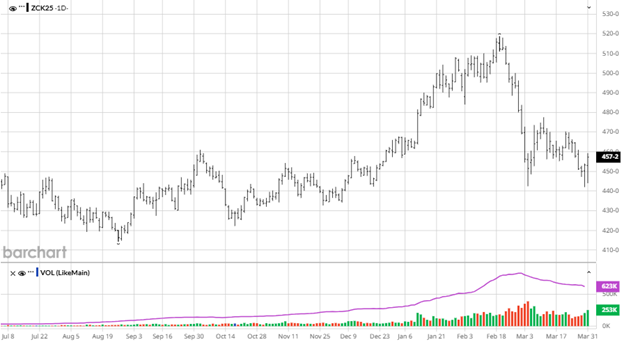

Corn has been trading sideways since the end of October and nothing from today’s USDA Report gives it reason to change course. The main news for corn has been the lack of news. Corn did dip 20 cents in late November but bounced back to the middle of the range it has been in around $4.45. In today’s USDA report they kept US production the same while raising the export forecast by 125 million bushels, lowering US ending stocks to 2.029 billion bushels. The global stocks number was also revised lower with production cuts to other countries, including Ukraine. While the report was modestly bullish corn will need some more news to leg up to the $4.60 range as South America is off to a great start.

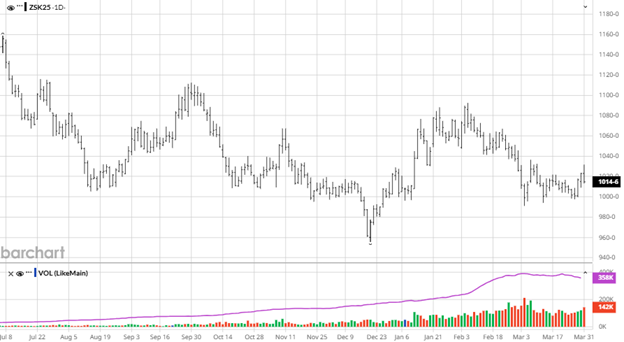

Beans have tumbled off their recent highs as the rocket higher ran out of fuel and has been giving back those gains. The USDA left US production the same with an overall neutral report with no major surprises. Global stocks were slightly raised as Brazil, India and Russia offset tighter supplies elsewhere. With no news to turn this recent downtrend around the market needs positive China trade news desperately as that was the initial “news” to drive markets higher.

Equity markets have rallied from the November dip and are within a couple % of new all time highs. The markets are expecting another rate cut this week and would be surprised if there is not.

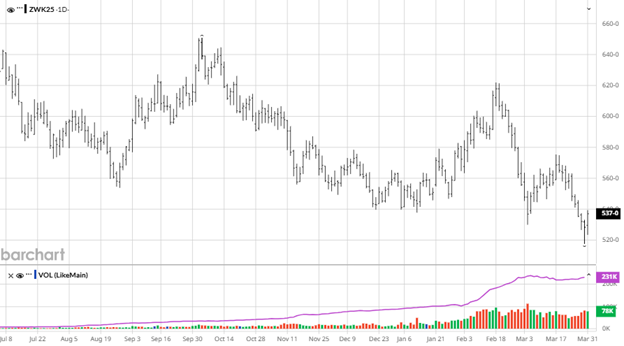

The wheat numbers were mostly unchanged and did not have any major news to change the direction of trade but could turn around on global trade news.

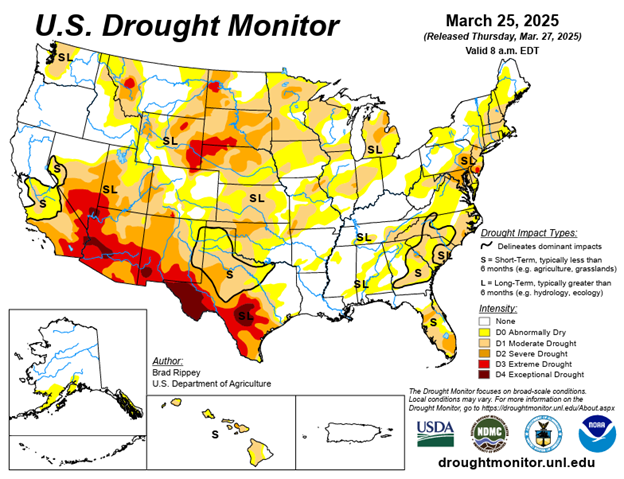

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn’s Thursday rally was met with a post report Friday dip and gave up 10 cents back to $4.30. Despite the late season crop problems of drought and rust, the USDA did not find the corn yield loss that was expected and came in with a 186 bu/ac estimate, higher than the trade estimate. With higher production came higher US ending stocks, but those were not raised as much as yield as corn exports and domestic industrial demand has been exceptional this fall. The chart still looks constructive, but after a 30-cent rally in one month, the market will look to take a breather, especially after today’s report.

Beans have been on a great run higher, albeit with some volatility, until Friday’s USDA report. Coming in that hot to a report can lead to a let down which we saw to some extent. The bean yield numbers were not as surprising as corn, coming in close to estimates, but the market still took a hit. The number to look at was the US held bean imports to China unchanged at 112 MMT for the 25/26 marketing year. A flash sale report did show sales of 1.1 mbu to China around the time the trade deal was in the works. The delayed data is hard to fit with all the other news out there but China buying anything is a good sign.

Equity markets have been volatile the last few weeks as worries of an AI bubble continue and several large companies such as Palantir, Meta and Oracle are well off their 52 week highs. Volatility will likely remain in the market for a bit as we will get caught up on economic data that was missing during the government shutdown.

The wheat numbers were bearish as domestic and world stocks continue to climb on record world yields in all producing countries and exporters finding exports difficult to come by even at rock bottom prices. Wheat will remain an anchor on corn rallies.

Cotton adjustments show 900K more bales of US production, 200k more bales of US exports, and 700K more bales of US ending stocks compared to September.

Drought Monitor

Here is the most recent drought monitor as harvest rolls on.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn had been trading in a range north of $4.20 the last couple weeks but dropped below there on the heels of the Sept 30th USDA Report. The USDA raised US ending stocks for corn from 1.325 billion bushels to 1.532 billion which pushed December corn prices to new 1-month lows. With plenty of supply and massive crops in both the US and South America the last 2 years, balance sheets have ample supply while demand for US corn remains strong outside of demand from China. With funds holding bearish positions, it will take a combination of them changing their tone and China showing up with purchases to give prices some news to rally on unless we get in the fields and the yield just isn’t there.

Beans were lower post USDA report as well despite the report being neutral continuing their recent downtrend. The biggest hit to beans in the past couple weeks came when President Trump and President Xi had a call and no announcement of Ag purchases were made around it. Without China buying US beans there is no major upside currently, except for potentially lower yields. South America’s crop has been able to satisfy China’s needs as that trend will continue moving forward until they run out of supply.

Equity markets continue to trade at or near all time highs as a slowing job market could lead to more rate cuts after the Fed cut by 25 basis points this month. While GDP growth had a strong bounce back quarter and the stock market is still doing well, fueled by AI stocks, the overall economy is showing some warning signs but remains strong.

Wheat continues to make new lows with a slightly bearish USDA report with larger US production.

Corn harvest is 18% complete and soybean harvest is 19% complete.

It seems more and more likely that there will be some extra government assistance to farmers this year with the depressed prices.

Drought Monitor

Here is the most recent drought monitor as harvest begins.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

This episode of “The Hedged Edge” explores the critical challenges facing US grain exports, focusing on wheat quality and Mexico’s market dynamics. Hosts Jeff Eizenberg and Ben Hetzel, joined by David Munoz from Bartlett Grain, discuss the USDA report, global grain trade complexities, and the potential risks of losing Mexico as a key buyer due to inconsistent wheat quality. The episode provides insights into transportation logistics, international competition, and strategies for maintaining competitive grain exports in a challenging global market.

___________________________

___________________________

Check out the complete Transcript from our latest podcast below:

Quality or Quantity: Keeping Mexico as a Key US Grain Buyer

Jeff Eizenberg 00:54

Welcome to the next episode of The hedged edge. I’m your host, Jeff Eisenberg, and I’m here with my co host, Ben Hetzel. First of all, we can’t thank everyone enough for being a part of last week’s inaugural episode. The feedback from the community and everyone around was fantastic. And again, can’t thank enough to kbjm and kndc for hosting us. These episodes are designed to be here for the community, to be able to participate and engage and learn a little bit of something exciting today that Ben and I are on the air again here with you. It’s shortly after the September was the report. But here’s the shock. What people really need to know is that Mexico’s mills are asking for wheat from the United States that hasn’t consistently delivered. If we don’t raise the quality, we could lose our cornerstone buyer.

Ben Hetzel 01:42

Yeah, thanks, Jeff. Exciting to be on again today. Thank the listeners for tuning in to us here on the radio, and the people that download our podcast. We did have the USDA report out, kind of some minor tweaks, really honestly, Jeff, not a lot of news for the wheat side. Little bit of news on the corn side, and not much of anything for soybeans as well. So I guess on the wheat us ending stocks at 840, 4 million bushels supportive versus the estimates that were the trade kind of thought 865, global ending stocks at 264 point 1 million metric ton, a little heavier than expected, which keeps a little pressure on, but overall, not a big shock.

Jeff Eizenberg 02:30

And I agree with you, there Ben on the wheat. The biggest shock to me was two things, one in corn, 1.4 million additional acres planted acres. That’s 98 point 7 million planted acres, the largest ever. And then number two, you look at that number, most people will be running for the hills, thinking the market’s going to sell off, but no, we were able to rally the market about six cents. Now, you know, I don’t know how you feel, but that, to me, is about as shocking as we could expect,

Ben Hetzel 03:02

yeah, yeah, it is always interesting when you get these reports of what’s actually going to happen and what’s moving. The market. Did not expect the rally today in corn off of that it looked like beans rallied a little bit at the close as well. Or we had oil up pretty good today. But wheat, wheat stagnant, fell a little bit at the end.

Jeff Eizenberg 03:25

There we go. And then ultimately, on the beans side, the reality is we don’t have any buyers, and China is still absent and unavailable for purchases of beans. So we’ll see how that shakes out into the into the quarters ahead. But you had a comment then that you and I, you and I, you and I are talking about storage. It was kind of interesting.

Ben Hetzel 03:44

Yeah, I happened to run across the little article on the available farm storage versus the production. And production outpacing farm storage quite significantly. You got states like North Dakota at 131% versus storage. You’ve got Kansas at 133 versus storage, Missouri at 129 South Dakota, 128 pretty much all the states, until you get into the deeper south, well into the 15 to 30% more production than storage available. So it’s going to be interesting in what appears to be some challenging marketing conditions. We talked a little bit last week. One interesting thing, we talked about the potential for a nice crop of corn out in these fringe areas like western North Dakota and South Dakota. We did end up freezing quite a bit of our corn, so and soybeans. So it’ll be interesting to see how that all pans out, what what corn was far enough along, or what beans were mature enough to handle that frost. But we definitely will see a reduction,

Jeff Eizenberg 04:50

and you guys are now the you’re the wettest and the coldest, yeah.

Ben Hetzel 04:55

So it’ll be, it’ll be a challenging harvest for most producers. That have row crops and a lot of questions unanswered yet, you know what to do with this, this stuff, if it does end up having significant issues and so lot to unpack there down the road, but significant production all the way around. We talked a little bit about that last week too, Jeff, that there’s so much wheat, so much corn going to get harvested. Beans going to have a really big yield on beans, comparative even with acres down, we had a big canola harvest in the US. We’re expecting a big harvest in Canada. So one thing we are seeing in Canada is some quality issues, similar to what we’re kind of experiencing in western North Dakota in general, on the wheat side, but again, just big bushels, even with acres being down on some of these particular crops, not all of them, of course, we just learned on the corn. But the market is not really the same status quo as what we’ve seen, especially on soybeans, so stuff’s gonna have to find a home, and we’re seeing challenges on the wheat for sure, already.

Speaker 1 06:08

If you wanna listen back to this episode or find past episodes of The hedged edge, visit kbjm.com or kndc radio.com under Listen Live and podcast options, or either stations, free mobile app under podcasts,

Jeff Eizenberg 06:23

okay, flipping over to today’s topic, quality or quantity. Why the US risks losing Mexico. Ben, we’ve got our guests here with us. He’s online. Would you mind a quick intro?

Ben Hetzel 06:34

Yeah, thanks, Jeff. It’s my pleasure to introduce David Munoz. David is our guest today. He’s he was born and raised in Mexico. David spent the past 15 years in ag commodity trading stints in Mexico, China, Singapore, Thailand and now the US. He spent nearly a decade with serious global Ag in Minneapolis, focused on spring wheat and global supply and demand. He’s now helping integrate with Bartlett grain, who they just teamed up with out of Kansas City. David brings truly international perspective of grain markets, and he still finds time to spend with his wife and two young daughters. Welcome, David, glad to have you on here. It’s it’s a pleasure to have you join the podcast today. I’m excited to see where the discussion goes today with wheat in general, but global supply and some of the trade partners we have around the globe.

David Munoz 07:32

Excellent. Hi friends. Jeff, thanks very much for inviting me. Happy to be here. Absolutely.

Jeff Eizenberg 07:38

And David, your company is just merging. Could you give us a quick background there? It’s pretty

David Munoz 07:43

exciting. Yeah. So series global, AG, also known as Riverland. AG, here in the US, it’s been in operation for 15 plus years. Not that long, we operate a series of assets, physical assets, warehouses, elevators in Minnesota, North Dakota, and then across the border in Saskatchewan and Manitoba. It’s headquarter in Minneapolis, where I am based. And I personally been with the company for, like you said, for almost it’s gonna be eight, nine years soon. And just a couple of months ago, Bartlett grain was based in media in Kansas City. I’m sorry they decided to acquire our company. So at the moment, we’re in that period, that transition and merging with them. And I think it’s going to be exciting, as they have. They have some strengths, and we have some, and there’s some. Was no overlap, and the whole thing made a lot of sense, was probably going to make us stronger as one

Jeff Eizenberg 08:32

company. That sounds great, exciting. I gotta, I just gotta jump right in and ask you, you grew up in Mexico. Right now, Mexico is the quasi Savior to our American grain crop. And so can you help us all understand just a bit more? Is this truth or fallacy? Is the Mexico the great Savior?

David Munoz 08:53

Well, I mean, it’s truly just, I mean, it’s a neighbor. It’s there’s a lot of compliment each other, both countries. The infrastructure has grown expanded, and it’s much better than it used to be. And obviously, since the free trade agreement in the 90s, Mexico is is one of the top buyers of us, grain, bulk grain commodities. And then obviously Mexico sense what Mexico is good at in exchange towards north of the border. So there’s a lot of compliments, like I say, the population has grown the animal protein, the animal sector has grown as well. So that demands more and more corn meal, all types of protein. So it’s been, it’s been, it’s been a good market for the US in general.

Jeff Eizenberg 09:37

It’s good and, well, we can’t forget about the tortillas, right? So exactly.

David Munoz 09:41

So those are white corn. So Mexico self sufficient in white corn. But all the yellow corn then comes goes to the feed sector and the industrial sector like starches, but also as the population changes its diet, basically eating little bit less of tortilla, less corn, more wheat based products that require flour, that. That’s where the wheat consumption has has also grown over the years. And there’s some wheat production down there, including including a Derm, for instance. But there’s, it’s just clearly not enough, and the geography doesn’t lend itself. The US produces much better and cheaper, cheaper levels. So that that’s, well, it all makes sense. So that’s good market.

Ben Hetzel 10:18

So David, help our listeners understand, how does most this grain get to Mexico? You know, those of us in the trade understand, and that’s how I got to know you, obviously, through trade. But for the average listener or the producer out there, shed a little light on how we how we transport most of the screen. Obviously, we’re a border nation, but there’s more to it, right?

David Munoz 10:42

So I think that it’s pretty interesting, because it really comes flows across the border in all modes of transportation, primarily by rail, so the so called shuttle trains, so 110 car trains that carry 400 plus 1000 bushels of whatever, soybeans, corn, wheat, that’s the main transportation. Probably around 60% of the trade happens through that mode. But then, obviously, through the coasts, you have a bunch of it. So it goes through the river, gets loaded at the Gulf, both Louisiana or the Texas Gulf, and then goes through the main, the primary port, which is Veracruz. And that’s how probably 35 40% of all the exports from the US to Mexico happen. There’s some that also happens through the Pacific Northwest, where, let’s say, soybean crushers are based near the Pacific in the Guadalajara area. And then they bring the vessels through there. But then we also even have trucks, right? All what Texas produces, for instance, that’s, there’s a lot of trucking that happens just just by truck from Texas, so you get it all. So like I say, it’s just wheat, roughly what Mexico brings in from the US is primarily wheat, corn. Yellow corn is by far the biggest. Then you have soybeans. You have some meal, more and more with a with a crushing industry growing in the US, there’s a lot of meal. There’s going to be a excess supply of soybean meal, so that a lot of them is now making its way down there as well, although there’s some US based companies that have and domestic companies that have crushing facilities there. So that’s, that’s, that’s that also happens quite a bit.

Speaker 1 12:13

Want more agricultural market expertise. Listen to full episodes of the hedge edge podcast, wherever you get your podcasts, or visit RCM, ag services.com, get the complete market analysis and strategies you need to succeed.

Jeff Eizenberg 12:28

Viv, you had mentioned in our early conversation that we’re ultimately going to that we need to work to maintain our quality so that Mexico can consistently buy from us. Can you shed some light? Where are we in the quality discussion specifically related to wheat, North Dakota, South

David Munoz 12:44

Dakota region, yeah, when it comes to wheat. So the good thing is, Mexico is a consistent buyer of all classes of wheat when it comes to soft with winter, for instance, or HR, W, it’s all grown in the south the problem with that is that you have Russia, which has become a major, major grower of wheat in the world, and exporter to the point where it makes it cheaper to substitute HR w. So the HR W area is in trouble. But then you get with a high protein wheat, which is grown hrs, North Dakota, for instance, and Canada. That’s, that’s, that’s a wheat, prime wheat around the world that has no other substitute. That’s the good news. But the bad news is, or the other news, in a way, is that you’re competing against Canadians. What we’ve seen, I think, in the past few years, is that Canada has invested a lot of time and effort and money on on on its seed technology, and getting very close to the to the flower millers, just in general, what do they need? What milling characteristics? Characteristics are they looking for and trying to plant those seeds that feed their needs? So between that and also the weather, which we’ve had bit of an erratic weather here past couple of years in in the northern plains, that has made that the quality between both weeds, it’s they’re just not quite the same, or at least that’s what the feedback we’re getting from some of the farm bills down there. We’ve also heard that from some European based customers, because our company also seeps by vessel through Duluth to the European market, primarily Italy. So we’re getting more of this feedback that they feel that the quality is just not exactly the same with Canada. And obviously, if this keeps, if this keeps going into the future, probably what you’ll see is that then they’ll they won’t be as willing to pay the same amount of money for for for either or variety. And that’s where there’s a risk that you can, you can the farmer might see that reflected on on the bits. So something to keep an eye on.

Ben Hetzel 14:38

David, would you say that the US mill, because of the supply being so close, doesn’t have to deal with it the same way that the Mexico market does, in the sense that it just is reflected in price all the time. They want a specific quality or specific baking characteristics, they know roughly where to go find. That I know years ago, we used to run a program that we had some IP wheat. It was a very, very high quality in terms of baking and milling, and so we had growers that would grow that specific variety, and we would ship it in dedicated freight to those mills that needed that product. And the real world example. And I like to share this with kids that come through the facility on field trips. When you’re making a hot dog bun, it’s a lot different than when you’re making a hamburger bun or a loaf of bread. When you’re at a ballpark, you want that hot dog bun to hinge, and to get that hinge effect, you have to have really strong baking characteristics in that that dough. And so if you’re just making a loaf of bread or hamburger buns, it can be split and cut, and there’s no issue, but a hot dog bun has to be a little bit higher grade so that you can get it to flex. Do you think there’s that’s part of the issue, the US doesn’t have to deal with that same quality concern on a direct level versus Mexico, and that’s why our farmers are growing these varieties, particularly focused on yield, maybe not quality.

David Munoz 16:18

I would say there’s some of that. I would agree. I think the other aspect of it is that the US meal also brings some, some Canadian Wheat, for instance. So they also have, they have, I think, a better access to blend if needed. While the Mexican flour mills Also, due to space, it’s more constrained to try to bring two different varieties of the same wheat to then get what they need. So at some point, it’s just easier for them to buy one or the other. Now, I guess important to mention to to our listeners, that this year, the harvest we’re just is coming out of the ground looks much better. And I think it’s going to be very interesting we follow up here in six months or whatever, and see what the feedback we get from the end users. I expect them to say, well, at least that the spread between both both wheats is not as wide, which is what has happened almost for two years in a row, to the point where some of the millers, they’re like, I don’t want to take my chances. Just ship me Canadian if you can. Now, obviously you have other markets, like the Asian market, especially Taiwan, which they just buy really high quality wheat, but that’s what’s grown in Montana, and it costs more. There’s a premium for that. So the one thing now that you mentioned that segregation with some of the customers, they’ve asked for it like it’s possible. Now the problem, and I know a lot of the farmers are going to say, are they willing to pay for it? And that’s where it sometimes comes to not really, because it just costs more segregation, IP, the logistics, you just can do it at the same price. And that’s where the quality guy will tell you, that’s my dream. But then obviously the procurement and the purchasing department says, like, not really interesting.

Jeff Eizenberg 18:01

It’s a wild thing to think about, that the purchasing department is really in control, right? But, but in the reality, quality is something that has transpired over time to be the leading factor, particularly for higher end markets, higher end products. And just this week, I was passed an article because we we actually do some export ourselves out of the US into South America. And then in reverse, we have some customers in Mexico and in Dominican Republic that are buying corn out of South America. And the question when I actually went down to a facility, I was in facility in San Pedro, Dominican Republic, and I asked him, I believe I get you cheaper corn out of the United States. And his response was, I’m sorry, we don’t buy from the US corn. We only buy, yeah, from Santa rim and the I wanted to understand that more and literally, this week, we did the research. And it goes back to a 2008 2009 period when the local buyers were complaining about the quality of the US corn. It was too dusty. It was cracking. The myotoxins were out of control. They didn’t have the same color. The milling yield, to your point, wasn’t the same, and so they left the US market, Dominican Republic, and they have never come back, even though we can get them cheaper corn today. So if I think about that, then I asked the question you just mentioned, two years in a row of underperforming quality, is that a wake up call for the farmers and producers in the areas in the north that we’ve got to focus on quality and not just this quantity.

David Munoz 19:48

Yeah, I also, and it’s a good question. I mean, I’m not an agronomist, but I think it has to do with the seed technology, so something to be probably further invest. Get it. Why is this happening? I’m sure some of it has been weathered like I say. I’m sure the farmers, they do a great job planting the the seed, the seeds, and then doing whatever they they do best. But I feel that there’s something related to the tight connection between the farms, the millers, and what it’s needed to get that has seems to have been a little bit more put more emphasis on north of the border. I think in the US, I do see Association like the US wheat associates, or these organizations that help open the markets abroad, they do an excellent job of marketing us grains, or, in the case of soybeans, usig, or the US greens Council on the in the case of corn, they do an excellent job opening the markets. But there’s an element more on the wheat side that has to do with quality, right? It’s in a ways, corn, not necessarily, but corn is corn. There’s less, less differences between origins, but with, with, with wheat. Now wheat is created equal. And what we’re finding is that even between high protein wheats US and Canada, they’re not necessarily the same. So that’s something that definitely we want to we market heart of the of the wheat out of North Dakota. So we were very interesting that that doesn’t change right to the point where we have to almost sell at a discount to Canadians, just because of that, that aspect of the of the quality that we’re the feed that we’re getting,

Ben Hetzel 21:27

yeah, it’s it is a tough challenge for the wheat industry, because nitrogen fertilizer has such an impact on on that quality and the timing of getting it in there. And, you know, the agronomists obviously know a lot more about this particular topic, and work closely with our producers in this area, in the wheat growing region. But you know, as I think about what we’re talking about, and the price of nitrogen right now being so high relative to what the grains have done, and you touched on it, David, you said exactly what we see, you know, corn. You can raise corn East River in the I states, and then you can raise it out west here, and it’s still the same corn. It might be lighter test weight or or, you know, smaller kernel, whatever it is, but it’s still corn. And wheat is not that way. But you bring up a very good point that there are lots of different varieties of wheat out there, some that focus heavily on yield, some that focus heavily on characteristics, milling characteristics. So it’s just a good thing for our listeners, our growers in the region, to know that this does matter, and we’ve seen it. Two years ago, you and I traded some grain directly into Mexico, because our quality made sense to go there, versus where we traditionally trade to and and that particular year, we had a lot of grain grown for yield, and we had to get rid of it. So we were finding all kinds of homes for it, and that compounded the issue. We fertilized, we did everything we could, but it just out yielded and outperformed what, what it had available to it. And so we didn’t have that good, rich milling characteristics built into it that we needed.

David Munoz 23:13

Yeah, no, agree. And again, it’s, I think it’s a tough one, because the farmer needs to do what, whatever he can to so the operation works, and a lot of it, especially with prices, how low they are, one of the ways is to just out yield their way out of it. So I think it’s a it’s a tough one, and I understand, because we’ve had the conversation with growers in the past, and obviously the some of the feedback, they immediately say, Okay, well, but who’s going to pay for growing? Less yield and more with the protein or whatever other quality. So it’s a tough one. And then there’s an element of north of the border. Often they have a even on the fixed advantage, or they have a they have a competitive rails, just because how the system works in Canada, where there’s there’s the rates are capped by the government, so there’s certain amount of money that the rail railroad companies can make, and if they do, once they hit that, well, the rates have to be reduced so they don’t make more, more than, more money, than than the cap, which doesn’t happen in the US, right? It’s free market. And they’ll, they’ll raise them, or they’re lower them, if the market need, needs it like, like it’s happening recently with on the soybean cycle, there’s no there’s China side on the picture. So then the rates have just come down to incentivize. Yeah, it gets pretty

Ben Hetzel 24:29

complicated, the whole global trade. And we see even again, in the last week, some changes with India and Canada and some things going on there. The US had their round of that here, what, 10 days, two weeks ago, with India, as we increase tariffs due to them buying Russian oil. Now there’s some talk that India might hold some imports from Canada. So it’s going to be a challenge this marketing year with depressed prices, like you said, and then all these other issues. Is popping up between these nations?

David Munoz 25:03

Exactly. Yeah. And I think at a macro level, what we’ve seen is that as other countries have become more competitive. So in the case of we, we say Russia keeps growing at a cheaper, cheaper level, to the point where it can export into into Mexico cheaper than from Kansas or for the East Coast flour mills, it’s just cheaper to bring in vessels from from Europe or Russia than rail it across the Midwest, in the case of Soviets and corn is Brazil is now obviously a powerhouse, and it just feels that they can keep growing and growing and growing the area. So for the US is becoming harder and harder to compete. Obviously, that’s why at all levels of of government. They, they, I think they’ve understand that they, they need to create domestic demand as much as they can, and not rely on on the especially a single buyer, like in the case of soybeans, right at least for wheat is a bit more more diversified. It’s just a matter of competing. In the case of spring wheat, competing against Canada in this in this case,

Speaker 1 26:01

if you’re enjoying today’s show, check us out on Facebook. Just search RCM, ag services for market updates and tips. Find us on Facebook today.

Jeff Eizenberg 26:11

Shifting directions a little bit. We are talking here with David Munoz, with Bartlett grain, David, we’re shifting over to talk a bit on logistics. Right now. We’re hearing rumors about the Mississippi River going to be dropping eight feet. Are we going to get barges down the river? So what’s what’s going to happen with the export side of things? Are we going to have to shift over to rail, or is basis going to widen even further, because there’s going to be nowhere for our grain to go this fall? What are your thoughts on logistics?

David Munoz 26:39

I mean, so far, what we’re seeing is that there’s a very healthy book of business on the corn, on the wheat side. So for instance, corn, it’s, we’ll get a record export number. It’s been very competitive. It’s been even up until now. It’s competing against Brazil and Argentina into a lot of destinations. That window will close, and should have closed by now, but it hasn’t. There’s also one of the other big producers, which is Ukraine. They’ve, they’ve had, they didn’t have a very good crop last year. So there was an opportunity there. Now it will rebound. And the crops are seem to be rebounding in many areas of the world. So I think for next year, that’s where I think is going to get tough with a very large crop we’re getting. And then also export number on the estimates, that is really high and won’t be easy to to hit. On the soybean side, obviously it’s just bad. There’s no, no, no way around it. Without China, they’ve already covered October and probably part of November, with their needs out of Brazil. And then we know that the new crop, the Brazilian new crop, comes in in January, February. So the window is getting really, really narrow for the US to export. And spring wheat is relatively stable compared to last year. So that’s exports are going well. Mexico is taking quite a bit. Logistics are tight, but they’re not they could be worse if we had a Soviet program. But given that we don’t have a soybean program, that’s allowing, I think there’s capacity on the on the rail side, on the bar side, for the other grains. So I don’t foresee big issues at the moment, just because probably with like, like I said, we don’t have a soybean program, otherwise things probably they’ll be pretty tight. But by now,

Jeff Eizenberg 28:21

in terms of the buying from China, people also are hanging on to the fact that they’re going to buy our soybeans. And if I look at markets and the way that I track if we see both corn and beans trend higher because of our export program, and then a chance of China that would only probably drag wheat up with it, which could ultimately be good for all, all grains. But let’s, let’s be real. Do we think that China is coming?

David Munoz 28:47

In my opinion, I see, I mean, there might be some deal that gets done, but I think they’re, at least they’re getting ready not to. They haven’t bought a single bushel for, as we know, for this new crop, they have inventories in the country, which is something they do with all all the, all the grains that probably they don’t have to and then Brazil is coming up with a massive, massive harvest, probably for next year as well. Well, they had one this year, and now they’re, they’re about to plant their new crop, and they, I think it’s just a need. I mean, Brazil, by its own, feels that they can, they can, they can serve all China. And then obviously there’s some, some shuffling the US takes other markets. But it’s just not enough. There’s no one country that can substitute what what China buys. And at the end of the day, China consumption, just in general, it’s starting to decrease. Right as their, as their, their population is not growing that much anymore. It’s more more stable. So it just, I think that’s what we’re seeing here in the US, kind of the acreage, especially in the weed side of it’s just the charts are dramatic, right from 20 or 30 years ago. There’s just less, less needs to be planted, perhaps. And what it’s planted, they have to find uses, domestic and in other, in other ways. So no, in my opinion, I believe China is not gonna, it’s not gonna save us this time. But. Hope I’m wrong for the for the sake of the farmers well,

Ben Hetzel 30:04

and I think Jeff and David, one of the interesting little side notes that I’d like to add is, when you if you’re producing grain to market to the world, you need to target the places that are long term sustainable partners. You need to really build them up and and nurture those relationships, so to speak. And China has been on the decline, as you stated. But you look at India and what’s going on population there Mexico, which we have a we have good trade relations today, but India is a huge, huge player. And unfortunately, we don’t, we don’t really have a good relationship today in there. And so it would be interesting to see where this all goes. But it would be, it would be exciting to see some of these markets open up for the US, and hopefully we can get these trade deals, these this trade war, kind of put to the side a little bit and help these commodity prices come back for the producer, because that’s a challenging situation we’re in right now at the farm level. So but I one thing I want to say, Jeff, too, is when we talked about our mission on this show, it was to provide farmers, ranchers and users, or the Ag professionals, the tools and resources to navigate the market and maximize margin. And I think for today, this episode with David, it, it did all that. And I I’m super excited to bring this to the listeners and have David on here. I hope we can have him again sometime because of his insights and knowledge in the global market. So really appreciate that.

Jeff Eizenberg 31:42

Yeah, that’s right. And David, it’s been, it’s been amazing having you on here today, and the excitement that the listeners should hear that Ben is working with somebody like yourself to understand all these challenges. You know, where Ben sits at the Scranton equity Co Op, there’s an opportunity for him and his team to listen to you which you are working with the buyers. And so the ultimate thing is know your customer and understand who’s on your team. Like Ben just said, working again with the with the co ops to find out what is coming next. What the end users need and want is more important now than ever in this global market, we’re not just selling to your neighbor, we’re selling to the world. And we should, all the producers on here should, should be very proud of that. And also need to stay stay educated. Can reach out to Ben at the Co Op, pop over and see him in Scranton. Over at Scranton equity exchange. Give him a call. Check out our website, RCM, Max services.com, and David, if somebody wanted to get and get a hold of Bartlett, where’s the where’s the website for them to go to?

David Munoz 32:49

Yeah, probably in their browser. They can just put on bartlett.com they’ll find it. Our series global like website was just recently integrated into them. So if you go to the Bartlett website, they’ll see now the locations that are also the ones that the series global ag River Land ag business uses currently, absolutely. Thank you very much for the invitation. Happy to be here and

Corn continued to move higher off last month’s lows following the September USDA Report. Most of the numbers came in along estimates but they increased planted acreage 1.4 million acres. This brings the US corn crop to 98.7 million acres, a new record. With about 90 million acres expected to be harvested, we will harvest 7 million more acres this year than in 2024, which equates to about 2 billion bushels larger crop than last year. Despite the added acreage corn bounced post report as weather issues, a dry finish, and disease pressure have caused speculation on the real size of this crop. As harvest gets rolling we will learn more about this crop.

The USDA Report did not have any surprises for beans as most numbers were close to estimates, but the report could be viewed as slightly bearish. To get beans moving higher, China needs to show up as a buyer and trade talks with China need to make progress. China and the US are reportedly close to a deal over Tik Tok which can hopefully build some momentum for progress between the two countries. The size of the soybean crop, like corn, has been hurt by lack of rains down the home stretch but with the solid start the end result is still in question as harvest rolls.

Equity markets continue to make new highs with the Federal Reserve expected to start cuts this month. With the downward revision of 911,000 jobs from March ‘24 to March ’25 the labor market weakness gives the Fed some ammunition to lower rates with unemployment being one of their mandates.

Secretary Rollins is in the process of looking into payments to farmers for this year with the low prices.

The wheat numbers were actually a bit supportive but lower world cash prices (Black Sea mainly) continue to plague prices. Wheat will remain an anchor for any potential corn rally as more wheat will be swapped in for corn in feed. Prices are back testing the 5 ½ year Covid lows.

Drought Monitor

Here is the most recent drought monitor as harvest begins.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn has rallied off the post USDA report lows with a large up day on Friday to end the week. Pro Farmer Tour wrapped up their crop tour and has an average US corn yield of 182.7 bu/ac which would still be a record on top of the added acreage, but well below the 188.8 the USDA came out with. The two sides from the USDA’s report is that they likely won’t come out with a higher yield again with some small weather issues developing, but if they keep it high and make another big correction in January saying the crop wasn’t as big as they thought it could cost the farm community billions. The weather has cooled off for much of the country but the lack of rain for extended periods may be a problem in the home stretch.

The Pro Farmer Tour found a bean crop more along the lines of what the USDA had coming in with a 53 bu/ac estimate vs the USDA’s 53.6 bu/ac. Beans biggest problem right now has been lack of rain for pod fill but a few well timed rains down the stretch could lead to a massive crop. China really needs to show up as a buyer for beans to leg higher but they can get all they want from South America right now even though they are paying a premium to get them vs US beans. The funds have a neutral position on the market as they wait for news that could send the market any direction other outside of the $10 – $10.50 range it has been trading in the majority of the last 6 months. China still remains a cloud over the market with the Trump administration needing to get Ag purchase commitments whenever they work out a trade deal in the coming months.

Equity markets continue to claw higher amidst pullbacks as earnings wrap up and AI and tech still drive the market direction. The Fed is expected to cut rates in September while the Trump administration’s attack on the Fed’s independence continues with Lisa Cook in its crosshairs currently.

ADM plans to close a soy protein plant in Bushnell, IL.

Brazil’s investigation into the Soy Moratorium (curbs Amazon deforestation) could threaten sustainable soy sourcing, with potential ripple effects in the global supply chain.

Wheat has been relatively flat the last couple weeks.

Cotton continues to trade sideways waiting on demand to pick up.

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

188.8 bu/acre… Hard to find a silver lining in the report for corn as the USDA ripped the band-aid off from the start instead of slow playing it. The average trade guess was 184-185 bu/ac which led to a big selloff seeing new contract lows. On top of the big yield number the USDA took the FSA planted acreage data and added 3 million acres in planted corn. The extra yield and acres could add nearly an extra 1 billion bushels of corn to the US and world ending stocks. The report did nothing to help the direction corn has been trading.

The bean yield was also above pre-report estimates, coming in at 53.6 bu/acre. Prices were higher though following the 3 million acre planted acreage cut and total production cut by 90 million bushels. The market was caught off guard by the 3 million acre shift as evidenced in the opposite price reaction to the report numbers. The bean rally will give farmers a chance to catch up on sales but it will also motivate more acres to be planted in South America on stronger prices.

Equity markets continued to perform well as AI and tech companies are still the major movers. Nvidia and Microsoft are now a combined 15+% of the S&P 500 index, causing some to worry about concentration, but luckily they are performing well so right now a rising tide raises all boats (money in S&P ETFs).

Wheat was in line with re-report estimates and had no major surprises. The weakness in corn will continue to weigh on wheat however.

Cotton saw a boost post report after the USDA lowered planted and harvested acres. Production was trimmed by 1.39 million bales to 13.21 million bales.

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Corn prices have drifted lower since Mid-July with no major weather issues and no major trade deal news. The corn crop ratings remain strong with about 73% of the US crop rated good/excellent and slking and dough formation ahead of average. Exports have slowed and funds have kept their short position about even last week. With the recent heat dissipating giving way to a cooler week, this crop has not been made yet but has not faced any prolonged growth challenges which continues to fuel the estimates into the 184-185 bu/acre. While this will be an impressive crop, from talking to growers across the country there are trouble spots due to disease and timing of rains which would help us get back to the low 180s which would give the market a bump. The market has been limping lower and will likely continue until something in the news cycle changes.

Soybeans have struggled lately as there has not been any news to boost the market. Exports this week were better but until China shows up as a buyer the demand for US beans is struggling on the global market. South America had a strong crop giving China more supply to buy so China may not show up until they have to unless prices fall enough to make them step in. Crop ratings remain strong, but the next month of rain will be important for pod filling and to get the crop across the finish line.

Equity markets continued to reach new highs before a sizeable pullback to end last week with the news of Trump firing the head of the BLS. AI and tech names continue to lead the way. Magnificent 7 stocks have had mixed reactions to earnings but nobody is sounding the alarm yet about tariffs as guidance remains steady.

Wheat has limped lower with corn and beans but saw good exports this week amid Ukraine’s sluggish exports.

The USD has strengthened in the last week but is still well below its year high. Historically this would have been supportive of agriculture exports but there are other factors in play this year.

The August WASDE report should provide some clarity and at least provide some new news for the market to digest and trade on for a bit.

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Last week was rough for commodities as corn dropped to make new contract lows in Dec ’25. The charts do not look good for corn and there is no good news to help either. There are no major weather concerns and South America is producing another record crop allowing for ample ending stocks in the world. The USDA June 30th Planted Acreage Report stated that corn has 95.203 million planted acres. This number is neutral to bearish as the market was expecting a slightly higher number but anything 95+ with the weather to this point in the year looks for a huge crop. The bears have the momentum right now but there are some trouble areas and a long summer ahead to bring the bulls some help.

Soybeans gave back the recent gains as well last week before the report on June 30th. Beans will likely continue to trade in the range they have been until we receive news to direct the market either on the trade agreement side or weather. The Planted Acres report had 83.38 million acres, slightly below expectations. The tax bill going through congress right now may give beans some help by getting rid of a 45z tax credit loophole but until this thing passes everything is on the table to get cut from it. Weather is good for the next 2 weeks so the market needs positive news from a US and China trade deal to give it a boost.

Markets set new highs after another V shape recovery following the liberation day tariff dip. Several tech stocks have led the way outside of the Magnificent 7 as AI continues to dominate headlines with spending continuing and companies talking about how it can help improve their margins.

Cotton acres came in higher than expected at 10.12 million acres. Cotton has been stuck below 70 cents/lb for a while and while the acreage number came in higher than expected we know there are issues with the crop and a lot of abandonment.

Wheat, like corn and beans, yawned at the report as the numbers were close to the average estimate with no major changes. After a mid June rally, the weakness to end the month was disappointing dropping 50 cents from the highs.

The weakness in the USD over the past few months will be something to keep an eye on as the year continues with it trading at levels we have not seen since early 2022.

Tensions in the Middle East continue despite a drawdown in aggression.

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

The March 31 Stocks and Acreage Report did not provide any fireworks as there were no major surprises in the report with the USDA saying there will be 95.326 million acres planted. While this is a large acreage number the trade and talk the last couple weeks was about the likelihood of the USDA coming out with a 95 number. While the report could have been worse, stocks coming in exactly in line with the estimate did not pile on with bad news. As we head toward planting, weather, South America and tariff wars will be the main movers now.

Soybeans came in at 83.495 million acres as their lack of profitability at current prices is making farmers switch some acres to corn. As you can see from the chart below there have not been much help for beans but if this acreage number is close to what we see, it is hard to think they would dip much below $10. The post report action was disappointing as beans continued lower.

Wheat had bullish news from the report as acreage came in 1.125 million below estimates. Wheat has some bullish world news for price with emergence concerns in the Black Sea and US Plains, despite recent price action. News out of the Black Sea and any issues with the US crop will be market movers for now.

The equity markets continue their volatile swings while President Trump’s “day of liberation” approaches on April 2 when tariffs are supposed to be going in place. Volatility will be the name of the game as many unknowns remain in the trade wars.

Cotton acres came in at 9.867 million. This is 1.315 million acres less than last year. Cotton needs to see demand pick up to get back and stay over 70 cents/lb.

Drought Monitor

As planting approaches the drought monitor begins to become important again as subsoil moisture always seems to be a problem somewhere.

PRICES

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

RCM Ag Services is a registered DBA of Reliance Capital Markets II LLC. Trading futures, options on futures, and retail off-exchange foreign currency transactions are complex and involve substantial risk of loss and are not suitable for all investors. Loss-limiting strategies such as stop loss orders may not be effective because market conditions or technological issues may make it impossible to execute such orders. Likewise, strategies using combinations of options and/or futures positions such as “spread” or “straddle” trades may be just as risky as simple long and short positions. There are no guarantees of profit. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge and financial resources. You may lose all or more than your initial investment. You should not rely on any of the information herein as a substitute for the exercise of your own skill and judgment in making such a decision on the appropriateness of such investments. Opinions, market data and recommendations are subject to change without notice. Reliance Capital Markets II LLC shall not be held responsible for any actions taken based on this website or attached links. Parties acting on this electronic communication are responsible for their own actions. Past performance is not necessarily indicative of future results.