The Lumber Market:

Just when we thought we had seen it all this year, the US bombs Iran. With that news we see the TASE at all-time highs today. If nothing else, it is weighing on the psyche of the investor. That in turn makes the big decision of home buying more difficult. And that will keep demand and building muted. So where is the risk in the next 3 months? The biggest is risk is to the producers. The Canadians will see higher costs that can’t be passed along. The US producers, especially down south, will see prices fall below breakeven. Looking at the other risk, it is on those holding jobs short. The producer side could just shut it down causing a major temporary spike in prices. The buyer could get stuck in the middle of it. It is a mess. Now as far as the middle trader goes, volatility carries a premium in markets. They should benefit.

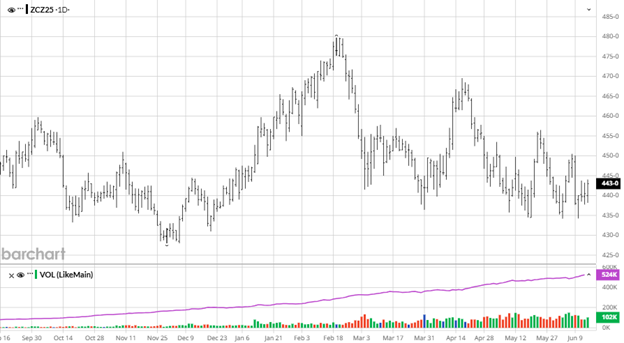

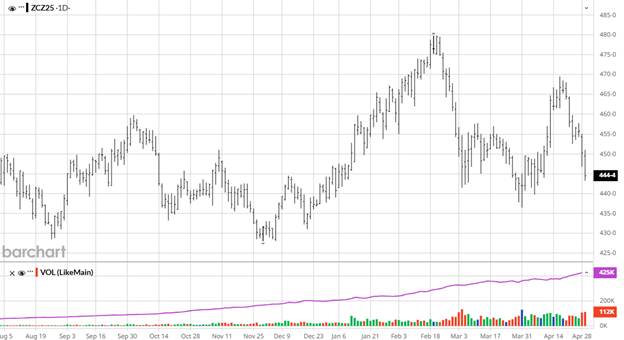

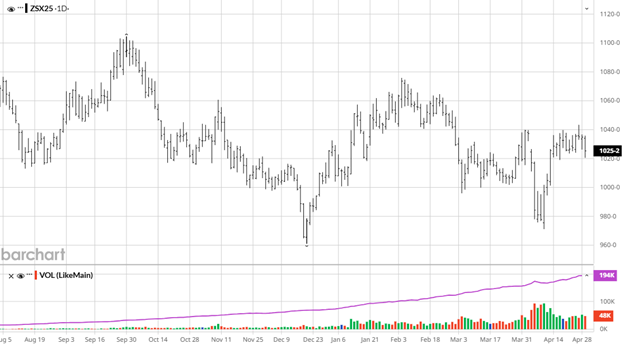

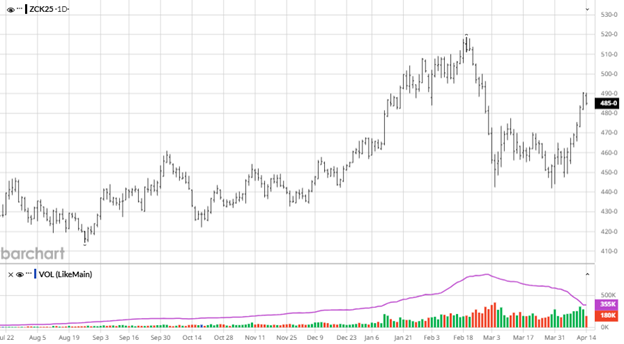

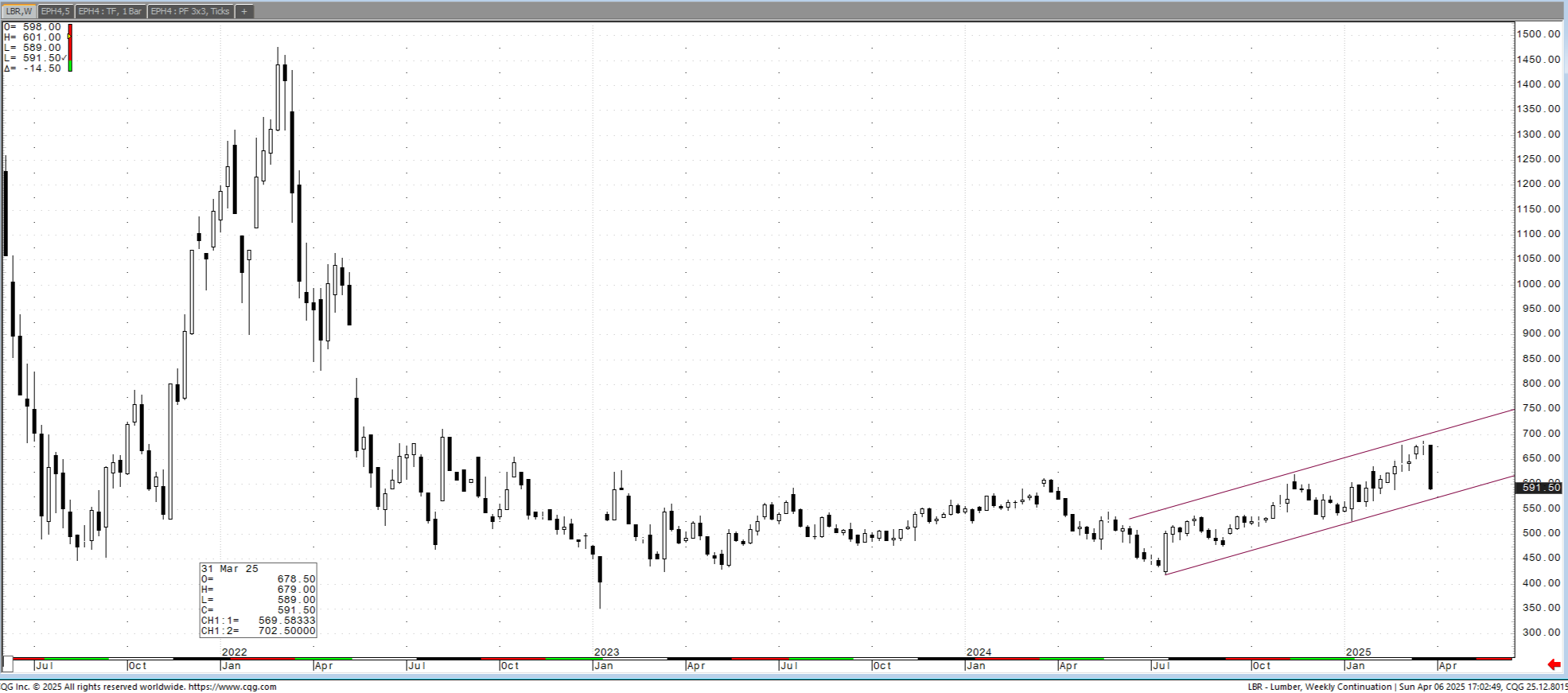

Last week July futures were off $10.50 on a trade dominated by the roll. The market makeup has the industry getting short eating up the funds exiting. The only other feature is that the yahoo’s are getting longer. The debate is which month is better to be speculatively long. The closer July gets to no limits the less it should be traded. Time holds the answer. Once the funds are done with the July buy side there won’t be much support.

Technical:

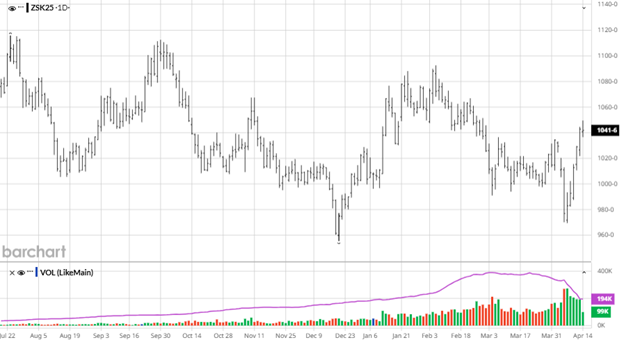

Technically the July is still in the neutral zone while the September is rolling over. That is the opposite of what most expect. The tech read is very fragile so not much of a run up would reverse it. They whole picture holds little opportunity. Most are relying on the pending price increases forced on the Canadians.

$100 crude is not helpful.

Daily Bulletin:

Southern Yellow Pine:

The Commitment of Traders:

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636