The Lumber Market:

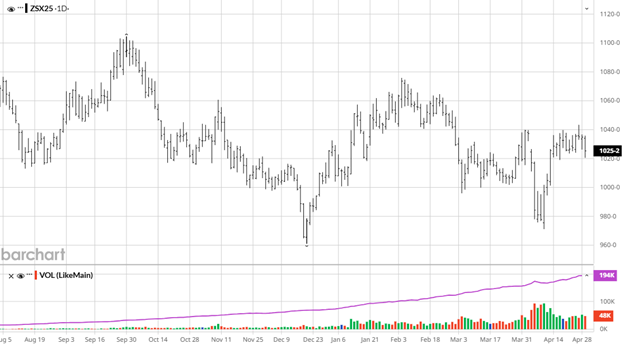

The futures market continued its trek higher on a journey to find real price discovery. A report midweek about two SYP mills taking downtime confirmed the reality of less product in the future. But at the same time we saw more weak housing news compounding the problem. Add to it that Trump in now loading both barrels and pointing it at Canada. The possible 25% tariff just keeps showing up. What we do see is many items holding lower levels because of the lack of demand. There is no reason to wait on these items in today’s environment. As long as the industry procrastinates the more chance there is for a spike higher when the SHTF. If it turns out to be a non-event, sell the board.

Technical:

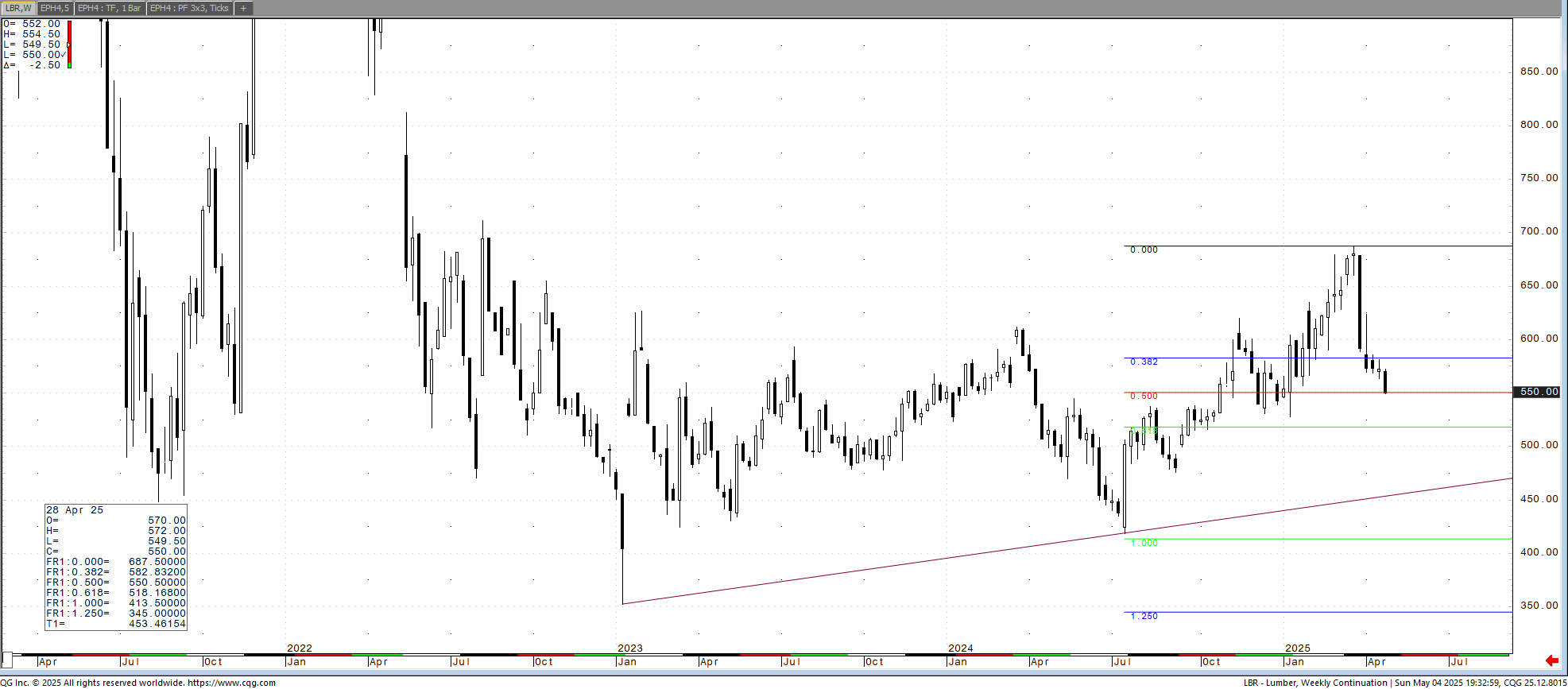

The midweek gap in September from 648.50 to 649.50 is a momentum gap. We can come back and close it early in the week making it more of the same or we can see additional momentum following it up. That would bring the 4-month gap of 673.00 to 708 into play. I do have an issue with a 76.80%. That is toppy without the momentum. I will say it could be less of a fact when we analyze the trade. The market shot up with the tariff announcements. These has been no resolution to it. Whatever the catalyst for the initial rally, a precedent was set. Any movement towards a tariff again pushes prices back up there.

This could take some time to play out. Owning cash at low levels with a good basis available has been the play for 3 years now. Today there is too much wood out there. It doesn’t mean you shouldn’t own some.

Daily Bulletin:

Southern Yellow Pine:

The Commitment of Traders:

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636

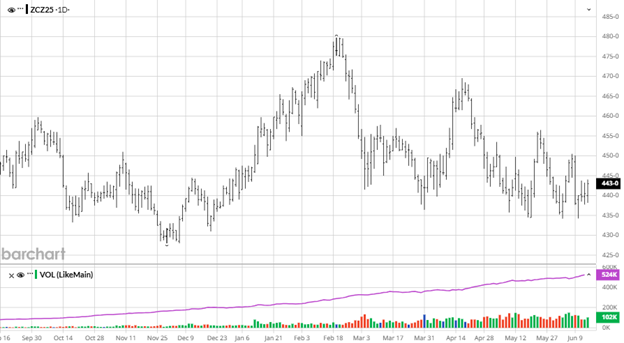

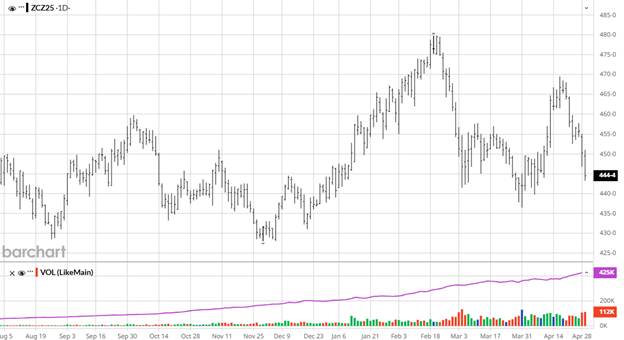

Soybeans gave back the recent gains as well last week before the report on June 30th. Beans will likely continue to trade in the range they have been until we receive news to direct the market either on the trade agreement side or weather. The Planted Acres report had 83.38 million acres, slightly below expectations. The tax bill going through congress right now may give beans some help by getting rid of a 45z tax credit loophole but until this thing passes everything is on the table to get cut from it. Weather is good for the next 2 weeks so the market needs positive news from a US and China trade deal to give it a boost.

Soybeans gave back the recent gains as well last week before the report on June 30th. Beans will likely continue to trade in the range they have been until we receive news to direct the market either on the trade agreement side or weather. The Planted Acres report had 83.38 million acres, slightly below expectations. The tax bill going through congress right now may give beans some help by getting rid of a 45z tax credit loophole but until this thing passes everything is on the table to get cut from it. Weather is good for the next 2 weeks so the market needs positive news from a US and China trade deal to give it a boost.