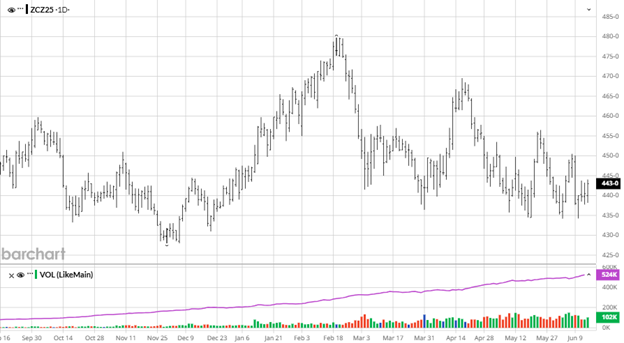

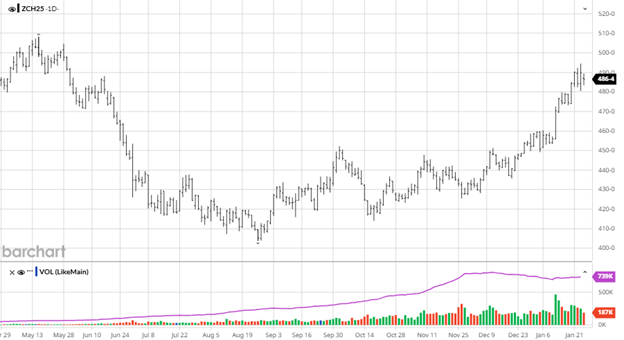

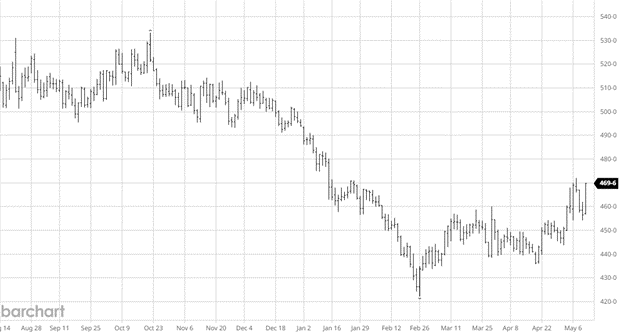

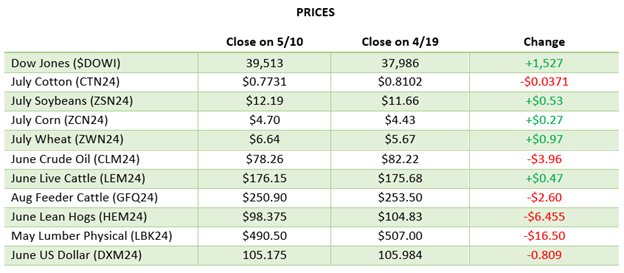

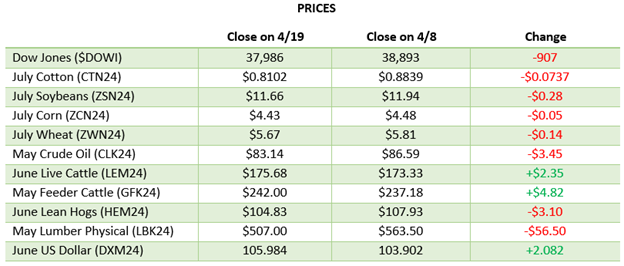

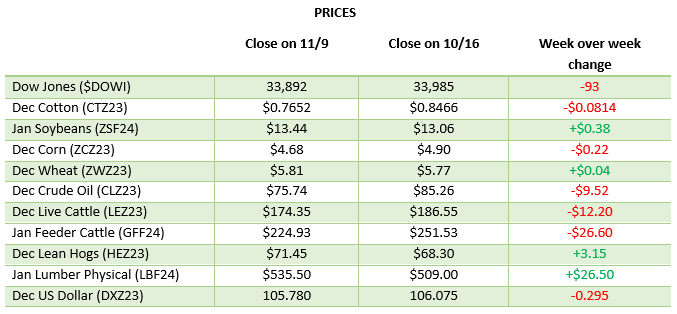

Corn has rallied off the post USDA report lows with a large up day on Friday to end the week. Pro Farmer Tour wrapped up their crop tour and has an average US corn yield of 182.7 bu/ac which would still be a record on top of the added acreage, but well below the 188.8 the USDA came out with. The two sides from the USDA’s report is that they likely won’t come out with a higher yield again with some small weather issues developing, but if they keep it high and make another big correction in January saying the crop wasn’t as big as they thought it could cost the farm community billions. The weather has cooled off for much of the country but the lack of rain for extended periods may be a problem in the home stretch.

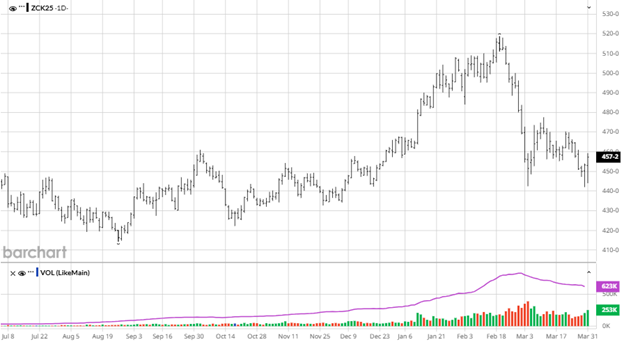

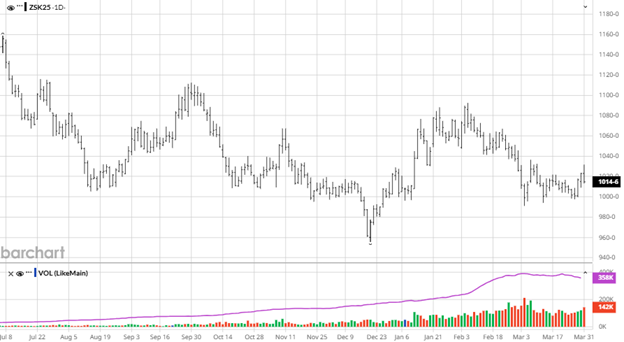

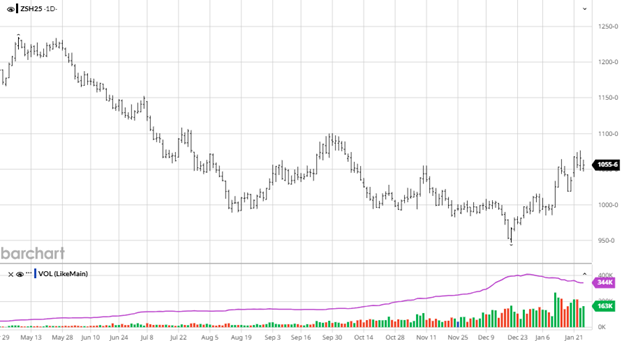

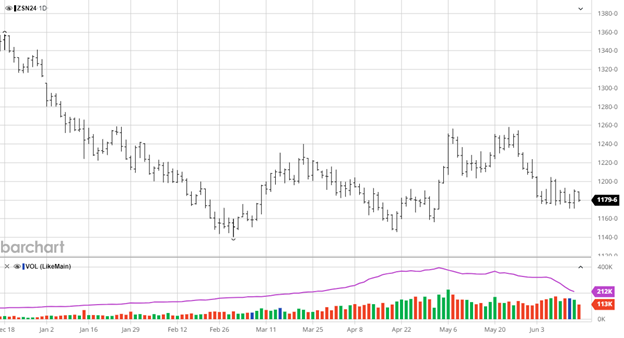

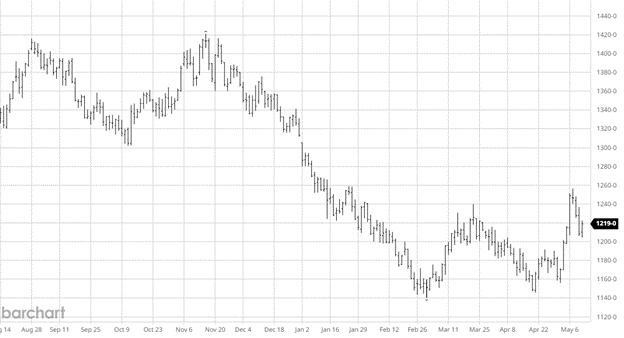

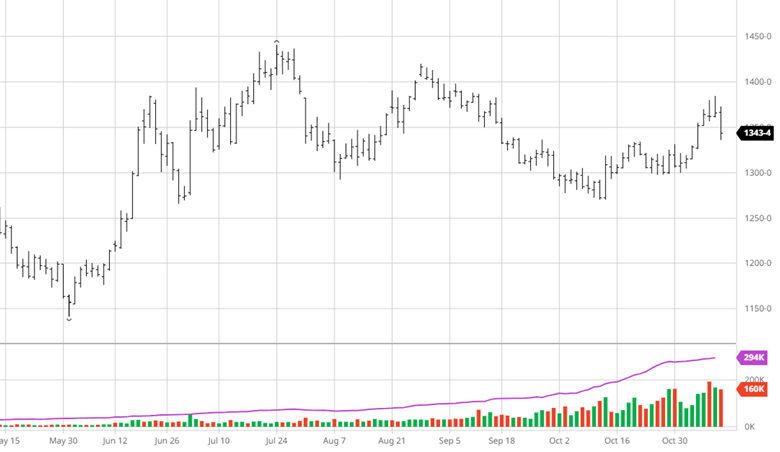

The Pro Farmer Tour found a bean crop more along the lines of what the USDA had coming in with a 53 bu/ac estimate vs the USDA’s 53.6 bu/ac. Beans biggest problem right now has been lack of rain for pod fill but a few well timed rains down the stretch could lead to a massive crop. China really needs to show up as a buyer for beans to leg higher but they can get all they want from South America right now even though they are paying a premium to get them vs US beans. The funds have a neutral position on the market as they wait for news that could send the market any direction other outside of the $10 – $10.50 range it has been trading in the majority of the last 6 months. China still remains a cloud over the market with the Trump administration needing to get Ag purchase commitments whenever they work out a trade deal in the coming months.

The Pro Farmer Tour found a bean crop more along the lines of what the USDA had coming in with a 53 bu/ac estimate vs the USDA’s 53.6 bu/ac. Beans biggest problem right now has been lack of rain for pod fill but a few well timed rains down the stretch could lead to a massive crop. China really needs to show up as a buyer for beans to leg higher but they can get all they want from South America right now even though they are paying a premium to get them vs US beans. The funds have a neutral position on the market as they wait for news that could send the market any direction other outside of the $10 – $10.50 range it has been trading in the majority of the last 6 months. China still remains a cloud over the market with the Trump administration needing to get Ag purchase commitments whenever they work out a trade deal in the coming months.

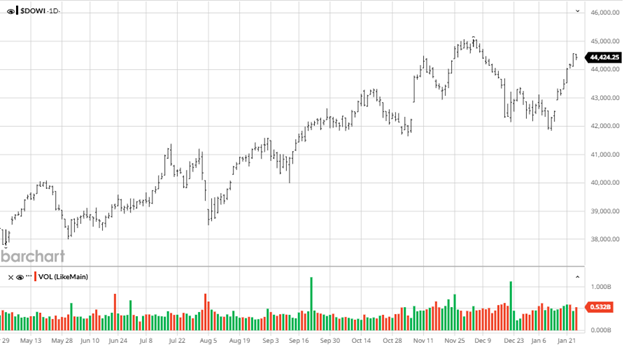

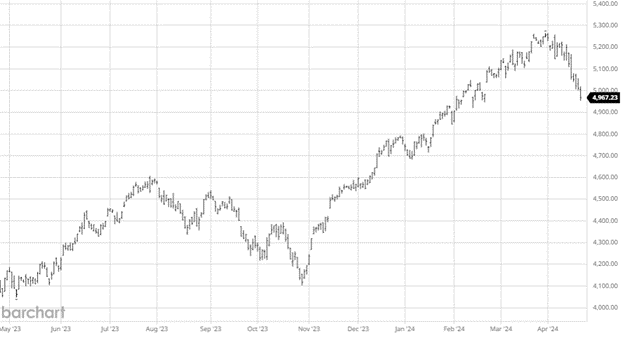

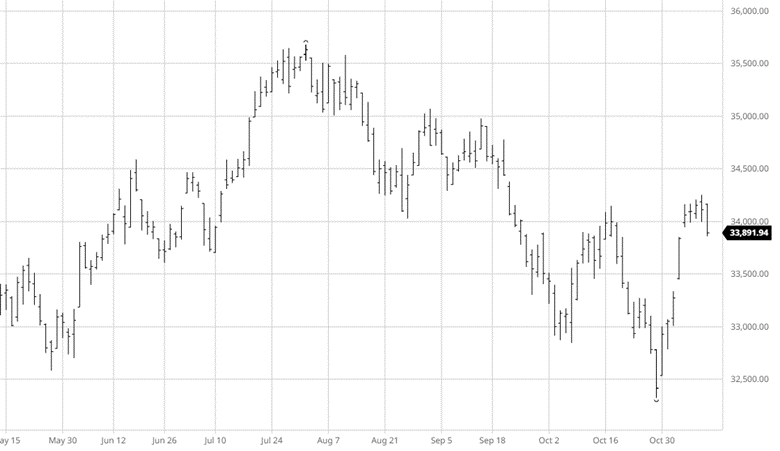

Equity Markets

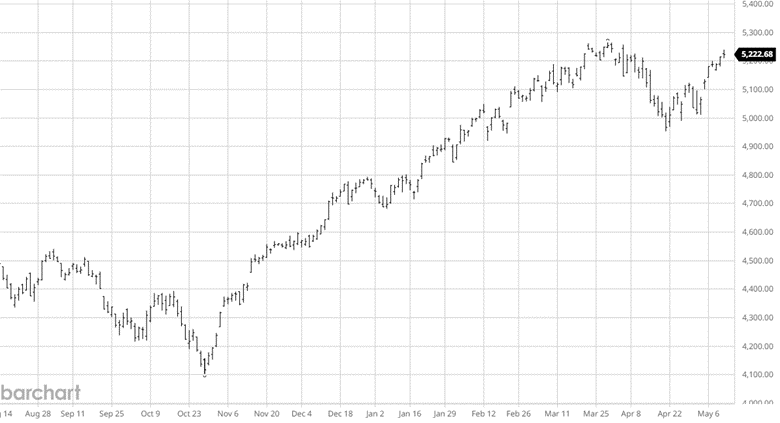

Equity markets continue to claw higher amidst pullbacks as earnings wrap up and AI and tech still drive the market direction. The Fed is expected to cut rates in September while the Trump administration’s attack on the Fed’s independence continues with Lisa Cook in its crosshairs currently.

Other News

- ADM plans to close a soy protein plant in Bushnell, IL.

- Brazil’s investigation into the Soy Moratorium (curbs Amazon deforestation) could threaten sustainable soy sourcing, with potential ripple effects in the global supply chain.

- Wheat has been relatively flat the last couple weeks.

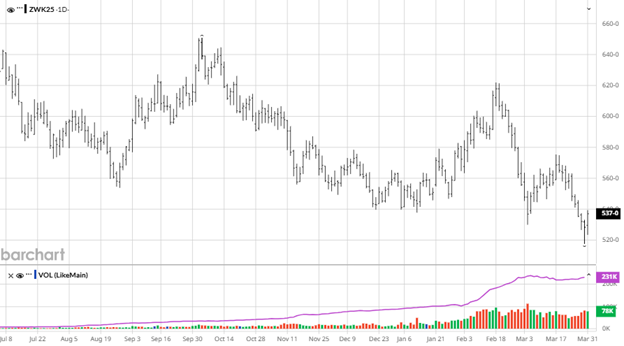

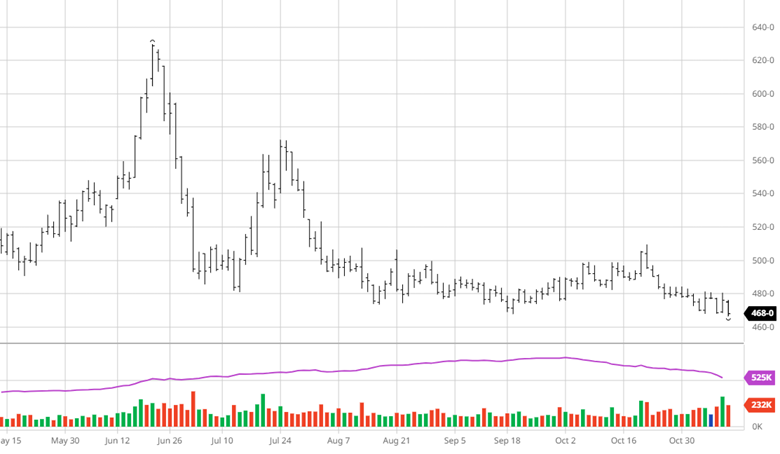

- Cotton continues to trade sideways waiting on demand to pick up.

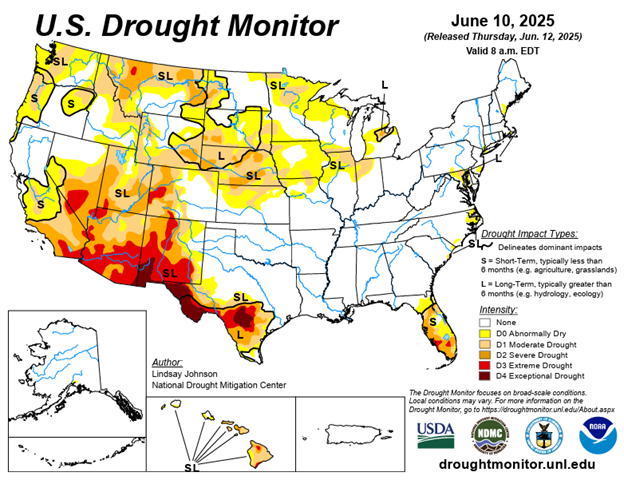

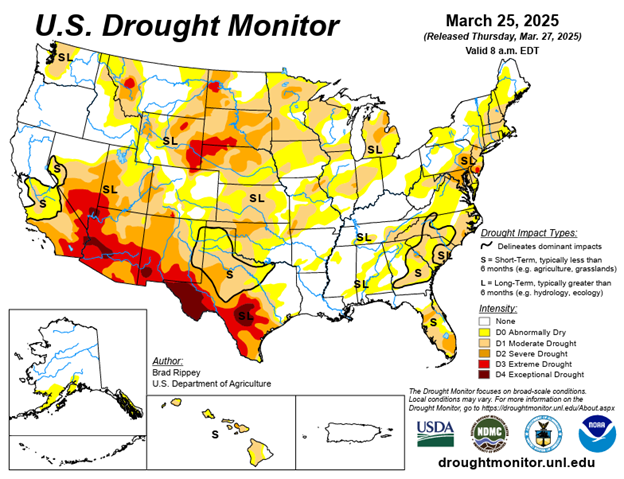

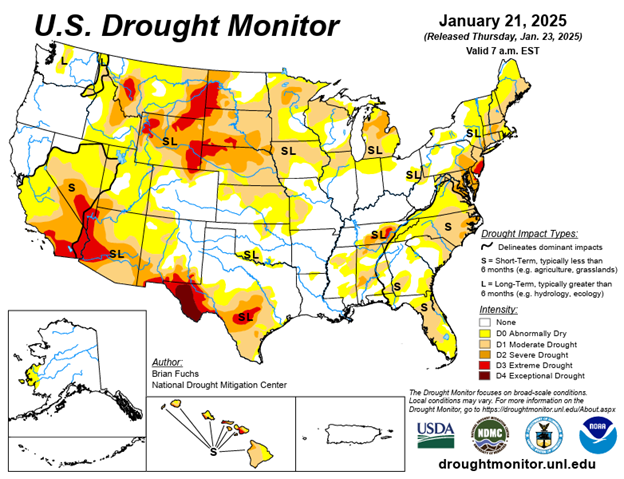

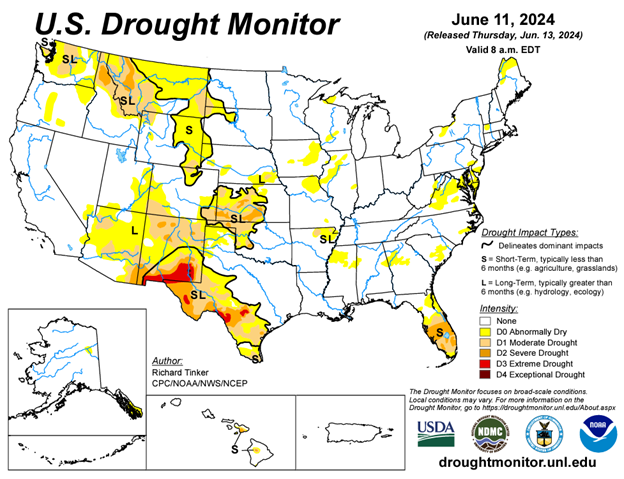

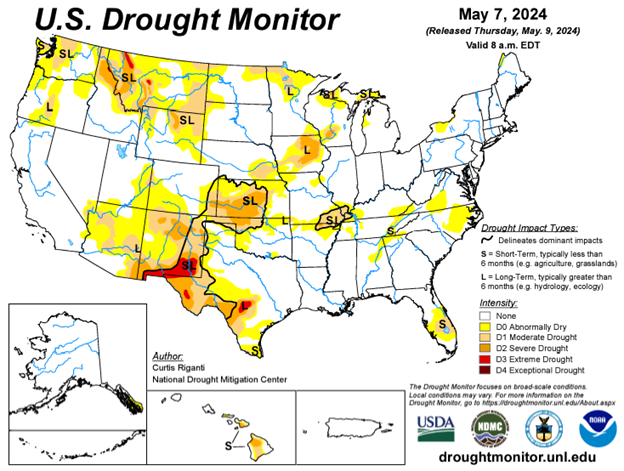

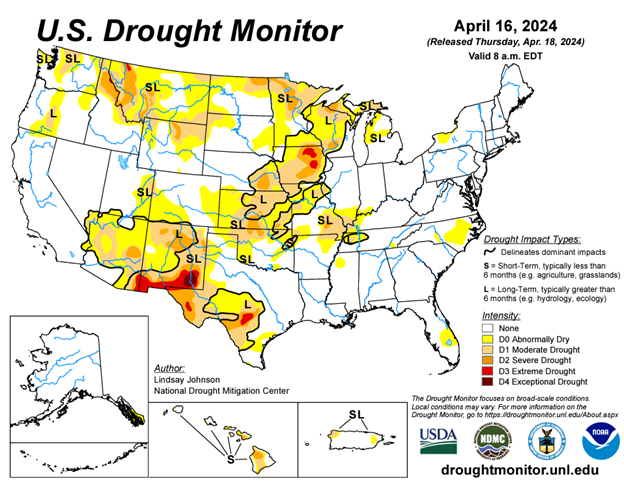

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.