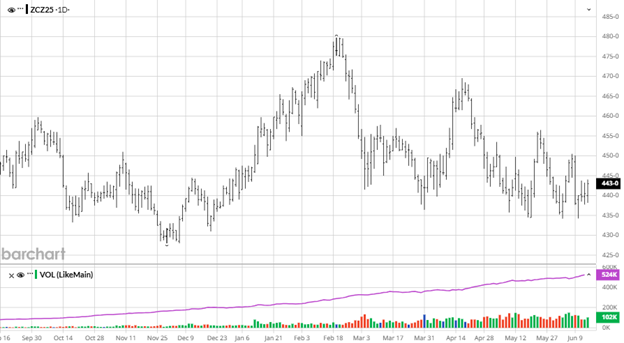

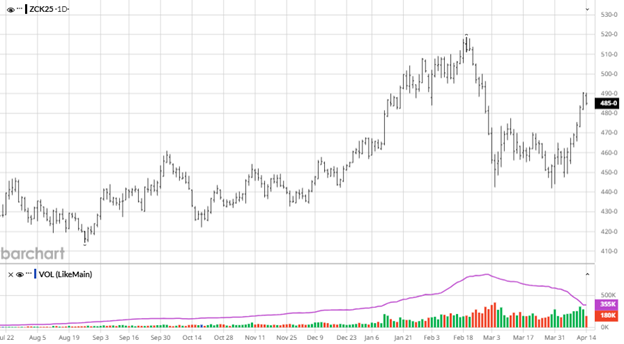

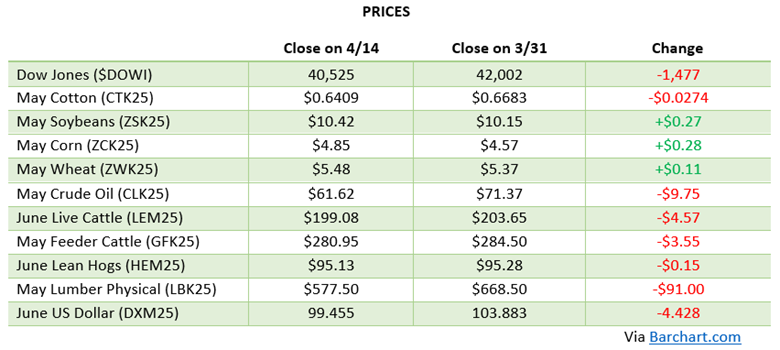

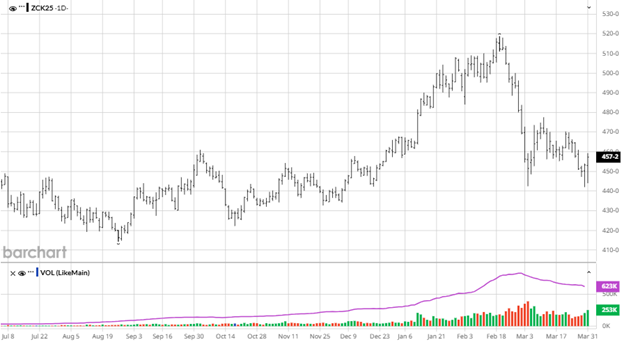

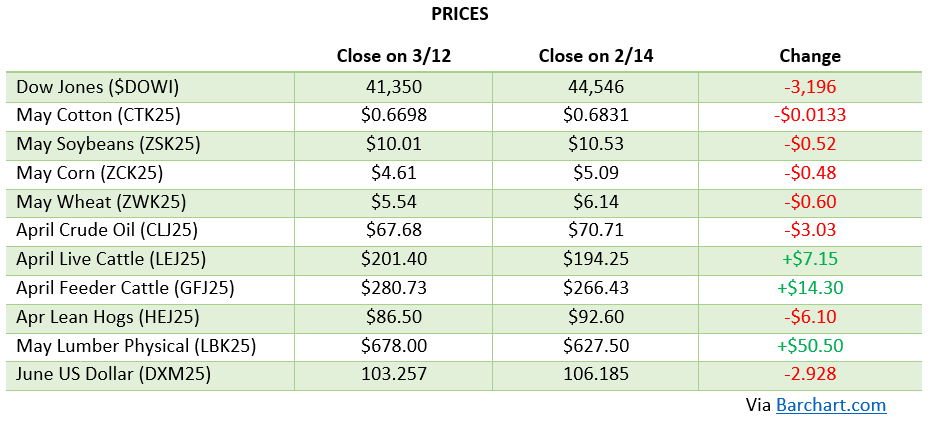

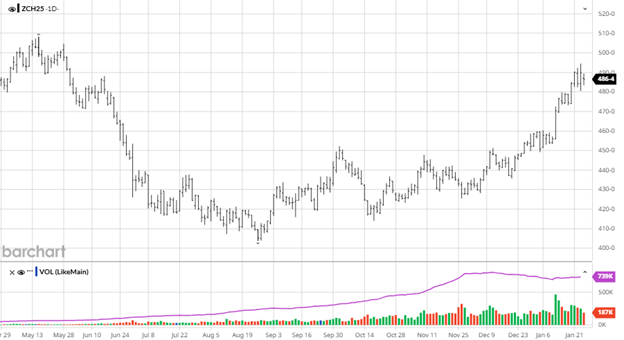

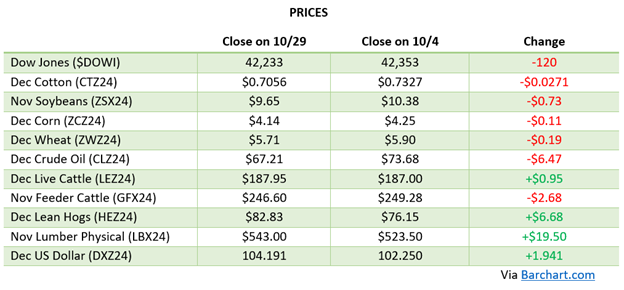

Last week was rough for commodities as corn dropped to make new contract lows in Dec ’25. The charts do not look good for corn and there is no good news to help either. There are no major weather concerns and South America is producing another record crop allowing for ample ending stocks in the world. The USDA June 30th Planted Acreage Report stated that corn has 95.203 million planted acres. This number is neutral to bearish as the market was expecting a slightly higher number but anything 95+ with the weather to this point in the year looks for a huge crop. The bears have the momentum right now but there are some trouble areas and a long summer ahead to bring the bulls some help.

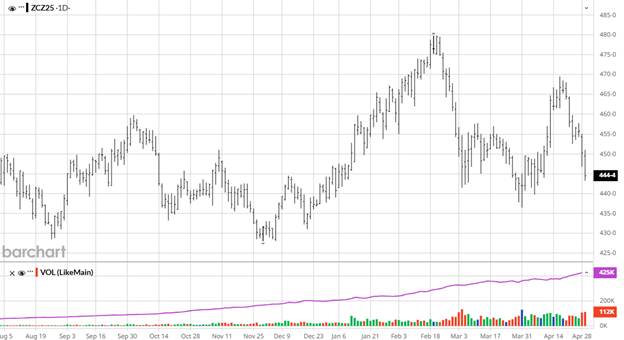

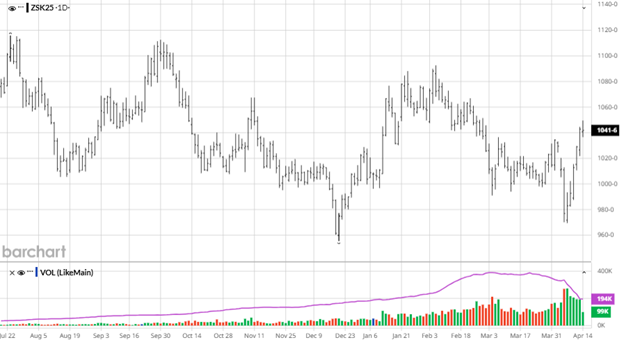

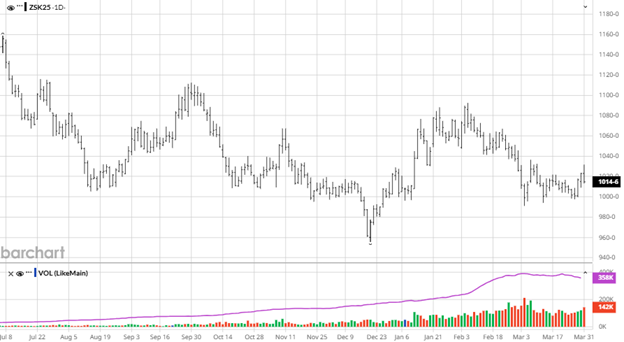

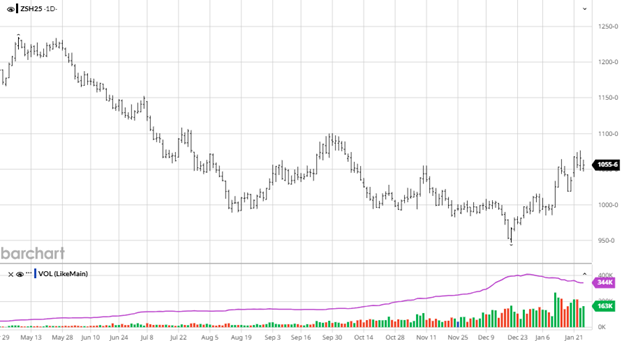

Soybeans gave back the recent gains as well last week before the report on June 30th. Beans will likely continue to trade in the range they have been until we receive news to direct the market either on the trade agreement side or weather. The Planted Acres report had 83.38 million acres, slightly below expectations. The tax bill going through congress right now may give beans some help by getting rid of a 45z tax credit loophole but until this thing passes everything is on the table to get cut from it. Weather is good for the next 2 weeks so the market needs positive news from a US and China trade deal to give it a boost.

Soybeans gave back the recent gains as well last week before the report on June 30th. Beans will likely continue to trade in the range they have been until we receive news to direct the market either on the trade agreement side or weather. The Planted Acres report had 83.38 million acres, slightly below expectations. The tax bill going through congress right now may give beans some help by getting rid of a 45z tax credit loophole but until this thing passes everything is on the table to get cut from it. Weather is good for the next 2 weeks so the market needs positive news from a US and China trade deal to give it a boost.

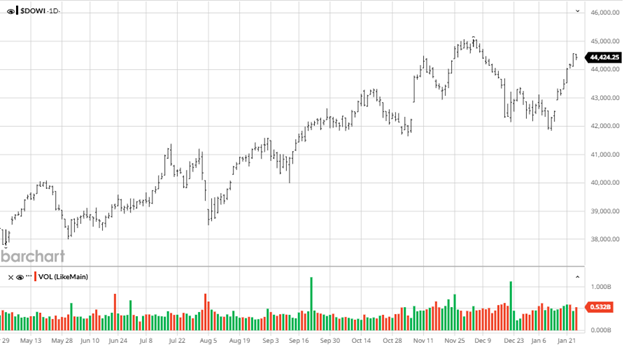

Equity Markets

Markets set new highs after another V shape recovery following the liberation day tariff dip. Several tech stocks have led the way outside of the Magnificent 7 as AI continues to dominate headlines with spending continuing and companies talking about how it can help improve their margins.

Other News

- Cotton acres came in higher than expected at 10.12 million acres. Cotton has been stuck below 70 cents/lb for a while and while the acreage number came in higher than expected we know there are issues with the crop and a lot of abandonment.

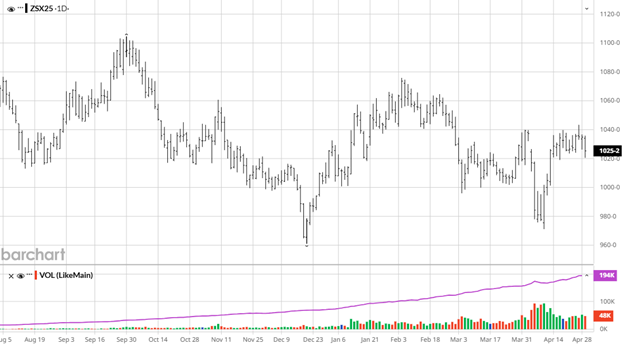

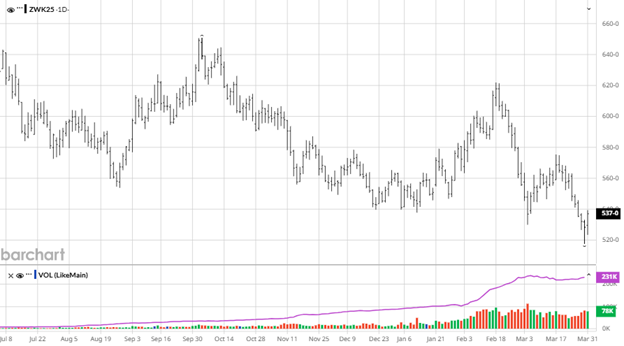

- Wheat, like corn and beans, yawned at the report as the numbers were close to the average estimate with no major changes. After a mid June rally, the weakness to end the month was disappointing dropping 50 cents from the highs.

- The weakness in the USD over the past few months will be something to keep an eye on as the year continues with it trading at levels we have not seen since early 2022.

- Tensions in the Middle East continue despite a drawdown in aggression.

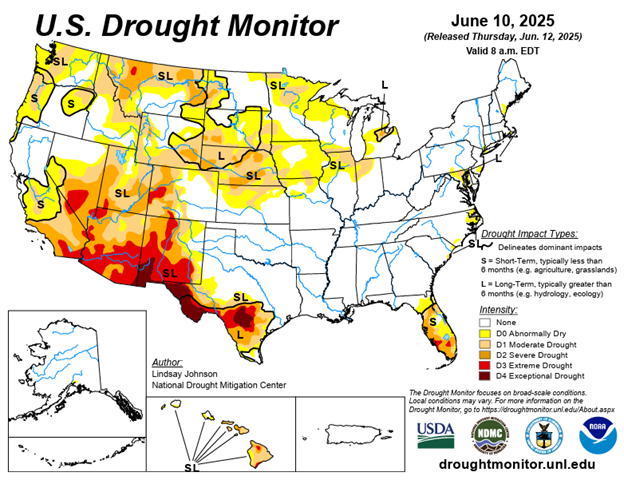

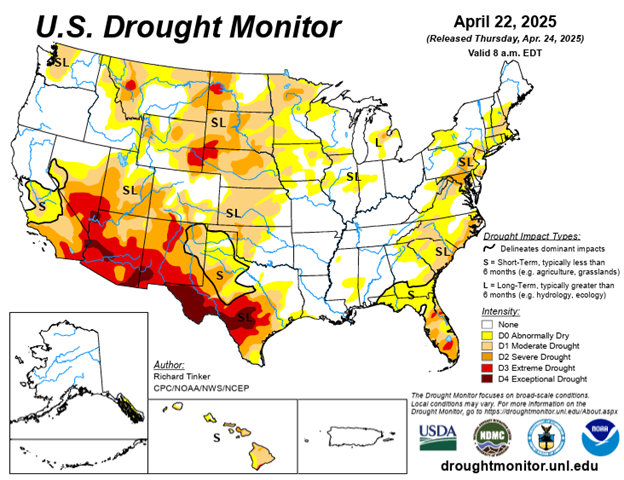

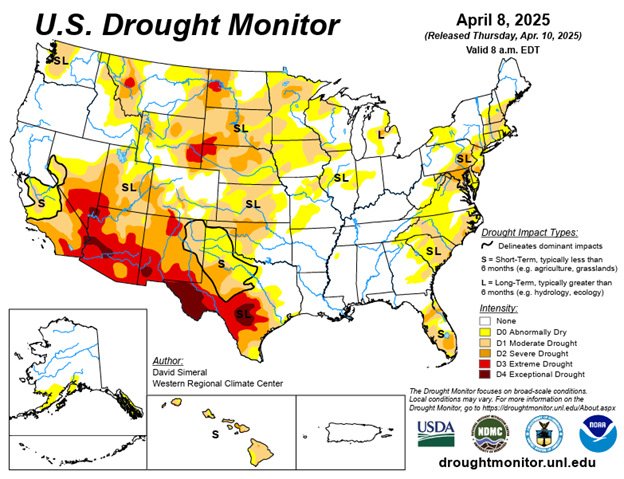

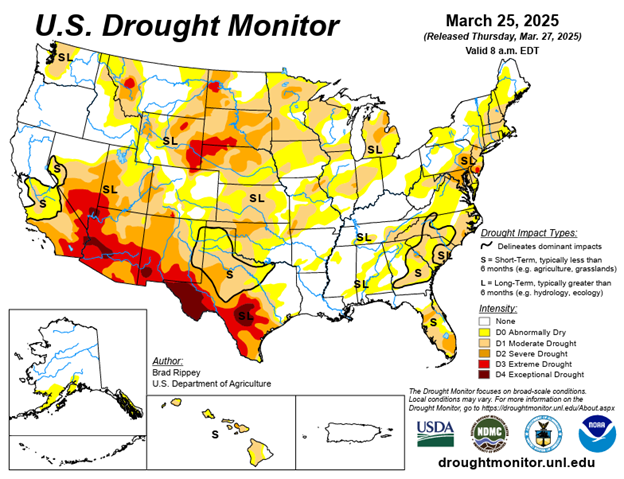

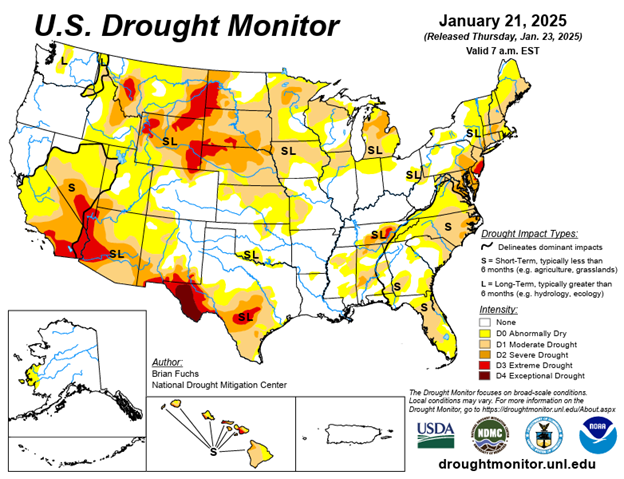

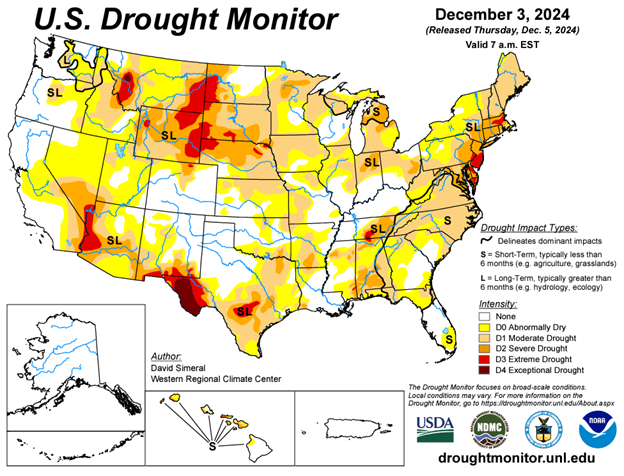

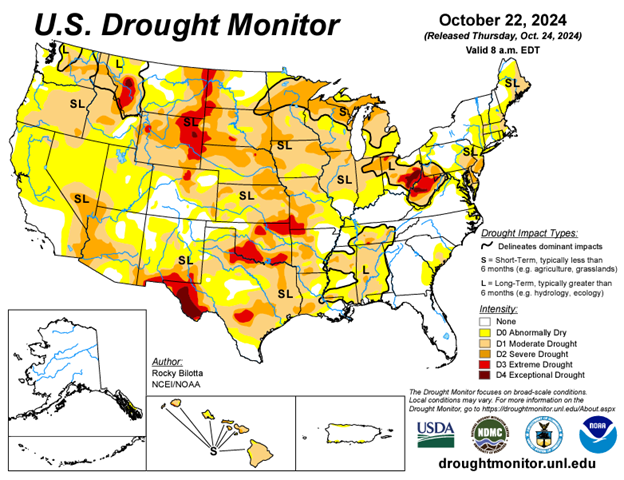

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.