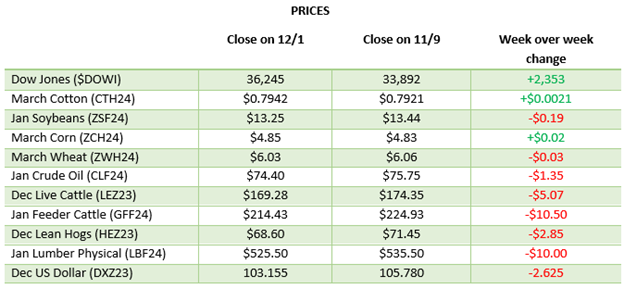

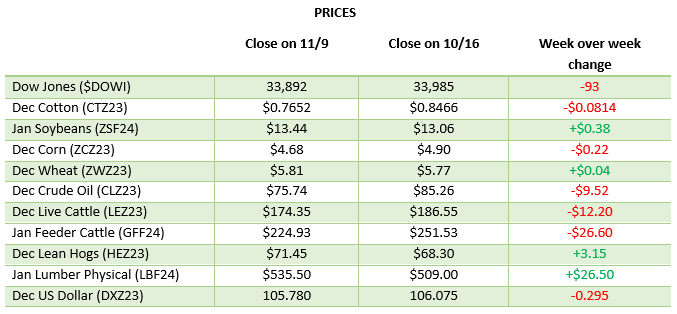

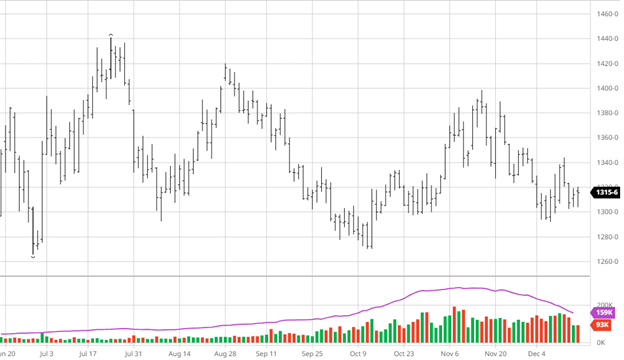

Corn has been rage bound for the last two weeks with no catalysts in the market to move it much either direction. The weather in South America has improved slightly in areas that got off to a tough start but doesn’t seem to have made much a difference on the market. It is still a wait and see approach for the South American crop, nobody wants to jump to conclusions. Th Biden administration is supporting tax credits for ethanol-based sustainable aviation fuel, which would result in a major new demand source down the road. The markets will likely be muted in both volume and price movement as we head into the end of the year.

Soybeans have bounced around the last couple of weeks with a steady stream of exports and the Argentinian peso devaluation. The latest crush report from NOPA recorded a record for the month and about 3 million bushels more than pre-report estimates. The demand for beans has been there and seems to be significant but with so much time still to go before South America’s crop is known. Estimates keep shrinking the Bazil crop, which the market shrugs off, making it a hard market to be overly bullish in when good news is not met with good market reactions.

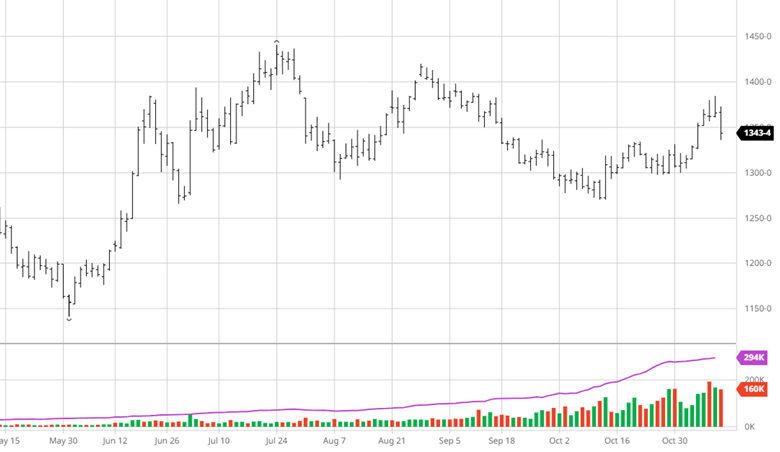

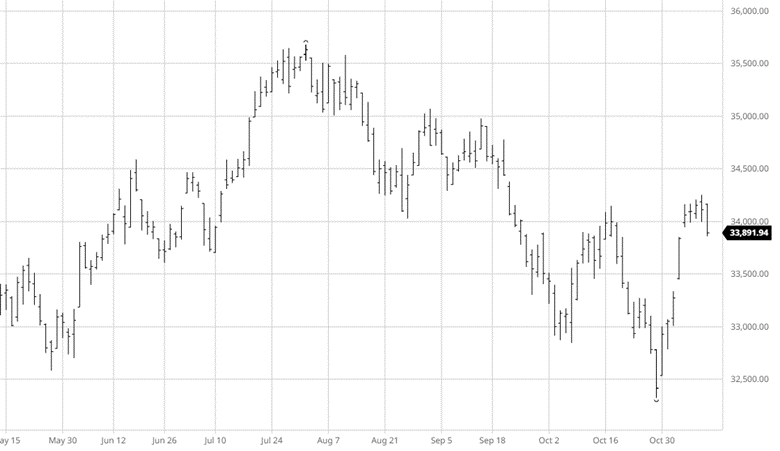

Equity Markets

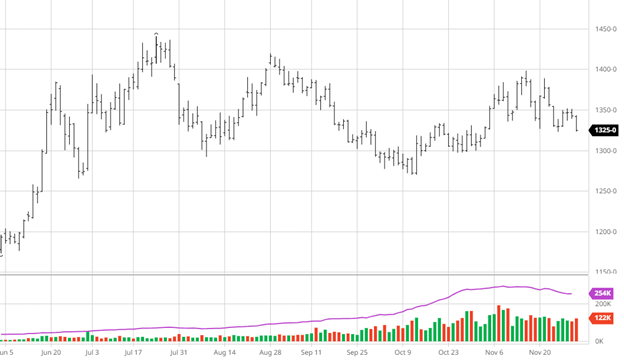

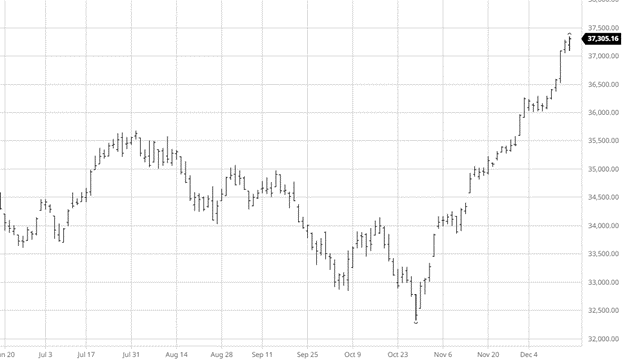

The equity markets continued their run higher this week as the Fed kept rates steady and seem likely to begin cuts in 2024. The rest of the market has begun participating as the Magnificent 7 stocks had done most of the heavy lifting to this point. Analysts are still warry of a soft landing recession but for now the markets are moving higher in the short term.

Other News

- The Fed held rates steady this week with markets expecting them to start cutting in the first half of 2024.

- Argentina devalued the peso by more than 50% to try and help the nation’s struggling economy.

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.