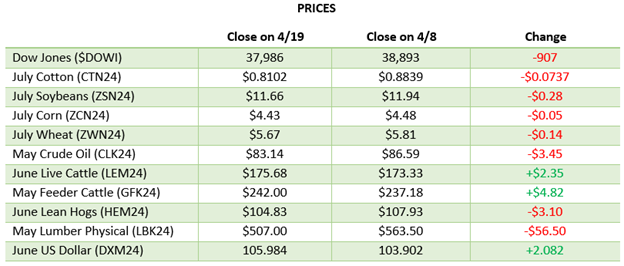

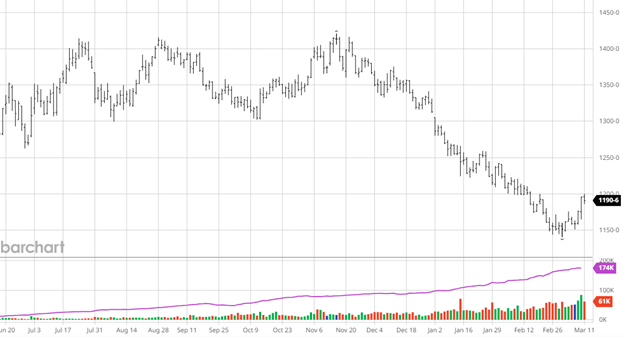

Corn has seen a strong rally over the last couple of weeks as planting is slightly delayed in parts of the US and funds seem to have changed their tone a bit. Last week’s USDA Report did not have any earth-shattering news but did provide some good news for the markets. US corn stocks were lower than estimates heading into the report along with world stocks for both 23/24 and 24/25. The production outlook for this year, 181 bu/ac, continues to show how the advances in agronomic practices and seed genetics continue to grow. All of these carryout and stocks numbers are based on those production estimates so if we begin to see weather issues or problems at the end of planting, we could continue to see revisions to the downside, and vice versa with great weather and conditions.

Beans had a rough week after a strong start to May. The USDA Report leaned bearish as the South American production continues to expand for the upcoming year. The USDA is slowly trimming Brazil’s bean crop but is still above CONAB’s estimates by a bout 300 million bushels. The recent flooding in southern Brazil will force their hand to lower their expectations but the CONAB estimates on losses will be closely watched. Another promising development in the report was the expectation of record imports and usage in China. While much of this is expected to be met by Brazil and issues with their production will still need to be met.

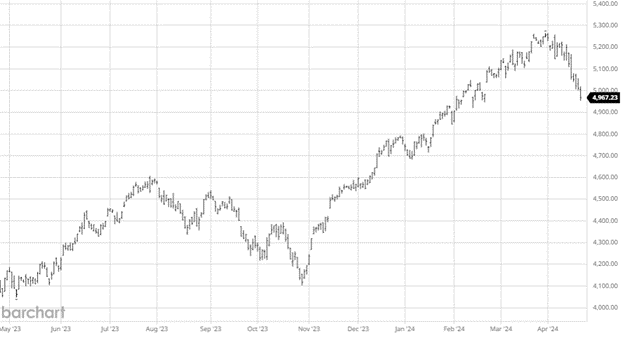

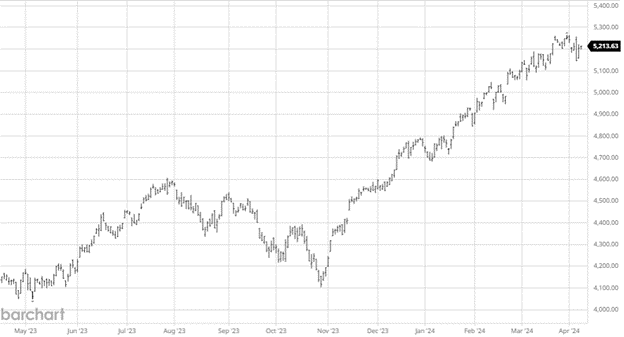

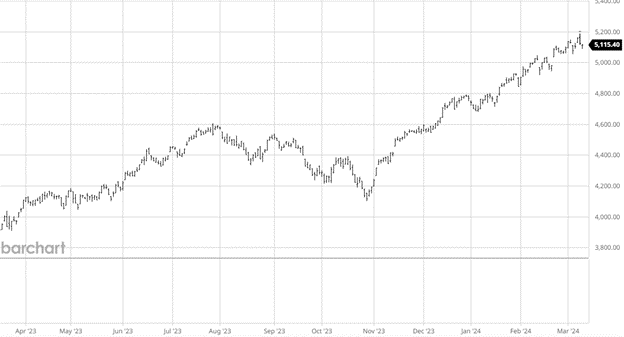

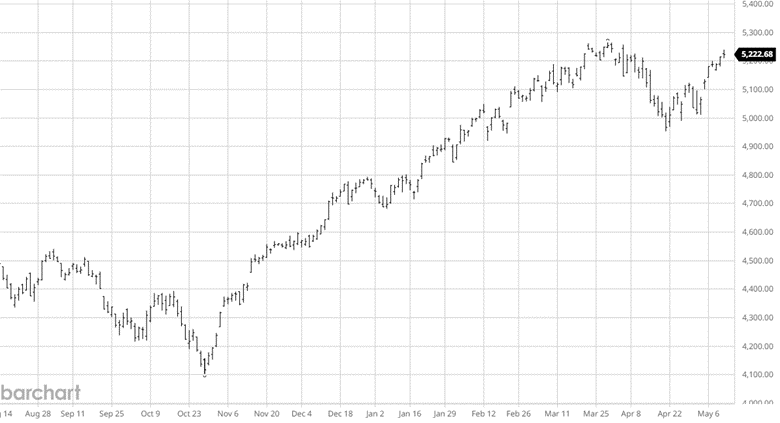

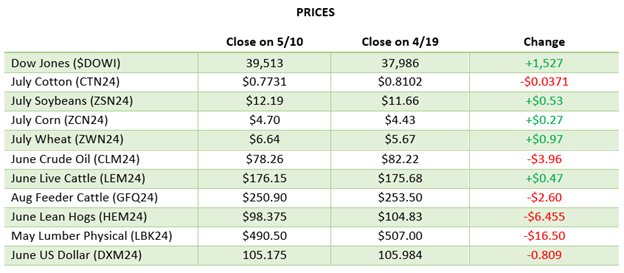

Equity Markets

The equity markets have rebounded over the last couple weeks with earnings season going on. The feeling on Fed rate cuts keeps pushing them back with one not expected until the fall and at least one fed chair thinking we may not get one this year as inflation remains sticky. Rates will remain data dependent but the feeling of higher for longer continues to seem more likely.

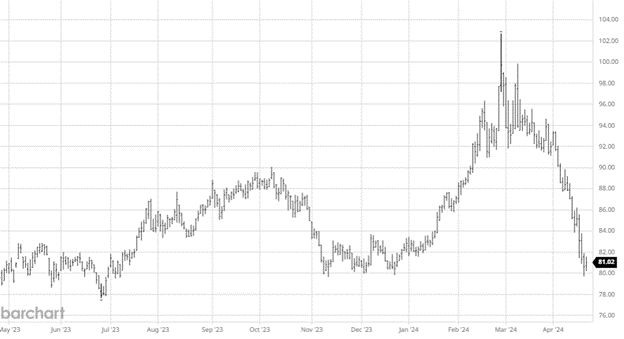

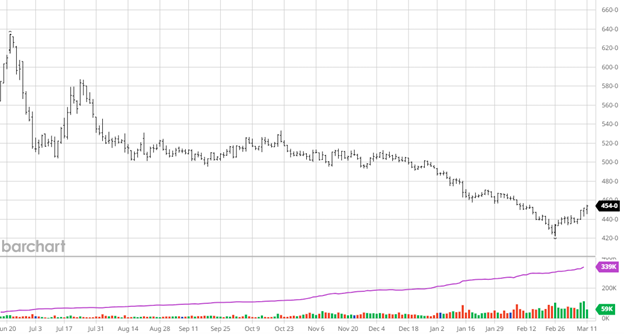

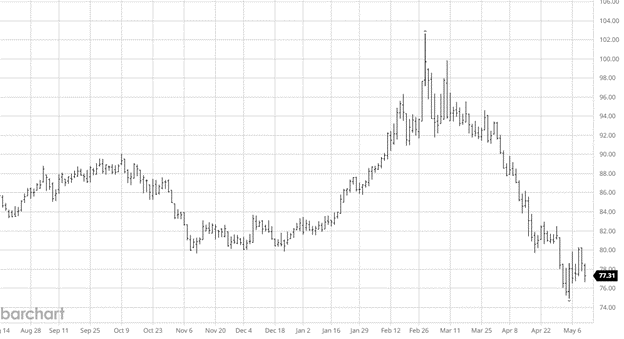

Cotton

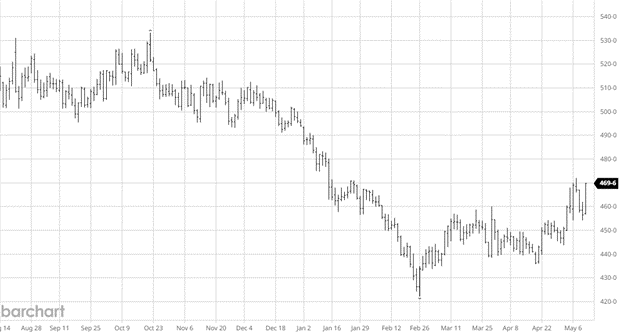

- Cotton has fallen well off the February and March highs as the lack of demand in the global market mixed with funds exiting their long positions has beaten down the market.

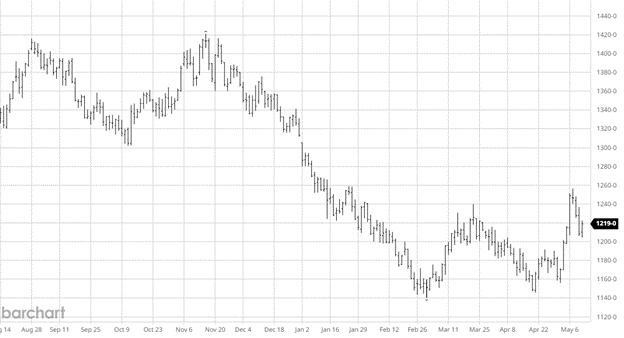

Wheat

- Wheat’s recent rallies are welcome after struggling to find much positive movement in the market to start the year. Frost damage to Russia’s wheat crop and a dry pattern in the Black Sea has been the recent mover as the USDA Report had some mixed numbers. Smaller than expected US stocks, 24/25 world stocks and total production with higher than expected world wheat stocks for 23/24.

Other News

- Conflict continues between Israel and Palestine as a ceasefire has been negotiated on many sides, but nothing has been agreed to yet.

- Major flooding across southern Brazil has killed thousands of livestock and will have an impact on their crop but the extent of which is not known yet

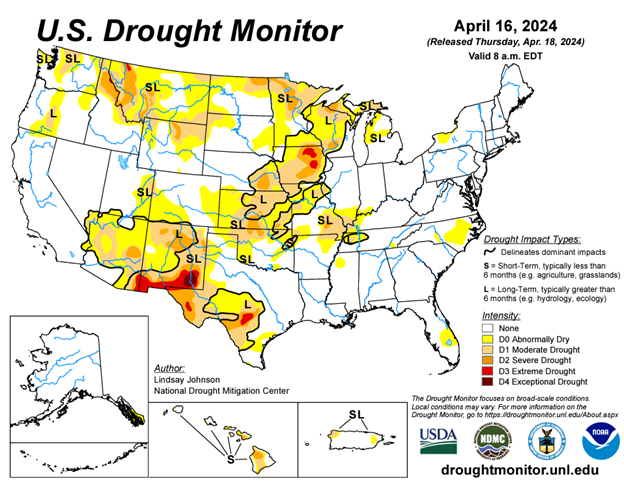

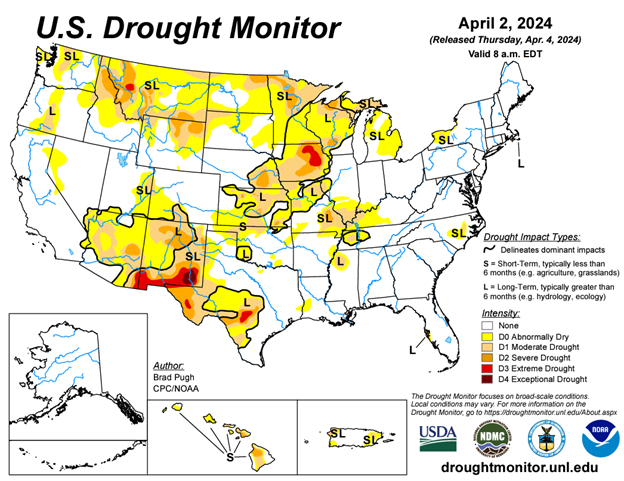

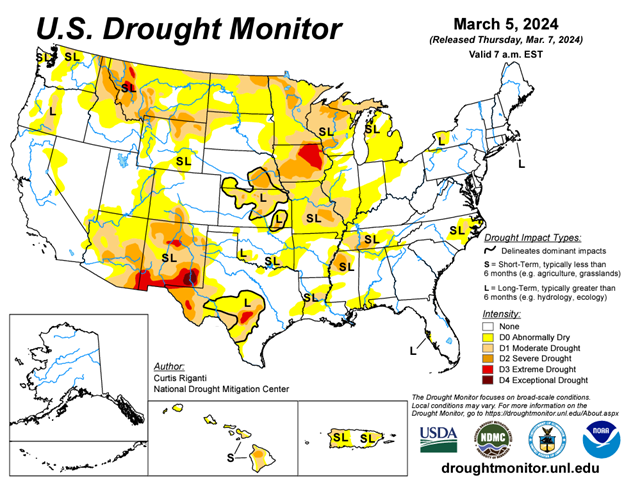

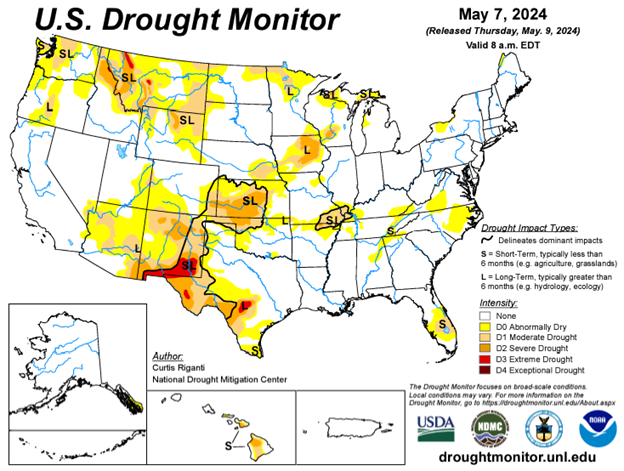

Drought Monitor

Here is the current drought monitor as we head toward planting with subsoil moisture a focus.

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.