The Lumber Market:

There has been a shift from a supply and demand market to a “cost of supply vs. demand” market. By that I mean the actual supply does not have a relationship with its cost. The cost will be driven by a tariff charge. Let’s separate the two. If there were not any tariff threats facing the market today, the slack demand would be pressuring the market lower. I have seen so many times in the past of a spring that never developed. The wood bought covered the wood needed. It’s starting to have that type of feel. Let’s take a step back. Futures are up $120 from the lows this year. We are putting it all on the tariffs, but part of it could have been the spring run. I’ll say that because demand lacks any momentum. If the tariffs came out tomorrow, prices would go up, but demand would not. I am not calling for demand to slow. I just want to be clear that today we are an “cost of supply market.” Any other year it would be a sell in May and go away. This isn’t any other year.

There are two types of hedging. The first is basis trading locking in a profit. The other is risk management or the protection of the company. This medical insurance comes at a cost and always gets questioned by the higher ups, until it works. You have to have inventory. You also have a plan to protect it in place.

Technical:

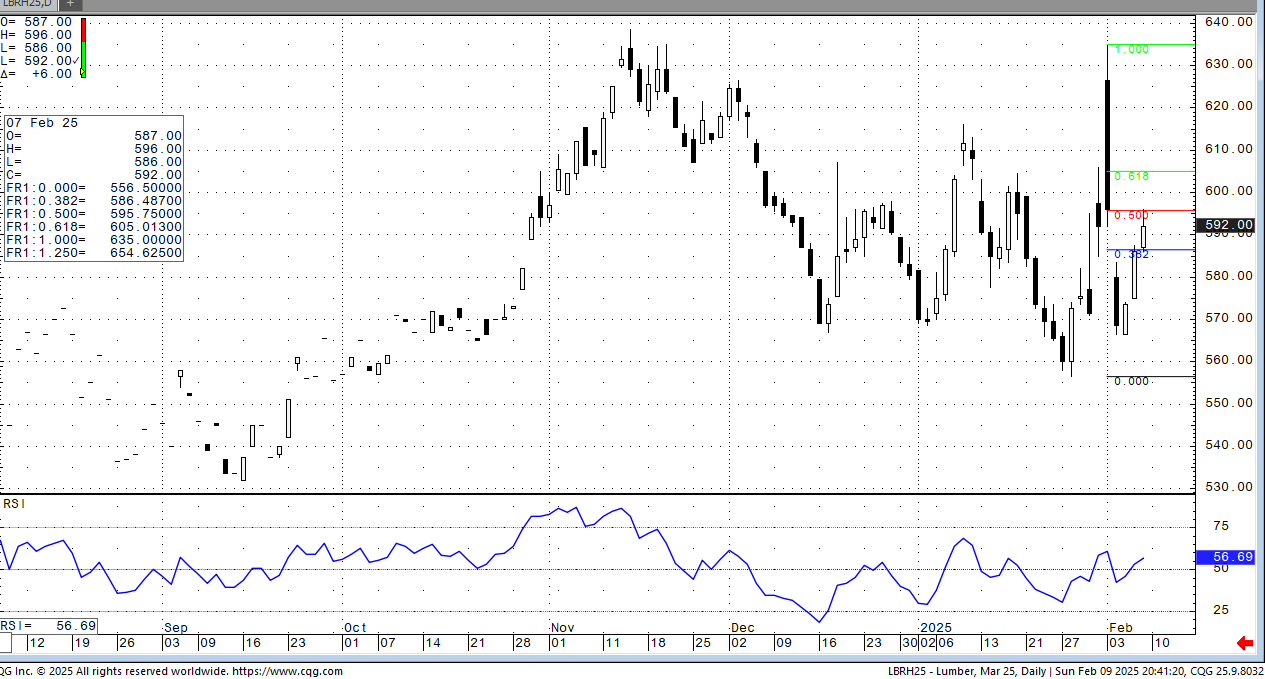

The Bollinger bands are slowly moving back together. There is a long way to go, but viewing the market getting range bound is the play until something comes out. There is a strong support line in May sitting at 632.40. I think the focus this week should be on the chart pattern in futures and not on any rumored tariff garbage. I’m not positive, but I heard of spreads on DraftKings between a college bball teams and lumber are getting sent out.

Daily Bulletin:

The Commitment of Traders:

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636