Recap:

Coming into the week we were expecting a sloppy trade. With a later Thanksgiving and the recent run up, a technical correction was not out of the question. The problem is that lumber futures have a tendency of unwinding gains in a hurry. That’s what we saw in January futures from Wednesday on. There was no change in market conditions to warrant a rollover so what caused the steep selloff?

The lumber market has changed. There will be times of tightness exclusively caused by supply reductions. JIT from here on out will keep you undersupplied in a trending higher market. That said, the standard operating procedure will remain the same in 2025 with the boss calling for no losses on excess inventories. That’s a receipt for price spikes. Most will agree that it will be harder to buy something in a rallying market. What holds many back is the fact that once the cycle is over there is no support. That is what we are experiencing now. The futures market can settle back towards its original value. With the cash and futures prices so close, I would not expect the futures to return to 560. The discovery period of the next level should be higher. The issue I see is that there are about 15 trading sessions left between now and the new year to gain some momentum. It might be the algo/fund buying or the cash trade picking up again. This is a tough environment for price discovery. Buy the mistake.

Technical:

The market was able to fall to the 595.15 retracement point. The major support point is the 50% mark at 586.25. The RSI is 44.50% and the stochastics are heading lower. Both indicate a market that had pressed higher than value and now is giving it back. If this was a court of law a new precedent of 623.50 is on the books. The 200-day moving average is 566.70.

The key takeaway is how to trade the basis. There needs to be a recalibration of the model. $40 or $50 basis is still great. The issue is when. The first spike could be followed by another so now you are managing the futures. It looks like the trade switch could be one that the trade makes money on the cash side now. All these are signs of a change in trend. We are still in a sideways market. The trend is only a minor factor in the overall trade. If you have too much wood, hedge it.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

Brian Leonard

bleonard@rcmam.com

312-761-2636

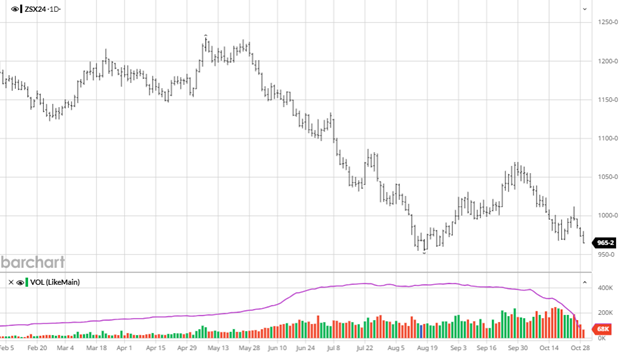

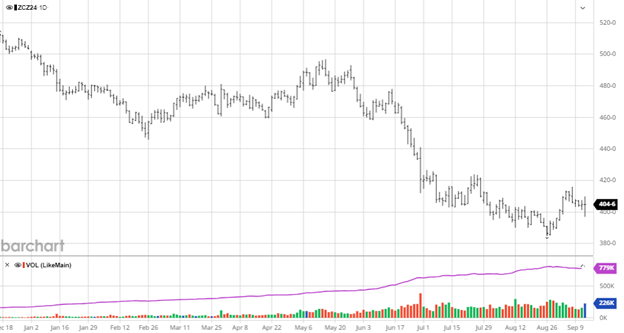

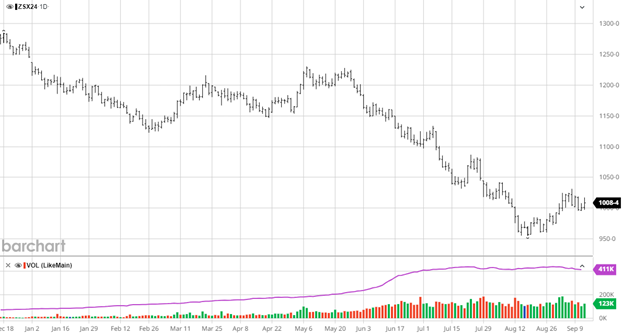

Soybeans weakness over the month has lowered it with corn. Beans do not have any bullish news on the horizon as they failed to rally through technical resistance. With the election next week, a tariff war with China would hurt beans in an already depressed market as we have seen in the past. Funds are very short and will need a catalyst to get them to change course, which currently is lacking. Bean harvest is 89% complete which means there won’t be much opportunity for unexpected bullish news moving forward.

Soybeans weakness over the month has lowered it with corn. Beans do not have any bullish news on the horizon as they failed to rally through technical resistance. With the election next week, a tariff war with China would hurt beans in an already depressed market as we have seen in the past. Funds are very short and will need a catalyst to get them to change course, which currently is lacking. Bean harvest is 89% complete which means there won’t be much opportunity for unexpected bullish news moving forward.