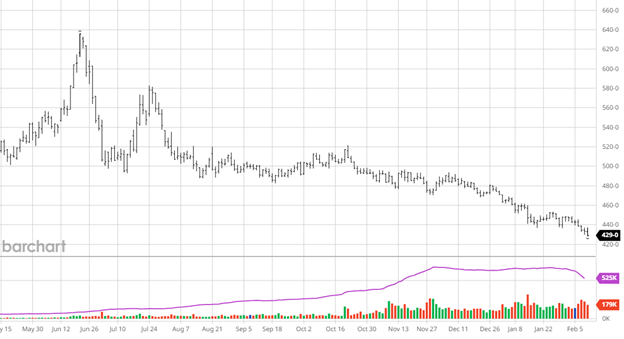

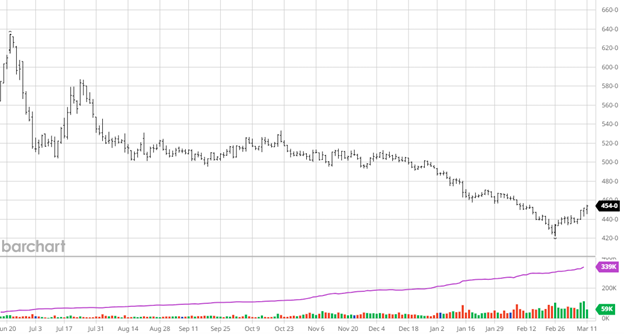

Corn has managed to peel off its recent lows despite no major changes in the market. South America’s harvest is moving right along, while the crop appears to be smaller than initially anticipated, the increase in acreage seen will still likely make this a record crop. The March USDA Crop Report gave a little ground in their estimates for South American production of soybeans but slightly raised the estimates for production in Argentina for corn. These changes were inconsequential to any market movement as CONAB numbers this week will be the next data to give the market more direction.

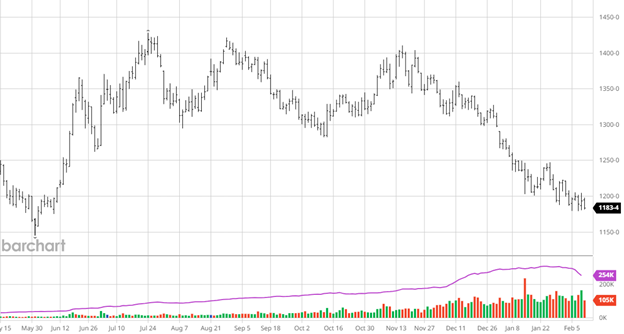

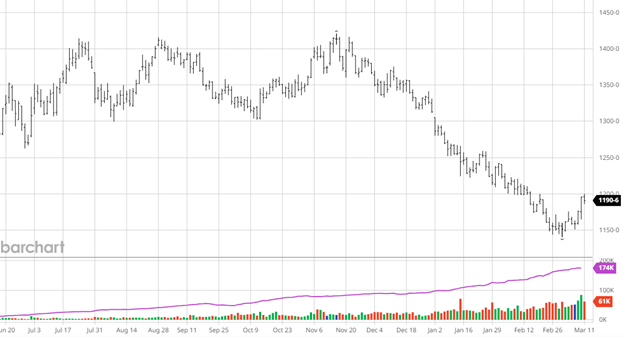

Soybeans got some good, but not great, news in the USDA report with the USDA slightly lowering the production in Brazil. While many private estimates in South America are still lower than the USDA’s, this shows that the USDA believes the others may be right but are not yet willing to give all their production back. This week’s CONAB numbers will be worth keeping an eye on. Basis has been slowly rising during harvest, hinting at this crop being smaller than expected. Continued gains following Tuesday’s report would be welcome as the further we can put the lows behind us, the better.

Soybeans got some good, but not great, news in the USDA report with the USDA slightly lowering the production in Brazil. While many private estimates in South America are still lower than the USDA’s, this shows that the USDA believes the others may be right but are not yet willing to give all their production back. This week’s CONAB numbers will be worth keeping an eye on. Basis has been slowly rising during harvest, hinting at this crop being smaller than expected. Continued gains following Tuesday’s report would be welcome as the further we can put the lows behind us, the better.

Equity Markets

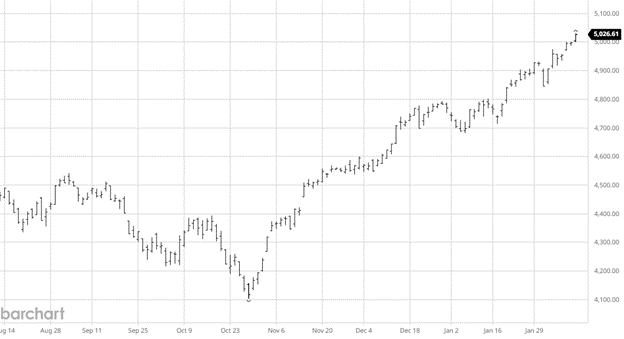

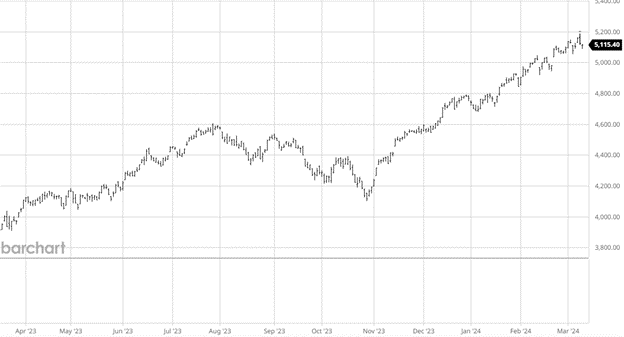

The equity markets continued their grind higher with a broadening in recent weeks to other names outside of the Magnificent 7. With slower job growth and a slightly higher unemployment rate, the Fed appears to be getting what they aimed for in a soft landing, but inflation is still sticky. The Fed may begin cutting rates in the second half of 2024.

Other News

- The stock market continues to make all time highs while AI stocks have driven this rally, some rebalancing appears to be occurring.

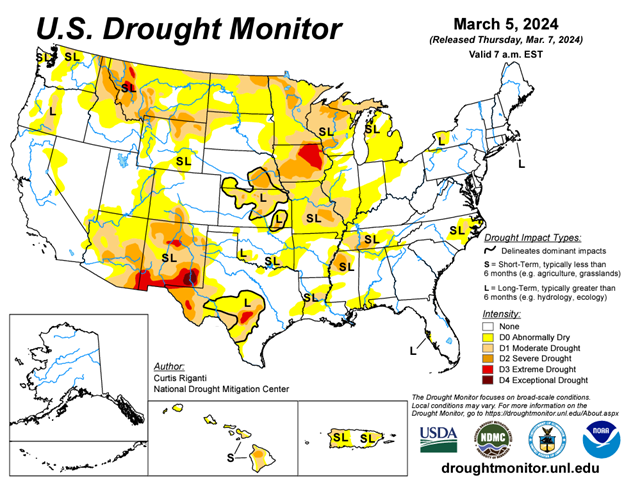

Drought Monitor

Here is the current drought monitor as we head toward planting with subsoil moisture a focus.

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.