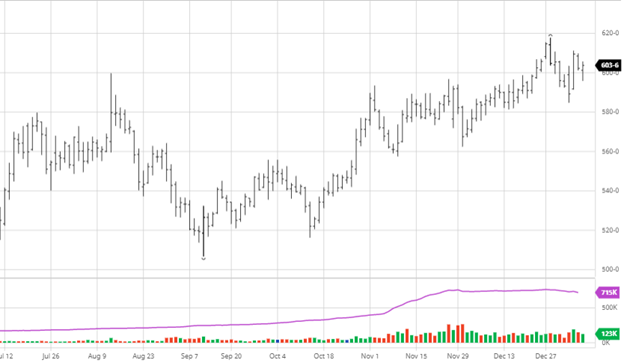

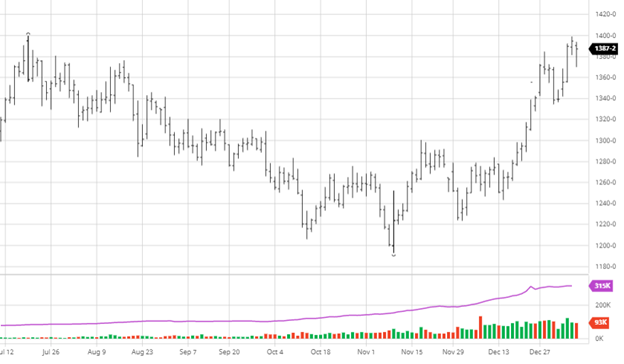

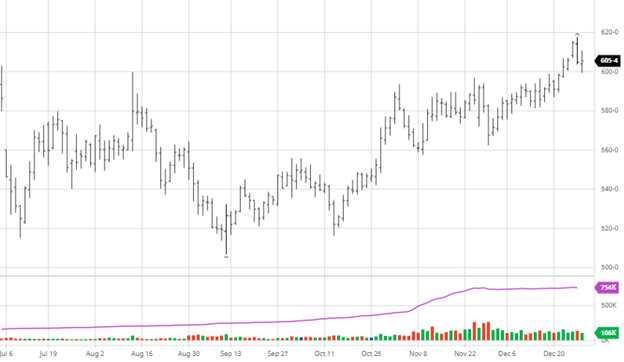

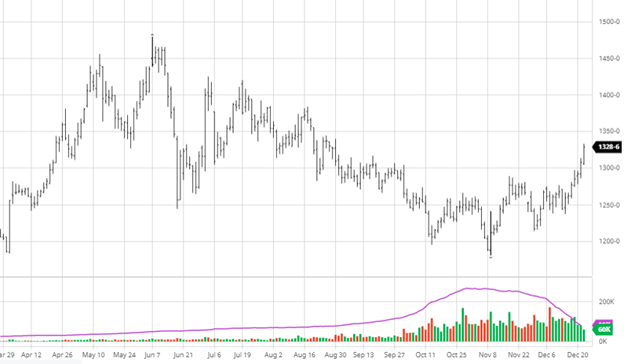

It’s hard to believe that this market has reentered the hyperbole dynamic we saw last year when the market lacked any restraint in upward pricing. The market bottomed on November 2nd at $606 and has gone straight up since. On Friday, the March contract made a new high of $1,250. That is a run of over 100% during the holidays. So, what are the issues causing these spikes? First is the massive contraction of this industry, creating a buy pattern that is out of balance. There are fewer players in the pipeline, making it consistently tight. The other is the new two-week to 30-day pricing that keeps everyone in the market almost daily. A quick summary of today’s dynamic is that when demand is good, there is a constant need to buy, and when demand slows, there is no need to buy under the current model. We started with the latter this time.

The need to buy throughout the 3rd quarter dropped nearly 60%. The new model of only buying when needed and only buying an item that will ship caught the market short. The previous models always had a buying program in place as prices fell, and these guys don’t. If the market slowly turns, there should be enough inventory at the mill side to keep costs balanced. As we saw in November, the slowing of production and shipment issues caused a bottleneck overnight. The market now needs to settle to ease the pressure on prices.

Today, the issue in front of the industry is that they bought great at $700 then added to the pile at $1,000 but are still averaged well. The next time they step up to the trough price will be $1,200, which is off their charts for breakeven.

Let’s Get Technical:

This type of market doesn’t relate well to momentum indicators. That said, March made a new contract high at $1,250 with an RSI of 76.70%. There is a lot of room to the upside. The math keeps bringing the value (volume) areas into focus. The two areas are $1,250 and $1,550. A good indicator on the last run was the Fib extensions. Today the 1.38% move in March is $1497. The technicals are building for a push to that level, and there isn’t much pushback from the trade. It will take a lot of energy to get there, so a pullback in some fashion would be efficient at this point of the cycle.

Weekly Round-Up:

You heard it here first… Because of global economics, if this market goes up to the $1,500 level, it will take out the historic highs, and the momentum build-up will be too great to cool. So, there should be minor issues out there of prices going higher. If you asked us if we would buy it today, we’d say, “I wouldn’t buy it with all of Doug’s money.” You can’t discount the ease of producing this commodity. There is no fundamental cause for this commodity to be over $1,000, and we just have an incredibly inefficient marketplace today.

Open Interest and Commitment of Traders

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

https://www.cftc.gov/dea/futures/deacmesf.htm

About The Leonard Report

The Leonard Lumber Report is a new column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Before You Go…

The 2021 U.S. grain crop has the potential to be one of the largest on record. Where did all the yield come from, what areas were the hardest hit, and why on God’s green earth are grain prices still so high?