Recap:

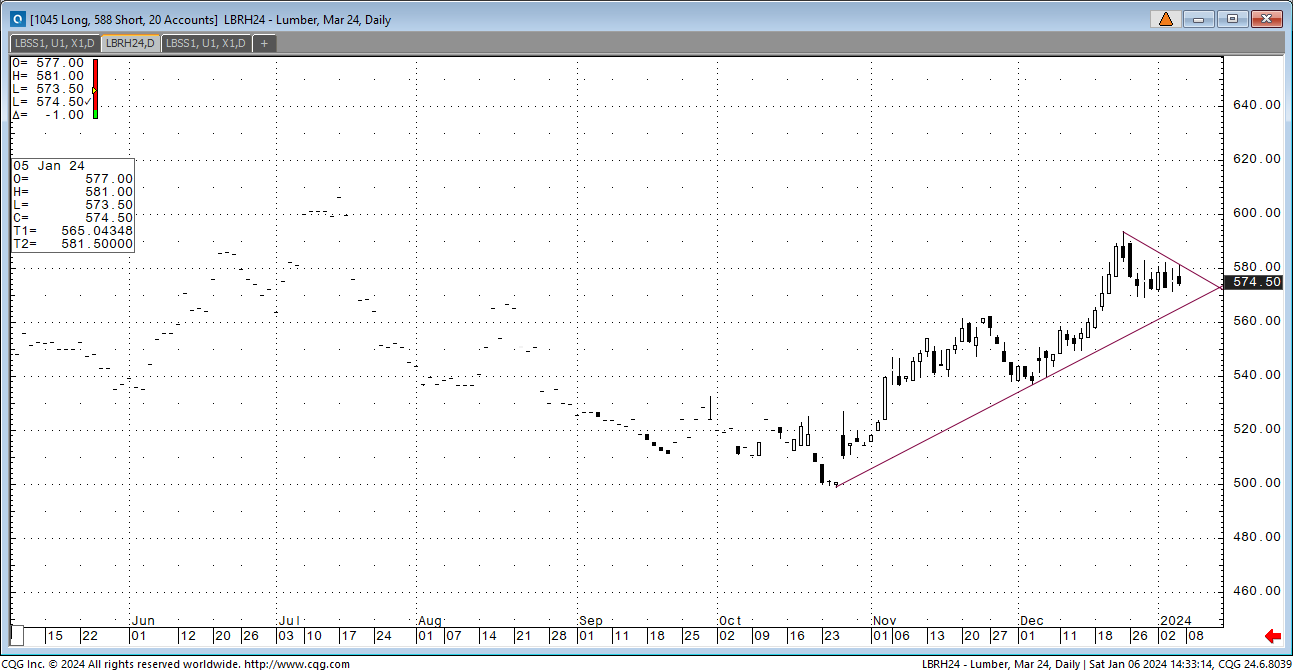

Last week, the futures market saw a healthy correction, dropping $22 in 4 sessions. March expired at 560, which was right in line with expectations. What was different was that most expected it to carry a premium, not a discount. My point is that this cash run has been far more significant than most expected. That leads to the question of how much was bought and whether it is enough. The cash side has hit the pause button to get a read of where they are. This is typical in any run but also leads to a quieter cash market and a futures correction. That sums up the week. Now what?

The industry focus is always on the micro. Today, wood continues to go out the door at a good pace. It has been a fluid trade for 18 months so that that feature will remain. The mills do have a tighter grip on certain items. This is related to logs and production. Most items are still under and over-produced within the typical timeframe. Timing that imbalance has always been a challenge. What remains in place is that a cash market run will not continue with some items tight and others abundant. The focus for this upcoming week will be on items liquidity. A sharply lower trade in May futures on Monday will give an immediate answer.

The macro picture has to be looked at. We can see the data on fewer shipments, log issues, fires, and the “worm.” What we can’t measure today is the potential headwinds of a slowing economy, rates that are higher for longer and affordability. All that is slowly creeping into the multifamily side of the business. That we can measure. The question is if a slowing multifamily sector takes the energy out of the starts number going into the fall. If it happens, we can expect a flat trading range that mirrors 2023.

The industry has to look to futures to lock in a profit or to mitigate risk. Playing supply spikes isn’t the best strategy.

Technically, this market has strong support all the way down from here. The key points are the 38% at 598.80, the 50% at 590.70, and the 61% at 582.60. A close over $620 indicates the funds are back in charge.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636