The 2021 U.S. grain crop has the potential to be one of the largest on record. Where did all the yield come from, what areas were the hardest hit, and why on God’s green earth are grain prices still so high?

Today, we are joined by several RCM Ag Services grain markets experts from around the country to catch up on a post-harvest update and share an outlook for production and marketing in each of their respective regions for the remainder of the 2021 marketing season and the upcoming 22 crops.

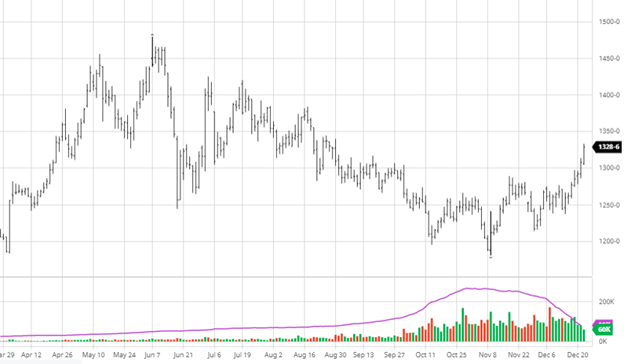

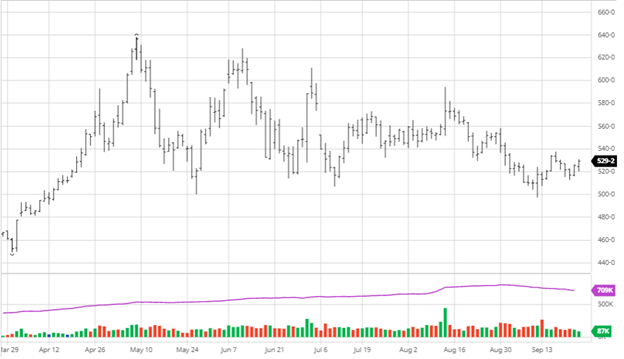

Since early December, corn has had a great run as South America’s dryness continues and delays planting in some areas. The corn crop is only about 60% planted in Argentina, which is the slowest pace on record for late December. Anything planted after January 10th will probably experience some yield drag. Their planting rate is on par with last year, but the weather has been far dryer and looks to continue going forward. As you can see in the chart below, March corn has rallied 90+ cents since early September. With continued strong basis and raises at prices, farmers have been given a gift but when the farmers choose to claim the gift and how long the gift stays available is another question. If Argentina and Brazil stay dry, this rally could continue, and we could retest the summer’s highs. Ethanol margins shrunk, and crude fell but remain at much higher than average levels, which will also support corn.

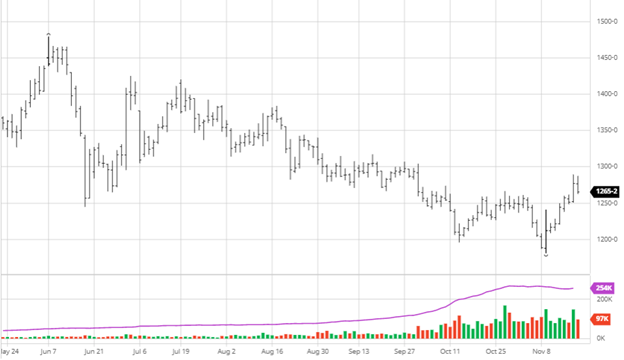

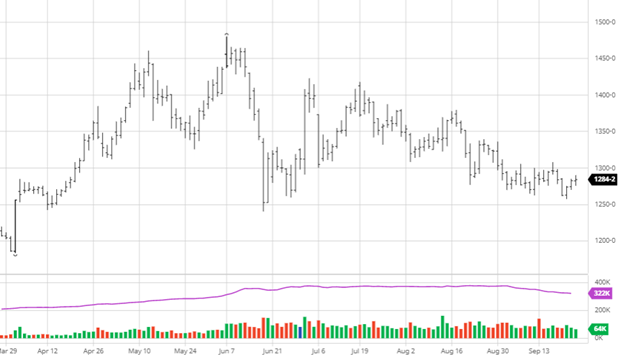

Soybeans, like corn, have enjoyed a nice rally as South American weather issues cause some worry. This week, Brazil’s bean crop had its production estimate lowered by 3 million metric tons by Parana’s crop analysis firm, Deral. While Brazil is still on pace to produce a record crop, it is not expected to be as large. They increased planting this year, so a larger crop is expected in Brazil, even with some headwinds. The basis is holding steady around the country for beans as we head into the new year. Beans and corn are likely to move together leading up to the January USDA report.

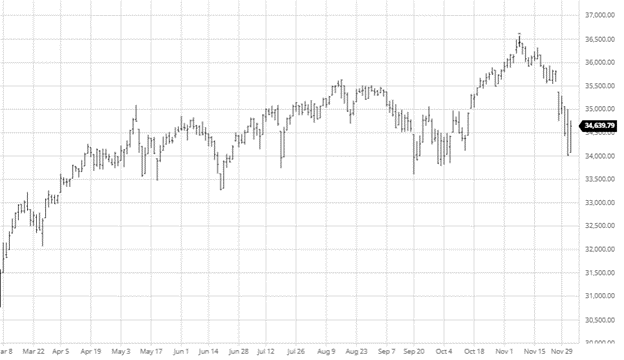

The Dow had a flat week and a half with volatility due to the Omicron variant having it all over the place with several large down days followed by a good bounce. The Omicron variant’s spread has been worrisome as restrictions start to come back into play in major cities. It will be important to keep an eye on this around the holidays as we also hope to see the “Santa Clause rally.” Senator Manchin also stopped President Biden’s BBB plan as he will not vote to approve it in its current form.

Podcast

Commodity prices have perpetually soared for the past year and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

Volatility was the name of the game this week as every market experienced it from, grains to equities. Corn partook in the excitement, as you can see from the chart below. Important to note is following the small rally in the past couple of days to get back to the levels we saw before Thanksgiving. Wheat was a big winner Thursday and pulled corn with it on the intensifying issues with Russia and Ukraine. If wheat rallies, expect it to pull corn with it even on limited corn news. The La Nina pattern continues to form in South America as southern Brazil remains dry, and forecasts have that continuing. Another non-corn-specific factor to keep an eye on will be energy prices, as ethanol production will depend on how the omicron variant will/could affect US travel into the winter and holiday season.

Soybeans, like corn, saw a bounce the last couple of days to get back to close to the range we were in pre-Thanksgiving. The bounce has brought us back in the range we were trading for most of October, which seems like a good place for the market to hang around when there is a lack of news. Exports continued but were on the lower end of expectations this week, while soybean meal and oil were as expected. If beans could close this week over the 20-day moving average, that would be supportive for bulls who are looking for good news. As harvest is wrapped up, all eyes turn to South American weather and their crops this year.

Crude oil has sank following the Thanksgiving holiday as concern over the new Omicron variant, and its impact on demand hit the market. While these concerns are valid as much is still unknown, the largest problem that seems immediate to demand will be air travel and international travel causing, less jet fuel demand. As of right now, it does not appear to be worrying many Americans, but as more cases are found, we will see how it will affect demand. OPEC+ countries also announced they might cut output if demand falls due to the virus, leading prices back higher.

Natural Gas prices have also faltered this week as a warmer U.S. winter is expected to occur, requiring less NG for heating. Diesel prices have also fallen a lot this week following the Omicron variant news and presents farmers with an opportunity to hedge their fuel needs for next year.

The Dow experienced a lot of volatility this week as news of the Omicron variant in the U.S. and more places worldwide spooked some investors. The reports are that it only has caused mild symptoms, which is good, but the reaction was not of fear of the virus itself but how the governments will respond with potential lockdowns and travel bans soon. On Thursday, the strong bounce-back shows that investors are still eager to get in the market, so any large pullbacks will be met with buying if it is seen as a jerk reaction, but any longer lasting weakness could be seen as a correction. The down-trend of the last week has made some investors worried and moved some to the sidelines while we see what happens. Powell will stay as head of the Fed and said they might start tapering and raising interest rates sooner rather than later as inflation does not appear to be transitory.

For the past year, commodity prices have perpetually soared and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

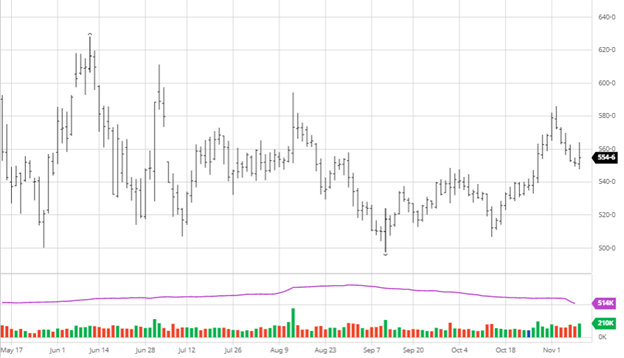

Corn has seen a good bounce since the Nov 9 USDA report and has traded relatively flat the past few days despite some intraday volatility. There was no specific market-moving news to fuel this rally but tidbits here and there to help fuel overall positive sentiment. IHS Markit updated their acreage for 2022 planted acres estimate with corn coming in at 90.8 million acres, 2.5 million lower than 2020. Ethanol production stays hot as the weekly grind rose to 312 mbu, up 7 from the previous week and well ahead of the USDA estimate for the year. With increased input costs going into 2022, the decrease in acreage makes sense, as balance sheets will be tighter. As harvest nears the end, eyes turn to South American growing conditions for the months ahead.

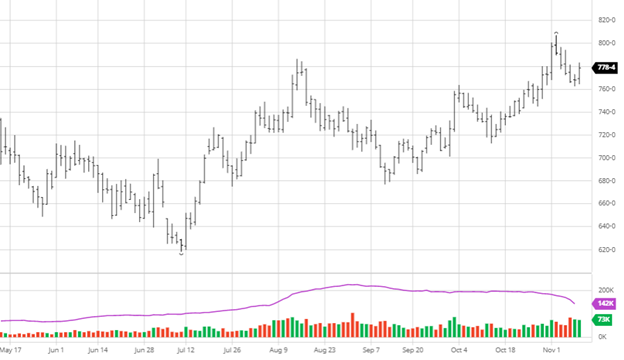

Soybeans, like corn, have seen a solid rally since the USDA report. Soybeans continued their rally on Thursday until the EPA announced they would release their renewable fuel mandates by the end of the week. As the Biden administration has not been much of an ally for the ag sector, the decline on the coming news makes sense. Soybeans had decent exports this week as buyers keep showing up in the market even as prices trek higher. Continued demand from exports will help support beans, and it will be interesting to see how many beans get stored and who took advantage of higher prices with forward pricing. We will see this play out in the cash & basis market come the spring, but we expect most farmers to store corn for now. IHS Markit estimated the 2022 bean acreage to be 87.9 million acres, 700,000 acres less than 2020.

The Dow struggled this week as earnings continue to come in, but market volatility seems to be expected with the holiday season coming up. The Fed can still raise rates this year, and the Biden administration has not yet announced their nominee to head the Fed (either keeping Powell or someone new).

Cotton

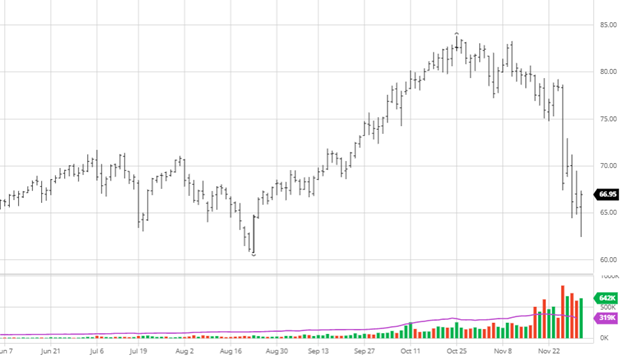

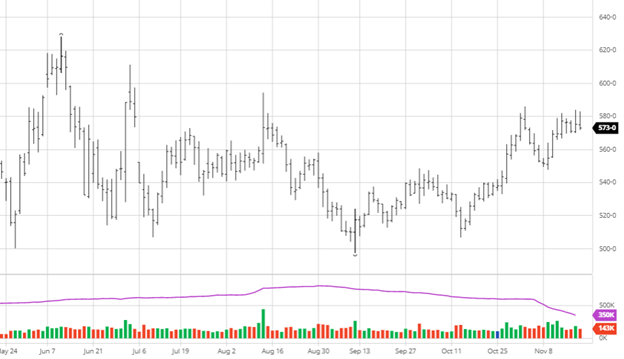

Cotton has had life in the $1.10+ range for a while now as demand overseas is high for U.S. cotton. Growers have seen mixed yields across the country but nothing too surprising to the market. Cotton demand does not seem to be slowing down anytime soon as the world still is coming out of the pandemic, and some countries still have major restrictions.

Podcast

For the past year, commodity prices have perpetually soared and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

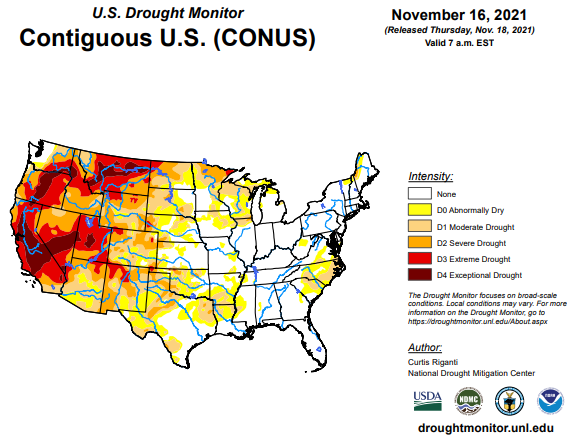

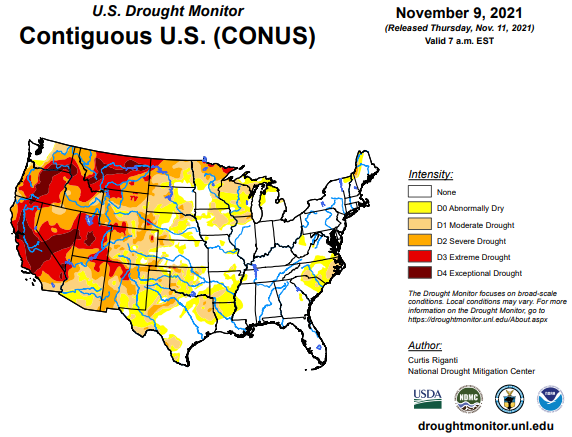

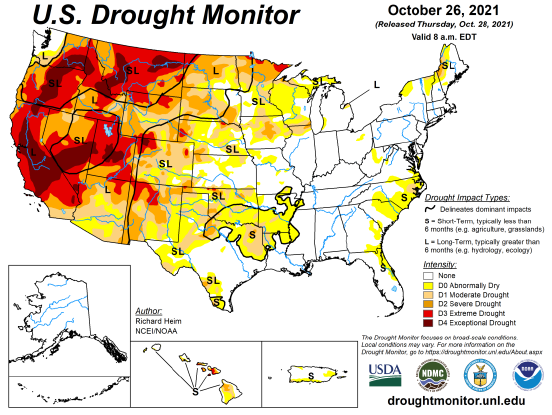

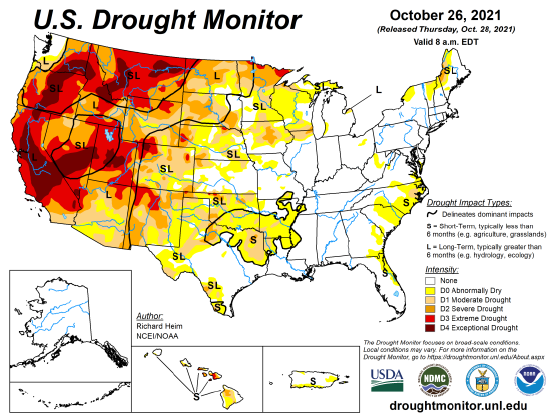

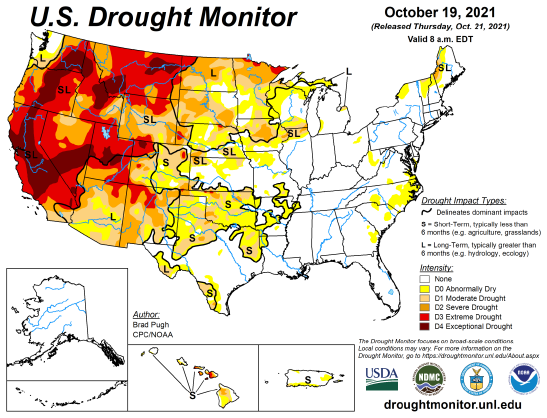

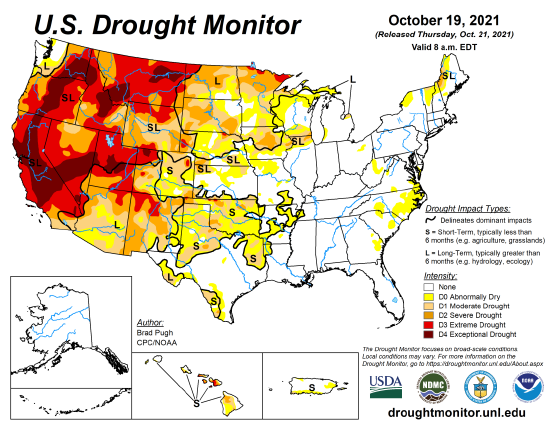

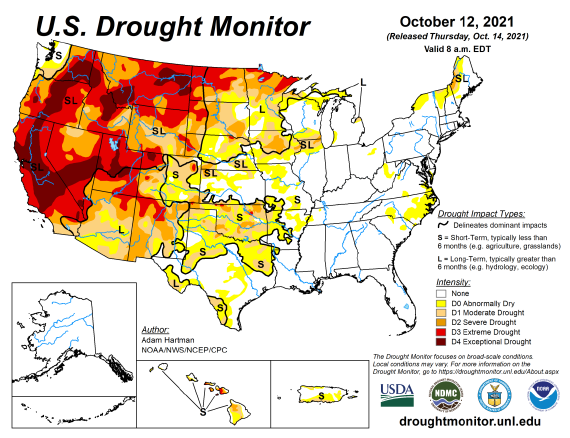

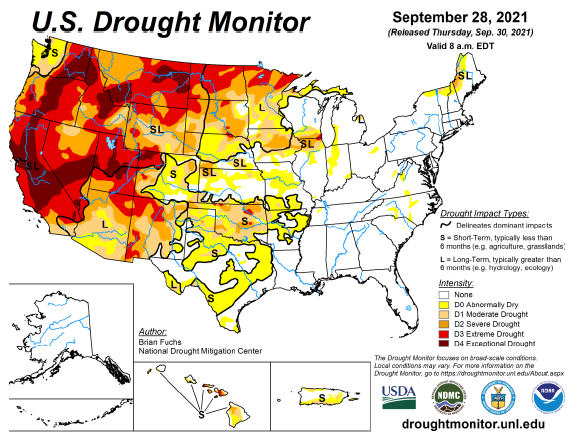

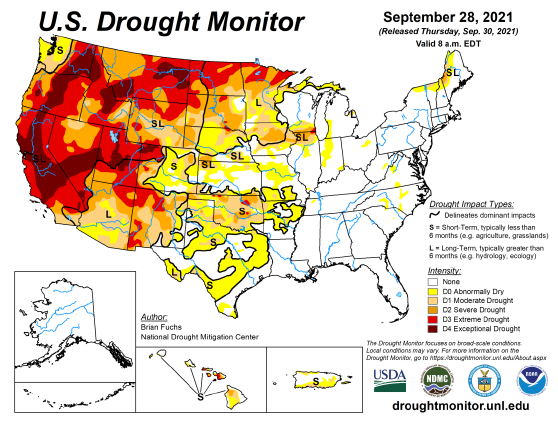

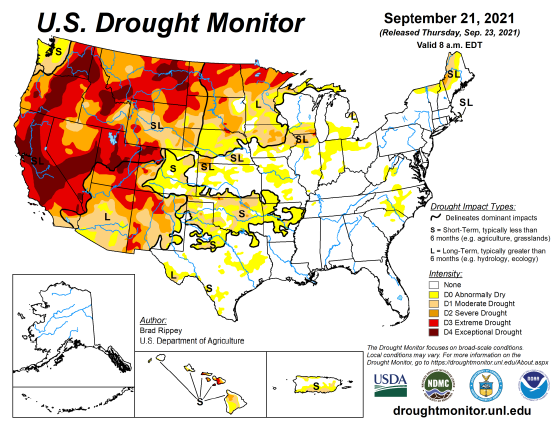

U.S. Drought Monitor

The maps below show the U.S. drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

Corn was struggling this week heading into the Nov 9th USDA report, where it saw a good bounce after its release before falling back to only finish up slightly higher on the day. The corn numbers that came out of the report were fairly neutral, with a 177 bu/acre yield and 15.062-billion-bushel U.S. production. The yield was slightly raised from 176.5 the month before but was right in line with estimates, so there was no significant reaction on that number. Overall, there were not many surprises for corn as most bullish reactions came from soybeans pulling them higher with them. With ethanol margins very profitable and crude oil staying higher, the demand side will continue to keep basis levels high. As harvest was 84% complete at the start of the week, there is still time for any weather issues to create issues to finish up harvest, but this is always expected, so being this far along is helpful.

Soybeans had an excellent bounce post USDA report but finished well off the highs of the day. The yield came in at 51.2 bu/acre, down 0.3 from last month, along with lower world-ending stocks. As far as U.S. ending stocks. the USDA pegged it at a manageable 340 million bushels, slightly up from last month —these numbers are not outright bullish. South America’s weather is non-threatening right now; however, with solid world crush margins, there is not much reason for a bearish outlook heading into the winter. With funds currently flat, we may hang around this area trading until new news enters the market.

There were no surprises in the wheat report,, but it did follow beans higher after a down week leading into the report. US wheat stocks came in at 583 million bushels (pre-report estimates were 581 million) and world-ending stocks of 275.80 million metric tons (pre-report estimates 276.5 MMT). Despite the recent pullback, there is still a bullish sentiment in the market moving forward for the time being.

The Dow has continued to trend higher this week as it has put together an impressive month despite Tuesday’s pullback. Many markets have led it higher from tech to industrials, with the new infrastructure bill playing a role.

Side note: The crypto markets have also been on a tear the past couple of weeks. It will be interesting to watch heading into the end of the year after an impressive last year and a half.

Podcast

For the past year, commodity prices have perpetually soared and continue to trend higher. We’re diving into the fertilizer forecast with a unique guest, Billy Dale Strader, a branch manager for Helena Agri-Enterprises in Russellville, KY., who is truly at the epicenter of the rising fertilizer prices.

Billy Dale planted his agriculture roots on his family-owned farm and has managed regional seed and chemical sales at Helena for the past decade. In this week’s pod, we tackle the big question for farmers and ultimately end-users — is the impact of higher-priced inputs, like seeds, chemicals, and fertilizer, on the supply and demand for the major U.S. crops? Listen or watch to find out!

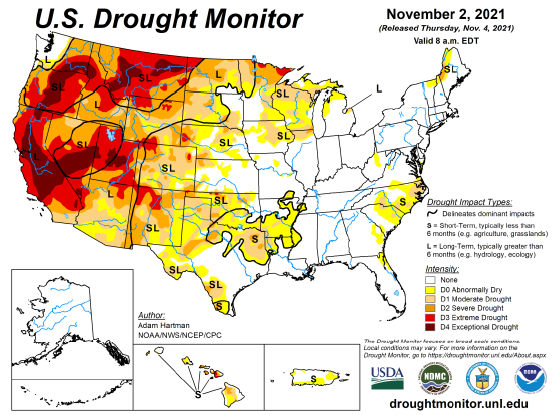

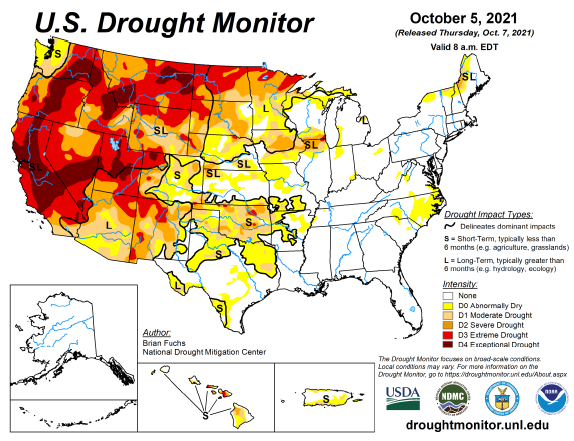

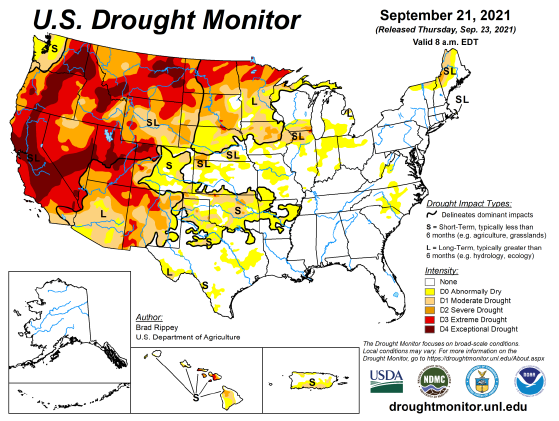

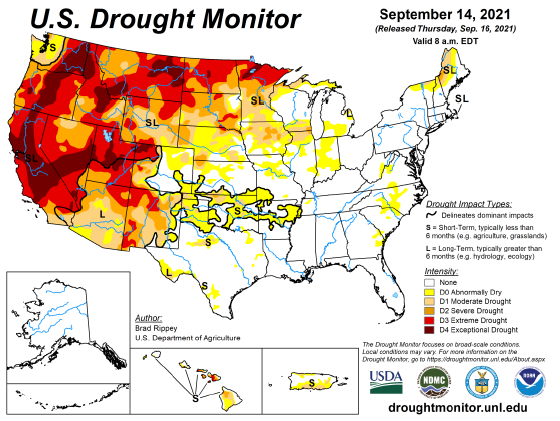

U.S. Drought Monitor

The maps below show the U.S. drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

Corn has continued its rally as the bulls seem to have their mojo back following a time where they could have been uneasy. Despite the disappointing export report, corn was able to keep the momentum going Thursday. This week’s weather week will slow down harvest and could cause issues for what is remaining in the field. Higher basis has been seen across most of the country as a lack of available corn continues to put pressure on elevators while ethanol plants are running on great margins and can afford the basis. Going forward it will be interesting to watch how farmers manage the corn they store. Do they hold it until we see much higher prices? Will basis become so favorable it is hard to hold on to it while farmers are making payments for products for next year? These questions do not have any answers right now, and only time will tell, but one thing is for sure, input prices are going up and farmers know how valuable their crop is.

Soybeans have had a good bounce from their low a couple of weeks ago, even if it is not as an inspiring rally as corn. Like corn, the weather will delay harvest and reduce yields in many areas that were off to a great first half. South American weather is generally good for the next week with Argentina receiving their best rains of the season so far. The weather over the coming weeks/next couple of months will be important to getting them off to a good start. Like corn, it will be interesting to see the number of beans stored vs. sold after harvest. As beans continue to struggle to find a pattern, we hope to see one develop in the coming weeks, hopefully, a good one.

The Dow had another good week with one big down day followed by a bounce-back on Thursday. As Q3 earnings continue to roll in, it has been a mixed bag with large companies like Amazon and Apple falling post reporting.

Oats

The Oats market has been on a tear the last two months as Canada’s and the upper plains crop had a multitude of issues due to drought conditions. This has created a supply problem on top of already higher grain prices across the board this year.

Podcast

The Hedged Edge is back, and we’re jumping into the thick of the commodity markets with RCM’s own King of Cotton – Ron Lawson. Cotton prices have exploded since the COVID crash, rising more than 236% from the March 2020 lows. While prices have backed off from the October 8th high, cotton is one of the purest supply + demand-driven markets around the world and has caught fire along with the global inflation bug currently running rampant across many commodity markets.

U.S. Drought Monitor

The maps below show the U.S. drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

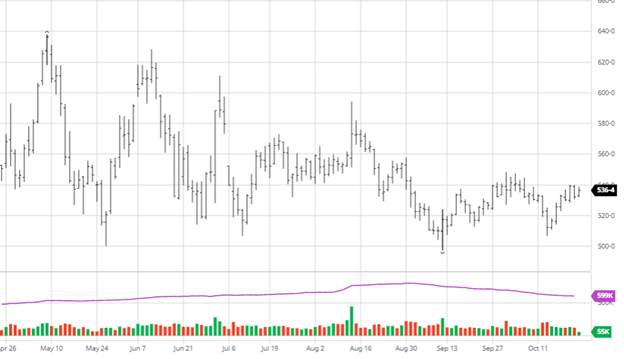

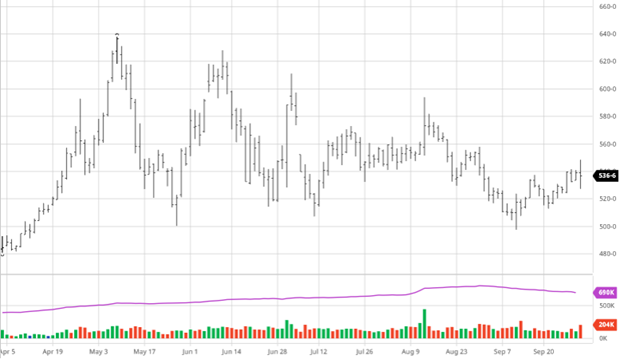

Corn has seen a good rally since the lows that came after the report. Due to the world energy values falling, corn is still well above where it was last week, despite the pullback on Thursday. Rain in the eastern corn belt that was expected to slow harvest coming up has turned a little drier but still present. The rains this week will further deteriorate the already poor-quality plants. The yields were coming in better than expected in some areas the first half of harvest, but we should expect them to be lower in the second half.. NOAA on Thursday released its outlook for a warmer winter in the U.S., which hit energy prices and could see them trend lower, which would not help corn, among other things. It is vital this time of year to start paying attention to South American weather, and right now, Argentina is off to a dry start. Ethanol production continues to grow as margins remain above $1 per bushel, pushing plants to produce at top capacity. This week’s output was the 3rd largest ever and will be an important supporting factor for corn going forward.

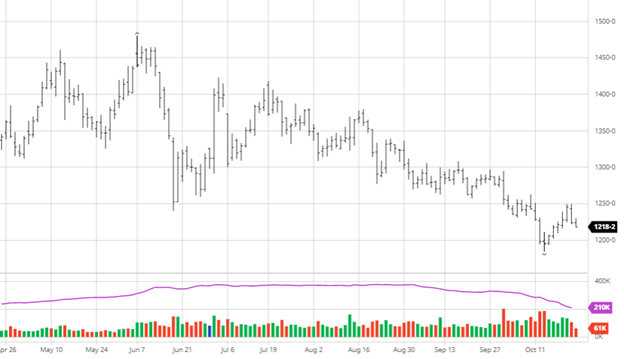

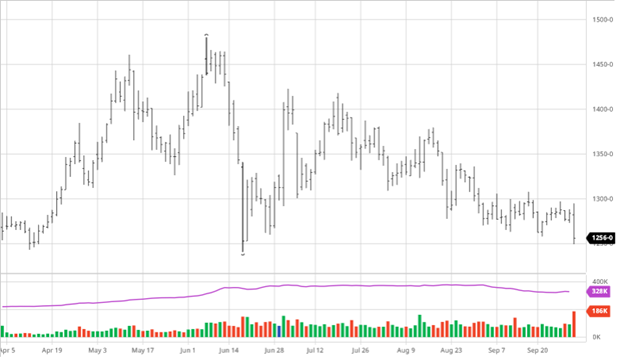

Soybeans have had a good rally since the report, like corn even with the pullback at the end of this week. World bean oil and veg oil markets saw a rally this week that helped pull soybeans up along with many of the same factors as corn. Weekly exports this week were 2x that of last week and the highest in 13 months, with China being the main buyer. According to the most recent USDA report, if we can get consistent demand from China moving forward, that should help soybeans despite the crop being bigger than initially thought. The chart is tough to look at, but the market did close above the 20 day moving average at one point this week. It will not get back to that level to end the week, but the double high of $12.49 ½ this week makes it look like that $12.50 range may be hard to break through unless we get more bullish news. All eyes will move to the 2022 contracts next week as we begin to look at options for stored beans.

The Dow had another good week as we have seen a good October for the equities market. After a tough September, this is good to see money back in the markets as questions around tapering, inflation and other Fed issues remain. Supply chain woes continue to plague many industries and will probably only worsen with the coming holiday season.

Podcast

In this week’s podcast Simon Quilty, from Melbourne, Australia, and Jeff Malec join Jeff Eizenberg to discuss global meat markets. We get an overview of the global meat market: beef, poultry, and pork, the main players and their main concerns, including labor and shipping shortages being a critical problem. Simon talks about how he goes about hedging the various contracts providing risk management for the current disruption for in-demand meat products.

The maps below show the U.S. drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

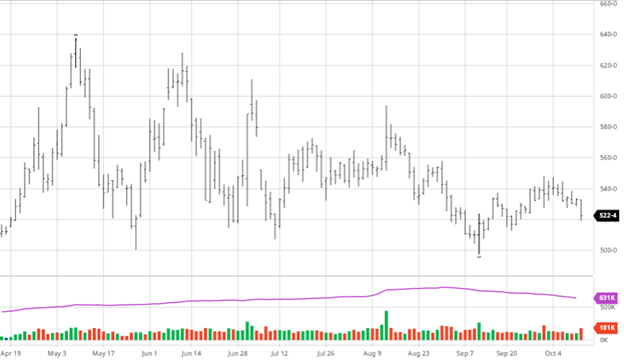

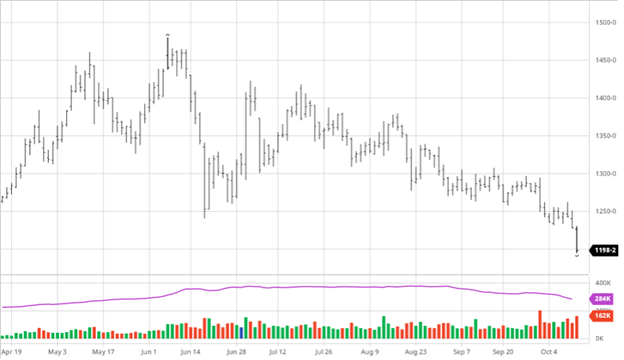

Corn had been in neutral heading into the October 12th USDA yield report, seeing bearish numbers. The report raised yield to 176.5 bushels per acre, slightly higher than the report last month. U.S. ending stocks and world stocks were both raised while also raising exports, lowering feed and residual use. The somewhat disappointing yields in the eastern corn belt were offset by better-than-expected western corn belt/plains yields. Demand looked to be lowered due to the continued export issues out of New Orleans since the hurricane, and a record crop in China won’t require them to import as much. The season-average corn price received by producers was left unchanged at $5.45. A higher yield and supply is bearish news, but the numbers do not appear to have been bearish enough to where we will retest harvest lows anytime soon. The cash market will continue to give us an idea of how much corn is actually out there, along with private estimates as harvest rolls on.

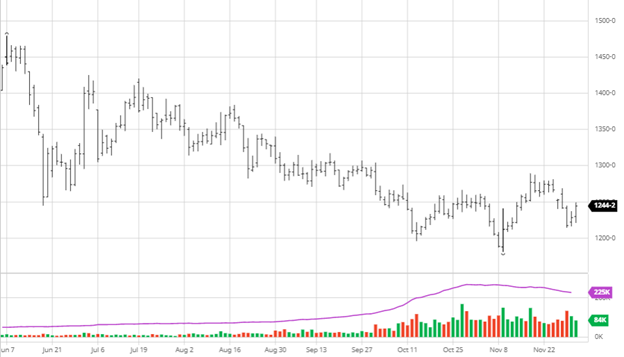

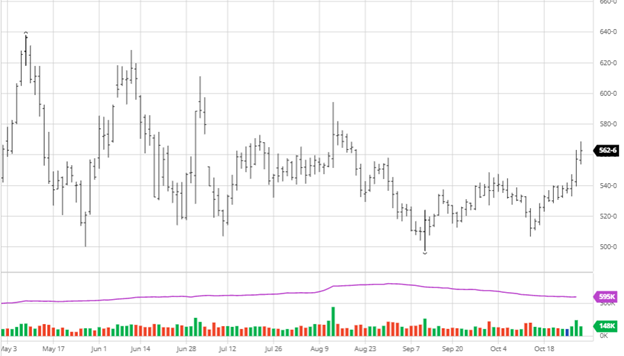

Via Barchart Soybeans have been struggling the last couple of months, and the previous two reports have not done them any favors. As you can see in the chart below, it has been tough sledding since early June for beans. The USDA raised yields to 51.5 bushels per acre, up from the September report. The feeling that the U.S. bean crop was getting bigger with the good late-season weather came to fruition in the report. World stocks were also revised higher, creating another bearish concern. Without demand from China or a problem in South America, there aren’t many bullish factors for beans. If either China demand or SA weather turn in favor of the U.S., we could see some support, but until then, there is not much helping the market.

The report covers many areas of the agriculture landscape. If you would like to view the full report or look at something else not covered, here is the link.

Dow Jones

The Dow bounced back this week following the rough end of September. Congress agreed to pass a short-term agreement to keep the government funded until December. There was a small amount of worry in the markets as the deadline loomed, but the same concern will return in 2 months when they need to pass a long-term plan and a debt limit adjustment. Any bounce back after a significant drop is good to see to level everyone’s heads.

Podcast

Check out our recent podcast where we’ve brought on one of our real-life firefighters from RCM Ag – Jody Lawrence, along with Tim Andriesen from the CME Group to provide us with some inside baseball knowledge of the current state of agriculture markets. They discuss the real-world application of short-dated options to fight the recent blaze of volatility surrounding agriculture markets potentially.

The maps below show the U.S. drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

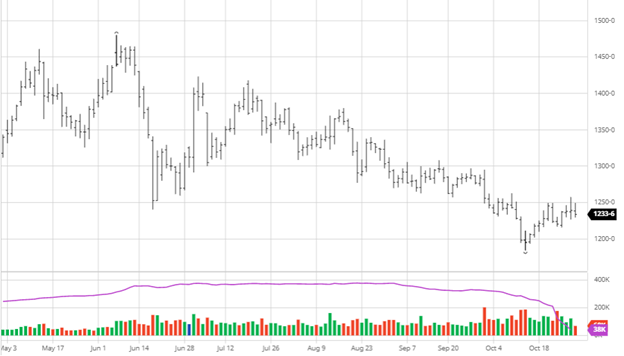

Corn took it on the chin upon the release of Thursday’s USDA report before bouncing back to finish only slightly lower on the day, but still up on the week. The report may have left more questions than answers hanging around as they raised ending stocks, but as we mentioned last week, the current basis and cash markets hint there may be less corn out there than the USDA believes. Corn stocks came in at 1.236 billion bushels, which was higher than the average estimate going in. Harvest was 18% done at the start of the week, and further progress will have been made with favorable harvest conditions. Exports this week were not great for corn, while beans were strong. The next major report for corn will be the October 12th yield update. With harvest getting off to a fast start, it will be interesting to see if the private estimates and USDA are closer to each other than usual this far in.

Soybeans fell post report as estimates were well lower than the USDA number of 256 million bushels. The average estimate was 174 million bushels which caused the immediate and lasting drop following the report. Obviously, nobody saw this number coming as it was well higher than the highest estimates. It is now time for the market to decide if they believe that number leading up to the October 12th yield report. Beans had great exports this week, but that was not enough to fend off the bears with the report. All the losses for beans on the week came from the report, as it had been pretty flat until Thursday. Soybeans harvested at 16% and will continue like corn this week. Like corn, the October 12th yield update will be critical as harvest has progressed further and we have a better idea of the crop.

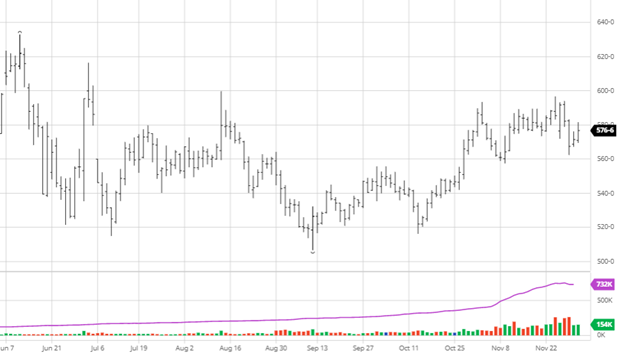

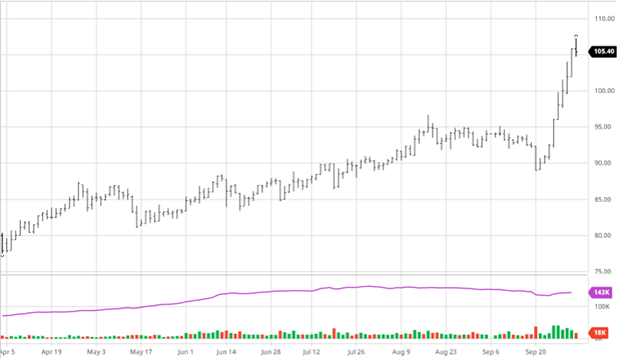

Cotton has been on a great run the last two weeks as you can see in the chart below. Cotton busted through several technical indicators in the 97 cent range while also clearing the 99.47 high from January of 2012. China has started to inquire about purchasing cotton as many companies look to import cotton and no longer use cotton from Xinjiang. Ultimately this is a supply/demand driven rally from strong global demand and uncertainty about the crop until it is out of the ground. Forecasts for rains in West Texas this weekend are not helpful for the crop and could cause issues depending on how much it does rain. Even with further upside potential to the cotton price this is a good opportunity to set floors to take advantage of this run up. As always look at your production and make the informed decision that applies specifically to your operation and not a cookie cutter plan.

Note: Since the writing above, Cotton has now topped 105 with December 2021 Cotton touching 107.28 on what seems to be a made rush of continued buying…. hold on to your hats!

Wheat saw a post-report rally as all wheat stocks came in at 1.780 billion bushels, which was below the pre-report estimates. Keep an eye on Russia as the export tax on Russian wheat will cut acres from their regular planting and could play out in the US wheat market as well.

Dow Jones

The Dow struggled again this week as September proved to be the worst month for stocks since March 2020, when Covid hit. Rising treasuries and interest rate hikes in the future had some to do with it, but September historically is not a great month for performance. One bad month in the span of a year and a half should not ring the alarm, but it will remind everyone that stocks can go down.

Podcast

Check out our recent podcast where we’ve brought on one of our real-life firefighters from RCM Ag – Jody Lawrence, along with Tim Andriesen from the CME Group to provide us with some inside baseball knowledge of the current state of agriculture markets. They discuss the real-world application of short-dated options to potentially fight the recent blaze of volatility surrounding agriculture markets.

The maps below show the US drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

Corn was pretty even on the week, only losing 1 cent as overall market weakness to start the week pulled it lower, followed by a rebound the last few days. Harvest continues to roll on as there has been great weather the last week in most parts of the country. Inconsistent yield reports coming out of the eastern corn belt have raised an eyebrow, but with a long way to go before the end of harvest, it is not a market mover. As always, when harvest comes, we will begin to get an idea of how many bushels are going straight to market and how much will go into storage. The late rally in 2020 and into this year may have some farmers trigger shy along with a La Nina year in South America. The exports were steady but nothing major to move the markets one way or another. Look for the shipping/export problems to continue until all the issues caused by Hurricane Ida are fixed. The next USDA report on the 30th will be what the market and traders position themselves for over the next week.

Via BarchartSoybeans have had a similar bounce back after the start of the week but still fell slightly. Exports have been strong recently as China continues to be a buyer as US beans have become competitive in the world market. Harvest for beans has gotten going as well and will continue in the coming weeks. Dozens of crush plants in China have been forced to close while the government looks to reduce electricity use to meet energy-saving goals. There has been a lot of confusion around the biofuel mandates but, until we get a final answer from the Biden administration, the market does not seem to be interested in rumors.

The Dow has gotten its losses back following the Evergrande driven collapse to start the week. The quick bounce back after the worst day in several months is good to see for the bulls, while the bears do not think that is the only issue in the market and a correction is still due. Despite the bounce back, the Evergrande news will be followed for a while.The Fed did not make any major changes this week but may be looking to towards the end of the year.

Podcast

Check out our recent podcast where we’ve brought on one of our real-life firefighters from RCM Ag – Jody Lawrence, along with Tim Andriesen from the CME Group to provide us with some inside baseball knowledge of the current state of agriculture markets. They discuss the real-world application of short-dated options to potentially fight the recent blaze of volatility surrounding agriculture markets.

The maps below show the US drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

RCM Ag Services is a registered DBA of Reliance Capital Markets II LLC. Trading futures, options on futures, and retail off-exchange foreign currency transactions are complex and involve substantial risk of loss and are not suitable for all investors. Loss-limiting strategies such as stop loss orders may not be effective because market conditions or technological issues may make it impossible to execute such orders. Likewise, strategies using combinations of options and/or futures positions such as “spread” or “straddle” trades may be just as risky as simple long and short positions. There are no guarantees of profit. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge and financial resources. You may lose all or more than your initial investment. You should not rely on any of the information herein as a substitute for the exercise of your own skill and judgment in making such a decision on the appropriateness of such investments. Opinions, market data and recommendations are subject to change without notice. Reliance Capital Markets II LLC shall not be held responsible for any actions taken based on this website or attached links. Parties acting on this electronic communication are responsible for their own actions. Past performance is not necessarily indicative of future results.