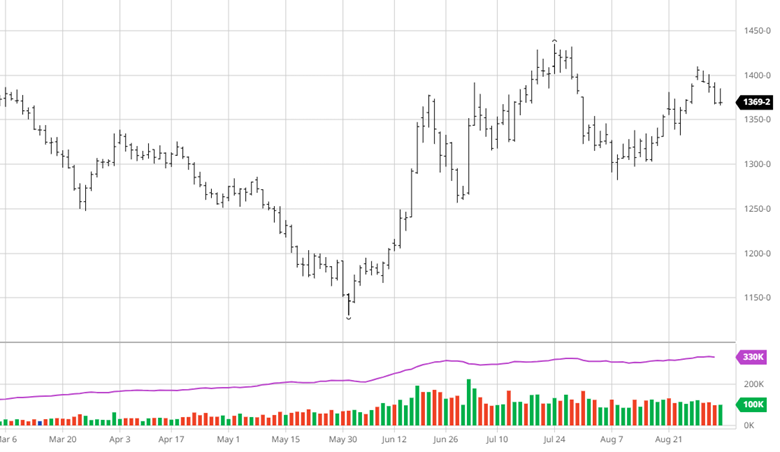

Futures and cash took different paths last week, but neither blazed a trail. The cautionary flags are out en masse throughout the industry. The time it takes to replenish the system can be measured in days, not weeks. The reason for the quick turnaround lies in the marketing of wood today. There are a lot of sellers out there with one goal: to sell. Items never seem to get tight despite some very good business. Cash last week found the last of the participants while futures saw the “deals” again. The key takeaway for the week was that the market remains in a sideways trade. The minor blips up and breaks down have nothing to do with the overall trend.

Thought:

The fiscal year-end for many in this industry comes in around the October time frame. By then, the focus becomes the 2024 building season. The industry has already moved on to next year. There are many of the same issues to contend with. Let’s take a look. The US economy, and for that matter, any country on earth, has never experienced such an influx of capital into the system. There are no models or equations to guide us. Every business today has to react instead of plan. That creates opportunities. It also causes many firms to be far more cautious.

Right now, the homebuilders have the goose and its golden egg. Rates and existing home sales remain sticky. One high and one low. There is no way they will over-accelerate construction. They will continue to feed the system but at a pace of plus 5 to 10%.

The multifamily sector is starting to have an inverse effect from the high rates. The ROI is just not there for many.

Today, lower lumber prices would not accelerate building, nor would rising prices slow it. It is all about sales momentum, which remains steady. Many are beginning to wonder if an economic slowdown, i.e., higher rates and higher unemployment, won’t slow construction. Most need to realize that between the Chips Act and the Inflation Act, there will be 2 trillion dollars entering into the system on top of what is already there. That spigot will not slow. 2024 could end up being very lucrative.

Summary:

The futures market has done a good job of trading in between the goalposts. The time after the roll tends to see the funds adding. That will lead to new lows and widening goalposts in today’s environment. No momentum indicators call for a steep decline. The lows will be fund-driven and a grinder. One trade to watch is if the industry gets short here. There are no spec shorts in the market. The industry shorts have been here for months. Will others jump in? Next week should be a carbon copy of last week. Let’s hope we don’t test the circuit breaker system…..

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636