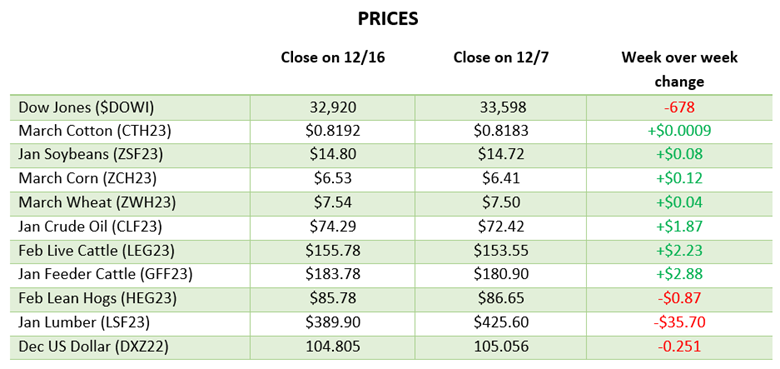

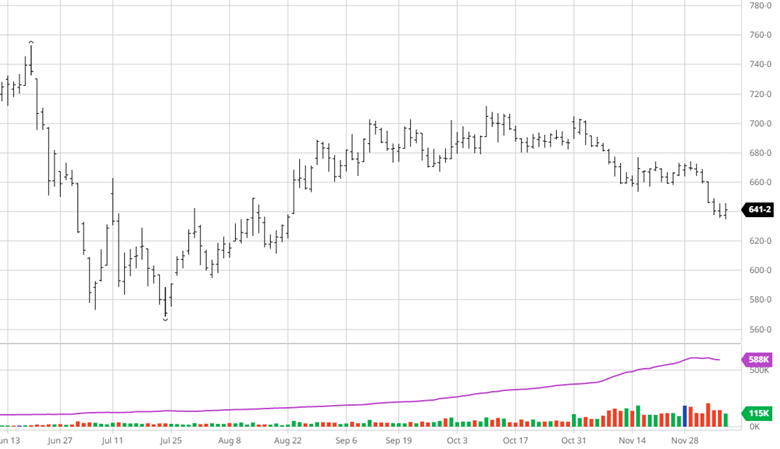

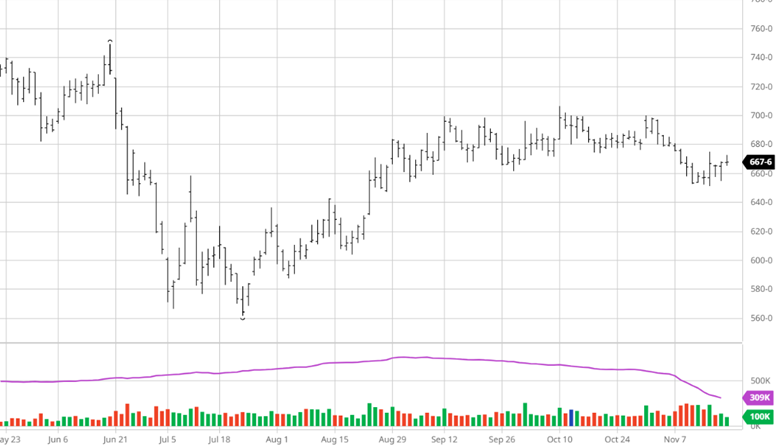

Corn made gains over the last two weeks with the continued escalation of bombing in Ukraine and more dry weather in Argentina. Exports remain uninspiring as the year comes to a close. China announced they will reduce some travel restrictions while covid infections continue to cause problems and continued lockdowns. Brazil’s expected record crops could offset some of Argentina’s losses but what extent will be determined in the next 2 months. The news has been slower as we get to the end of the year but the continuation and escalation of the war along with the other factors can continue.

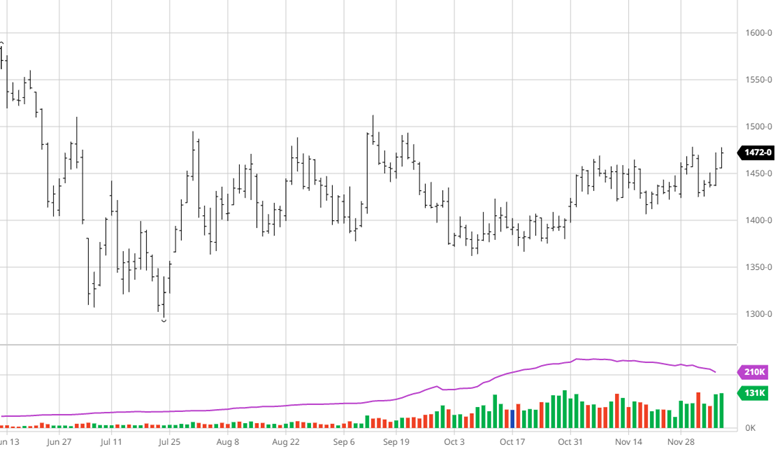

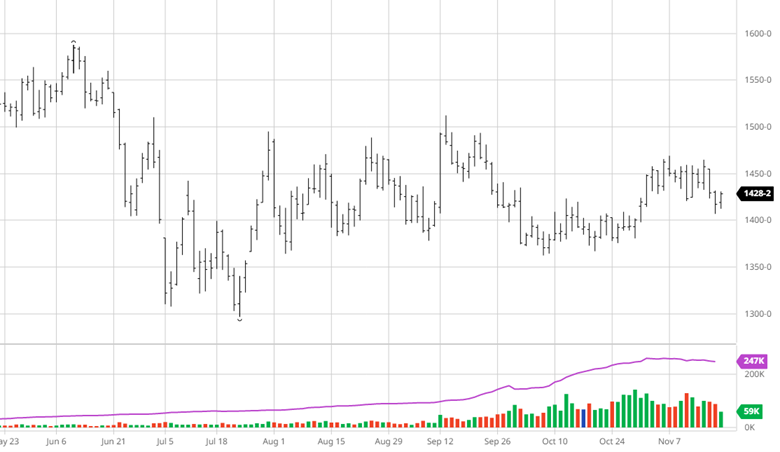

Soybeans participated in the market rally over the last couple weeks making solid gains back over $15. The Argentinian crop is rated as just 10% good to excellent, down from 12% the previous week. Brazil’s weather has been quite favorable to their bean crop which is much larger than Argentina’s. While exports remain lackluster, once Brazil begins to harvest they will become worse. The rally into the end of the year was very welcome and the start of 2023 will set the tone into the spring.

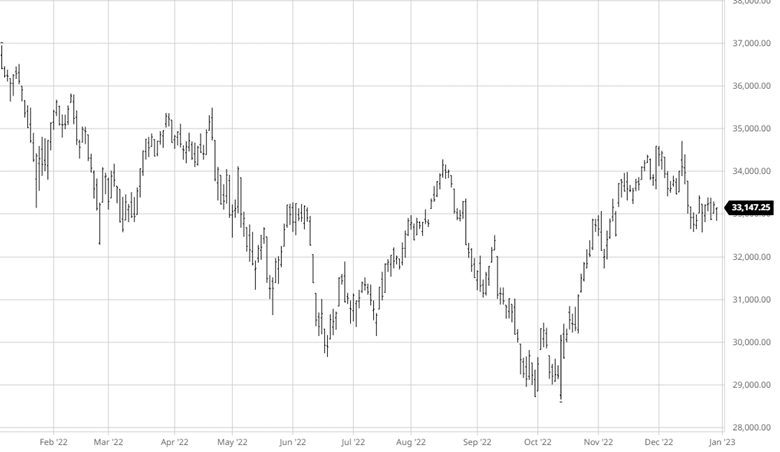

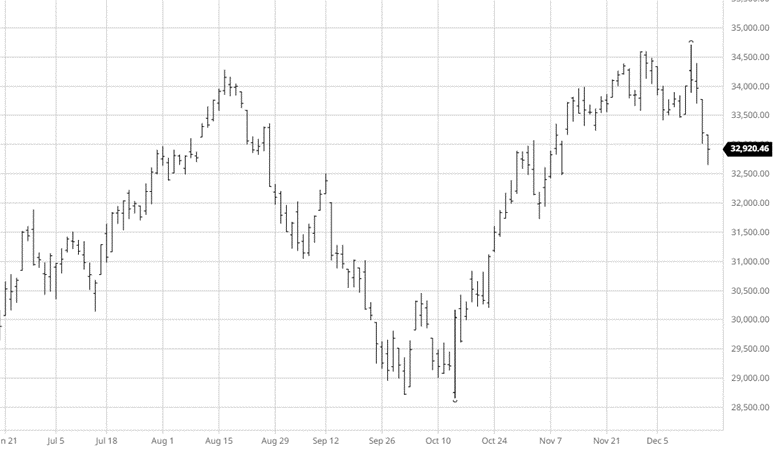

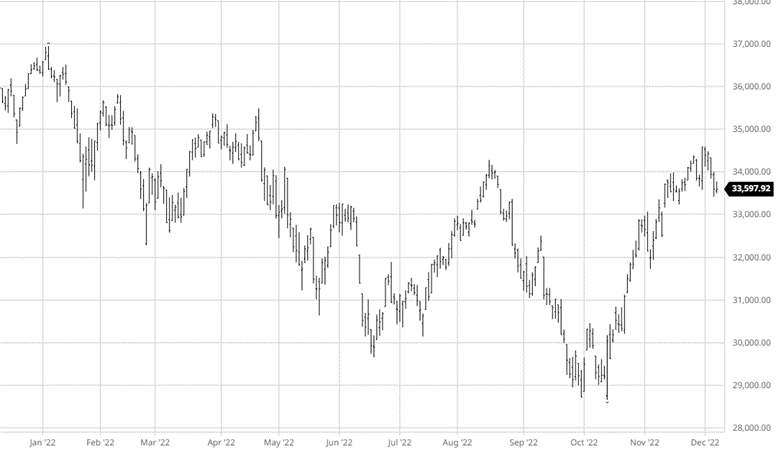

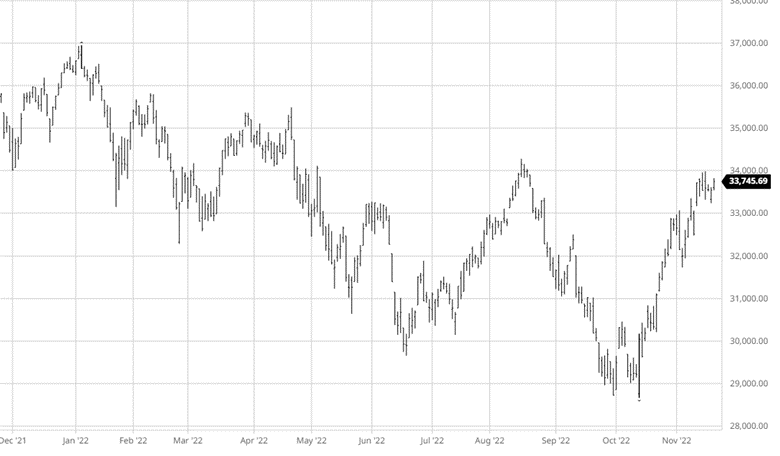

The Dow has been flat the last couple weeks while the NAQDAQ and S&P 500 stocks saw losses. The continued rate hikes into 2023 along with recession fears continue to weigh on the market as investors look for answers along with some tax loss harvesting to end the year. 2022 was not a great year for the markets as a whole and 2023 will sure to hold its own surprises.

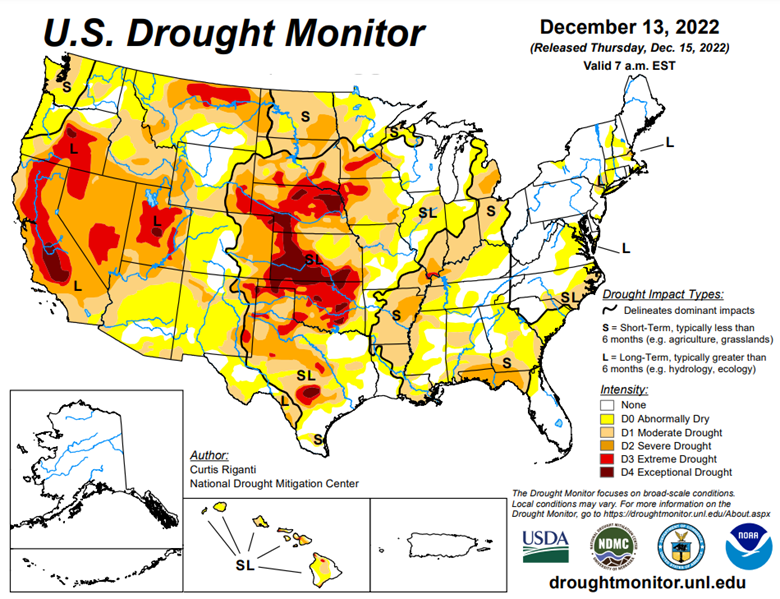

The Hedged Edge is back online with a guest who could be this podcast’s most important guest of all time. At a time when inflation is running rampant through the world economy, drought conditions are drying up our rivers, and the global supply of grain is scarce. We are tasked with the question, “what the hell is going on in logistics, and is there any relief in sight?”

To help address these questions and more, I am joined today by a man that needs no introduction to most in the physical commodity sector – Woodson Dunavant with the Dunavant Logistics company based in Memphis, TN.

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or [email protected].

The liquidity issue in the marketplace seems to be getting worse not better. At this point in the cycle, we should start to see a few green shoots. None were to be found last week as futures hit a new low on Friday. The outside markets are having a bigger than normal effect on our trade. Mostly due to the lack of news here. I’m confident that overall production on January 1st. will be less than the amount produced December 1st. The market seems to agree but throws in the fact that there will also be less homes starting on January 1 than started on December 1. The question becomes of how long the drifting lower will remain in place.

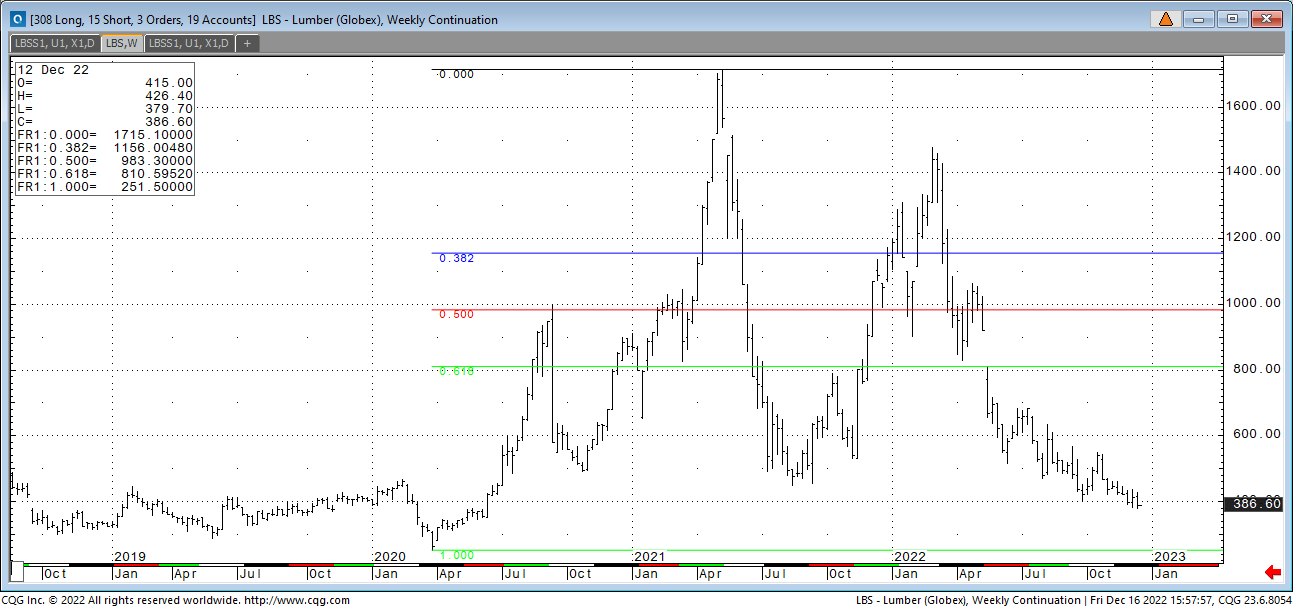

Look at the chart below. It has a Fibonacci measurement from the contract low during covid to the highs in 2021. Look to the left and 2019. The sideways price channel for the year was developed with an average of 1.29 starts. If that is the number, we are looking for 2023 then a sideways trade for a year could be expected. I’m not sure if that will develop but it does look like the current futures market wants to test that theory. I’m in the camp that next year will be somewhat subdued, but at a higher level. Next week will be more of the same unless the short funds start to cover. It hasn’t shown up yet so that is even a limited wish.

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

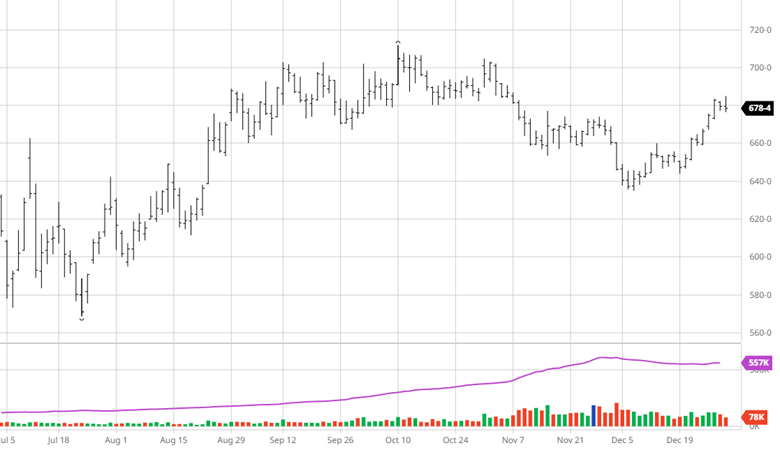

Corn had a good week making gains on mixed news across the world. The war in Ukraine has picked back up with more bombing and aggression from Russia after a “quiet” few weeks. Exports were better this week as we head into the end of the year well behind the expected pace. Weather in Brazil remains good in most areas while Argentina forecast is becoming wetter. Markets will likely remain cooled through the holidays unless there is any unexpected news (flooding rains, further escalation in Ukraine, etc.) that is not already priced in.

Soybeans were relatively flat this week with a mix of up and down days. We are back up trading at the top of the range we have seen since July. Whether it fails at this level again or can move higher may require some surprise news to the market as exports were good, but the market seemed to shrug off. With South America expected to produce a record crop and those beans hitting the world market in a little over a month, finding buyers for US beans could become challenging. Like corn, news may be quiet heading into the end of the year and holidays.

The markets were down this week following a good amount of volatility following the Fed’s announcement of a 50-point hike in rates with comments indicating there will be more raises in the future and could be held higher for longer. CPI came in better than expected but still hot at 7.1%. While we are 2% lower than the highs, we still have a long way to go to hit the target of 2-3% which the Fed will continue to work towards.

The Hedged Edge is back online with a guest who could be this podcast’s most important guest of all time. At a time when inflation is running rampant through the world economy, drought conditions are drying up our rivers, and the global supply of grain is scarce. We are tasked with the question, “what the hell is going on in logistics, and is there any relief in sight?”

To help address these questions and more, I am joined today by a man that needs no introduction to most in the physical commodity sector – Woodson Dunavant with the Dunavant Logistics company based in Memphis, TN.

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or [email protected].

What a difference a year makes. This week 12 months ago saw a $170 trading range with a high of $1069. Last week we saw a $50 trading range and a high of $436. Last year the market was in a full panic. Today it is not. The reason I bring this up is that it has been one hell of a run and now we are suffering from the hangover. No one can argue that we are in full stop mode that has pushed prices to the lowest level since the covid shutdown. Is it sustainable? Probably not. Will it go lower probably. All that said, this market is going to start working itself out of this spiral lower trading. What are those indicators?

This market has sold off sharply because of two issues. The first is the drastic slowdown in construction on the horizon. The other is an industry with no appetite for inventory. The first is a known value. The estimates of a 30% reduction in building are getting announced almost daily from builders large and small. The distribution side of the industry is in for some real pain and is drastically trying to curb supply. That brings us to the other issue and that is the fact that everyone is curbing inventories. Everyone is off at least 30% of volume by now. That is a formula for the downward spiral to end. That does not indicate a turn but shows a limited downside from here. If you add in the technical read, we get the same conclusion.

The weekly outlook shows a pattern of limited downside. The futures market has traded between the moving averages and the lower band since June of 2021. Today the spread between the lower band and the averages is $100. That spread was over $300 for almost 2 years. The lower band sits at 374. The averages sit around 473. The market could take the 373 band out, but history tells us that it will recover. That band will lower but it isn’t indicating that today. This pattern also shows us how much resistance there is at the 473 level.

To sum it up the call is for a bottoming action followed by a sideway trade. Most of our headwinds are not supply and demand related anymore. They are driven by outside economic issues. This week’s Fed announcement could upset our market, but regardless we have started the process to find equilibrium. The lack of the roll has been surprising.

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

December has not been good to corn as we started the month with a slide lower into the $6.40s. There has not been any major news change with a good start for corn in Brazil, China lockdowns, and the war in Ukraine continuing to hold the headlines. While weekly exports have been good but uninspiring, the weakness in the USD should help US ag exports be competitive in the coming months before the South American harvest. The humanitarian corridor has continued to work as ships leave Ukraine, but as always this is something to keep an eye on for any bad developments. Russia is expected to resume ammonia exports soon, which would help keep input costs for 2023 from getting much higher.

Soybeans have seen a nice improvement with their slow march higher from the beginning of October. The EPA came out with lower-than-expected biofuel mandates sending soybean and other world veg oil prices lower while meal has taken off higher. Soybeans hit their highest price since mid-September this week with buyers coming back in the market with a weakening USD. South Americas start has been good enough to where the market expects them to produce another record crop but there is still a long way to go. Right now, there does not appear to be much higher of an upside than the low $15 range in the near term, but if South America has weather problems, that could be the catalyst to move higher or if weather remains good the next move lower.

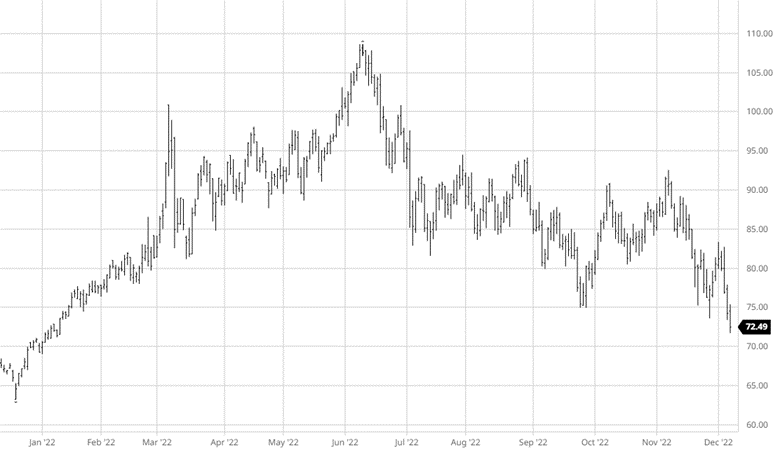

Crude has had an interesting second half of the year following its peak in June. While it has traded between $80-90/barrel most of that time, this recent dip below $75 shows there is a lot of uncertainty as we head into winter. The sanctions on Russian oil by capping it at $60 goes into effect this week while many investors do not expect to see it having a major impact immediately. With Russian oil already trading below the $60 and their breakeven closer to $40 it does not appear this will dampen exports for them with India and China continuing to buy. Europe is still struggling with energy as the war in Ukraine continues. Further guidance from the UN or another shock to the market (China loosening Covid restrictions) could send Crude back higher to its recent trading range.

The equity markets had a great November rallying over 10% but have gotten off to a sluggish start in December. While data comes in still pointing to a strong economy and job numbers the ball is in the Fed’s court on what to do with rates. It is expected that there will continue to be rate hikes into 2023 with the Fed potentially keeping rates higher for longer than originally anticipated but slowing the rate at which they raise them. Some of the largest companies in the world have either laid off workers or frozen hiring as many questions remain for next year.

The Hedged Edge is back online with a guest who could be this podcast’s most important guest of all time. At a time when inflation is running rampant through the world economy, drought conditions are drying up our rivers, and the global supply of grain is scarce. We are tasked with the question, “what the hell is going on in logistics, and is there any relief in sight?”

To help address these questions and more, I am joined today by a man that needs no introduction to most in the physical commodity sector – Woodson Dunavant with the Dunavant Logistics company based in Memphis, TN.

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or [email protected].

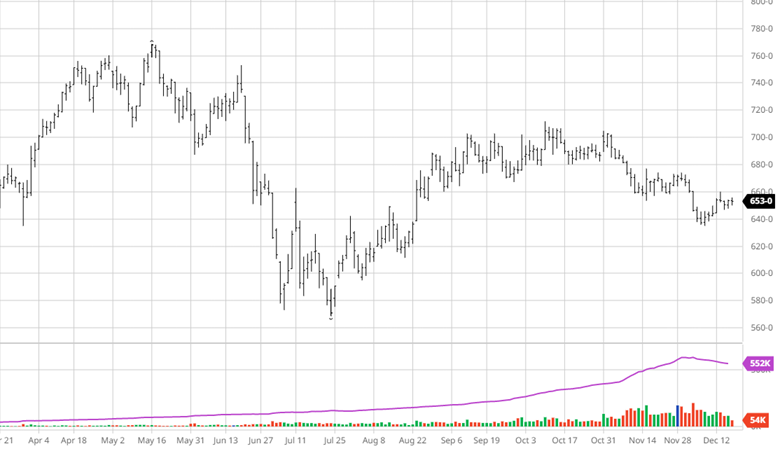

If you have been around long enough you have seen times when there is no market. It was always caused by some event. This time the focal point is on the free money causing an overbuilt/overpriced housing sector. The market now has to digest the run up. Commodities in general will have extended swings as traders are either 100% in or totally out. The issue today is that the buyside continues to add cheap product to the pile for the first quarter. This could be a Peter and Paul moment. We are going into a critical week for the market. There needs to be a shift in interest level going into the end of the year. We shall see.

I talked about the futures market starting with a 3 handle back in late July. It took over 4 months to get there. Except for a few corrections the futures market has traded sideways. Only when the cash market accelerated down did futures finally sell off. Futures were building the bottom end of the range. Today they are just following an unhinged cash market. My point being that futures is looking at the low $400 as a tradable level. That is not a buy recommendation, just a value area. I have been around too long to think the mills will find a bottom anytime soon. Firms today really believe that all this will end soon, and things will be back to normal. There is little planning going on to limit exposure. It will take time.

The technical picture could be friend or foe. On the friendly side the whole momentum complex has come together. Rarely has a market continued its trend without some type of correction. With the RSI at 29% there may be more downside but with the pattern and going into the holidays I expect a little pop. Now on the foe side the Bollinger bands are moving sideways but January futures closed under the lower band. Futures tend to bounce right back into the band area. If futures continue down, it will take time and distance for the bands to catch up. Doing the math today that level would be $307.80. There is the shock.

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

At this point it’s time to keep it simple. I remember the quote from Ronald Reagan about the cold war. He said, “let’s keep it simple. We win they lose.” Today we don’t have a road map. We don’t have historical data. All we have is the market in front of us. The data indicates a market headed for $300 while the real fear is it goes up $300. Both are a reality. Without a supply disruption the market is geared for a slow erosion with light rallies in between. Any signs of fear from the buyside and the mills will be off the market again.

Most would agree that housing is in a created recession. That is a recession caused by a steep increase in prices. Whether those price increases were cost related or not, it has the same effect at the end of the day. The only question is how deep of a recession the US go into. A layoff panic will drag housing into a deeper recession. A recession with minimal layoffs will allow the market to find a level and build off of it. The bad news it may take until the 2nd quarter to see how bad it could be.

Today the futures market is at a standstill. It is drifting lower with the cash market. The January futures contract has had a $38 trading range in November so far. There are three days left but nevertheless that is the smallest range in years. All the pressure in futures comes from the electronic trade made up of either the algo or the funds. The industry has pared its inventory to a level that hedging is not necessary. That is friendly. Any disruption in supply sets off the panic beginning with the funds covering shorts. That is where the big run-up would come from.

From a technical standpoint the market is close to a move. The Bollinger bands are as tight as we have seen in months. The sideways trade has pushed the market into an area calling for a breakout. A strike will set things off to the upside. A .75 raise in December will probably cause the bottom to drop out. In either case the futures market wants to trend. I’m still a fan of mitigating upside risk. The downside is easy.

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

With this abrupt pause in our industry it may be a good time to do a review of 2022 and projections for 2023. The reason for an early start is that any movement from here will be the result of first quarter planning. There are three focus areas that will drive prices. The first is the decline in demand and new forward guidance. Next is the cost of production and lastly is the equilibrium equation. Let’s go last to first.

I now call the equilibrium equation a numerical defense. The focus in the last decade was just how underbuilt the housing industry had become. I call it a numerical defense because we continue to use an old formula to get this rather high number. It is based on a husband, wife, two kids and a dog. That isn’t the typical household today, so the underbuilt number is high. In the mid 2000’s we took starts up to 1.6 because of spec buying. If fell to 500 once the spec homes were empty and for sale. This recent hysterical run was fueled by 401K borrowing or buying among other factors. The point I am making is that at 7% mortgages and a 385K starter we are overbuilt.

Next is the cost of production. Does anyone think it could be in the $400’s? Nope. We are all looking at a $600 number. I know I am and can defend that number. That is for 2×4 2&B spruce. I think the entire basket of products may just be cheaper in some respects than we think. A good example is SYP. 10 years ago, that would not play into the mix as much as it does today. The cost of production is a non-defined factor in pricing today. It will be dragged into it eventually, but for today a mill trading spruce under $400 speaks volumes.

Finally, another difficult statistic to follow is demand and construction. We are seeing the expected push in building for yearend. The builders are getting it done while also looking for at least a 30% drop in construction for the first half of the year. This strategy to build and then abruptly stop seems counter intuitive. They are increasing available homes in a falling demand market. What this will do is extend the period of easing until the excesses are cleaned up. It isn’t an economic strategy but more of an accounting move. My first thought is to be careful of the home builder stocks in the short run.

The expectation from here is to look for the shock to the system that turns the market. Until the market experiences it the trade will be one of floating into a buy round that lasts for three days or two weeks. In either case new lows can follow. This market remarkably looks like the lumber market of old. Can that be possible?

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Corn strung together several days lower in a row last week with a neutral USDA report in the middle of it. The USDA raised the US yield to 172.3, which was within the range of estimates. While corn had been trading sideways for some time, the move lower remained in its trading range, followed by a bounce back higher this week. The black sea export corridor deal being renewed is welcome news for the world supply chain. Brazil and Argentina got some needed rain while some dry areas missed out. They are still suffering drought conditions, but it is also still early in the year. Exports improved this week from last, as the current price levels attract buyers.

Soybeans fell over the last two weeks, due to two days of large losses this week. Soybean Oil got hit as world veg oil prices fell, pulling beans down with it. The rain in Argentina helped speed up soybean planting but rain will still be needed moving forward as still about 25% of the country experiences drought. Bean exports, like corn, improved and better than expected this week. The lack of news makes this a difficult market to trade in as there are no overwhelming bullish or bearish factors dictating direction.

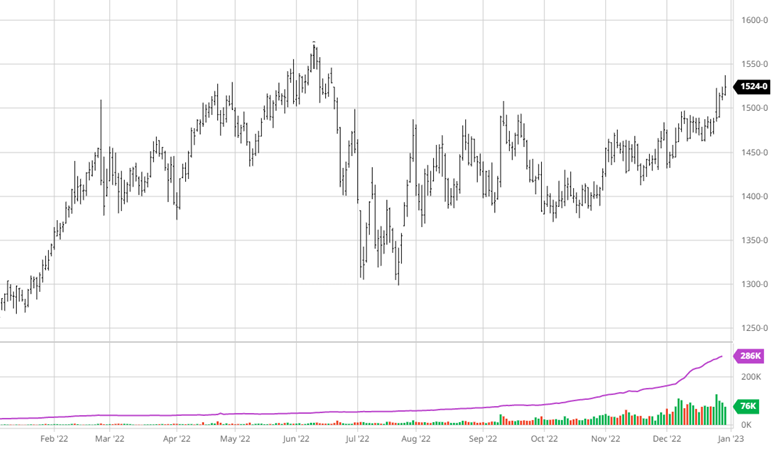

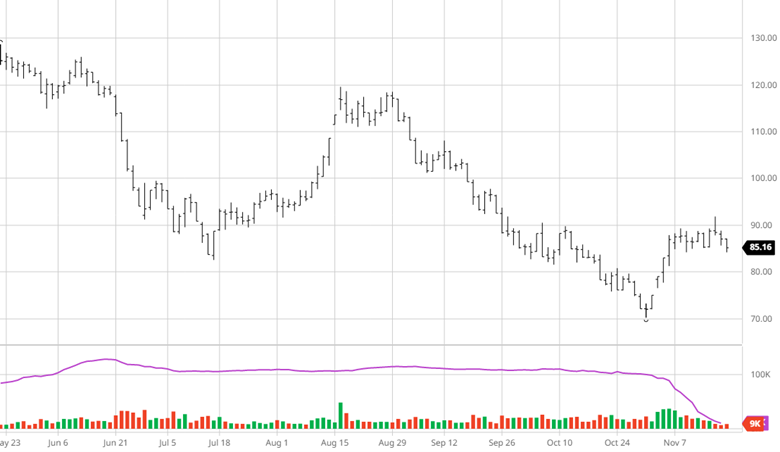

The US cotton supply was raised in last week’s USDA report with better yields and lower demand. The problem in the cotton market right now is demand. While more money is being spent , fewer units are being bought which translates to less consumption. With the continued high energy prices and inflation issues across the world people are prioritizing eating and heating their homes and fueling their cars (good call) over buying new clothes. The potential for a looming world recession in 2023 does not ease demand concerns as we would not see demand for cotton pick up as producers would sit on inventory they currently have. Until we get more clarity on the world outlook and 2023 it is a time to be cautious. The weakening USD will be worth keeping an eye on.

The equity markets started off November with gains after a cooler than expected October CPI of 7.7%. While a drop is nice to see it is important to remember the target is 2-3% so we are still much closer to the top than the bottom with a Fed rate rise coming in early December. The markets seem to expect a 50-point hike, but there is still plenty of time for that to change and get priced in before. One big question that remains for the markets looking ahead is “what will December bring?”. Will there be a Santa Clause rally? Will markets fall as investors do some tax loss harvesting? Many investors still think a recession is coming in 2023 and the next month and half could give us a better idea what to expect.

The Hedged Edge is back online with a guest who could be this podcast’s most important guest of all time. At a time when inflation is running rampant through the world economy, drought conditions are drying up our rivers, and the global supply of grain is scarce. We are tasked with the question, “what the hell is going on in logistics, and is there any relief in sight?”

To help address these questions and more, I am joined today by a man that needs no introduction to most in the physical commodity sector – Woodson Dunavant with the Dunavant Logistics company based in Memphis, TN.

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or [email protected].

The Hedged Edge is back online with a guest who could be this podcast’s most important guest of all time. At a time when inflation is running rampant through the world economy, drought conditions are drying up our rivers, and the global supply of grain is scarce. We are tasked with the question, “what the hell is going on in logistics, and is there any relief in sight?”

To help address these questions and more, I am joined today by a man that needs no introduction to most in the physical commodity sector – Woodson Dunavant with the Dunavant Logistics company based in Memphis, TN.

And last but not least, don’t forget to subscribe to The Hedged Edge on your preferred platform, and follow us on Twitter @ag_rcm, LinkedIn, and Facebook.

_______

_______

Check out the complete Transcript from this week’s podcast below:

What the hell is going on in logistics and is there any relief in sight? with Woodson Dunavant

Jeff Eizenberg 00:14

Welcome to the Hedged Edge by RCM Ag Services where we’re getting out the field and onto the mic to bring you weekly market updates, commentary from commodity experts in monthly interviews with the biggest names in agribusiness. Welcome to winner at least it feels that way after the one of the warmest falls in recent memory. Today, the hedged edge is back online with a guest who could potentially be the most important guest of all time on this podcast. At a time when inflation is running rampant through the world economy, drought conditions are drying up our rivers and global supply of grain is scarce, are tasked with the question, What the hell is going on in logistics? And is there any relief in sight? To help address these questions and more I’m joined today by a man who needs no introduction to most in the physical commodity sector once and done event with the done event logistics company based in Memphis, Tennessee, what’s in is the Senior Vice President of agriculture and Global Network Development for the company. And as part of the fourth generation of done event family to work for the company. He worked across the globe specializing in cotton trading from 2001 to 2009. And spent four years in equipment leasing, what’s in currently serves as logistics sales and business development for event focusing on the international market. He’s a member of the executive board of directors for Donovan Enterprises, Inc, and is on the board of directors of the Memphis Cotton Exchange and the Memphis cotton Museum. He received a bachelor’s degree in finance from Auburn University. Go War Eagle. What Dr. Woodson, welcome to the show.

Woodson Dunavant 01:59

Thank you. Thank you. Thanks for having me, Josh. I appreciate it. Glad to be here.

Jeff Eizenberg 02:02

Yeah, it’s good times. I mean, my first question your Memphis with the river being as crazy as it is really concerned for the catalyst industry and the restaurant industry. You know, I’ve I’ve had lunch at Blue City cafe over there on Beale Street. The guy told me he’s, he’s, you know, cooking up 180 fish a day. What? How’s he doing in all this? Oh,

Woodson Dunavant 02:26

to be completely frank, he’s doing just fine. Because all his cat fish are not coming out of the river. They’re coming out of the cat fish farms. They’re all in the delta. So he’s gonna be okay. He’s gonna be quite alright.

Jeff Eizenberg 02:36

He’s alright. Okay, well, I thought maybe they were you know, he’s grabbing them off the bottom fish at the Mississippi or something?

Woodson Dunavant 02:42

No, but they are finding each day that goes by you get somebody on the news saying that they found a civil war piece of memorabilia or something, you know that the river hasn’t been this low. And however many years and you know, you’ve got all these treasure hunters that are down there looking for some and things of that nature. But, you know, the real crux of it is what is it doing to the to the grain shippers right now. And it’s a mess. In some cases, you know, the river, where we used to be able to do two barges pass on one another. Now, in some cases, it’s just one line traffic. And then throw on top of that, typically, some of these barges will be able to go to three, you know, far out, and now they’re only able to go you know, back to back, if that makes sense, to lane single. And then add in that to the fact of the river being as low as it is, then they can’t carry the payload that they would be in years past as well. So you push all that back to the farmers pocket. And you know, his supply chain costs have really, really gone up a B, he can’t move the volume that he’s used to moving. So what is he doing? In some cases, you know, they’re just going to sit and put their put their product in their in their bed or their silo, until until things get better, which, you know, there’s there. I don’t know when that’s going to happen. You looked at Long long term forecast, things of that nature, you know, a couple couple inch rain in the Midwest, it isn’t going to move the river level up by 10 feet. So you know, we’ll just have to wait and see how that how that goes.

Jeff Eizenberg 04:26

It’s kind of a wild ride right now. And yet, the pictures and the images are stunning people sending drones to give you pictures. I do sense. I don’t want to get too into this before we get a little bit more background. But I do have a question and maybe we’ll tackle it a little bit later about about those drunk drunk foot photos. I feel like a little more a little. Maybe not exactly the river. They’re like the tributary so kind of make it sound a little worse than it is. Yeah, so what you just described is pretty pretty dire. Um, Before we get too far into into the state of things, Watson, I think it might be best if you could just to share your background of the company. And you know why we’re even talking with you about logistics. I mean, you guys have had an extensive knowledge of logistics systems, both rail, barge, freight, etc. So if you could maybe just share a little bit of that background, and then we can jump into these problems. And hopefully, you’re not going to solve the world’s issues by the end of this call.

Woodson Dunavant 05:32

No, there’s no question that that’s gonna happen for sure. We might need a beer, a glass of wine to really get to the bottom of it. So yeah, so don event is a family company that started in cotton trading with my grandfather, back in the 30s. In the 40s. My father took it over, took over the business in the 50s, when his dad passed away when he was in his late 20s. So he was sort of thrown into the fire. Early on, he was down on on Front Street, where we were all the cotton traders were at that time buying cotton from the Delta and and shipping it to the US textile mills, you know, the manufacturers who were ever on the East Coast, and even in the northeast,

Jeff Eizenberg 06:18

they no longer exist, right? Yeah. So,

Woodson Dunavant 06:21

you know, we used to consume between, you know, call it 10 and 15 million bales a year domestically, and right now, we’re just north of two. And, you know, we’ll talk about this later. But, you know, manufacturing coming back and things of that nature, you know, is that, you know, is that gonna go back to 10? million? No, is it gonna go to five? I doubt it. But who knows? You know, we’ll, again, we’ll hit on Mexico and other things like that later. But yeah, I mean, it is the US textile industry is very, very small. So. So what does that mean? So, as we transitioned into that, it mean, it meant that there was a blow up in the international world for textile manufacturing, primarily in in Asia, Southeast Asia, subcontinent, so on and so forth. So as as manufacturing, went overseas, my father went overseas as well, to be able to sell, sell cotton. So we were buying cotton, you know, from the 80s and 90s, early 2000s. Were buying cotton anywhere in the world, that cotton is being grown, and then we’re selling it to the manufacturers. So

Jeff Eizenberg 07:35

you’re buying from Australia, India, all over the world,

Woodson Dunavant 07:38

anywhere there was yeah, it was Becca, Stan, Brazil, Australia. Tragic. I mean, you name it, wherever it was being, wherever it’s being grown, we were there, buying it, and then selling it to the manufacturers. So in the mid 70s, my dad made the first sale of cotton to China, which was a huge development. I think that was in 72. And then Sunday eight, we made the largest sale of a million bales to the Chinese government. So that was really a big thing for both our company as well as us. cotton industry. And now today, cotton is, excuse me, China is still the largest consumer of us cotton in the world. They have a large crop themselves, but they they have a major surplus of need of imported cotton.

Jeff Eizenberg 08:32

So thank you, Nike and Adidas and everybody else, right?

Woodson Dunavant 08:37

Yeah, yeah, exactly. All clothing, upholstery. But you know, even stuff that you wouldn’t think of what cotton goes into is manufactured over there. And a lot of times brought back over here as well.

Jeff Eizenberg 08:52

So with all those purchases, and sales, then comes the logistics portion. Correct?

Woodson Dunavant 08:57

That’s right. That’s exactly right. So it’s still cheaper for the retailers kind of looking from field to fabric here from for us to ship a bale from St. Mississippi, to Shanghai, and then bring that bring that shirt back here to Memphis, it’s still cheaper to do that than it would be to do it here in the US, which is really, I mean, you can’t blows your mind. Really, the that’s the way it is. But that’s the way it is. So

Jeff Eizenberg 09:25

I got to ask a question about that. So it’s so interesting to me, the way you describe it like that, is it you’re gonna get the bail here, you ship it over, and it comes back. And then is it just because you have this, your network of the supply chain there is so strong that you’re able to from a net con economies of scale, have enough flow that you have enough movement between the vessels that you’re able to then you know, take it over. You don’t have to sit on a container for, you know, six weeks for it to manufac Asher, and come back. But you have enough flow where there’s always a container ready to come back the other way?

Woodson Dunavant 10:06

Yeah, I mean, that’s Jeff, that’s really deep. And I really wish I could tell you that, yes, we were involved from the field in the US all the way to the manufacturer. And then back here in the US. There’s so many different segments of that Donovan is not involved in that entire supply chain. Well, that would be really cool. If we were Yeah, it’s just there’s so many different pieces to make that puzzle all come together.

Jeff Eizenberg 10:31

We don’t need to get too in the weeds. But I’m curious if you were involved

Woodson Dunavant 10:35

with with our customers with helping them move it from the field to the oversee port, and then we sort of lose track of it there. And then on our on our import side, you know, we’re responsible from once the goods hit the port in Asia, to deliver them here to the United States and the distribution facility got because there is there is a dark area, there are a gray area that we’re not involved at all,

Jeff Eizenberg 10:58

leave that to somebody on on their side that can speak a language and manage that process got

Woodson Dunavant 11:03

Correct, correct. That’s right. That’s right. So so we did all the all the cotton trading, you know, the mid 2000s, come along, you know, 2007 2008, I’m sure some of your your, your readers will remember those days now crazy thing for when the spec and hedge funds got really involved in commodities that they thought they needed to commodity bucket in addition to their bond bucket and their equity bucket. And that really changed things from us where we’re trying to keep a hedged book with against our long physicals, the market would run up, we’d have short futures against our physicals. And then, you know, in order to hold those positions, we’re having to send money margin to keep those positions. And it just got, it just got too much for my dad and our family, whereby, you know, our net worth was on the line. And it just, it became really uncomfortable from a family standpoint, from a from a financial standpoint, everything and so he, you know, had the foresight to look at possibly marketing our cotton division. To sell it, we had multiple suitors. At the end of the day, Louis Dreyfus Corporation was the one that came in and bought all of our cotton trading people and divisions around the world. So we had things that they did not have in Central Africa, in Brazil, and Australia. And so it really helped them put together, you know, the full global portfolio footprint that they needed to go to the next level. So

Jeff Eizenberg 12:42

it’s no surprise today, they are the largest of, you know, knowledge. They’re right there. Yeah,

Woodson Dunavant 12:48

that’s correct. And we were in Donovan Donovan was right there with him, we were doing between four and 6 million bales a year globally, you know, between one and $2 billion of revenue, we were spending, you know, upwards of $250 million a year in logistics. And so that’s when the whole logistics thing for us sort of sort of tipped itself off. And when we were when we made that sale to them, you know, they they did not want any of our people that were doing the logistics. So we, we kept those people and we’ve built this this Threepio, which we will go into more detail about.

Jeff Eizenberg 13:25

That’s great. So then how many people that are on the team today, across the globe? As I know, you have global operations?

Woodson Dunavant 13:32

Yeah, it’s really hard to say, to put a number a finger on an exact amount of people, we’ve got a lot of contractors, we’ve got agents, we’ve you know, so it’s a real hard number to put, I mean, it’s north of 200. But it could balloon up to if you include contractors and agents and all that. I mean, it’s a really big number.

Jeff Eizenberg 13:57

Sure, not to mention all the people that are involved in you know, running the rail or you know, trucking etc, you get to put everyone together in the 1000s. So it makes makes good sense. Okay, well, that’s a that’s one heck of a ride for you. You’re in the family and obviously, to get to where you guys are here today. Now, it would have been seen that natural that you’re also still heavily involved in cotton.

Woodson Dunavant 14:27

We are we, we do so we do freight forwarding for a lot of our old cotton competition. We do a lot of a trucking and logistics for them. The whole bucket of Donovan logistics, it’s probably 10 or 15% of what we do. So it’s not it’s not it’s not as big as I would like it. But it’s still it’s a core. It’s a core business for us. And, you know, we do everything like I just said from documentation to try Looking to ocean freight in some cases. So yeah, cotton is in our blood and we can’t get it out of our blood, nor do we really want to so the side that we’re in now, we don’t have any risk for, for cotton and being able to be in the business without risk is a good thing.

Jeff Eizenberg 15:17

Yeah, I agree with that, you know, that’s, we’re all in that business. And it’s, it can be heart palpitating. So, okay. 15% is cotton, what other products are involved in agriculture, or if if it can be shipped your yours,

Woodson Dunavant 15:35

if it’s if it can be moved in a container, Jeff, where we’re going to be involved in it. So, you know, we’ve done everything from Peanuts, to soybeans, to corn to Rice, tobacco, alfalfa, you know, just anything agriculture, you know, we’d like to, for someone to come to us with a challenge of, you know, we’re only able to get 20 tonnes in a container, well, let’s bring it to a major city or a big place where there’s heavy weight, translate it, and we’ll get 25 times in the container. So for every five moves, you’re getting a free container. So every four, so yeah, that those are the types of things we like to look at with with our customers is how can we do things different? How can we maximize our plate payload? How, you know, how can we how can we be a solution to something that they need help with and that that’s how we grow our businesses is people come to us with problems and we help solve.

Jeff Eizenberg 16:32

Yeah, well, listen, that’s, that’s, that’s a great service. And obviously, you’ve been able to continue to grow. So you’re, you’re based in Memphis, would that also then insinuate that a majority of the operations and movements starts and ends there on the river? Or are you also focused on the ports and the International terminals as well?

Woodson Dunavant 16:56

Yep. So Memphis is home. Obviously, Memphis is where our headquarters is. Memphis is, is near and dear to our heart. And Memphis is great. We love Memphis, we see the growth. We’re very bullish on Memphis. As you know, we’ve got all five major railroads here, which only Chicago has that going through them. We’ve got the largest freight airport, with FedEx moving through here. We’ve got our 40 corridor, trucks moving, you know, east to west connecting the east to west coast. 50 fives connecting Mexico with Canada. So we’ve got, you know, road rail runway. You know, it’s all here. And so we’re, we’re very bullish on that. But to your question, no, Donald’s moving product in and out of every major rail hub in the United States, as well as port, we concentrate in the southeast, and then the Gulf, Houston and Dallas, Memphis, Savannah, Charleston, Norfolk, Baltimore, Wilmington, and then an inland we’re, we’re Nashville, and Memphis in Atlanta. And as I said, Dallas, so we’re really focused in the southeast, and then the Gulf. But we’re also moving product in and out of the P and W, in the northeast, as well. And in southern Florida. So there’s no real you know, we’re, we’re spread all across. So we’re lucky in that regard.

Jeff Eizenberg 18:29

That’s great. I guess it really kind of circles back to, like I said, at the beginning, you’re one of the most important people in the world to be talking to you right now. If you’re, you know, you’re so spread out that you are touching so many different pieces of the overall logistics. gameplan, or footprint, let’s call it that. And we all have been hearing about all the problems that are out there. And I guess, before we just say today, this is the problem today. It seems as if this the backups and the issues and the increasing costs and everything kicked off with COVID with the COVID pandemic, and then it’s just really never cleared the system. And then now we have new problems, right, we’ve got drought and other conditions. Was it was this is it fair to say that that was really that was the kickoff the Genesis? And is is that portion of it? Or is it portion of that portion worked itself through and we’re now facing other problems? Where are we at?

Woodson Dunavant 19:31

Yeah, I mean, COVID changed the supply chain. Things are not going to go back to the way they were pre COVID. Right? Post COVID COVID, whatever. I mean, it’s not going back to the way it was right. That’s crystal clear. The question is, what is it going to do in the future because it’s going to change again. You know, rates went through the roof. Now they’re crashing back down, both from mostly frame rates, breakpoint rates, yes,

Jeff Eizenberg 19:58

interest rates are going straight up. Yeah, interest rates going up

Woodson Dunavant 20:01

freight rates going down. I mean, we’re, we’re in a freight recession right now, you know, importers have, you know, they couldn’t get their hands on enough inventory. Well, now they’ve got too much inventory, and they can’t move it. The consumer is not buying as much as he was, you know, they all got scared last year, a lot of the retailers and they couldn’t get their product in for Christmas time. So they brought it in super early this year. And so you know, they are chock a block full these warehouses. I mean, I was reading this morning, Jeff, historically, historically, warehouse levels are about call it 10%. In terms of in terms of vacancy rate, and okay, right now, you’re at, like, want to say, like, around 3%. And it’s literally around 10% For the last decade, and so at 3% Now, it’s a good time to be in the warehouse business. Now. It’s done like, yeah, yeah. So you know, all that’s going to change, you know, everybody’s gonna go out and get their warehouse space, and then then demand is gonna go up, you know, and then things will change. But as it stands right now, being in the warehouse business is a very good business to be in.

Jeff Eizenberg 21:18

Yeah. And then you mentioned, when we talked to a couple of weeks ago, something that kind of speaks to that you said Amazon did their, their Black Friday, Black Friday, a week, thoroughly, which forced even more warehousing to be space to be taken up?

Woodson Dunavant 21:36

That’s right. That’s right. So and it’s not just Amazon. I mean, it’s all these retail guys, they’re all in the same boat together. So, you know, with with, you know, interest rates dealing with they’re doing geopolitical unrest, unrest and Ukraine, and in that area, diesel costs through the roof has really got me concerned, both in North Europe and in here in the, in the United States. I mean, there’s just a lot of uncertainty right now. And, you know, we’re just gonna continue to service our customers and do what we know to do, and just sit back and watch, you know, some of those other things that are outside of our control, but at the end of the day, affect me, my business, your business, my pocketbook, your pocketbook. So, you know, a lot going on right now. And obviously, the China and Taiwan deal. I mean, it, there’s a lot to be keeping around right now.

Jeff Eizenberg 22:34

Right. And there was a period in time when, you know, we saw the pictures on the news of, you know, 500 or 1000 boats back at the LA port. And, you know, a lot of that issue cleared the port issues

Woodson Dunavant 22:50

that cleared up, or I wouldn’t say it’s, I wouldn’t say it’s cleared. But it is, it is working itself out. The issue now is in Savannah, I think they’ve got 20 or 30 vessels awaiting birth there. So you know, once everybody saw everything in LA, they were like, alright, let’s switch everything to the East Coast, into the Gulf. And so you’re having some residual stuff there on the east coast, but you know, it that’ll work itself out, especially with demand dropping right now, I mean, a lot of our import clients have, you know, where they were doing, call it 30 to 50 containers a week of product, you know, they’re less than 10 an hour. And that’s, that’s material, you know, that that’s a massive drop in volume, the ocean carriers are pulling, pulling service out of the market to try to stabilize rates. So where they had four vessels that were on a string from Shanghai to LA, well, maybe they’re only doing two now. So you know, that that’s what they do in order to get their rates back up as they pull capacity on the market.

Jeff Eizenberg 23:58

But sounds like the airline industry, I think I paid like $800 to fly to Dallas a couple weeks ago, like really good. Two years ago, you were giving me a flight for $120.

Woodson Dunavant 24:11

We looked at going out west for spring break. And I can’t even tell you what it’s going to cost to fly a family of five from Memphis to Utah. I mean,

Jeff Eizenberg 24:22

we’re doing it we’re going to Park City and thankfully, I have a friend who has a place to stay but man, aside from that, I’m not

Woodson Dunavant 24:32

Yeah, it’s, it’s, it’s crazy. So so that’s what the that’s what the ocean liners do, as well to take capacity out of the market in order to stabilize rates. So, you know, they’ve done quite the ocean carrier community has done quite quite well in the last couple of years. So we shall see. You know, we should see how they prevail going forward, but I would think they’re going to be okay.

Jeff Eizenberg 24:59

Okay. circling back to commodity markets here. And I’m curious to the back to the river, I guessing that believe something like 60% of all US exports run through the Mississippi, and you were describing this one lane traffic versus multi lane. You know, as I start to think about what this is going to mean, have you seen a shift where people are, your customers are starting to, you know, hire rail and truck and, you know, incur those additional costs that are associated with having to move off the river? Or are you or our or our people, like you said, farmers just stuffing their bins full and the rest of world has to wait?

Woodson Dunavant 25:44

Yeah, I think that’s what you’re gonna see. I mean, you look with demand slowing down. That’s a good thing right now, what you would never say the demand is a good demand slowing down is a good thing from a farmer’s perspective. But to answer your question, I mean, we’re not seeing the grains go from, from a barge to, to the road, for example, me, you’re not, you’re not seeing, because at the end of the day, most of those sales are our bulk sales. So the product has got to move in bulk, you know, and it’s not going to be able, you’re not going to be able to move it to Memphis, and then, you know, I guess you could bulk rail it and translate it at a port. But if you’re not already doing that, in order to set something like that up, I mean, your costs are gonna go through the roof. And so yeah, I think it’s just kind of a sit back and wait, right now do what they can and try to fulfill the contracts if they can, and just just do their best. I mean, look, what the dollar is strong as it is, you know, that’s hurting them as well. So, you know, the farmers are going to be okay. But, you know, they’re just gonna go through a rough patch. And unfortunately, right now, from a timing standpoint, you know, all the crops are coming off right now. And so, you know, they want to get them on the move and get get them out and get ready for new crops. But that doesn’t look like that’s going to be the case next year.

Jeff Eizenberg 27:03

Well, you know, people can wait for close, they can’t really wait for food. So at some point, the basis is going to have to shoot straight up or, you know, they’re gonna have to figure out other solutions to get moving unless, of course, we you get some of the rain. And I guess, you know, you’ve been doing this long enough. 2012 was another drought year, and because we’re reading that the river was, you know, significantly low at that point. What was your experience in that timeframe? And how long did it take before you started seeing things kind of working more normal? Again? Not March or April or May that this? Yeah. potentially even subsides? Yeah. It?

Woodson Dunavant 27:44

I mean, it just depends on on on weather. Really? But yeah, I think spring is what you’re looking at. Once you get the snow melt off from the Midwest. That’s what typically always give the river its strength in its in its last as is that Snowmelt Runoff from north to here. And then that obviously takes it all the way down to New Orleans. So yeah, I think it’ll be spring, at the earliest. So, you know, hopefully, we can get, you know, enough enough rain and wet weather around here to be able to come back up a little bit, but it’s not going to be able to go back up to where it needs to be until until the spring.

Jeff Eizenberg 28:30

Let’s shift over here a little bit. You’ve mentioned the work and expansion of the company over the years. And, you know, I read an article that you guys posted, maybe earlier this year, on the growth in Mexico, do you just maybe talk to us a little bit about what you’re seeing there? Is it? Is it what’s what problem are you solving by expanding into Mexico?

Woodson Dunavant 28:55

Well, we’re, what problem we solve. And so we’re helping solve our customers problems. That’s what we do. And, you know, we saw an opportunity, with things in Asia slowing down of people and things moving, you know, not reshoring to America, but nearshoring to America. And you know that that’s where Mexico comes in. I mean, I’ve talked to multiple people, you know, over the past few months and even years, you know, maybe the quality of the product produced in Mexico doesn’t meet what it is in China, but they are somewhat competitive from a labor standpoint. So if we can get that quality then then I think you would see a massive, massive move to manufacturing in Mexico. So we saw an opportunity we’re it done event has operations at every border crossing from Laredo all the way to Tijuana, and everywhere in between. So we’re moving product both in and out via truck and rail. We have cross docking, we have warehousing. So you We’ve got a gentleman that runs that operation for us who use, I still need to introduce you to and your team, because I think y’all would be benefit to hear from him and what his capabilities are and how, you know, he can help you and some of your customers out with what he’s doing even enter Mexico, not not to mention the border. So we’re very bullish on Mexico, and the US and where that partnership is going to go from here. And so we are

Jeff Eizenberg 30:28

going both ways, right? You’ve got grains and other goods going into Mexico. And then as you’ve just described a little bit ago, how if there’s a chance for us to match the labor and quality, then if we move some of our texts will like, not us. But if some I’ve heard that China is buying up some textile factories and whatnot in Mexico, if they could replicate the work there, but just be closer to us that, then now you’re going the other way, right? You’re bringing it back in?

Woodson Dunavant 30:58

That’s exactly right. That’s exactly right. And, you know, it’s just it’s been a great venture for us. You know, the more and more we look at it, the more and more we like it, and the more bullish we are on it. So yeah, I’m very, very happy with where we’re going there, for sure.

Jeff Eizenberg 31:14

I was talking with a group today, and he was talking to me about Mexican ports, and how the terminals are hardly back over there, and only the largest vessels coming in. Is that been your experience as well, that these port contractors are very long and extensive? And just to break into that it would be difficult? And ultimately, I guess that would mean that there’s better chance for some of this rail and solutions? Yeah,

Woodson Dunavant 31:42

I mean, you know, I think in Mexico is a lot of people know, I mean, you’ve got to know the right people in order to get things done. And, you know, while while there might be longer contracts in place, I think that, you know, you can still get things done if you know, the right people there. Right. So, you know, I think that’s what the name of the game is there for sure.

Jeff Eizenberg 32:04

Is there other any other countries or regions that you’re focusing on other other than, than the Mexico opportunity? And obviously, you’re doing things in Asia? But yeah, I mean, you coming on? You

Woodson Dunavant 32:18

know, we’re, we’re pretty bullish on Vietnam, we’ve got a contingent going over there, I think in the next three weeks or so to go check things out, you know, they suffered from a lack of land and people, but, you know, they, everything that they’ve done is is very impressive. From a port infrastructure standpoint, from a manufacturing standpoint, from a labor standpoint. I mean, you’ve got invest foreign investment from all over the world going into Vietnam right now. And, you know, we’re, we’re quite bullish on on the goings on there, and so much, so I was, like I said, we’re sending sending three executives over there in the next few weeks to go to go investigate further and for sure, do you?

Jeff Eizenberg 33:05

Are you taking a translator? And are you on this? Are you on this contingent?

Woodson Dunavant 33:11

So luckily, we, you know, we don’t really need translators, we have agents and people that we work with, over there that are able to do that for us. So years and years and years ago, when we travel over there, you’d have to, you know, you’d have to have a translator, whether it was in China or Vietnam, or wherever, in Asia, you’re going nowadays, you know, with with as many agents in the network that we have, we’re able to go over there and get around and you know, to be completely honest, English will get you a lot further than you think, especially in Asia. It really will

Jeff Eizenberg 33:45

you heading on this trip, or you’re,

Woodson Dunavant 33:47

I’m not unfortunately, I wish I would I wish I was Vietnam was one of my top countries in the world that I’ve ever visited, both from a food standpoint, from a people standpoint, from a manufacturing. I love love Vietnam is awesome. Vietnam, Thailand and South Africa are the top three for me, for sure.

Jeff Eizenberg 34:10

Sounds good. So you know, this has been a it’s been a great conversation, what’s in it for you know, my takeaway from what you’re saying here is that we all need to think differently in the new environment moving forward, that it’s going to take strategic partnerships, it’s going to take innovation from different companies like yourselves, to come up with better solutions to move products and goods. And achieve really at the end of the day. Our goal of our company and the people with our clients we work with is to help them maximize their margins. And so it sounds like you’re very much aligned with that perspective.

Woodson Dunavant 34:48

Absolutely. Absolutely. If you get if you get if you’re comfortable in your supply chain right now, watch out because there’s a change coming and you know it like I said, we’re here to provide solutions when customers have problems, or they want to look outside the box, that’s, that’s who we are. And that’s what we want to help them do. And, you know, it’s a new normal that we’re in, you know, it may only last another three to six months, and then we could be hair on fire was something else. I mean, who knows? That will happen? Because, you know, I wish I could tell you that, you know, things will go back to the way they were. But as we all know, once you have a catastrophic, cataclysmic shift in supply chain, which we have had pre COVID to COVID to now. It’s a new way of doing business. And yeah, so it’s, it’s fascinating. The one thing that we didn’t touch on, was, I think you want to real quick on the rail issue.

Jeff Eizenberg 35:46

Oh, yeah, please. Yeah. What’s the story? Are they is it Congress is the only one that could solve this or what’s going on?

Woodson Dunavant 35:52

So they did they have originally they had said the 19th of November, they just extended it to December 4. And so they’re gonna have another couple three weeks negotiation, which I view is a very positive development. At the end of the day, Congress and or president are gonna have to step in, because if you were to have that happen, I mean, you talk about you think that the LA Long Beach strike was a big deal. You talked about stoking inflation. I mean, it would be tattered. Strophic, if we had a major rail, strike, I mean, you know, 40%, of, of all goods, in terms of weight is moving on the rail. And if you if you were to stop that, I mean, you can’t get from a food from a retail from you. I mean, you just goes on down the list. I mean, it would be I can’t imagine that the government would allow that to happen, though, they will step down at the 11th hour, if it gets to that point and put their foot down, they have to,

Jeff Eizenberg 36:57

yeah, I mean, everything with the just in time production that we have here and consumption in the United States, if even a day or two delay when we’ve seen with, you know, weather conditions or something backs things up, and it takes months for it to work through. So if you started if you had weeks or months off, oh, my goodness, you’re,

Woodson Dunavant 37:19

I mean, to your point, even even five days, like something like that would set us back by, you know, three or four months. I mean, it’d be crazy. So I do not think that that will happen. So you can come back and poke me when they do strike and then everything shifts.

Jeff Eizenberg 37:36

Instead, it was not gonna happen. Place your bets. Yeah. We get it. I appreciate that insight. Because then yeah, you’re at the pulse of it. I mean, I assume that the people in the rail industry don’t want it to happen either. But they also want to be paired paid fairly and get proper compensation. So

Woodson Dunavant 37:53

that’s right. That’s right. You can’t fault him for sure. Yeah,

Jeff Eizenberg 37:56

that’s exactly it. Well, no, this has been extremely good and extremely helpful beneficial to I think everyone listening and, you know, welcome, welcome. You obviously share it yourself. I always have one final fun question for everybody. And it’s what is your favorite extreme sport that you either participate in or would participate in if you maybe were back in your yet 20 year old buddy?

Woodson Dunavant 38:20

Oh, Lord and mercy, stream sport?

Jeff Eizenberg 38:25

I mean, you talk duck, honey, that’s kind of the kind of counts.

Woodson Dunavant 38:28

Okay, well, if that counts, then I will. You know, it’s an extreme sport, in some cases, for sure. Yeah. And I really enjoy it. So. Yeah, I mean, that would be that would be it for me. For sure. I was thinking more like MMA or boxing. Oh, yeah. Well, you could do that too. I mean, I really miss heavyweight boxing. And, you know, back in our day was was was when Tyson and Lewis but even before that, I mean, you know, we would block an entire night out, you know, to get ready for the boxing match. And I mean, it’s it feels like it’s gone. Like, MMA has just totally taken it over. But I mean, I feel like there’s still a space for good heavyweight boxing, and it just, it’s gone. It feels I just, I really miss that.

Jeff Eizenberg 39:15

Maybe Tyson was the pioneer of it, because when he bit Holyfield’s ear, nowadays, MMA if you’ve met somebody there, they might be like, yeah, that’s okay.

Woodson Dunavant 39:23

That’s right. That’s right. There’s no doubt there’s no doubt so

Jeff Eizenberg 39:26

pretty good. Oh, what’s the what’s the best way to get a hold of you have people had to want to want to connect?

Woodson Dunavant 39:33

Yeah. So reach out to me. My email address is very simple with some data of it. I’ve done have a.com Email me, you can give me a call. And happy to talk through anything with anybody importers, exporters, domestic domestic folks here in the US anything cross border. If I don’t know the answer, I’ll put you in touch with somebody here. That does. We’ve got we’ve got IT experts all over the place. Donovan, I’d be happy to put you in touch with whomever you need to talk to. So we’re, we’re really excited with our growth and where we’re going. And, you know, we’re just we’re in a we’re in a really good place right now. So, Jeff, I appreciate you doing this. I’ve enjoyed getting to know you over the past few weeks, and hopefully this won’t be the last time I talk to you.

Jeff Eizenberg 40:24

Yeah, we’ll do it again. We’ll check back in whenever fills back up. All right.

Woodson Dunavant 40:27

Sounds good, Jeff, appreciate it. So much

Jeff Eizenberg 40:29

Appreciate the time. Yep. Take care. Thank you.

This transcript was compiled automatically via Otter.AI and as such may include typos and errors the artificial intelligence did not pick up correctly.

RCM Ag Services is a registered DBA of Reliance Capital Markets II LLC. Trading futures, options on futures, and retail off-exchange foreign currency transactions are complex and involve substantial risk of loss and are not suitable for all investors. Loss-limiting strategies such as stop loss orders may not be effective because market conditions or technological issues may make it impossible to execute such orders. Likewise, strategies using combinations of options and/or futures positions such as “spread” or “straddle” trades may be just as risky as simple long and short positions. There are no guarantees of profit. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge and financial resources. You may lose all or more than your initial investment. You should not rely on any of the information herein as a substitute for the exercise of your own skill and judgment in making such a decision on the appropriateness of such investments. Opinions, market data and recommendations are subject to change without notice. Reliance Capital Markets II LLC shall not be held responsible for any actions taken based on this website or attached links. Parties acting on this electronic communication are responsible for their own actions. Past performance is not necessarily indicative of future results.