AG MARKET UPDATE: SEPTEMBER 30 – OCTOBER 12 USDA REPORT

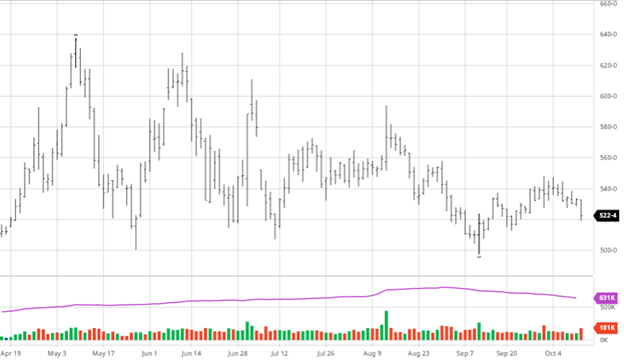

Corn had been in neutral heading into the October 12th USDA yield report, seeing bearish numbers. The report raised yield to 176.5 bushels per acre, slightly higher than the report last month. U.S. ending stocks and world stocks were both raised while also raising exports, lowering feed and residual use. The somewhat disappointing yields in the eastern corn belt were offset by better-than-expected western corn belt/plains yields. Demand looked to be lowered due to the continued export issues out of New Orleans since the hurricane, and a record crop in China won’t require them to import as much. The season-average corn price received by producers was left unchanged at $5.45. A higher yield and supply is bearish news, but the numbers do not appear to have been bearish enough to where we will retest harvest lows anytime soon. The cash market will continue to give us an idea of how much corn is actually out there, along with private estimates as harvest rolls on.

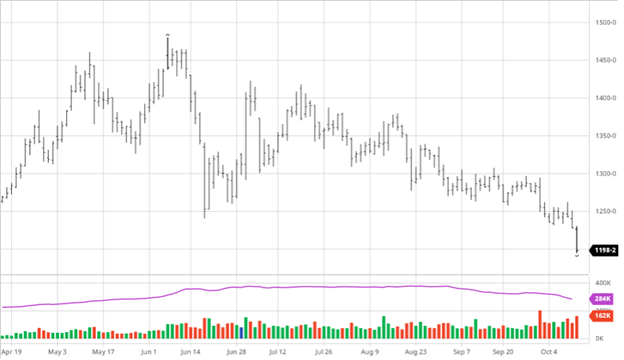

Via Barchart  Soybeans have been struggling the last couple of months, and the previous two reports have not done them any favors. As you can see in the chart below, it has been tough sledding since early June for beans. The USDA raised yields to 51.5 bushels per acre, up from the September report. The feeling that the U.S. bean crop was getting bigger with the good late-season weather came to fruition in the report. World stocks were also revised higher, creating another bearish concern. Without demand from China or a problem in South America, there aren’t many bullish factors for beans. If either China demand or SA weather turn in favor of the U.S., we could see some support, but until then, there is not much helping the market.

Soybeans have been struggling the last couple of months, and the previous two reports have not done them any favors. As you can see in the chart below, it has been tough sledding since early June for beans. The USDA raised yields to 51.5 bushels per acre, up from the September report. The feeling that the U.S. bean crop was getting bigger with the good late-season weather came to fruition in the report. World stocks were also revised higher, creating another bearish concern. Without demand from China or a problem in South America, there aren’t many bullish factors for beans. If either China demand or SA weather turn in favor of the U.S., we could see some support, but until then, there is not much helping the market.

USDA Report

The report covers many areas of the agriculture landscape. If you would like to view the full report or look at something else not covered, here is the link.

Dow Jones

The Dow bounced back this week following the rough end of September. Congress agreed to pass a short-term agreement to keep the government funded until December. There was a small amount of worry in the markets as the deadline loomed, but the same concern will return in 2 months when they need to pass a long-term plan and a debt limit adjustment. Any bounce back after a significant drop is good to see to level everyone’s heads.

Podcast

Check out our recent podcast where we’ve brought on one of our real-life firefighters from RCM Ag – Jody Lawrence, along with Tim Andriesen from the CME Group to provide us with some inside baseball knowledge of the current state of agriculture markets. They discuss the real-world application of short-dated options to fight the recent blaze of volatility surrounding agriculture markets potentially.

https://rcmagservices.com/the-hedged-edge/

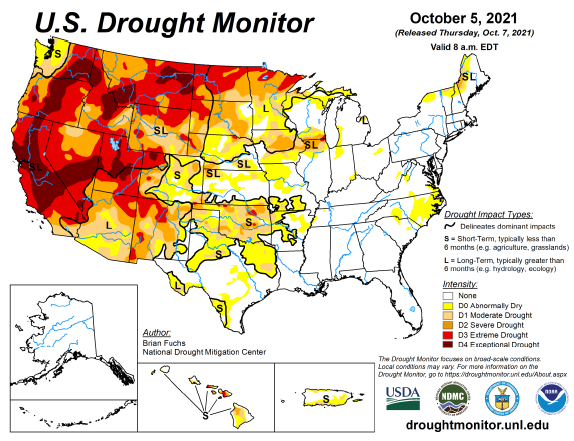

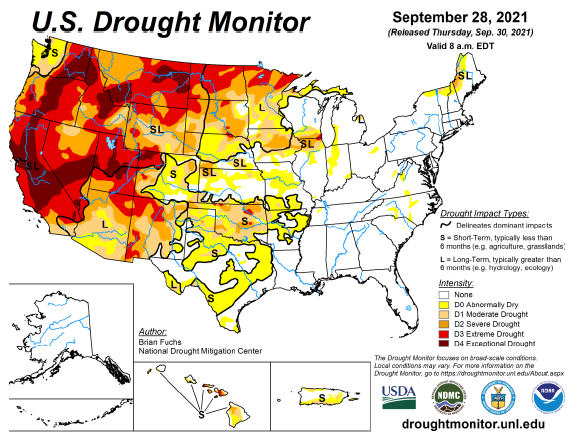

US Drought Monitor

The maps below show the U.S. drought monitor and the comparison to it from a week ago. The outlined areas in black are areas that the drought will have a dominant impact.

Via Barchart.com