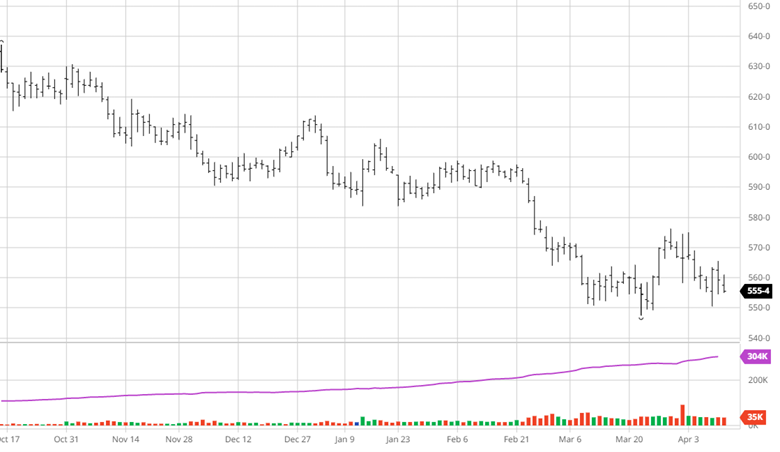

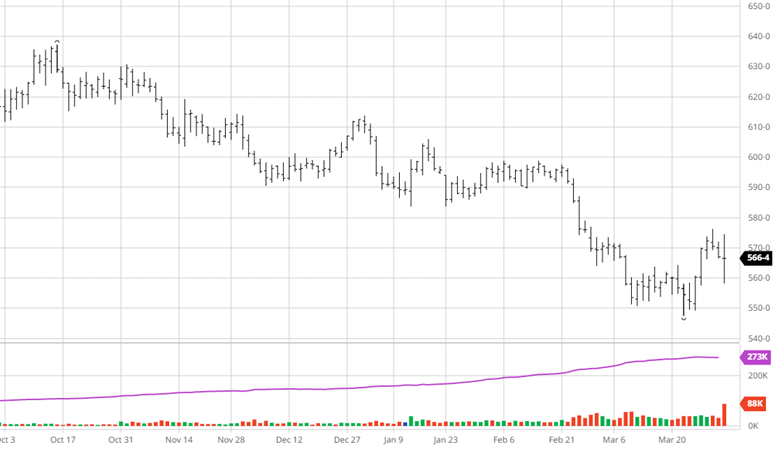

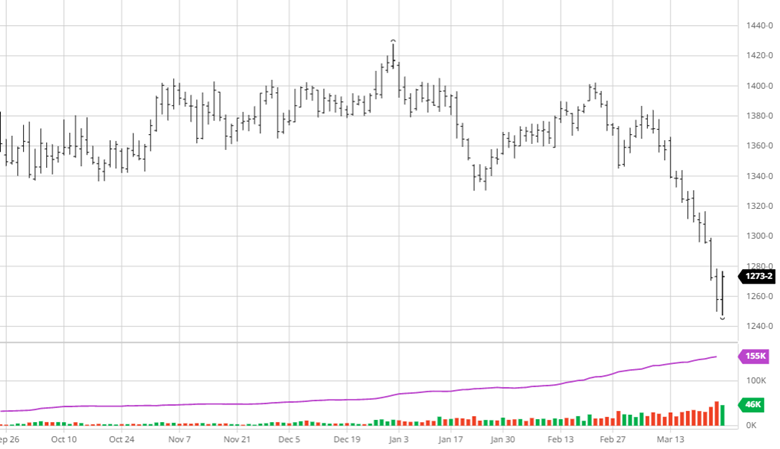

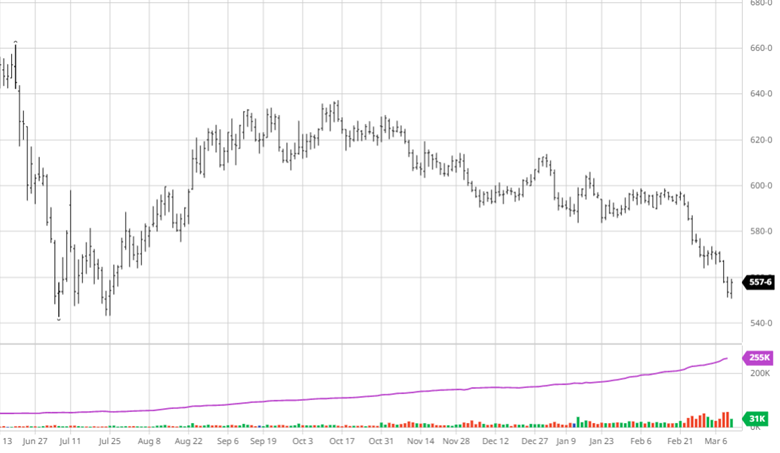

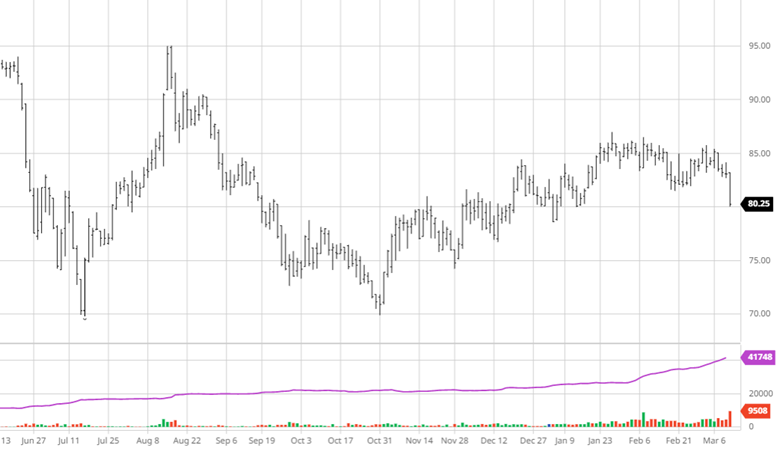

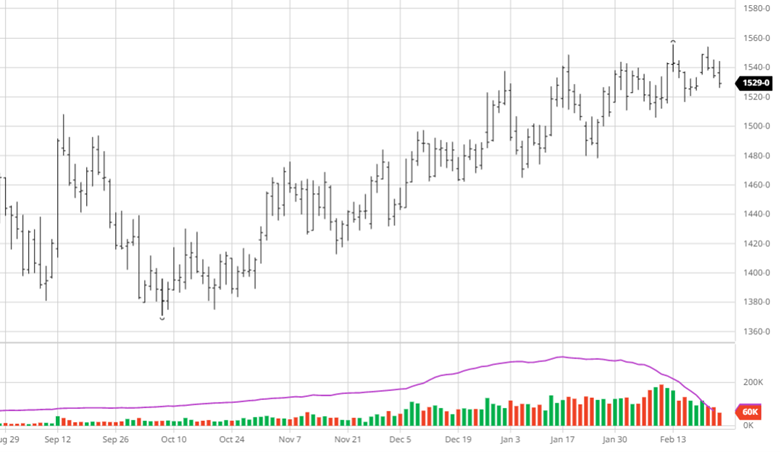

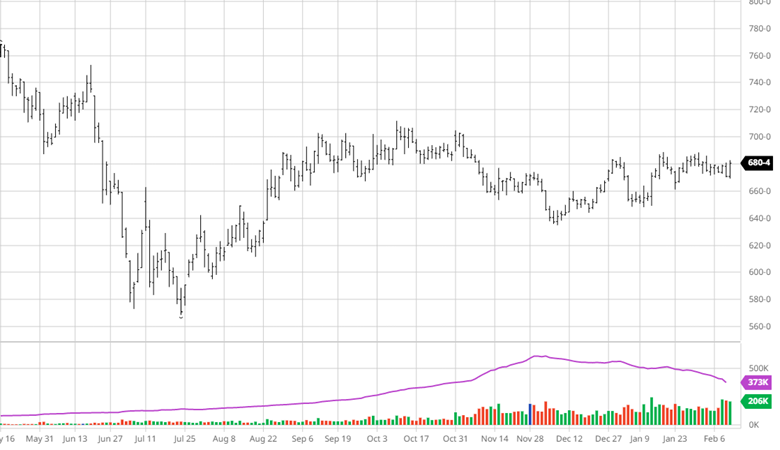

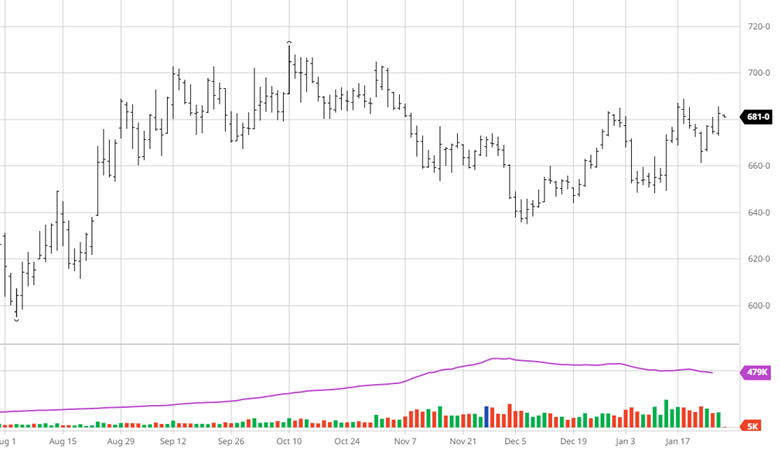

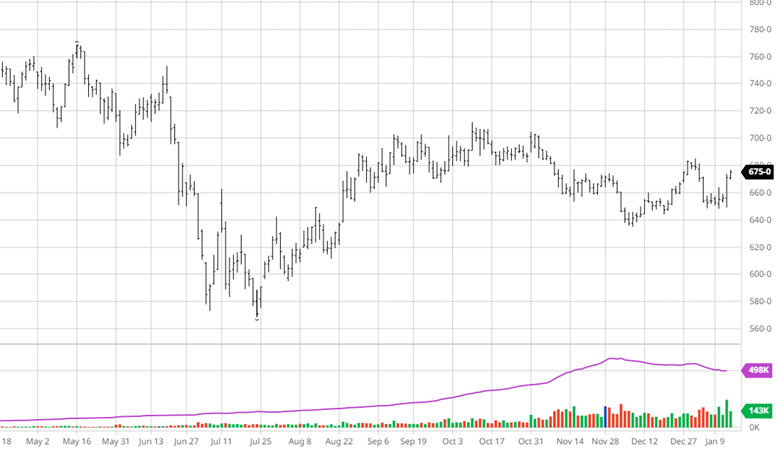

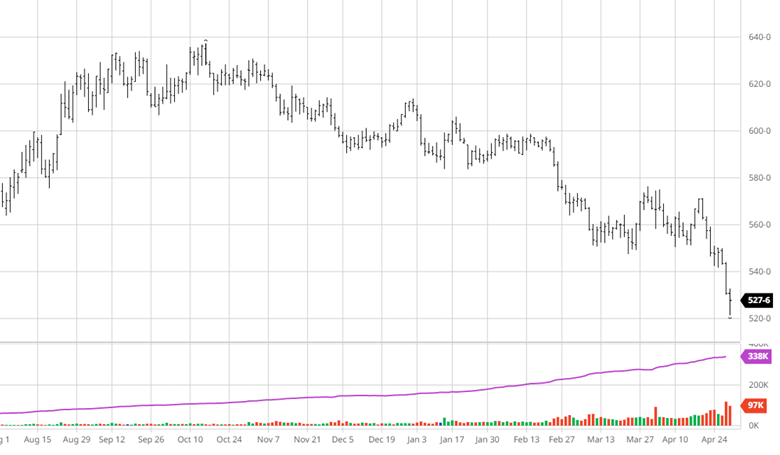

The losing streak continued for corn this week after another week with no bullish news keeps hitting prices. With Brazil’s prices as low as they are due to record production, China cancelled a 233,000-tonne corn purchase this week. This is not a new strategy by China as they cancel purchases from the US once they know Brazil can meet their demand for cheaper. This could lead the USDA to lower export expectations for the year and we would not be surprised to see more cancelations. While all the news has been bad of late and the chart looks ugly, the bounce off the lows to end the week was helpful. The weather remains cool and wet across much of the corn belt for the next week but should warm up and dry out after that to allow for quick planting come mid May. Corn planting progress was as expected this week at 14% complete.

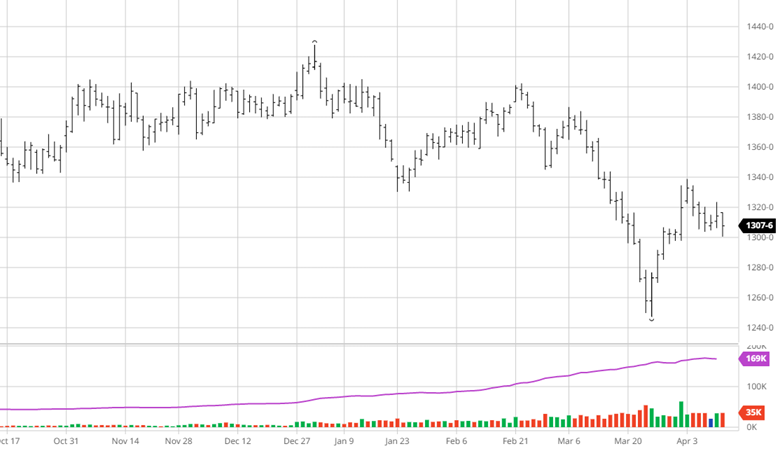

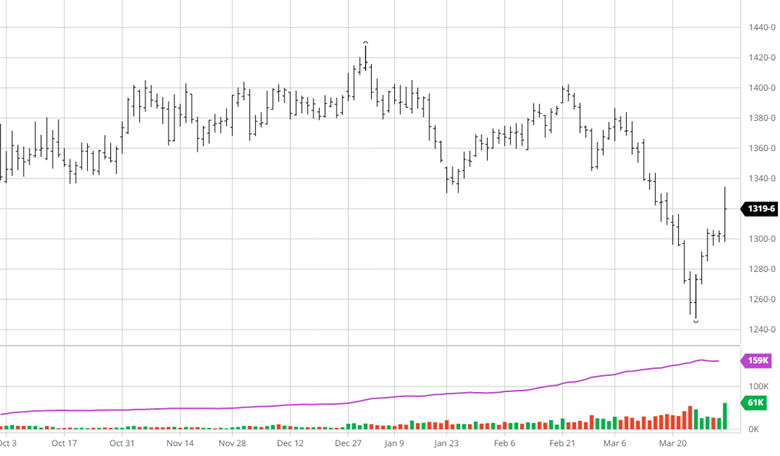

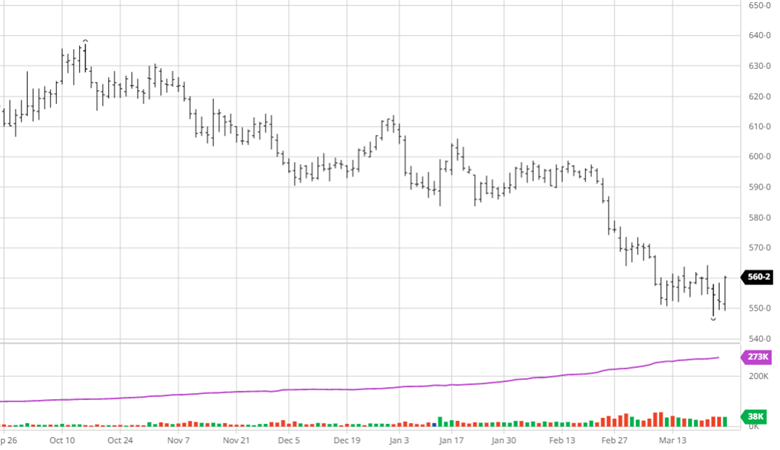

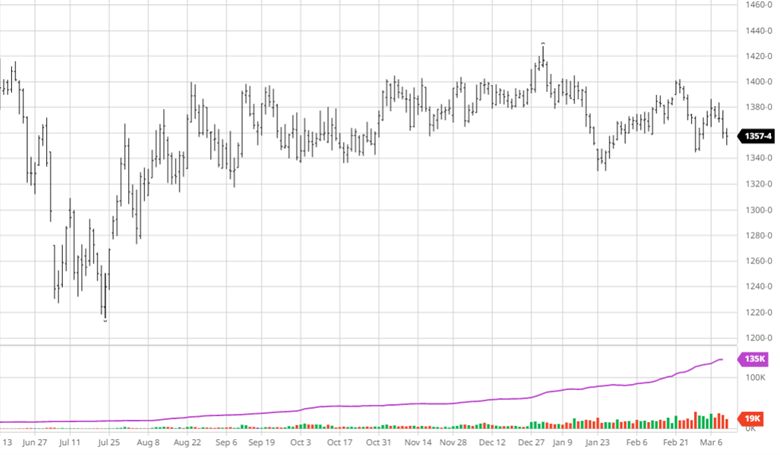

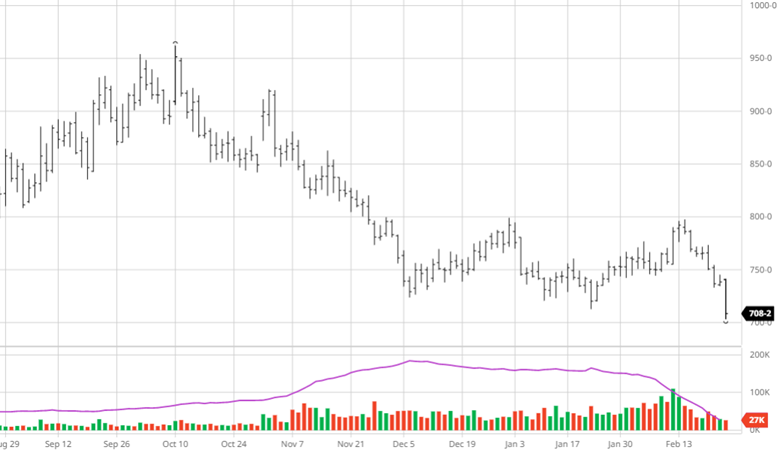

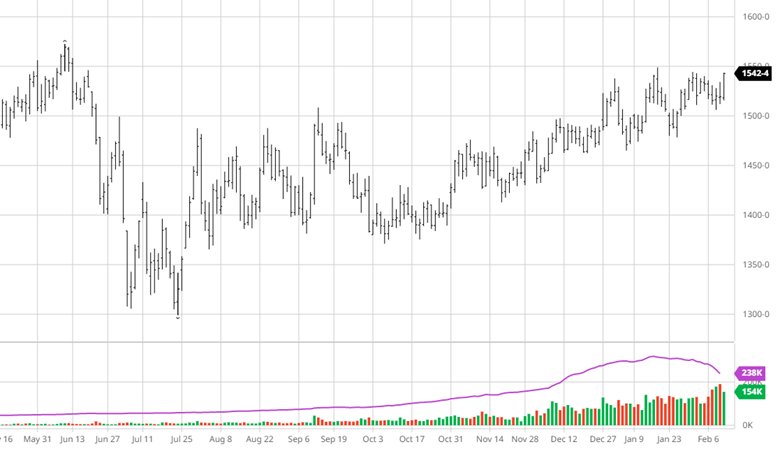

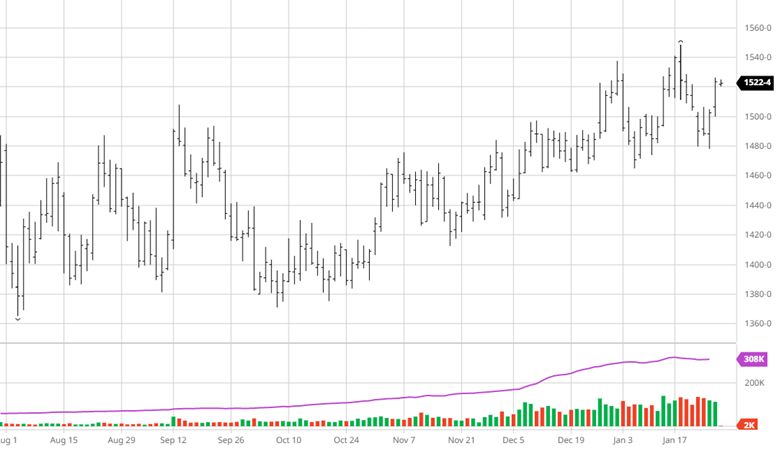

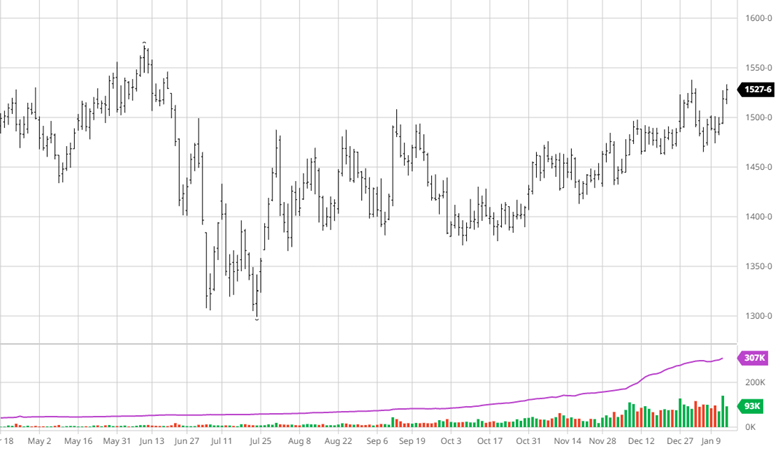

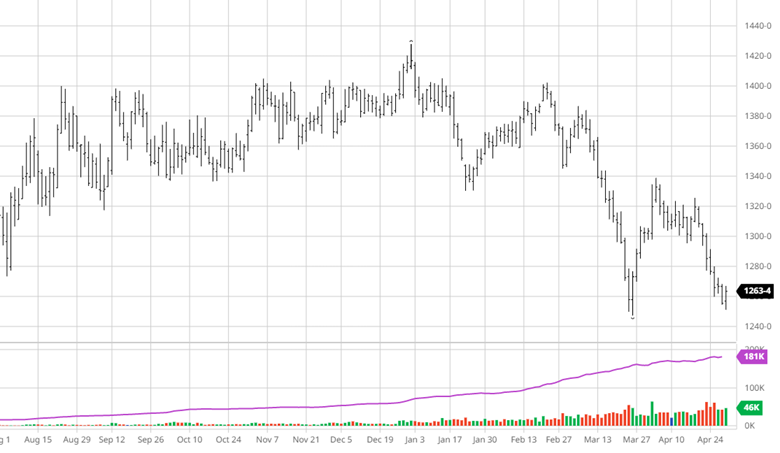

Soybeans had had seven consecutive days lower before their bounce on Friday to end the week. Brazilian markets had imploded but now appear to be stabilized, but still priced far below the US price. Like corn, there have been some cancelations and slow down in purchases, which will likely make the USDA lower export predictions for beans as well. Bean planting was seen 9% complete to start the week which is slightly ahead of expectations. Corn and Beans are both battling lower prices in Brazil and a good start to planting while they wait on news to change the trade direction.

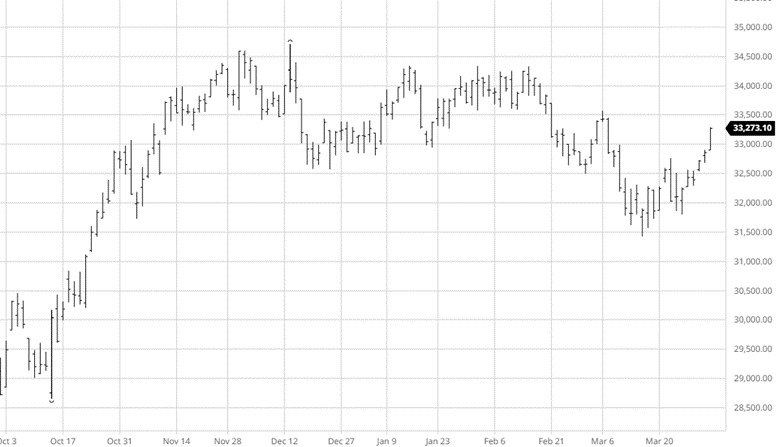

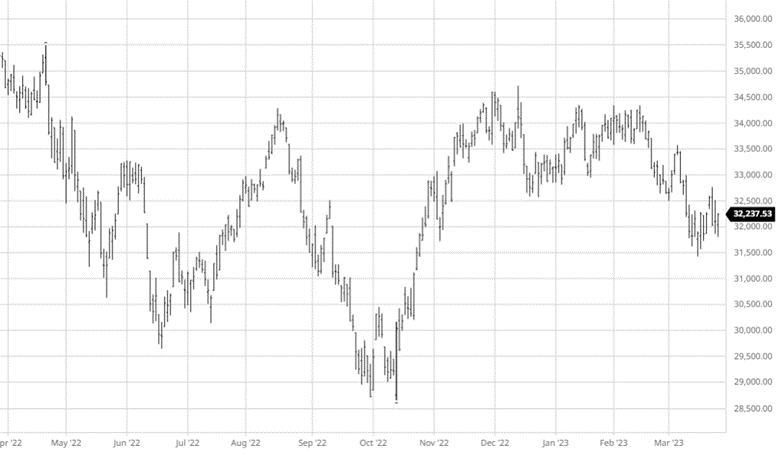

Equity Markets

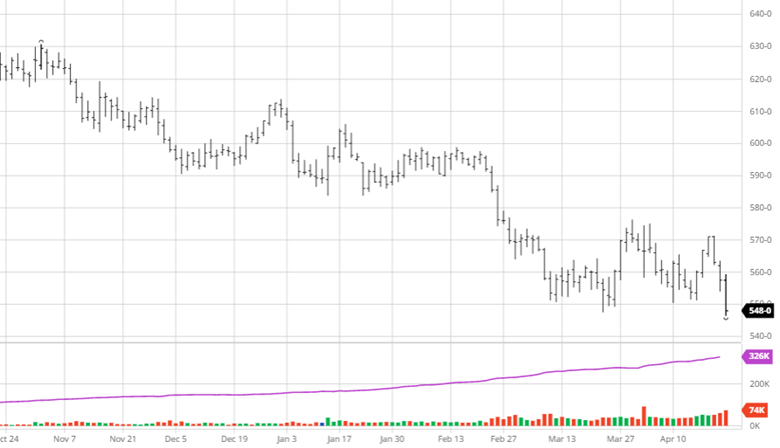

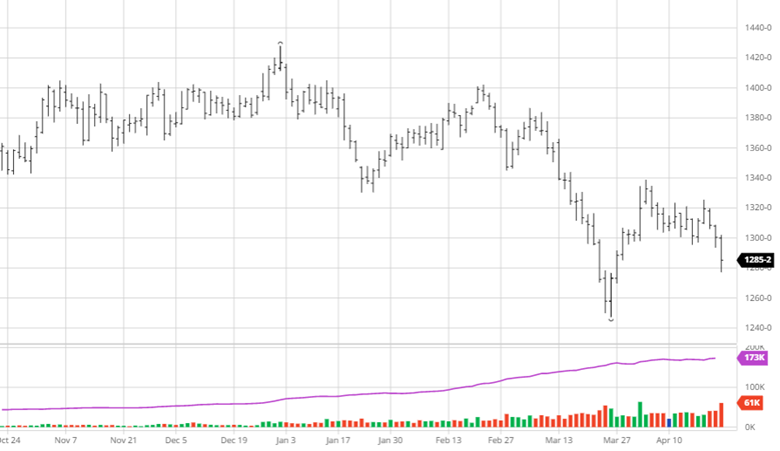

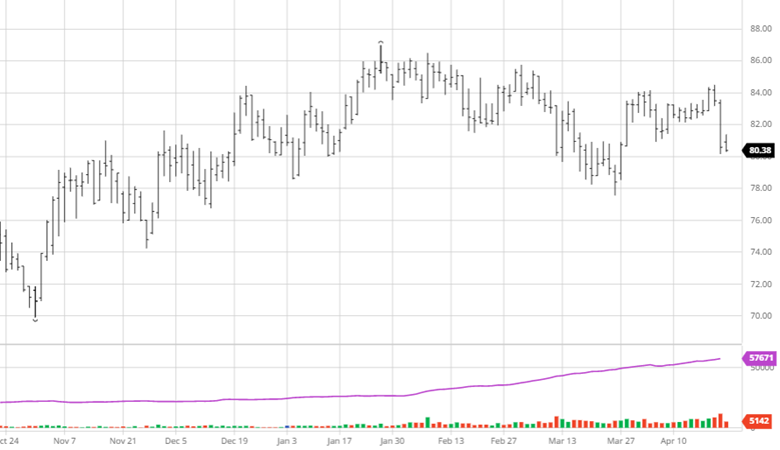

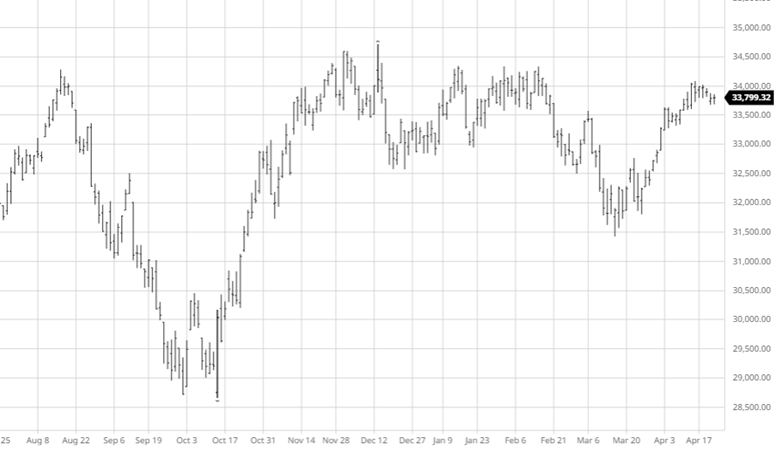

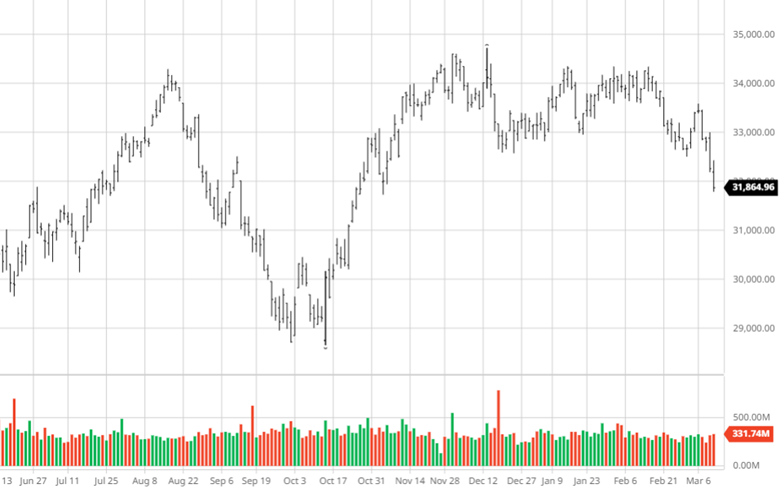

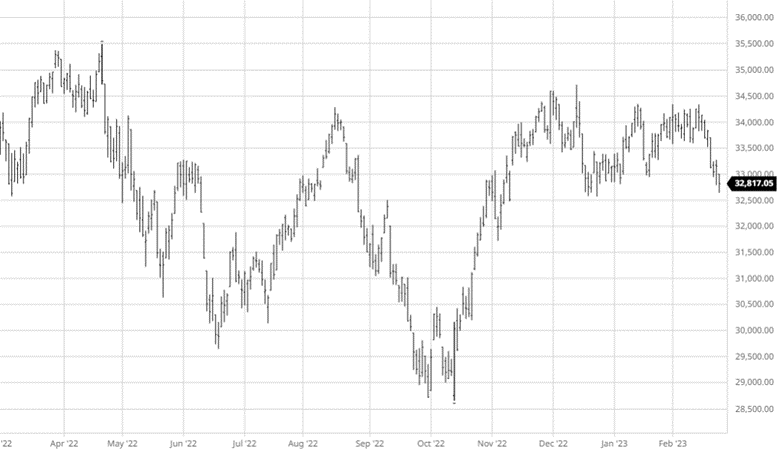

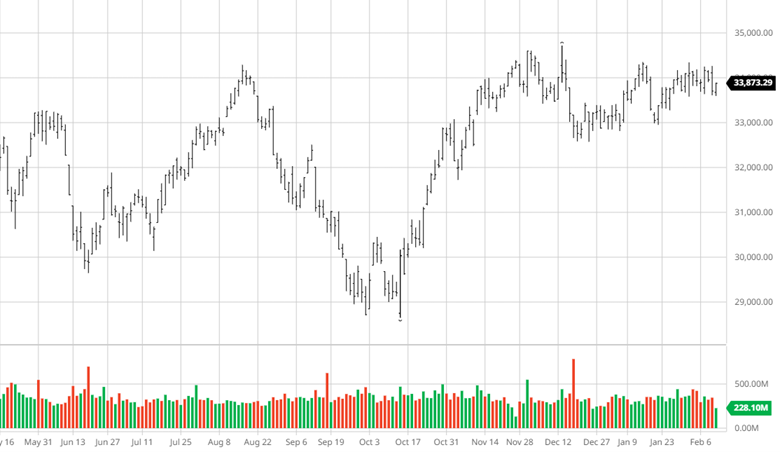

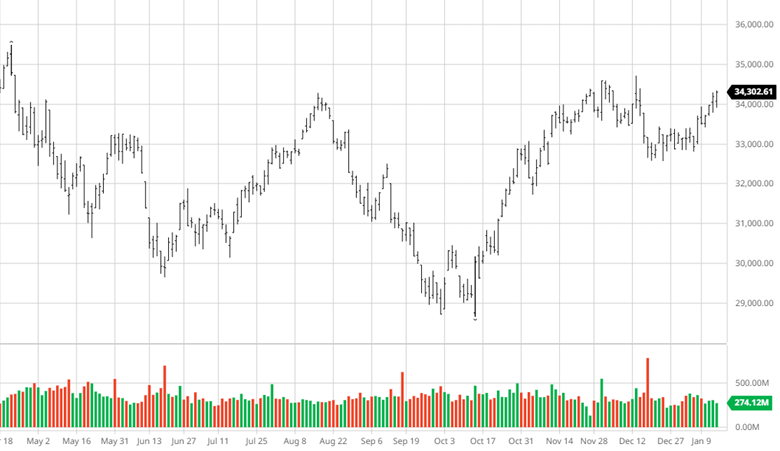

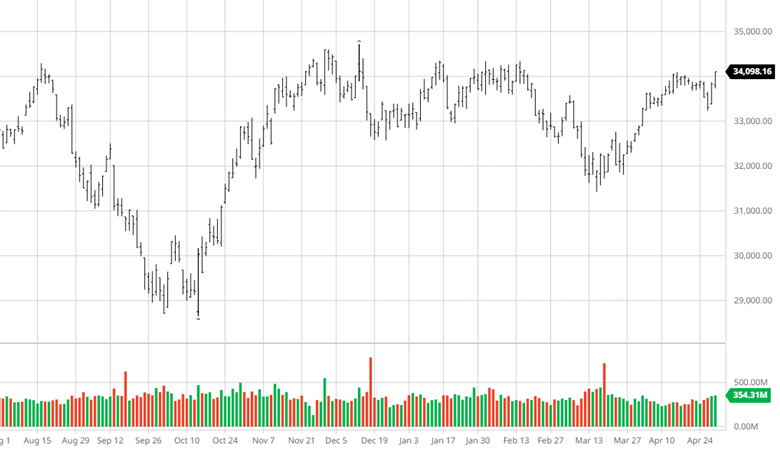

The equity markets got a bounce this week after several mega cap tech companies delivered strong earnings report. Next week’s reports don’t have as many big names but it does have Apple which may be the most important stock. GDP growth cooled for the 3rd straight quarter growing slightly over 1%, the drop of 1%+ quarter over quarter the last three will make Q2 growth important to see if that trend continues and we slip into negative growth, also known as recession territory.

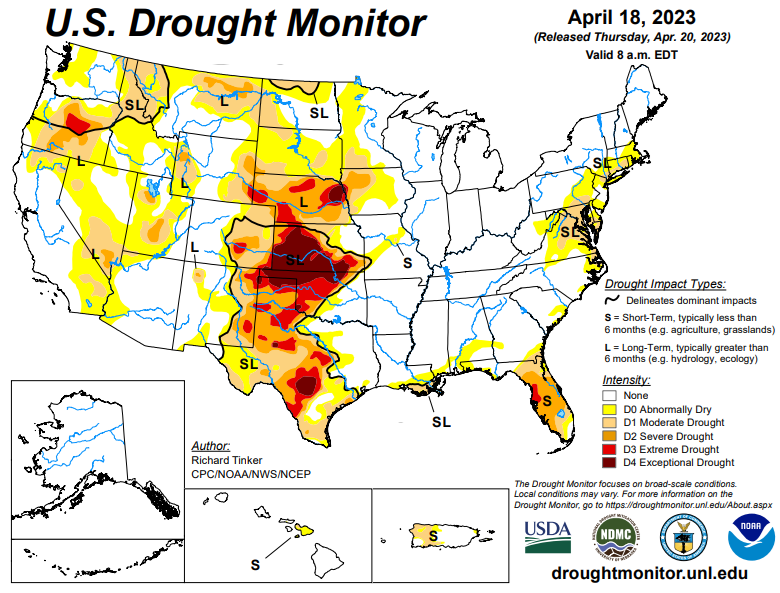

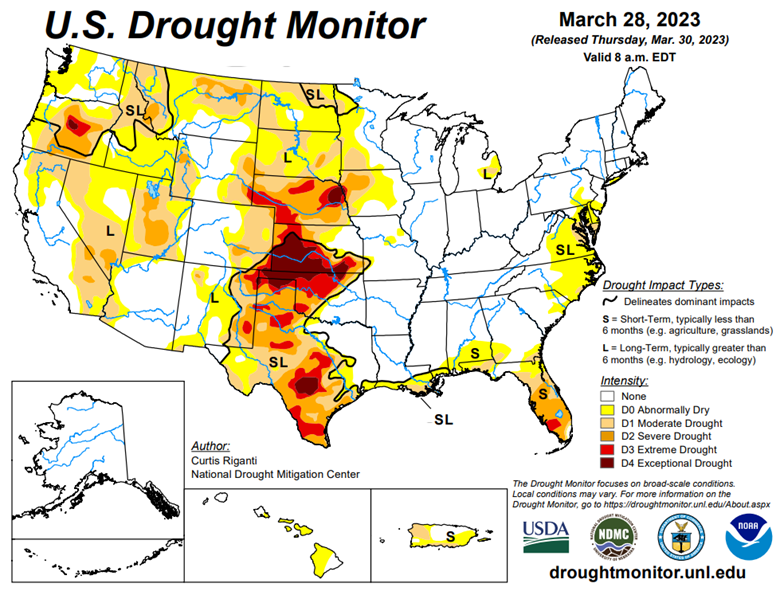

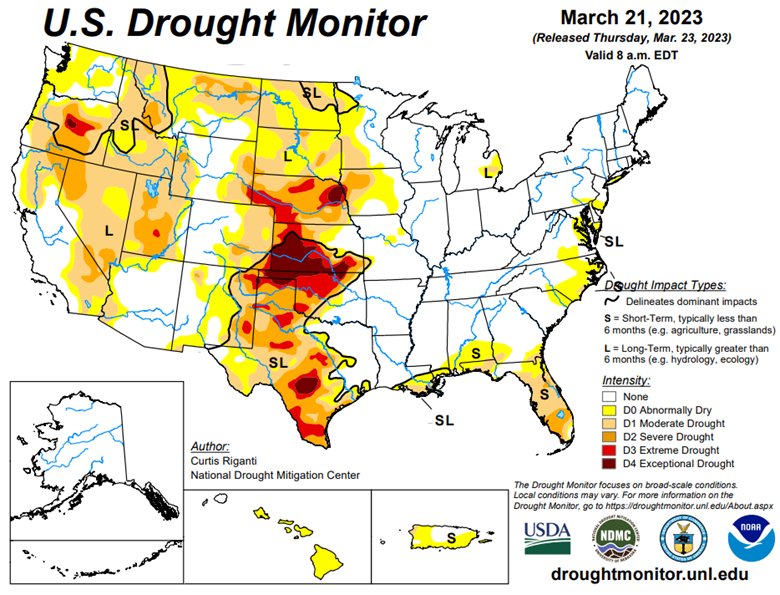

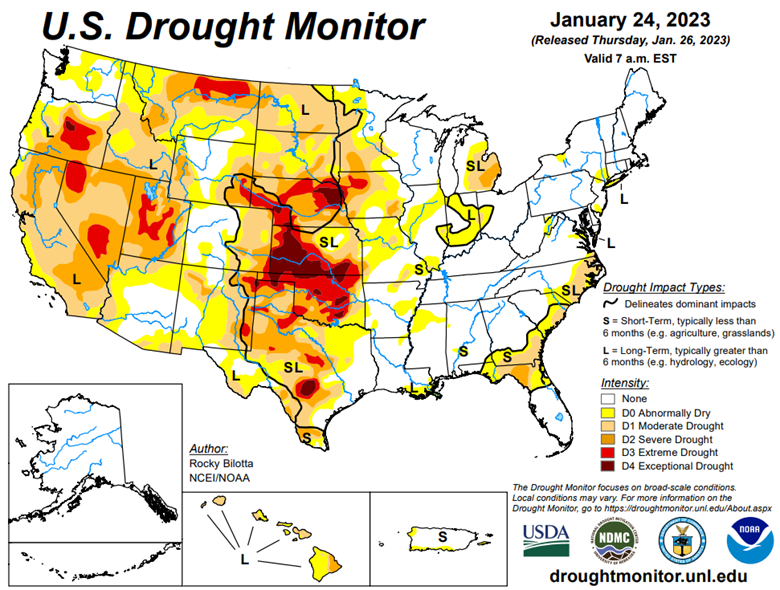

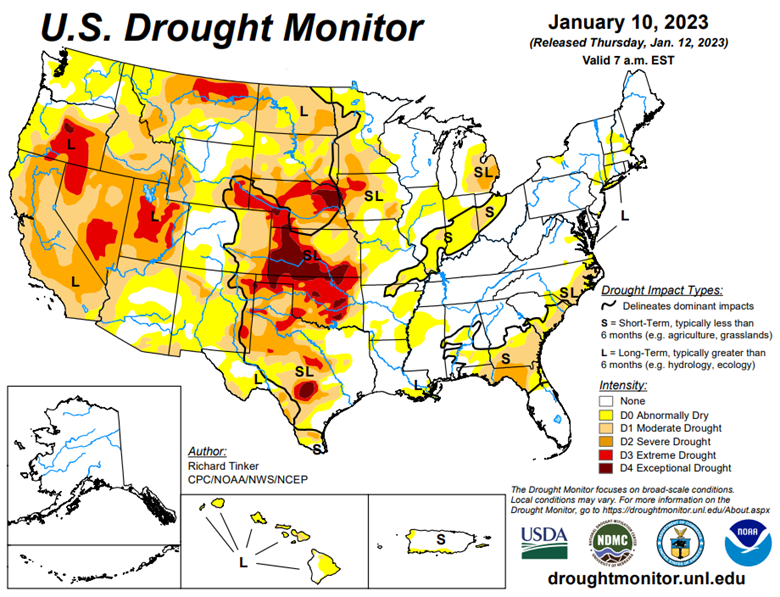

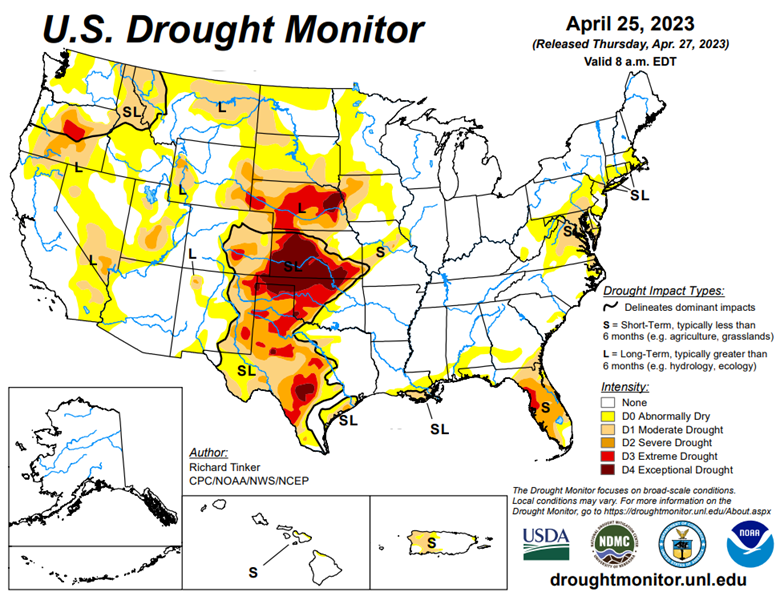

Drought Monitor

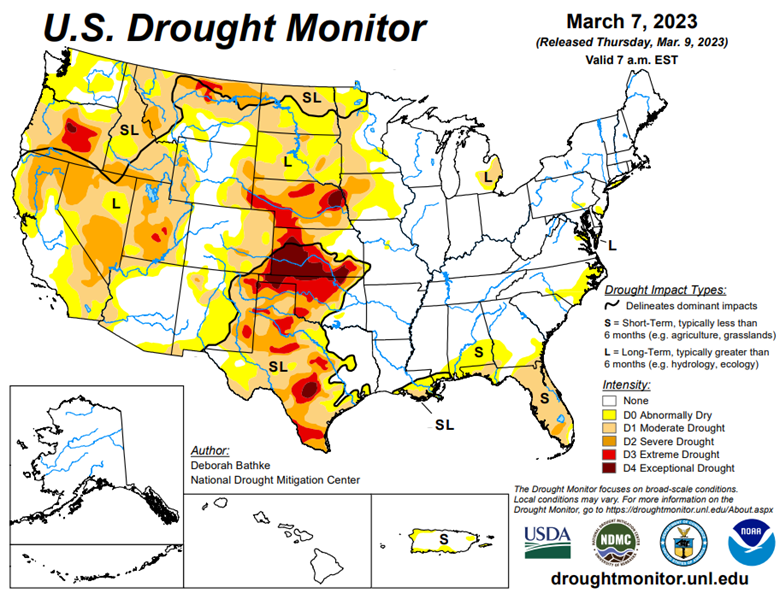

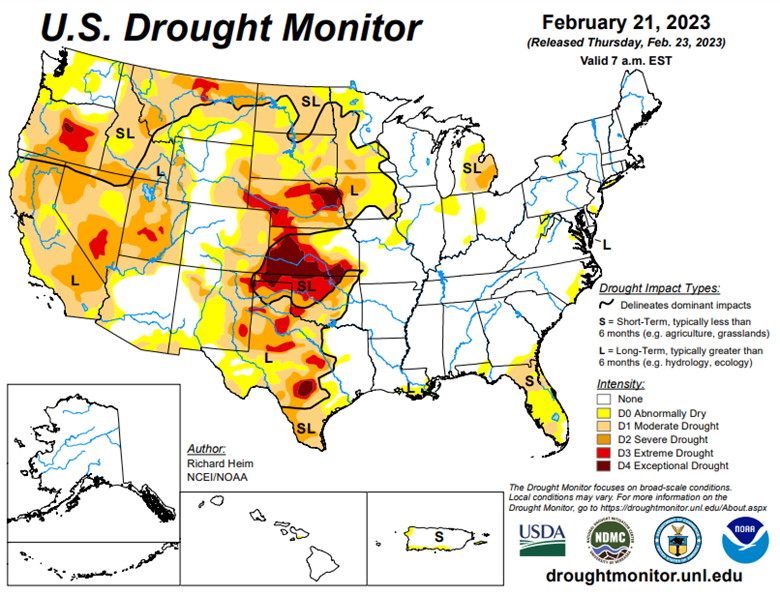

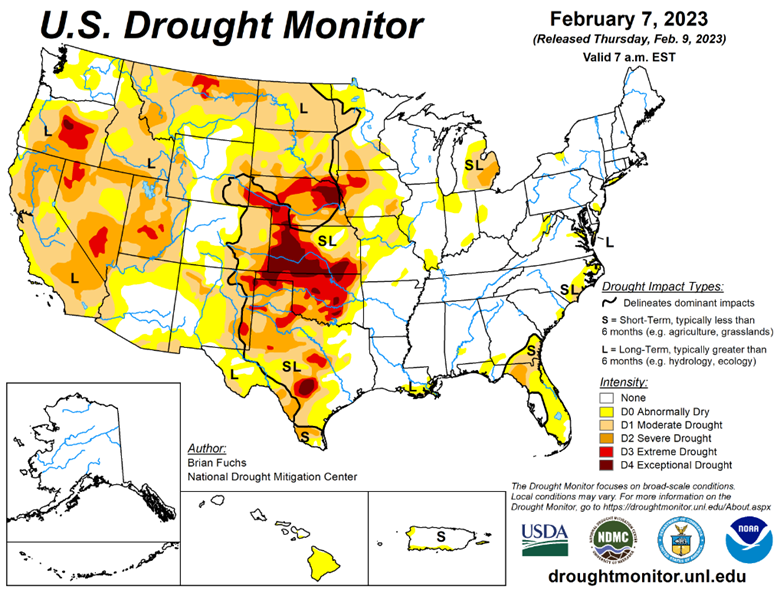

The eastern corn belt has gotten plenty of moisture, some too much, so far this winter with the western corn belt dry.

Podcast

With every new year, there are new opportunities, and there’s no better time to dive deeply into the stock market and tax-saving strategies for 2023 than now. In our latest episode of the Hedged Edge, we’re joined by Tim Webb, Chief Investment Officer and Managing Partner from our sister company, RCM Wealth Advisors. Tim is no stranger to advising institutions and agribusinesses where he has been implementing no-nonsense financial planning strategies and market investment disciplines to help Clients build and maintain wealth and reach financial goals since

Inside this jam-packed session, we’re taking a break from commodities, and talking about the world of equities, interest rates, tax savings, and business planning strategies. Plus, Jeff and Tim delve into a variety of topics like:

- The current state of the markets within the wealth management industry

- Is there a beacon of hope, or is it all doom and gloom for the markets?

- Other strategies to think about outside of the stock market and so much more!

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.