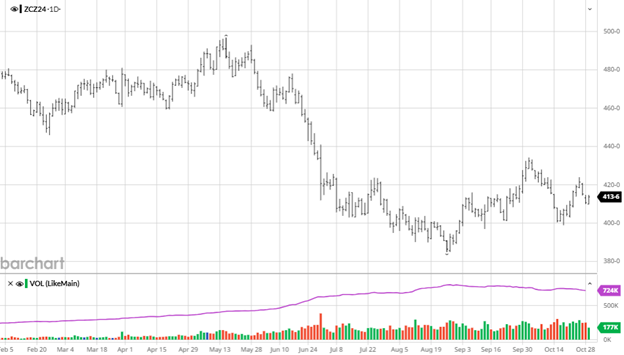

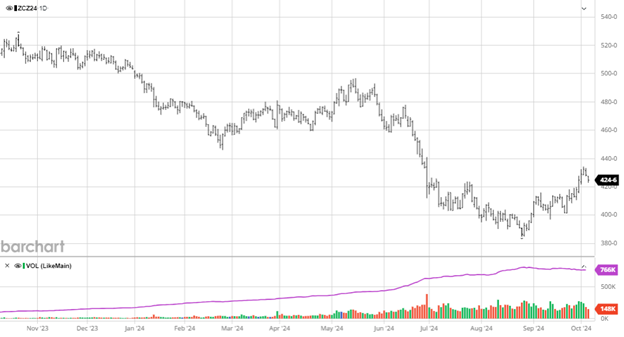

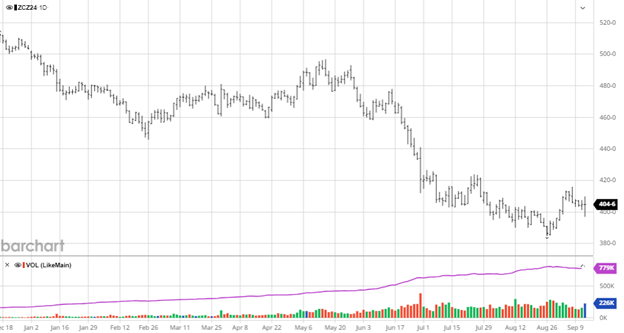

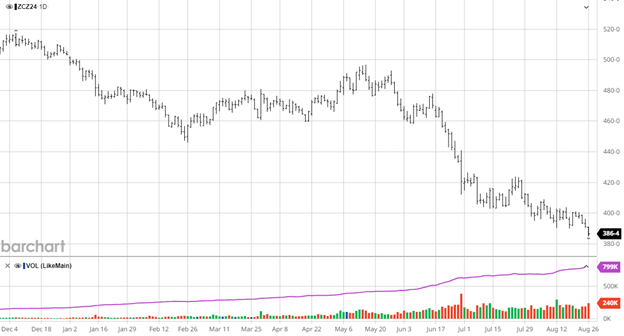

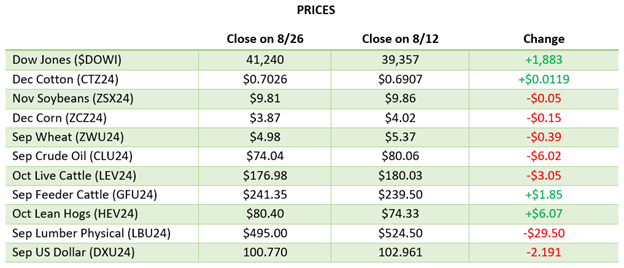

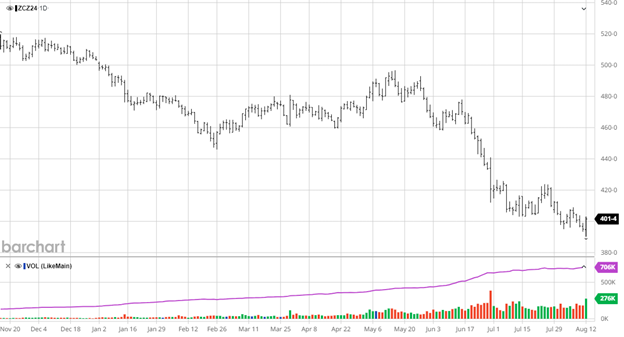

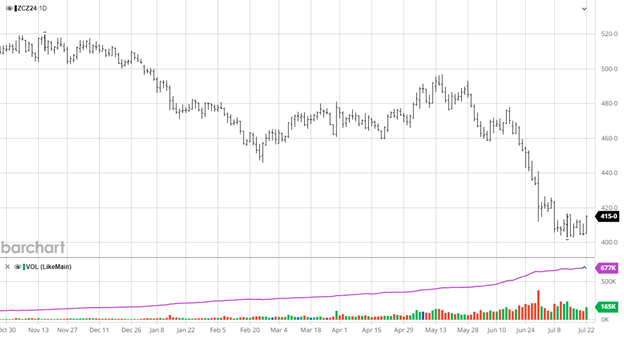

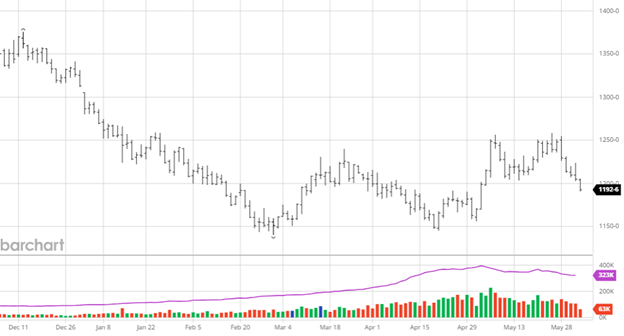

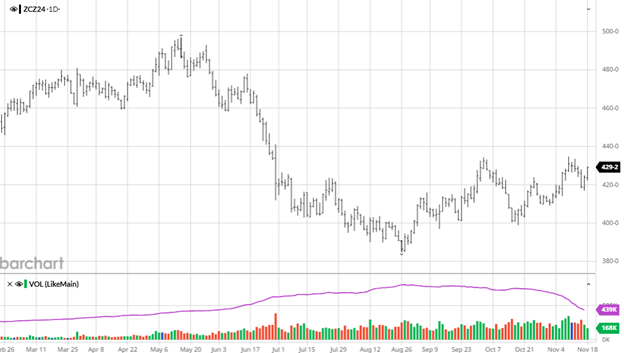

December ’24 corn rallied back to the $4.30-point last week, matching its recent highs from the start of the month. Corn’s 40+ cent rally from the August lows has been very welcome as harvest wrapped up and bins were getting full. Corn struggled to hold this level of trading for long a few weeks ago but with the December contract getting ready to expire and all the focus shifting to March the markets need some help to push to the $4.50 mark. Funds are long 550 million bushels of corn, the largest long position in 21 months. The November 8th USDA report had the ’24 US corn crop at 183.1 bu/ac, avoiding the fears of the USDA finding an even bigger crop and raising yields that would’ve sent the market lower. Exports have been solid but within expectations as post-election trade will involve countries positioning themselves ahead of the new Trump presidency.

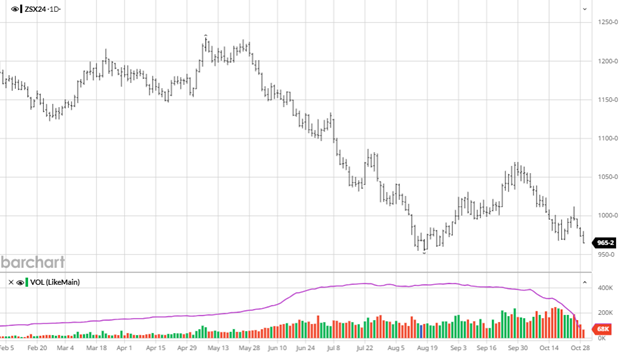

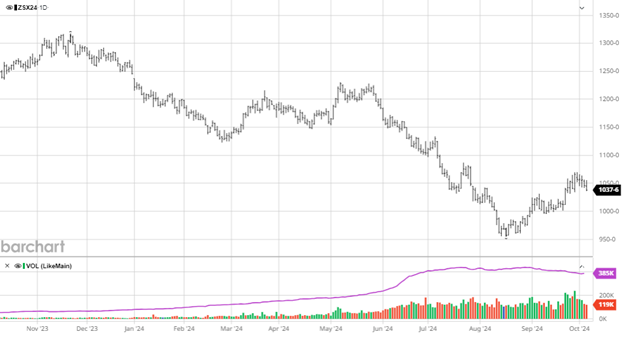

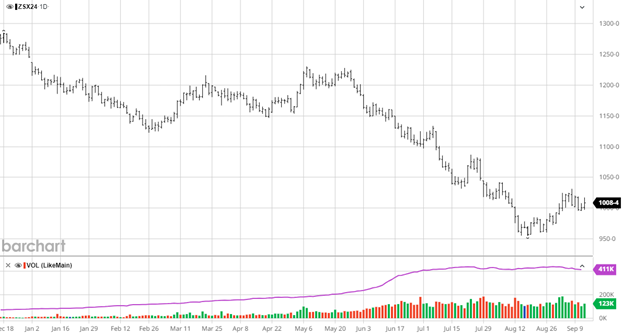

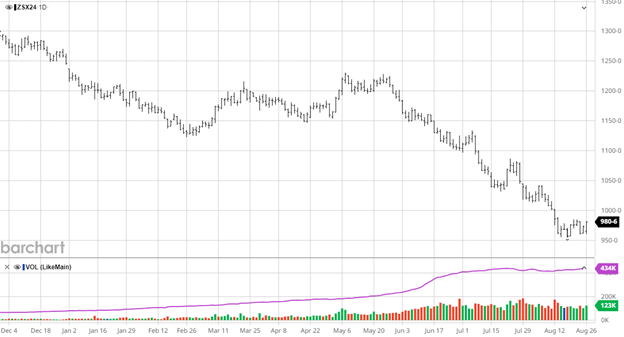

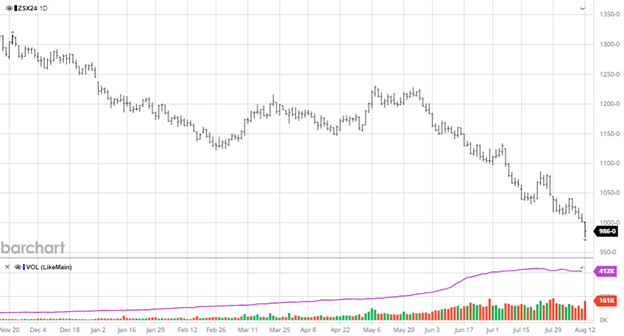

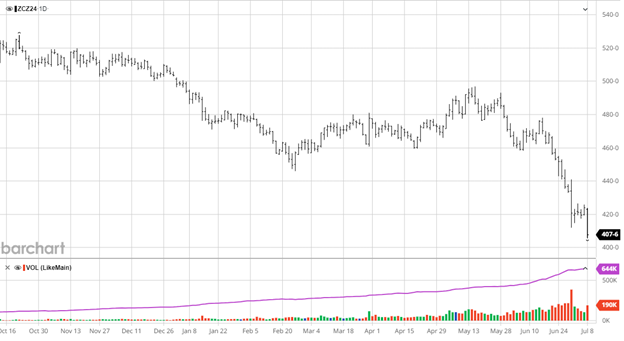

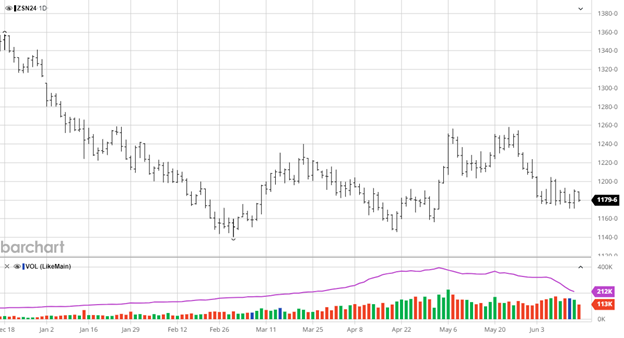

Soybeans recent rally was quickly given back with January soybeans trading just over $10. The recent lows in the $9.75 range appear to the where support is showing up as it has traded down to that range a few times but keeps bouncing back. The USDA had the US soybean production to 51.7 bu/ac, below the 52.8 bu/ac estimate the markets had priced in. While the market got an initial bounce from the report the fact that another trade war may be on the horizon with record bean yields in the US and South America, the supply and demand story is not friendly in its current state.

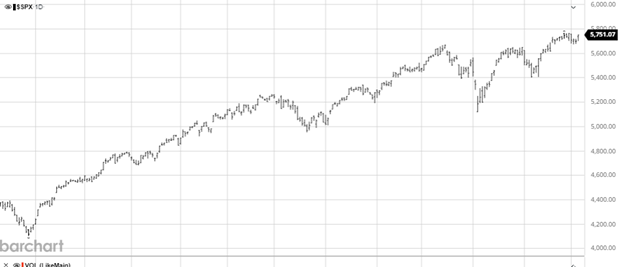

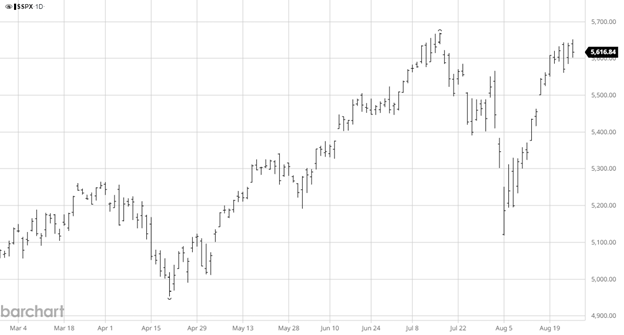

Equity Markets

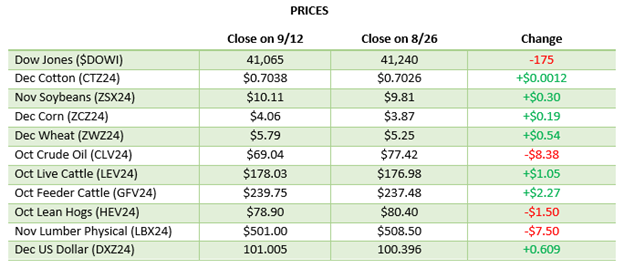

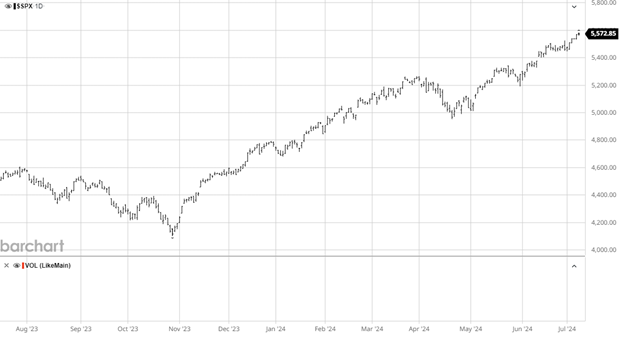

The equity markets rallied following the presidential election and have since given some back. While Trump is seen a market friendly, the “who will benefit?” is a big question mark as tariffs and promised lower government spending will have widespread effects. Republicans will control the house and senate but with some senators not high on Trump, he likely will need some help to do everything he wants (think Manchin and Sinema with Dems).

Other News

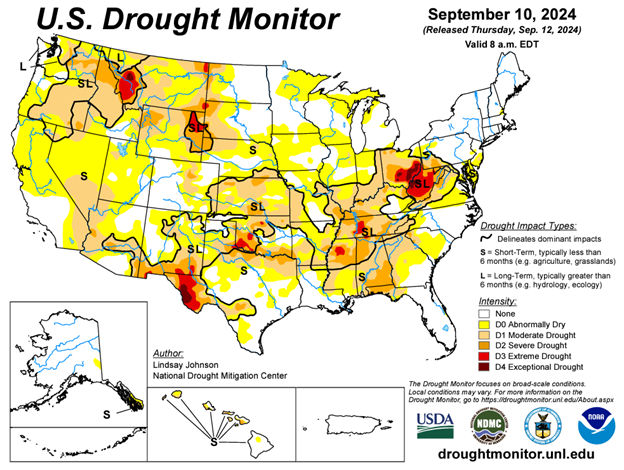

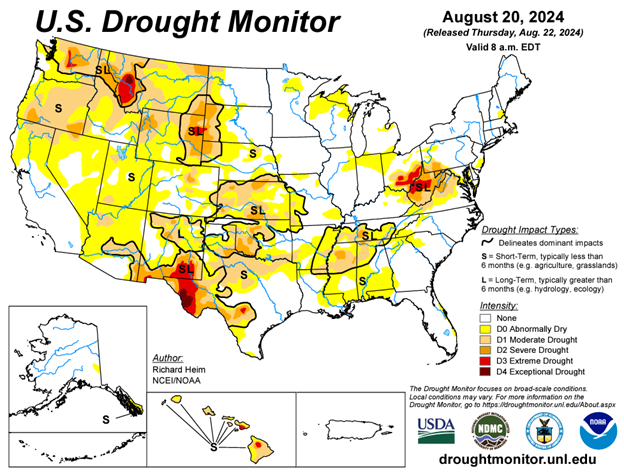

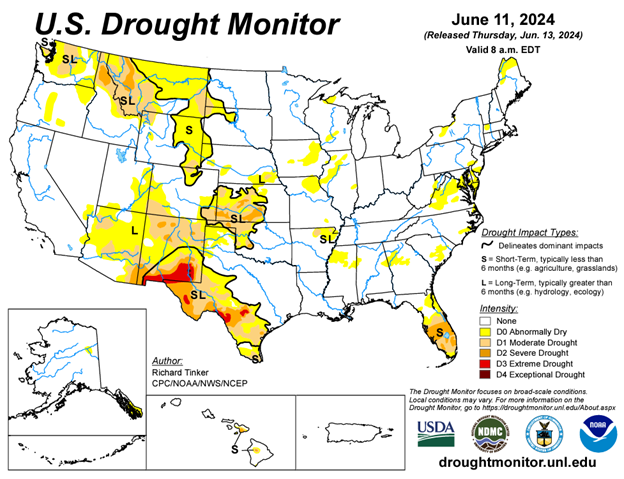

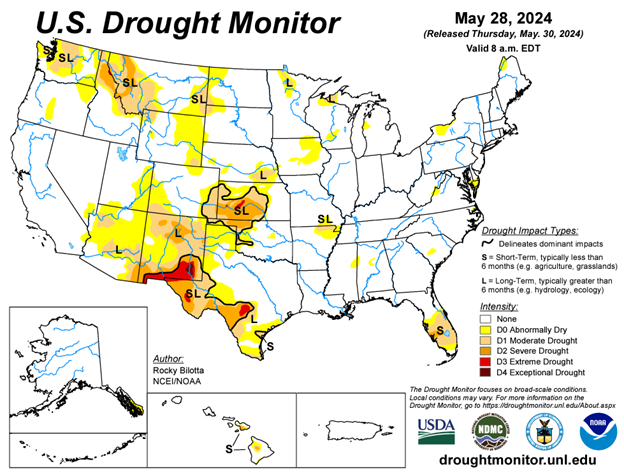

- South America is off to a good start with another record crop expected with the expanded acreage.

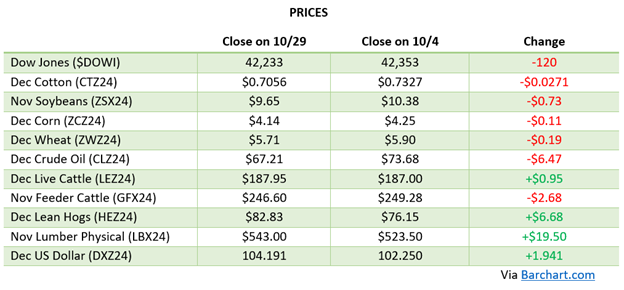

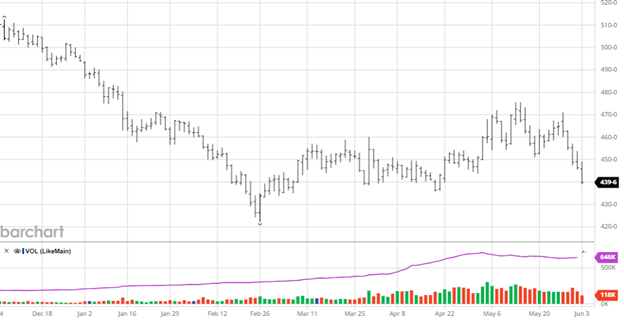

- Cotton has had a rough 2 months after falling below 70 cents with the recent low of $0.6626 squarely in the crosshairs.

- The USD has moved higher topping 106 following the election.

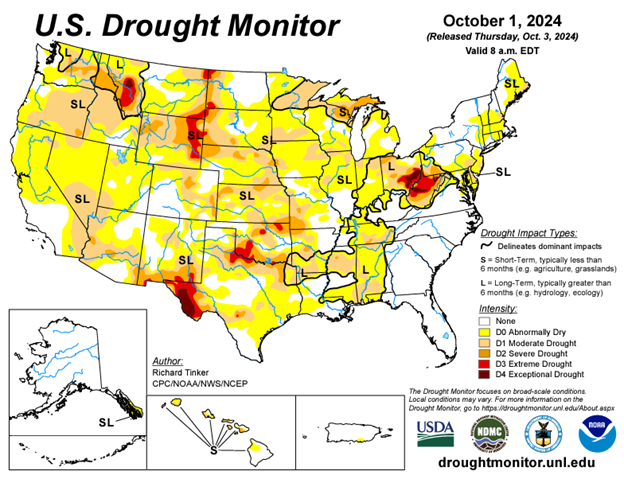

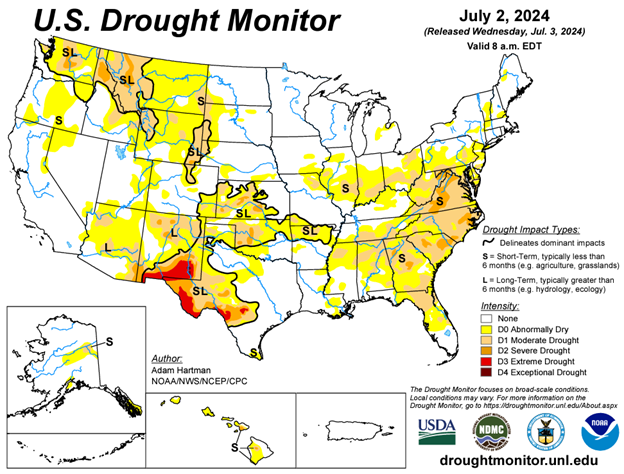

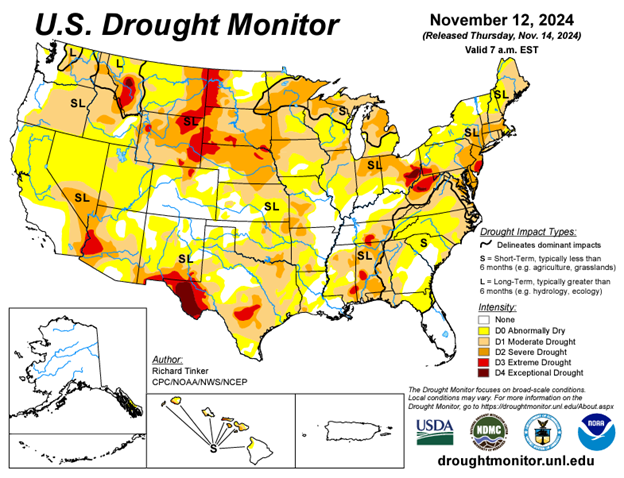

Drought Monitor

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.