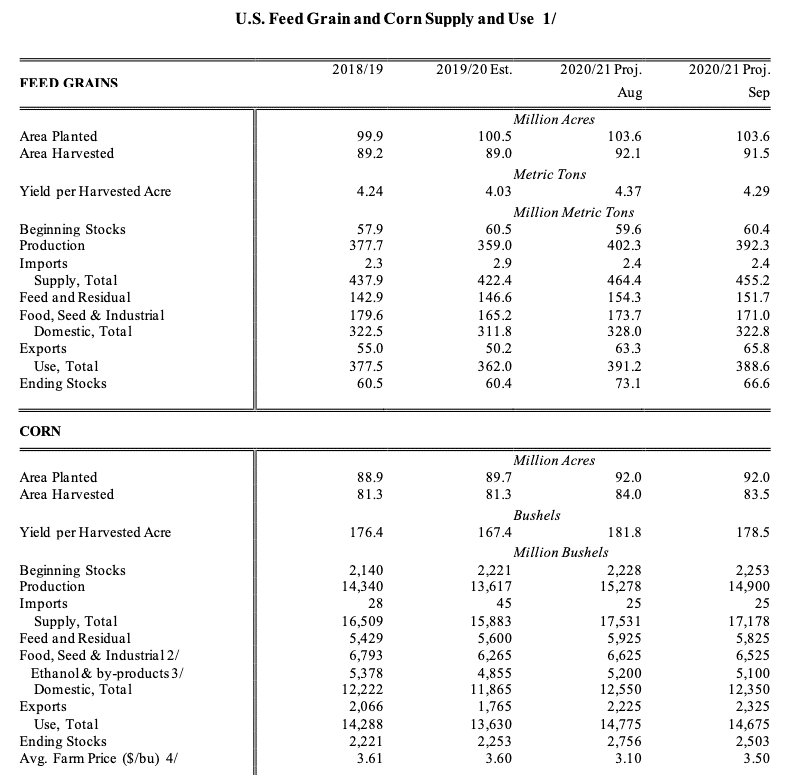

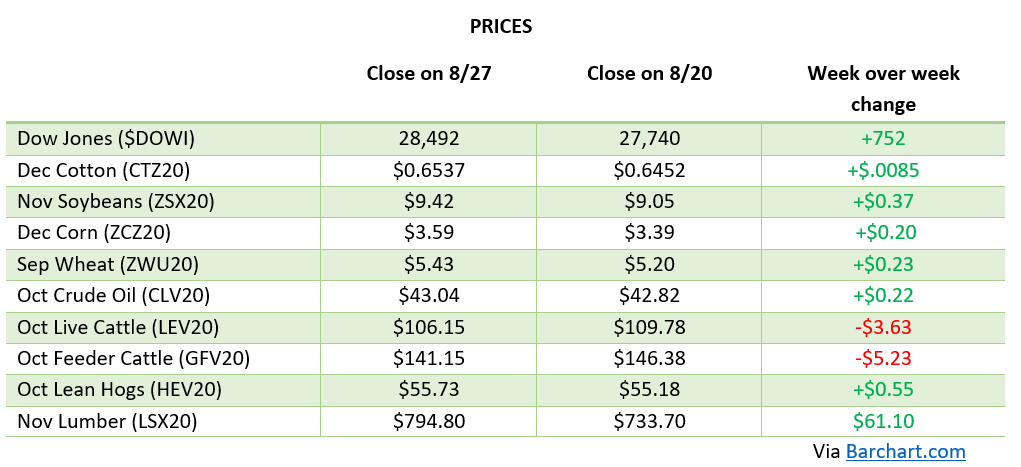

Corn gains on the week have been driven from continued strong export numbers as well as trade expectations of a 178 yield estimate heading into the USDA report on Friday. The report came out with a 178.5 bu/acre estimate which is pretty in line with what the trade was expecting. The drop from the 181.8 bu/acre yield estimate from the previous USDA report comes from a combination of the storm damage in Iowa as well as the extended stretch of dryness across many states to end last month. This impressive run up by corn from the lows seen in early August has been welcome heading into harvest. With a 2.5 billion bushel carryover still estimated we may see a tightening of prices as corn leaves the fields and we get a better idea on final yield as well as demand. The bump up in expected corn exports is good to see as the USDA expects countries (China) to continue their buying. Below you can see the Supply and Demand chart for corn from the report.

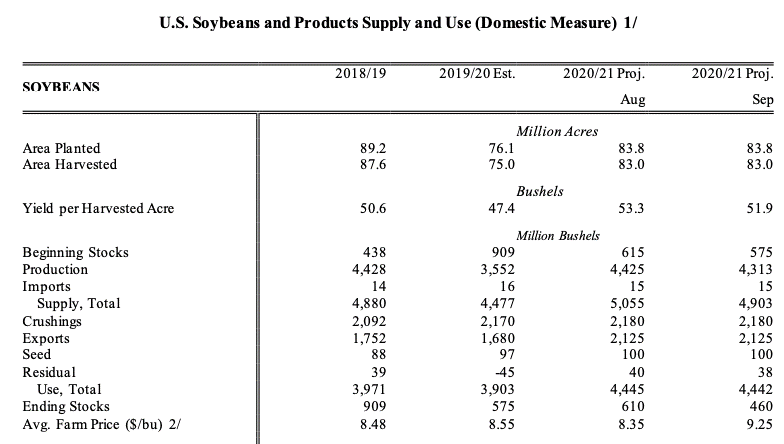

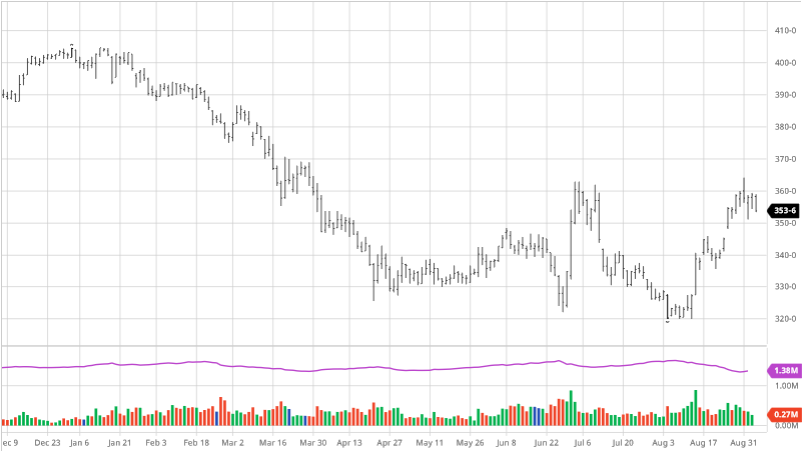

Soybeans have seen strong gains like corn in the last month. The report came through with numbers close to expectations with little surprises. Exports continue at a good pace and China announced that they intend to rebuild government stocks. A month ago $10 soybeans did not seem to be in play but now it is within a few cents. As we get closer to harvest the weather’s effect on the crop will be diminished outside of an early freeze that could cause damage. Keep an eye on exports to keep their pace and any bullish weather news as that magic $10 number looks to be met. See the Soybean Supply and Demand chart from Friday’s report below.

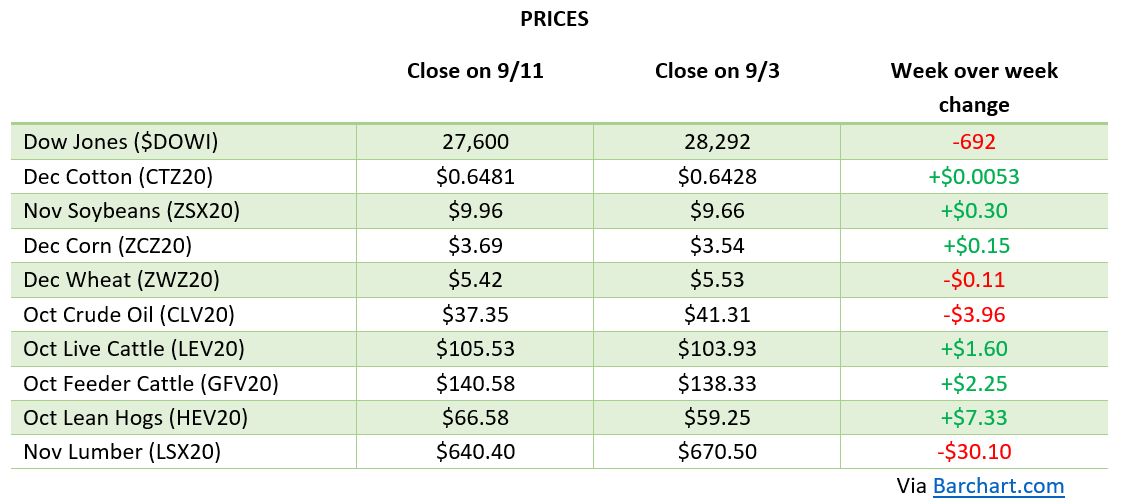

Dow Jones

The Dow has continued to bounce up and down finishing down on the week as tech continues its loses. As the pandemic drags on and business come back or close for good the attention will begin to shift towards the election.

Korea Bans German Pork Imports

South Korea banned German pork imports this week after an African swine Fever case was confirmed in Germany. This move falls in line with guidelines for animal food and safety and is an expected move as South Korea themselves have had trouble with ASF in parts of the country and has been banned from exporting its pork products. Look for some of South Korea’s demand to come to the US market.

USDA: The USDA released their World Agricultural Supply and Demand Estimates today, read the entire report here.

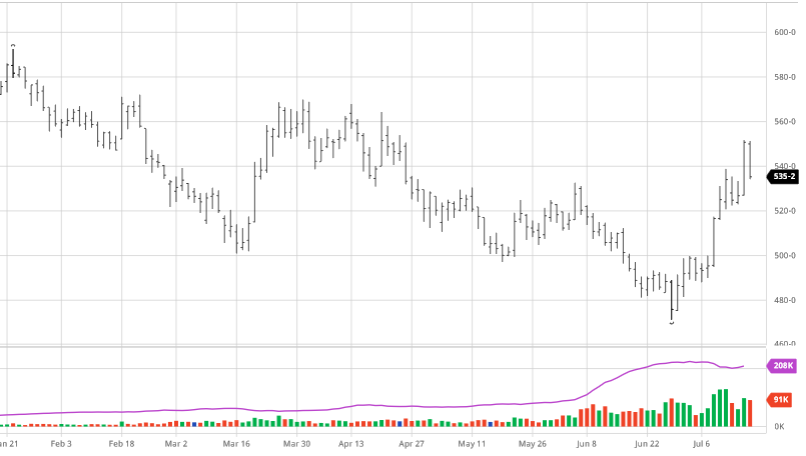

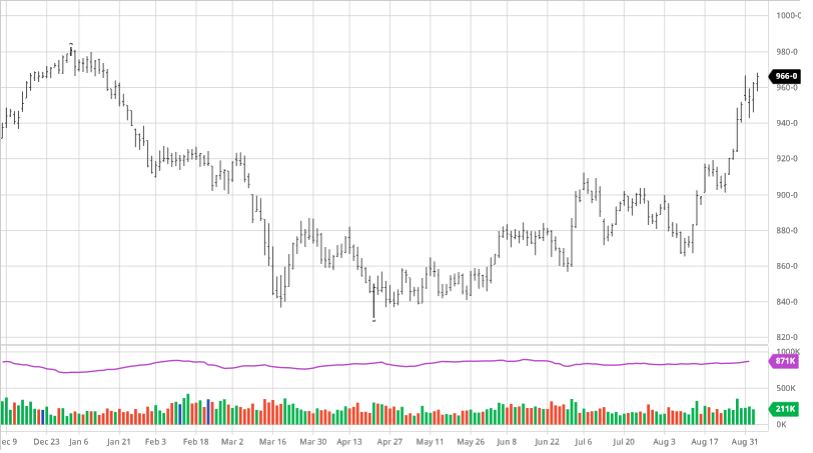

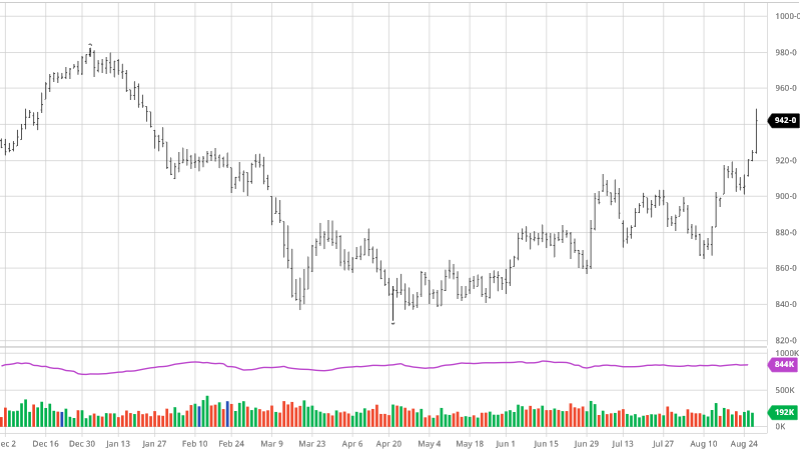

Large purchases from China gave Wheat a big boost halfway into the week. Wheat did have to give a good chunk of that boost back the following day due to a lack of confirmation on purchases, but any Chinese purchases at this point are beneficial to the markets as other Wheat growing countries are seeing lower yield numbers. As you can see below, markets are well off the lows that we set a few weeks back as Wheat has made a solid rebound. Just like with Soybeans, more confirmed purchases, or any purchases for that matter, would be beneficial to U.S. Wheat.

Large purchases from China gave Wheat a big boost halfway into the week. Wheat did have to give a good chunk of that boost back the following day due to a lack of confirmation on purchases, but any Chinese purchases at this point are beneficial to the markets as other Wheat growing countries are seeing lower yield numbers. As you can see below, markets are well off the lows that we set a few weeks back as Wheat has made a solid rebound. Just like with Soybeans, more confirmed purchases, or any purchases for that matter, would be beneficial to U.S. Wheat.