Recap:

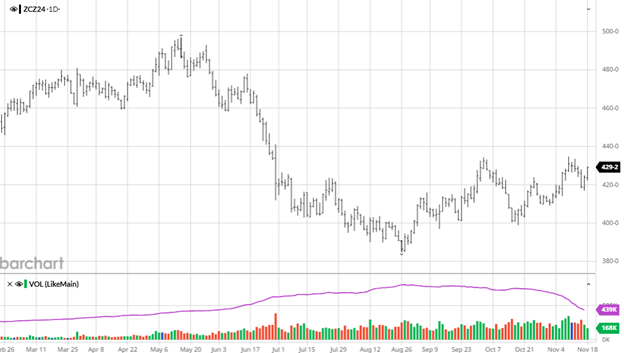

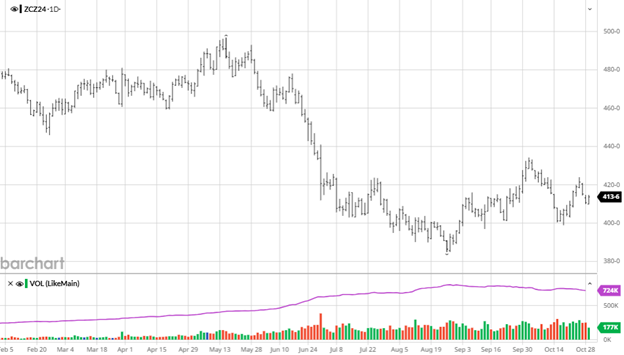

It was a tough week with selling pressure dominating. Who was selling? Most likely an algo that doesn’t grow a position. But I think the bigger question, and one that may linger for a few quarters, is why there isn’t much support on the way down. A quote Friday after existing home sales came out was troubling.

“On an annual basis, existing home sales (4.06 million) declined to the lowest level since 1995, while the median price reached a record high of $407,500 in 2024.” By the way, multifamily construction hit a record last quarter. The industry is very reluctant to participate beyond the contracts that they deal with.

New home sales do better as the existing inventories get sold. Today, with the higher interest rates and record costs, that won’t be happening any time soon. That leaves us in the same atmosphere in 2025 as it was in 2023 and 2024 when the builders created the market. That gives us the duty rally, the tariff rally, and finally, the shutdown/supply rally. At no time does it chase the industry into the marketplace to load up.

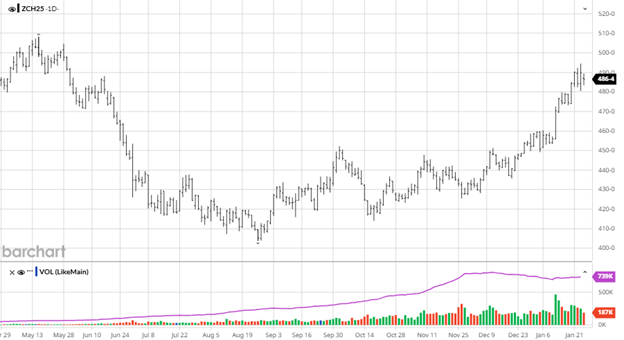

If nothing else, the trade is consistent. It made a high and then came back down to value, or at least what the charts call it. We spent a lot of time trading like this at $520. Value is determined by the volume traded in that area. $565 has had a lot. Have we moved our value area from 520 to 560? Too early to tell. The algo type selling strains the market but doesn’t represent it. The industry’s next move will. Just remember, business isn’t dead.

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636