Recap:

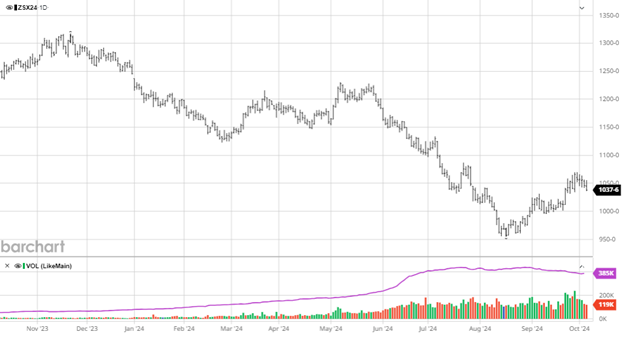

It was a very healthy week for both cash and futures. As a combination, it was the best week for price movement all year. The key was the market went higher on its own. There was no outside noise to push it. It was all demand driven. That leads us to three simple scenarios. The first is that the market is still underbought and will stay tight. This could be the case as the “off the market” mill is back in the game. A slow buy could drag the market higher since we’ve had a few years for the buy side to be engrained with less is more. The next scenario is that the market is searching for a new trading level, which would be higher. Futures may pull back and wait for cash but shouldn’t break sharply. Maybe good selloffs followed by rallies. Finally, the typical futures trade. Here, futures drop at least 61% back, often in a quick second.

My first thought is that the reduction in production is noticeable when demand picks up and then fades into the background as the market slows. We have a good handle on the industry’s inventory capacity. Without a logistics issue, capacity will always put a top in the market. Today’s question is whether we should remain confident in the numbers when supply is limited. The trade is content to stay the course. No one has seen any demand creep yet. This run is only a shot over the bow.

A critical factor in this industry is interest rates. Most haven’t noticed, but since the Fed cut on September 18th, the 30-year mortgage rate has risen by 80 bps. Going into 2025, the builders will negotiate the marketplace at a 6 to 7% rate. The Fed is looking for a 3.5 to 4% nominal rate, up from 2%. That will keep the 30-year locked above 6%. I go back to my “check the boxes” strategy. The multifamily guys will find a way to make the higher rates work. There is a ton of money in this sector that likes condos and apartments. They don’t like to “divest”. They value this sector. Our multifamily guys should look for an uptick next year in bidding. I’m not sure SYP isn’t already signaling things are getting better there.

Again, this is a multifaceted industry. The financial drivers go well beyond the mills and distributors.

Technical:

Jan had a $41 run from last Friday’s lows to the highs this week. That’s big. The stochastics were the first indicator of a possible rally. The other oscillators followed. Last week, I commented that the outside spec trade would see lumber as a buy. I’m not sure how much they participated, but we saw a big push through a small hole. Coming into this week, the signal is to sell. With a January RSI of 82.77% and a lag to the rally, they will see weakness and room to the downside. My point is that the futures market is overbought. The cash market isn’t.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636

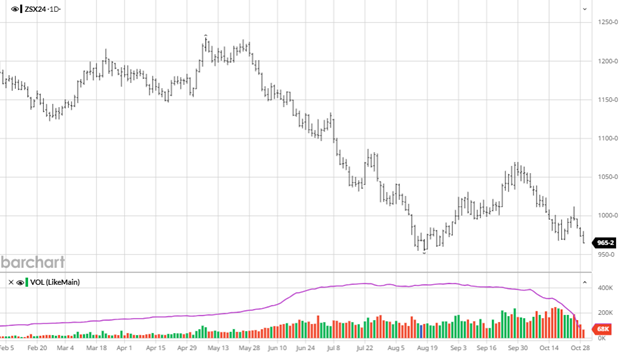

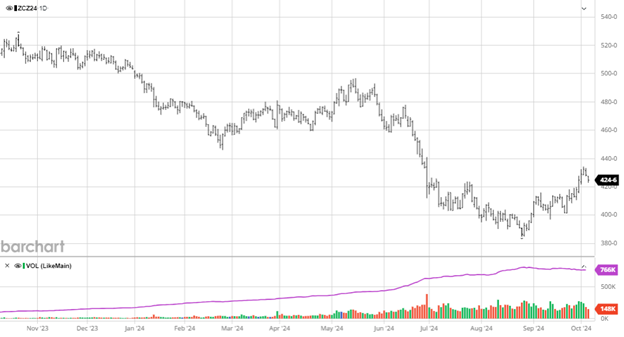

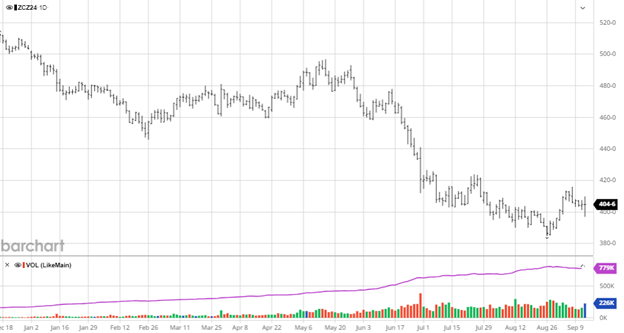

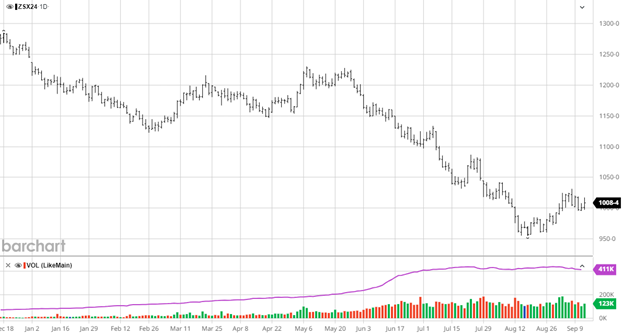

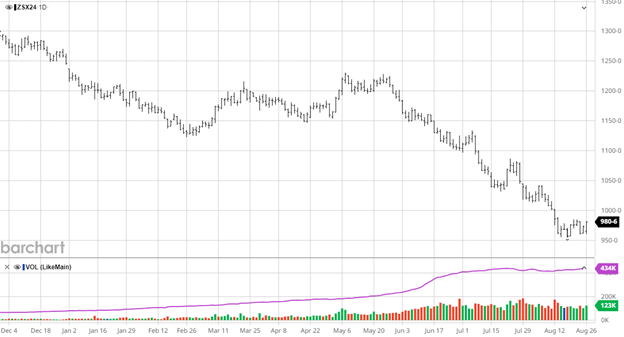

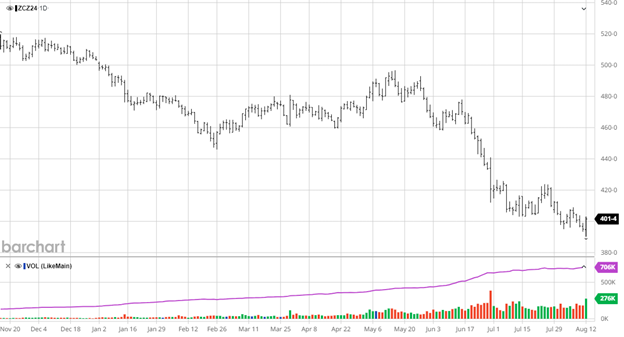

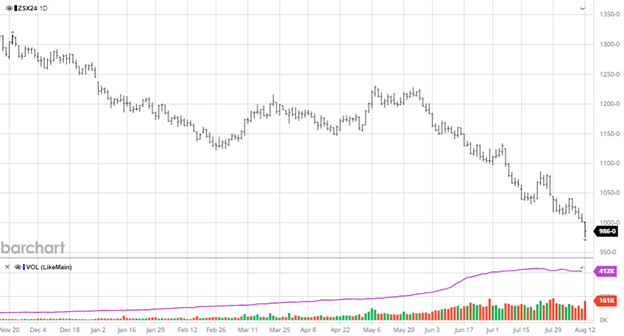

Soybeans weakness over the month has lowered it with corn. Beans do not have any bullish news on the horizon as they failed to rally through technical resistance. With the election next week, a tariff war with China would hurt beans in an already depressed market as we have seen in the past. Funds are very short and will need a catalyst to get them to change course, which currently is lacking. Bean harvest is 89% complete which means there won’t be much opportunity for unexpected bullish news moving forward.

Soybeans weakness over the month has lowered it with corn. Beans do not have any bullish news on the horizon as they failed to rally through technical resistance. With the election next week, a tariff war with China would hurt beans in an already depressed market as we have seen in the past. Funds are very short and will need a catalyst to get them to change course, which currently is lacking. Bean harvest is 89% complete which means there won’t be much opportunity for unexpected bullish news moving forward.