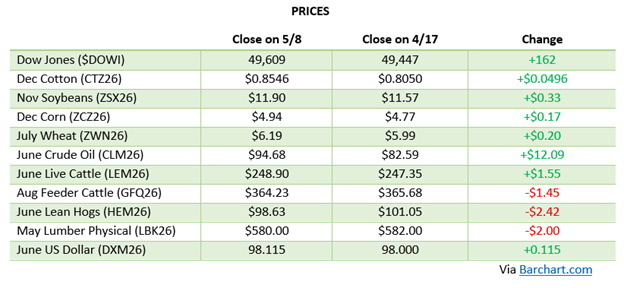

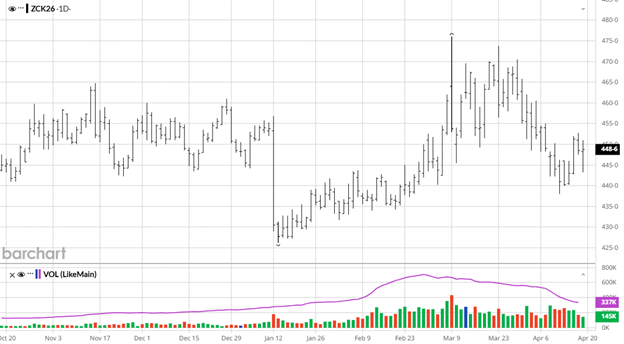

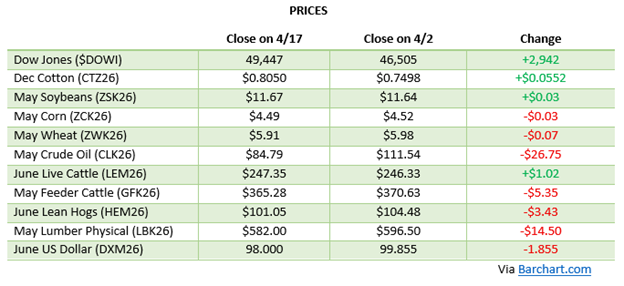

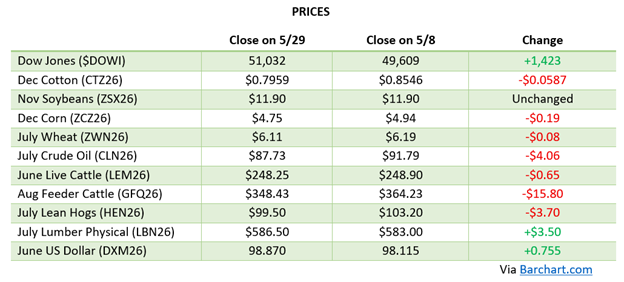

Corn has been a market defined by a tug-of-war between a bearish domestic supply picture and a geopolitical premium that refuses to fully disappear. Coming off the May 8th close, December corn had briefly flirted with the $5 level before pulling back as Iran peace talk optimism ebbed and flowed. The May 12th WASDE report, the first to include 2026/27 new-crop estimates, was the dominant event of the period. USDA pegged 2026/27 corn ending stocks at 1.957 billion bushels, down from 2.142 billion for 2025/26, a modest tightening but still well above comfortable levels. The initial reaction was muted, with the market already priced for a heavy supply picture. July corn futures settled in the $4.55 neighborhood in the days following the report, well off recent highs.

The real story in corn continues to be the fertilizer situation. Nitrogen prices, which spiked sharply when the Strait of Hormuz conflict erupted in late February, have only partially retreated from their peaks. Farmers across the country are scrambling for alternatives, manure, biofertilizers, and bio stimulants, but the economics remain challenged. This cost pressure has some analysts believing final planted corn acres could come in below USDA’s March intentions survey. Planting progress has been strong, with the week of May 24th showing approximately 89% of the crop in the ground, well ahead of the five-year average. Export inspections continue to run well ahead of last year’s pace, providing a supportive underpinning, and a flash sale of nearly 19.4 million bushels to Mexico was announced mid-month. If you can sell corn at profitable levels above your cost of production, it remains a reasonable conversation to have with your merchandiser given the uncertainty that still lies ahead.

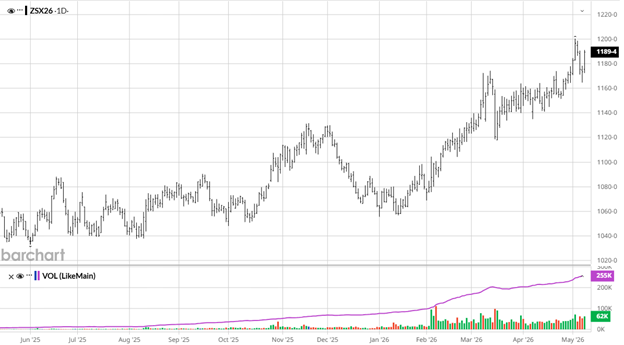

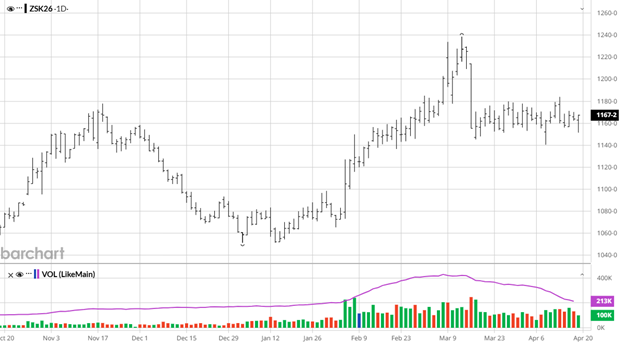

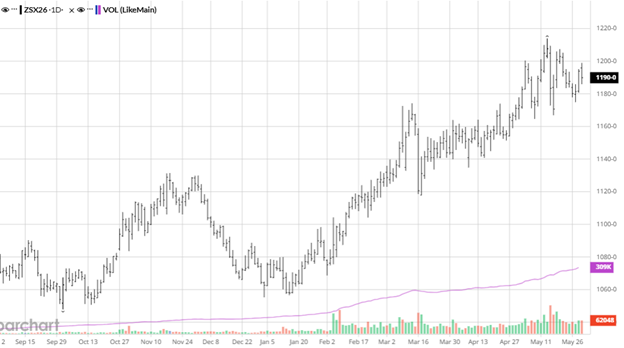

Soybeans were the standout performer of the period, posting their most significant rally in months following the May 12th WASDE. USDA surprised the trade by projecting 2026/27 soybean ending stocks at just 310 million bushels, a full 30 million below the 2025/26 figure and roughly 45 million below analyst expectations. The primary driver was a massive projected increase in crush demand, with USDA forecasting 2.750 billion bushels of crush for 2026/27, up 120 million from the current year, on the back of exceptional crush margins and booming soybean oil demand as a biofuel feedstock. Board crush margins holding well above $3 per bushel remain historically exceptional and are lending strong support to nearby contracts. July soybean futures spiked to two-year highs in the wake of the report.

Soybeans were the standout performer of the period, posting their most significant rally in months following the May 12th WASDE. USDA surprised the trade by projecting 2026/27 soybean ending stocks at just 310 million bushels, a full 30 million below the 2025/26 figure and roughly 45 million below analyst expectations. The primary driver was a massive projected increase in crush demand, with USDA forecasting 2.750 billion bushels of crush for 2026/27, up 120 million from the current year, on the back of exceptional crush margins and booming soybean oil demand as a biofuel feedstock. Board crush margins holding well above $3 per bushel remain historically exceptional and are lending strong support to nearby contracts. July soybean futures spiked to two-year highs in the wake of the report.

The rally has since come under some pressure, with planting progress running exceptionally fast, 79% of intended soybean acres were in the ground as of May 25th, ahead of the 68% five-year average and significantly above last year’s pace. Brazil’s Conab and USDA left South American production estimates largely unchanged, with Brazil expected to produce another enormous crop in 2026/27. Year-to-date U.S. soybean export shipments trail last year’s pace by about 21%, which remains an overhang on any sustained rally. Still, with domestic crush demand as strong as it has been in years, beans have a fundamental story to tell that corn simply does not right now. The long-awaited Trump-Xi meeting, which had been delayed repeatedly, amid the Iran conflict negotiations, remains a potential catalyst for a fresh round of Chinese buying that could push beans meaningfully higher.

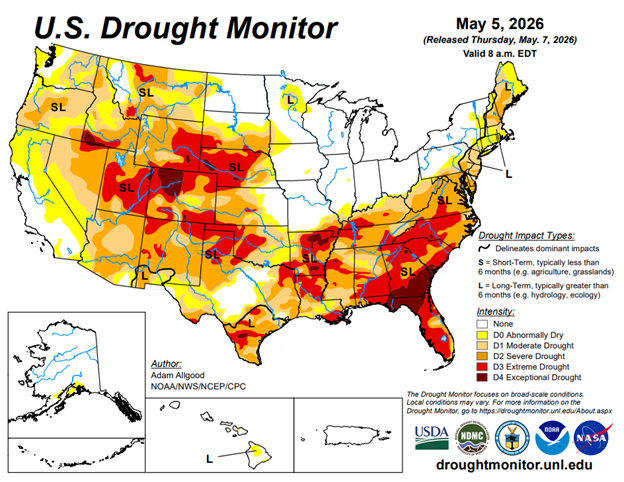

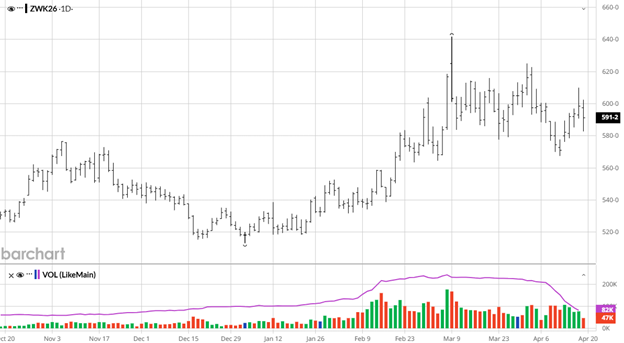

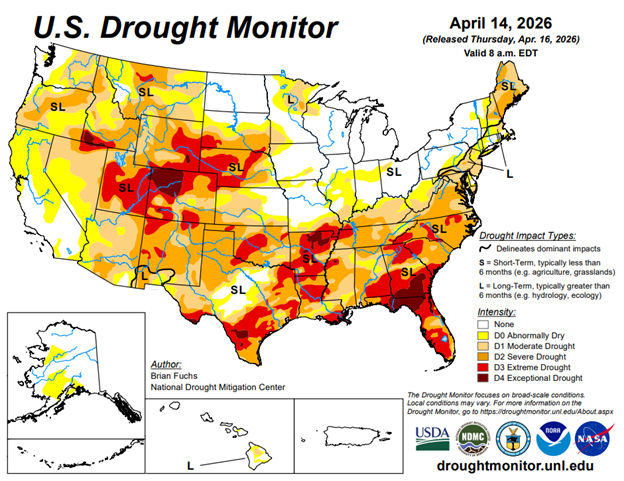

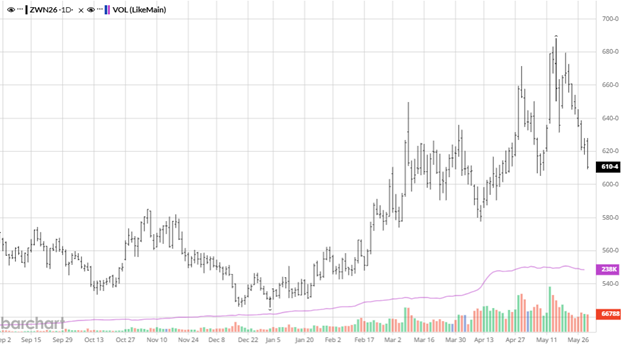

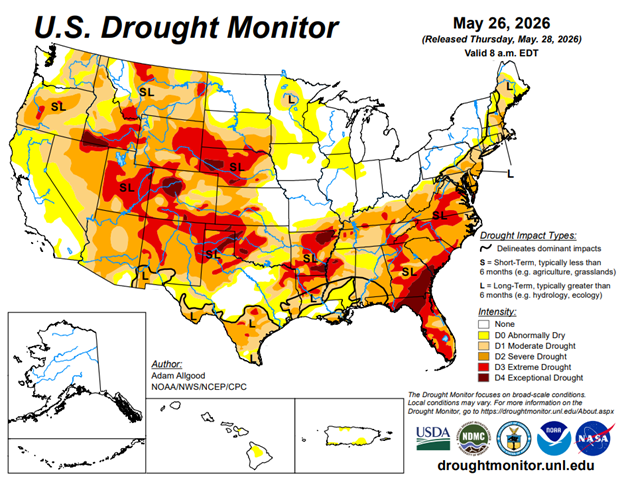

Wheat has been the most compelling story in the grain complex over the past three weeks, and for good reason. The May 12th WASDE delivered a shocking number: USDA projected 2026/27 U.S. winter wheat production at just 1.048 billion bushels, down 25% from 2025/26 and the smallest domestic wheat harvest since 1965. Severe, persistent drought across the Southern Plains, particularly in Kansas, Colorado, and Nebraska, has devastated crop conditions. At last check, only about 30% of the winter wheat crop was rated good or excellent, with maturity running well ahead of schedule due to extreme dryness. The recent volatility off contract highs took a big chunk out of the market but still holding over $6 in July wheat.

Equity Markets

Equity markets have continued their remarkable run, with the S&P 500 and Nasdaq posting new all-time highs during the period. The AI trade remains the dominant factor with AI being the dominant story during earnings. While PCE inflation came in at 3.8% for April the markets shrugged it off mostly. Some AI related names have gone parabolic in the last month creating a tough environment if you want to own those names.

Energy Markets

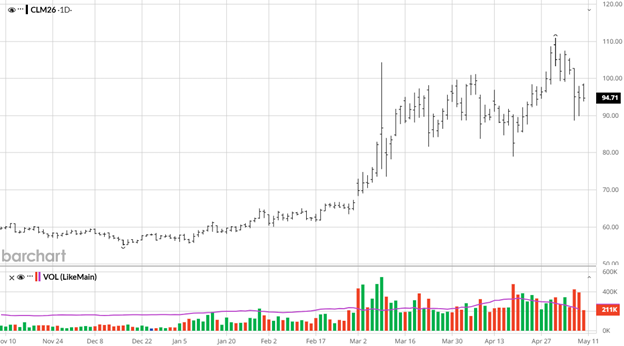

Crude oil remains the macro wildcard for the entire ag complex. WTI has been in a volatile, two-directional range throughout the period, with prices whipsawing on every Iran headline. Peace talk optimism has pushed oil down meaningfully from its April peaks above $110 per barrel, with analysts at UBS noting that crude has fallen roughly 20% from its 2026 highs on ceasefire negotiations. However, Iran crude loadings in May have run below 0.3 million barrels per day, a dramatic collapse from March’s 1.7 million barrels per day, meaning actual physical supply has not improved despite the diplomatic noise.

Other News

- Wheat’s surge to two-year highs has been the headline, but cotton has continued its own quiet rally. Hedge funds turned net bullish on cotton for the first time in two years this month as the war-driven surge in oil prices increased the appeal of natural fiber over synthetic alternatives like polyester and nylon, which require petroleum inputs. Producers who can lock in profitable margins at current levels while maintaining upside participation should be exploring their hedging options.

- Iran is reportedly reviewing a formal U.S. peace framework that includes reopening the Strait of Hormuz to international shipping. Markets are cautiously optimistic but skeptical.

- The EPA’s finalized 2026–2027 Renewable Fuel Standard volumes, set at record highs, continue to provide a structural floor under corn and soybean oil demand. Soybean crush is already running at historic highs in response, and these RFS volumes ensure that domestic demand will remain exceptionally strong regardless of where export flows go.

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.