Recap:

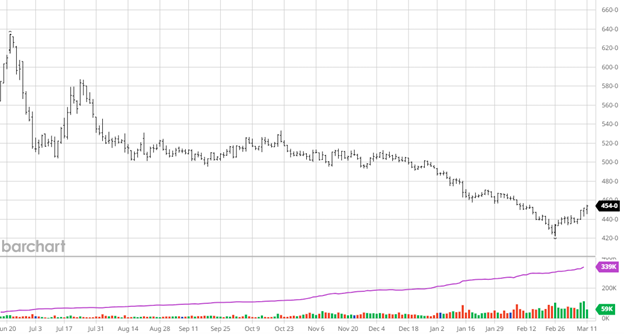

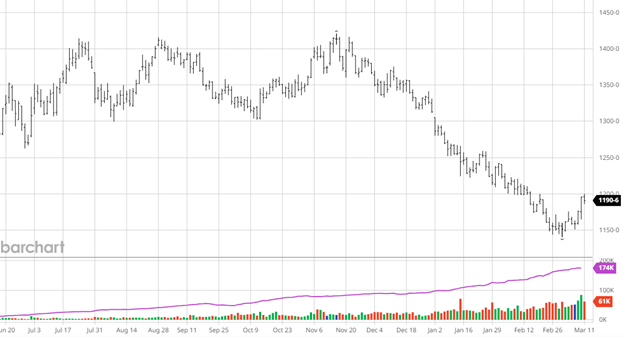

Mixed reviews. That is the industry’s opinion of this market. What we saw in futures last week was slightly more positive than mixed. Futures are showing signs of a turn. The market closed slightly higher for the second week as print continued down. It also works higher on low volume. That indicates a muted computer trade down here. The fundamentals are the focus. The funds are short but didn’t add much for the week. This lack of momentum puts them on the sidelines. So, with all the blah in the market, I would expect more of the same this week, but that’s not lumber. One side will try to push the market. Today, it is more likely that the longs will do the pushing, but never count the funds out. The cash market is getting better, albeit from some very low levels. That creep should support futures. There are still eight long sessions until May expires, so volatility could be an influence.

Technical:

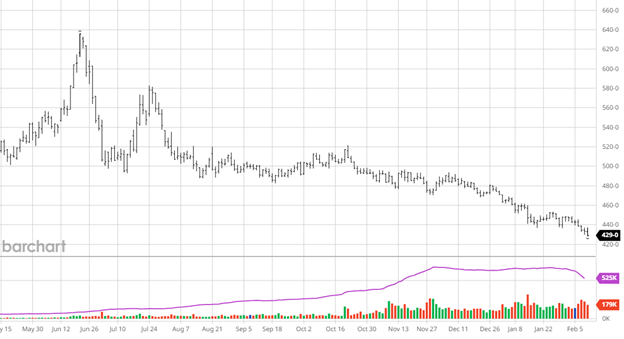

The tech picture is still no help. We see better momentum signs and a slightly higher trend but no confirmation of direction.

There are two key focal points. The first is the upside objective of 556.60, which is the 38% retracement of the move. A close over it may cause the short funds to start exiting. That push sends it to the 200-day moving average at 566.80, setting off another round of short-covering. All of a sudden, the futures market is at $600.

The other point is the low at 511.00. Here, the opposite happens, and the computers kick into sell mode. Futures fall to $480, and the cash market shuts off.

Your risk model should lean towards higher prices and hope it happens. For two years now, the market has never signaled an end to the basis opportunity. It still hasn’t.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636