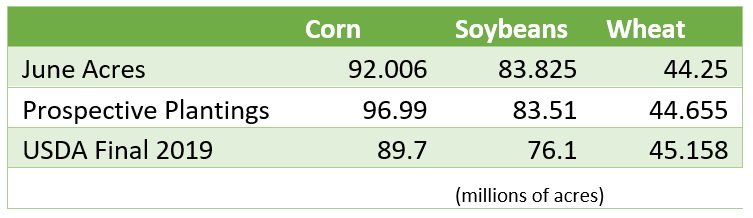

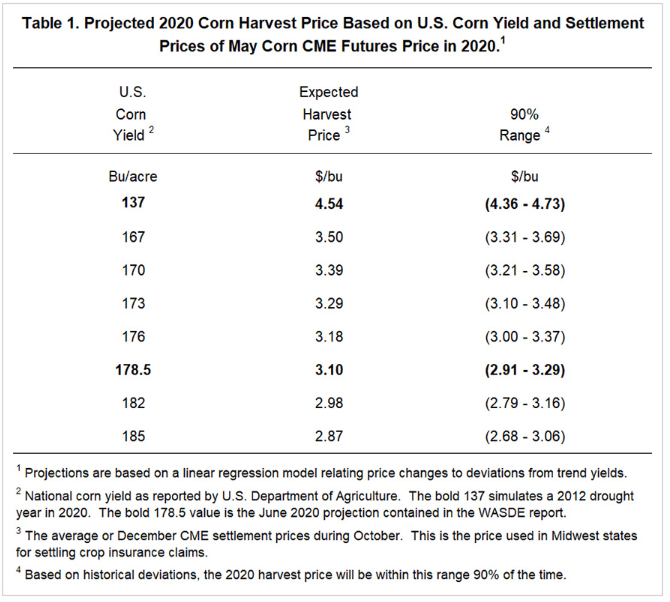

As weather across the country continues to be supportive for the crops corn prices have dropped. The past few weeks of timely rain and cooler temperatures has put a trend line or record national yield very much in view. From talking to farmers across the country many think this has potential to be one of their best crops and as great as that is everyone knows the larger the yields the lower the prices tend to be. With China well behind on their phase 1 trade agreement purchases, corn will need to get support elsewhere unless China decides to ramp up their purchases in the second half of 2020. Keep an eye on the flooding in China as they have lost over a million acres of farmland and will tighten their supplies. The higher crop conditions this week did not help prices either as they came as a surprise.

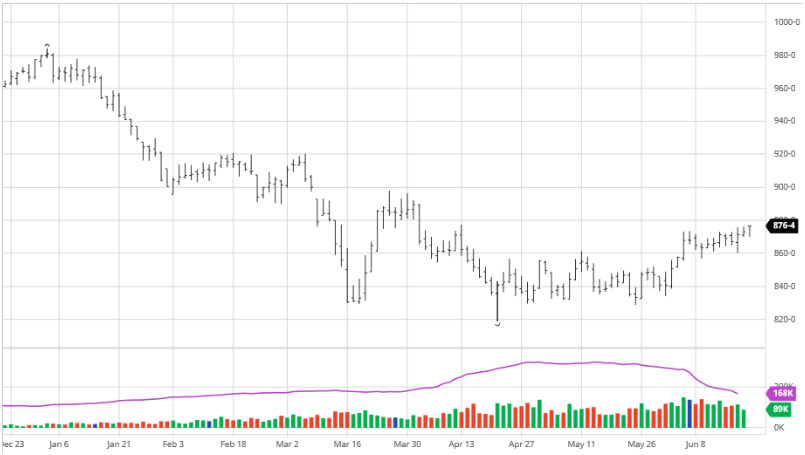

Soybeans and corn are in a similar situation where large yields are very much in play due to the weather of the past month and what looks to be coming. Soybean exports continue along at a good pace but nowhere near the Phase 1 agreement numbers that were expected. If China can ramp up their purchases in the coming months beans can get a boost that is unlikely to come without a weather problem. The good export news of late has been offset by good weather and higher expected yields which is frustrating seeing bullish news be uneventful for prices.

After a short term pull back from the near term highs markets bounced off a technical low and appear poised to give the highs another run. Weather watchers will be tracking hurricane Isaias and it’s potential impact to the delta over the weekend. In many cases the fear of hurricanes has been bigger than the actual punch. In reality, following the storm days in advance does little good and is often a story of buy the rumor and sell the fact. Look for prices to test the 65 cent level and be prepared to increase hedge protection above 63.50.

DOW Jones

The Dow continues its slight downtrend this week as Covid-19 cases remain high in many parts of the country. Despite good vaccine news coming out this week as several promising candidates move onto the next phase of trials, the Dow fell again. All eyes were on Capital Hill this week as Google, Facebook, Amazon and Apple’s CEOs were questioned by politicians looking at anti-trust issues. These were not huge market movers but something to keep an eye on as these companies have helped lead the charge up from the lows back in March along with other big tech companies.

Via Barchart.com

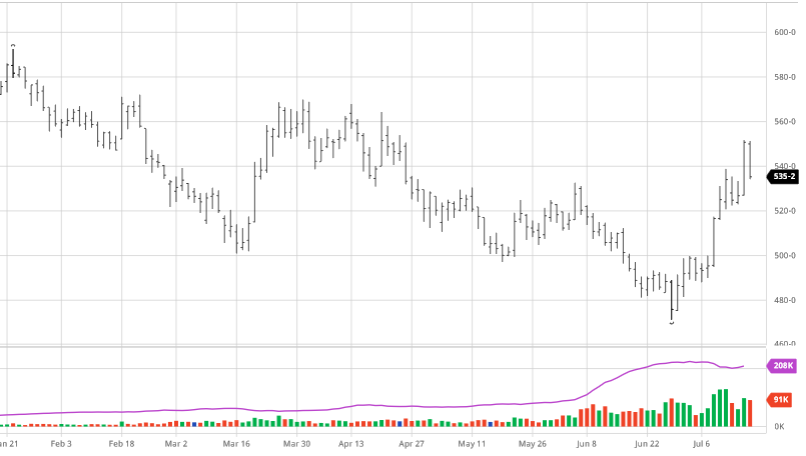

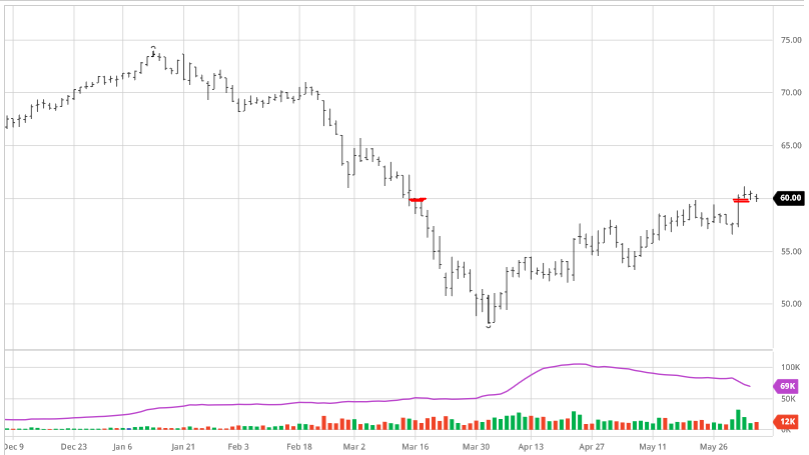

Large purchases from China gave Wheat a big boost halfway into the week. Wheat did have to give a good chunk of that boost back the following day due to a lack of confirmation on purchases, but any Chinese purchases at this point are beneficial to the markets as other Wheat growing countries are seeing lower yield numbers. As you can see below, markets are well off the lows that we set a few weeks back as Wheat has made a solid rebound. Just like with Soybeans, more confirmed purchases, or any purchases for that matter, would be beneficial to U.S. Wheat.

Large purchases from China gave Wheat a big boost halfway into the week. Wheat did have to give a good chunk of that boost back the following day due to a lack of confirmation on purchases, but any Chinese purchases at this point are beneficial to the markets as other Wheat growing countries are seeing lower yield numbers. As you can see below, markets are well off the lows that we set a few weeks back as Wheat has made a solid rebound. Just like with Soybeans, more confirmed purchases, or any purchases for that matter, would be beneficial to U.S. Wheat.