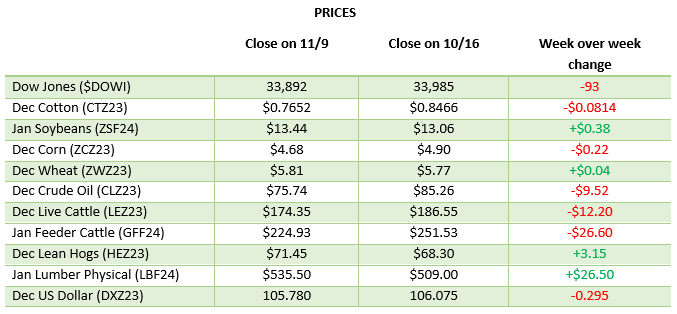

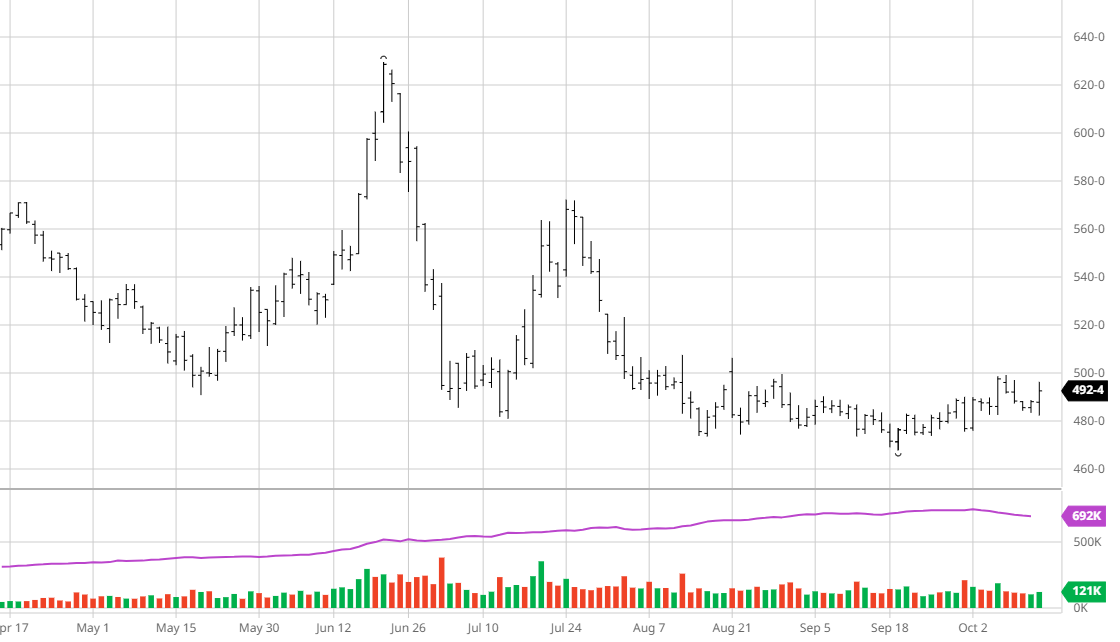

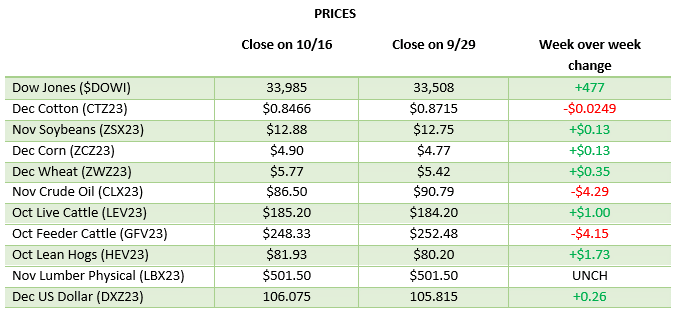

Corn has had a rough month as it continues its sideways to lower grind after briefly touching $5.20 in October for the March contract. While there has not been any major market news to direct the market a strong weekly export report this week was welcome to the market that had been bleeding lower. The last few days saw a nice reversal, seeing a 14-cent rally off this week’s lows. Basis has taken a nosedive in many areas of the country hinting that there may be more corn out there than initially expected. With harvest all but wrapped up for most of the country it will be worth keeping an eye on whether farmers store the corn and hope for better basis or get it off their books to pay back operating loans at the highest rates we have seen in years. Brazil’s weather remains about the same with beneficial rains expected over the next couple of weeks in the drier areas north and the south remains wet.

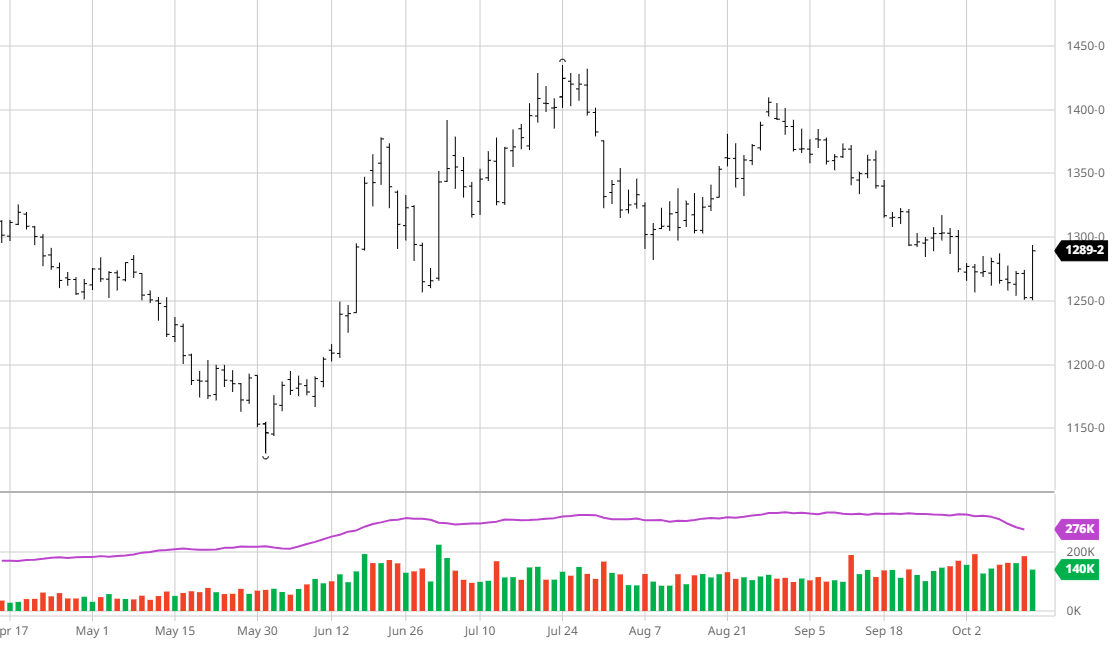

Soybeans have fallen over the last couple of weeks but is in a sideways trade in the big picture. Exports were not as strong as corn but better than expected. Brazil’s weather is the main focus for beans right now as the north is drier than normal and the south is still wet. The bean demand from China is welcome, as always, but sustained demand and not just demand while Brazil is having logistic issues will be important. The amount of rain in Brazil next week will be the main market mover until the report on Friday if we get some surprises.

Soybeans have fallen over the last couple of weeks but is in a sideways trade in the big picture. Exports were not as strong as corn but better than expected. Brazil’s weather is the main focus for beans right now as the north is drier than normal and the south is still wet. The bean demand from China is welcome, as always, but sustained demand and not just demand while Brazil is having logistic issues will be important. The amount of rain in Brazil next week will be the main market mover until the report on Friday if we get some surprises.

Equity Markets

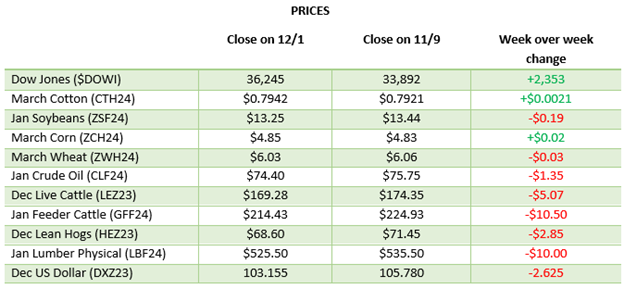

The equity markets had a great November seeing strong gains across the board as the Fed speak has turned dovish and inflation continues to cool. The markets are pricing in the Fed beginning to cut rates in the first half of 2024 while the general consensus by large companies and funds is that a mild recession is still in the cards next year. The big names had a good month and the 10-year note fell, but it was encouraging to see some laggards join the party. The end of the year always involves some shuffling, but economic data will continue to move the markets now that earnings are past.

Other News

- Charlie Munger passed away this week at the age of 99. A longtime investor and one of the brightest minds for financial markets the Berkshire Hathaway investor left his mark and knowledge on the financial markets.

- The next WASDE Report is Friday, December 8 at 12 ET

- Brazil is set to join OPEC+. Brazil produces about 3.7 million barrels a day which makes it a top 10 oil producing country.

- The ceasefire between Israel and Hamas ended as hostage swap negotiations stalled. The unrest in the Middle East will continue to dominate headlines.

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.