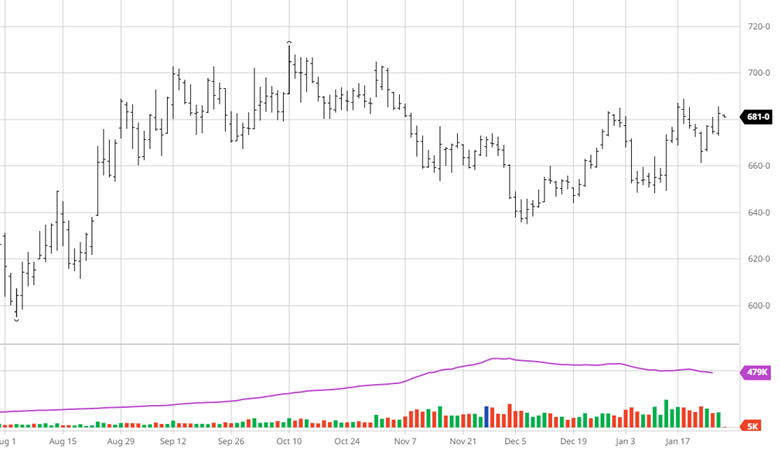

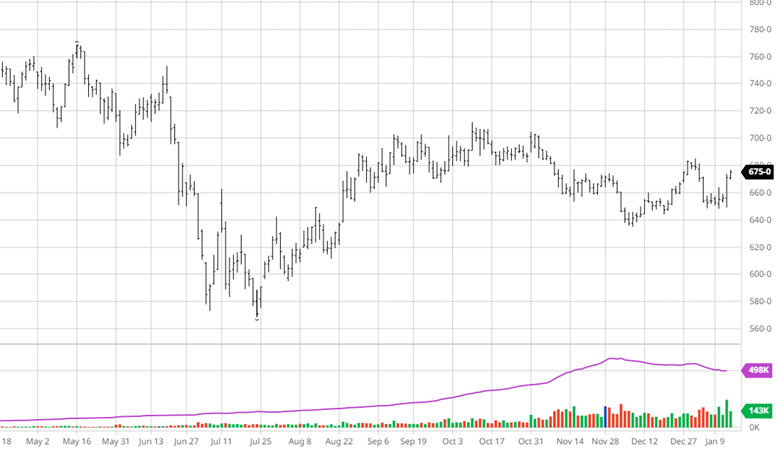

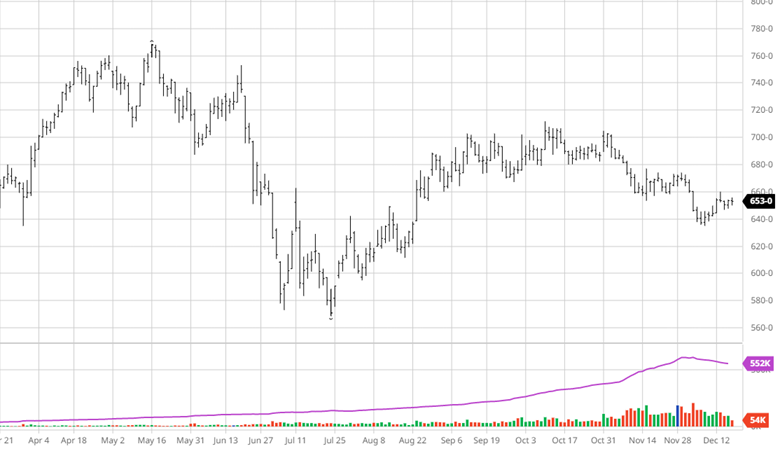

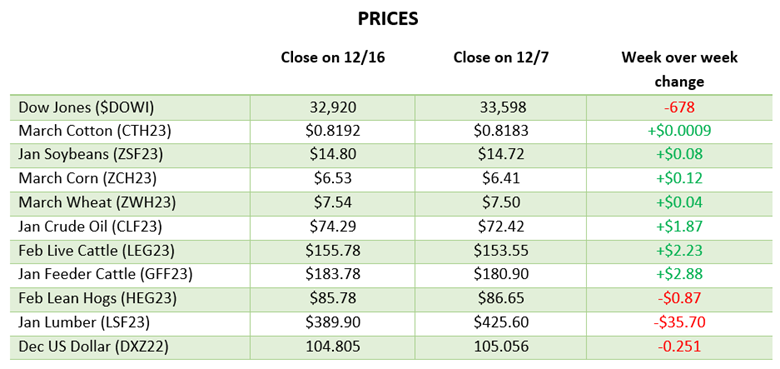

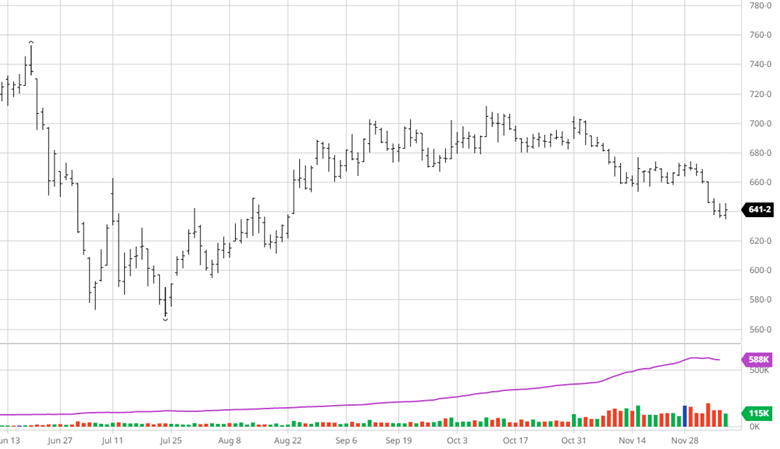

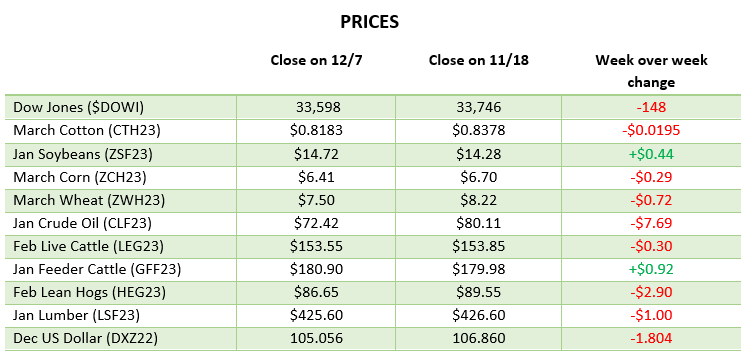

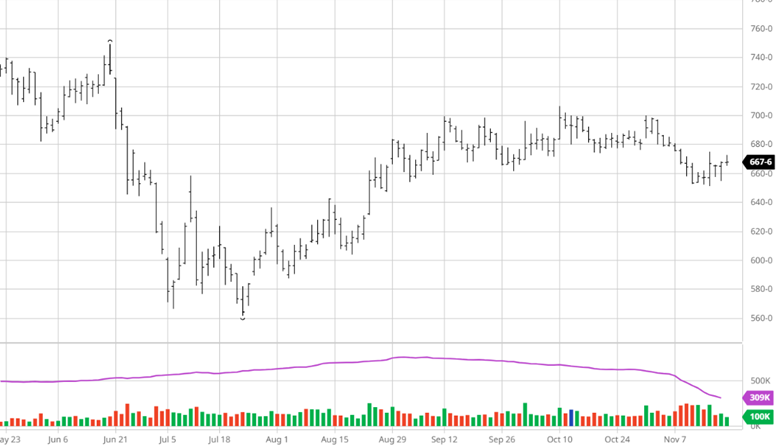

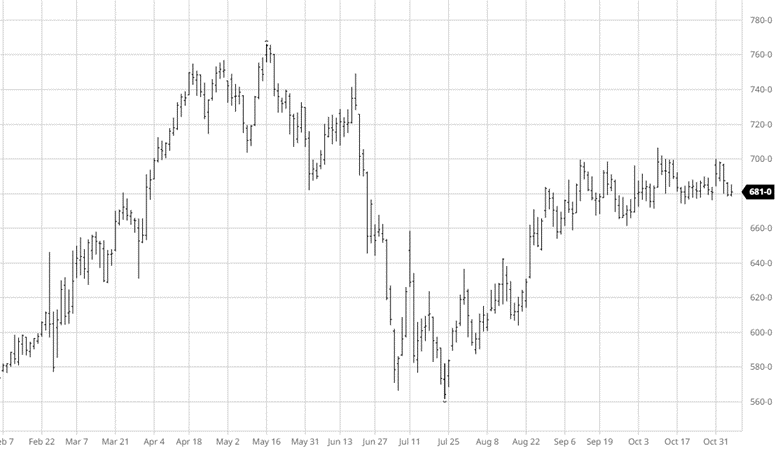

Corn took it on the chin this week as it traded lower to levels last seen in early January. The bulk of the losses came in the second half of this week following the USDA Ag Forum’s bearish numbers. The Ag Forum estimates 91 million acres of corn with a 181.5 bu/ac yield. While these numbers are not surprising as they are mostly just trend line projections the market still reacted in a bearish way as this would raise ending stocks. These numbers also expect neutral external conditions such as weather, politics, etc. While these numbers historically are not the most accurate the market does listen and this was a major bearish factor for the week. They also released their price expectation for the year with December corn being $5.60, this is about 17 cents lower than Friday’s close. February insurance prices for corn sit at $5.95.

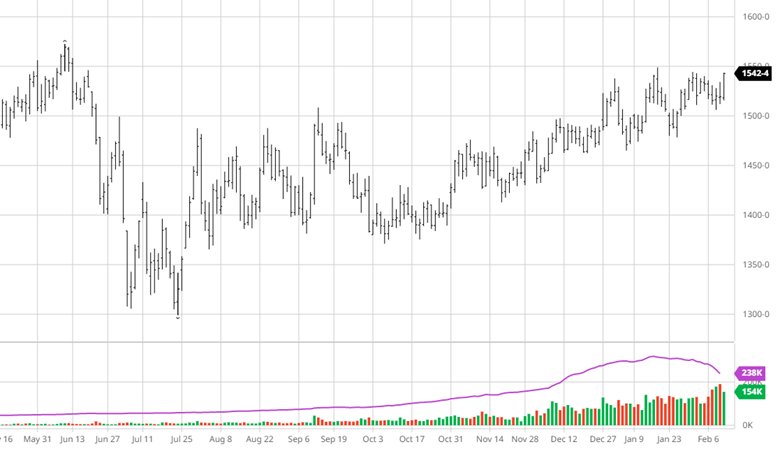

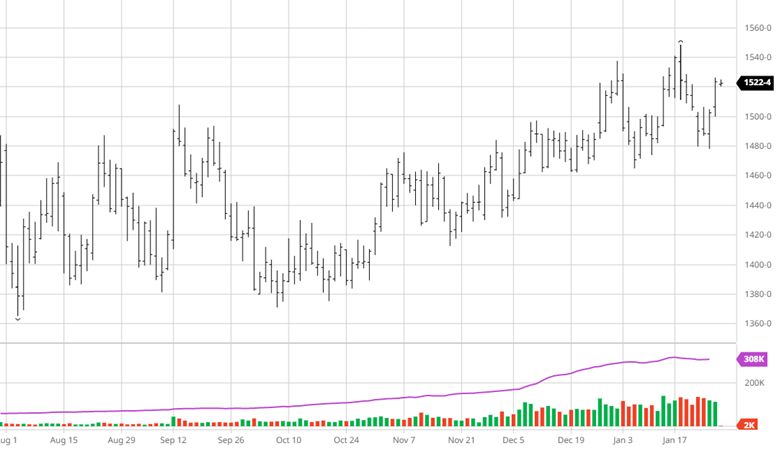

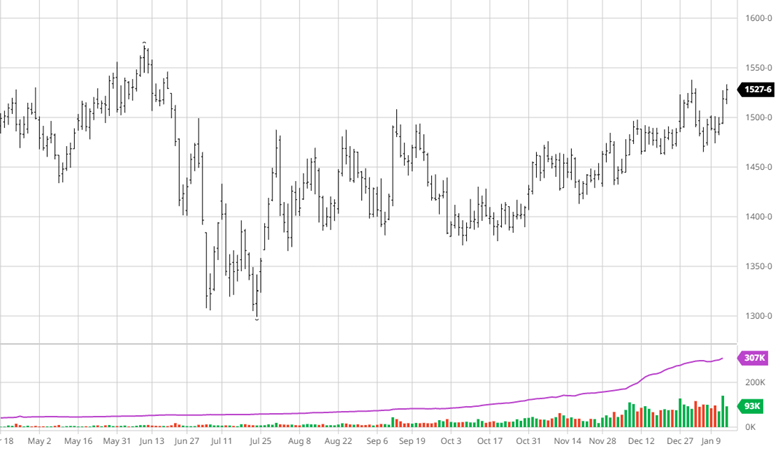

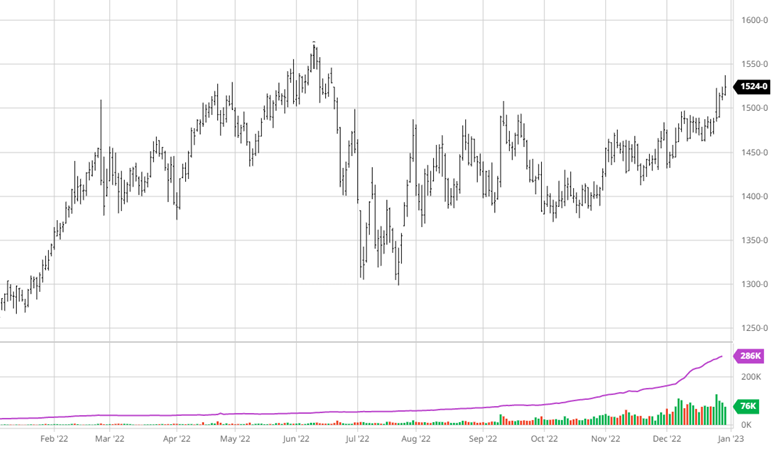

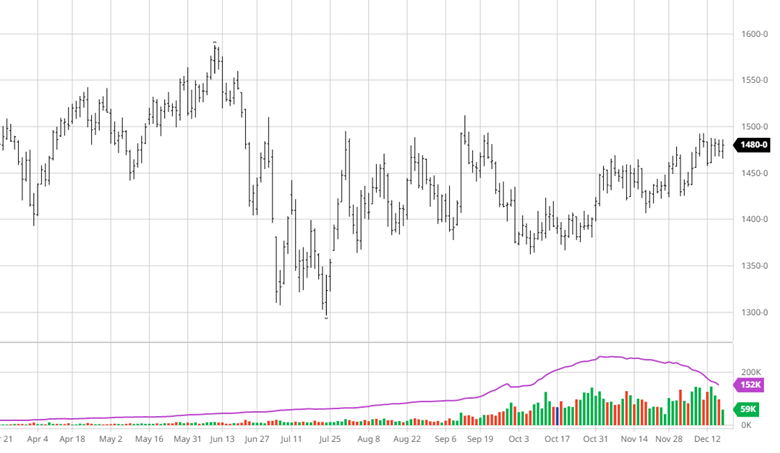

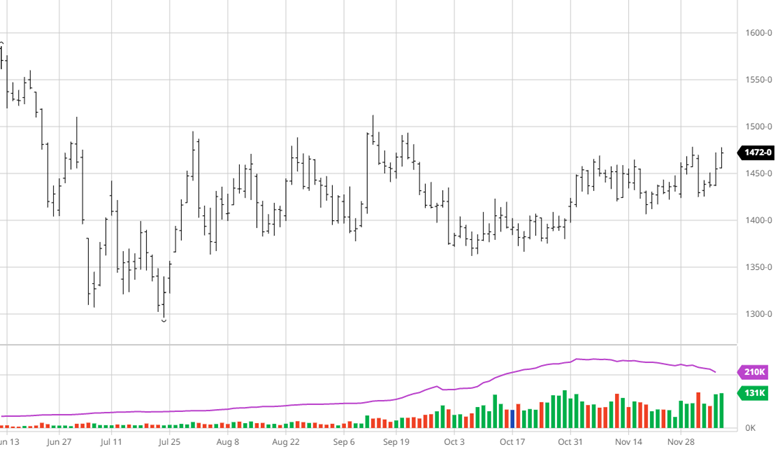

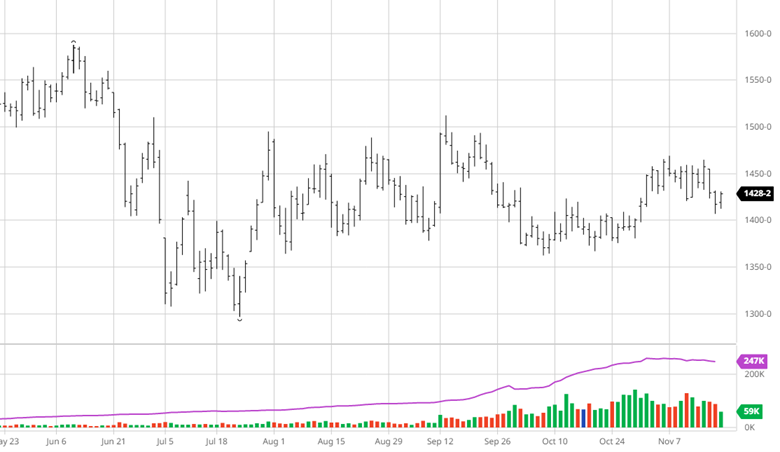

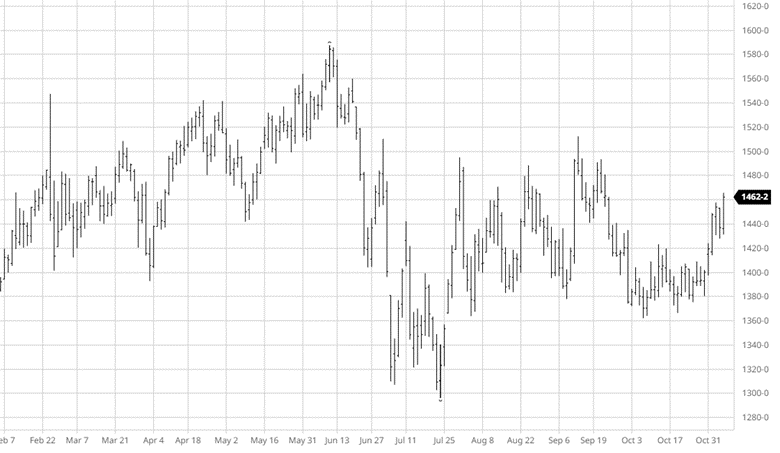

Soybeans moved lower to end the week in sentiment with corn and wheat. The USDA Ag Forum numbers for beans were 87.5 million acres with a yield of 52 bu/ac. These numbers are very realistic and did not send any shock into the market. These numbers would raise stocks by 65 million bushels to 290 mbu which would help alleviate some balance sheet stress. While these numbers were not surprising they did say they expect November bean price of $12.90, so there is room for downward movement in their view. The news that pulled soybeans lower had to do with other commodities as Argentine production estimates continue to fall and Brazil’s harvest is delayed. The insurance average for soybeans is $13.77 for November beans.

Soybeans moved lower to end the week in sentiment with corn and wheat. The USDA Ag Forum numbers for beans were 87.5 million acres with a yield of 52 bu/ac. These numbers are very realistic and did not send any shock into the market. These numbers would raise stocks by 65 million bushels to 290 mbu which would help alleviate some balance sheet stress. While these numbers were not surprising they did say they expect November bean price of $12.90, so there is room for downward movement in their view. The news that pulled soybeans lower had to do with other commodities as Argentine production estimates continue to fall and Brazil’s harvest is delayed. The insurance average for soybeans is $13.77 for November beans.

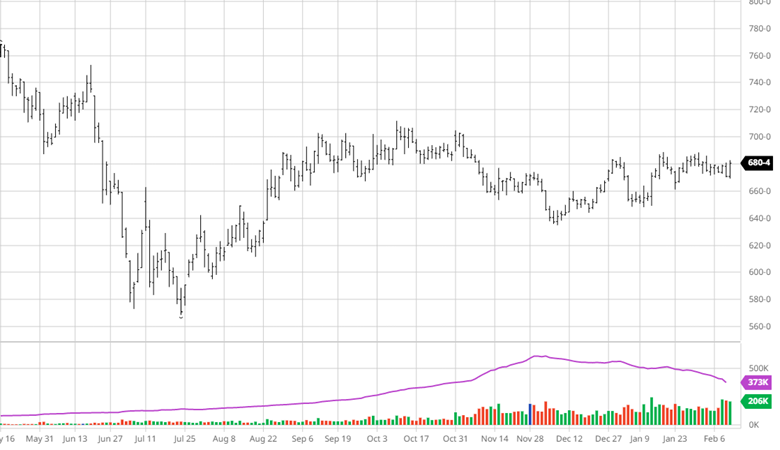

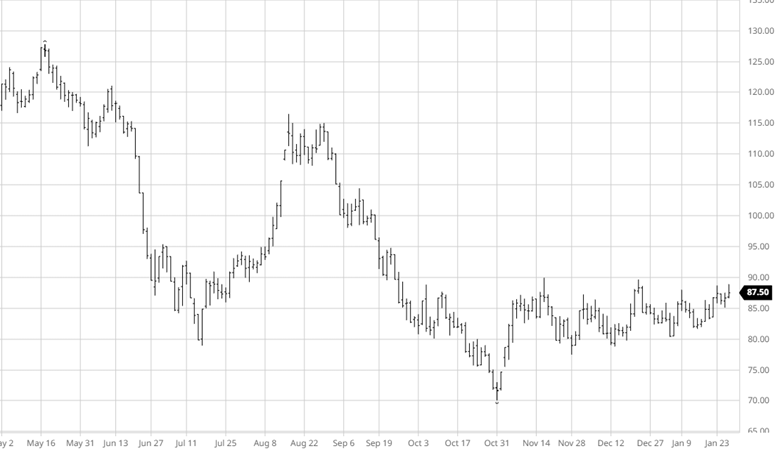

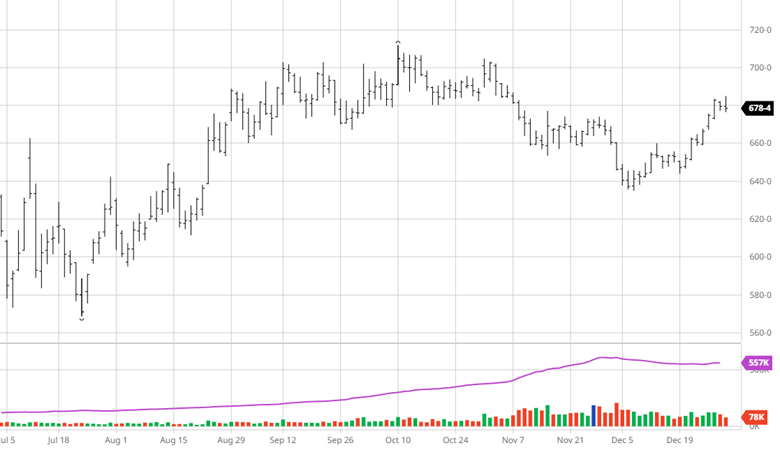

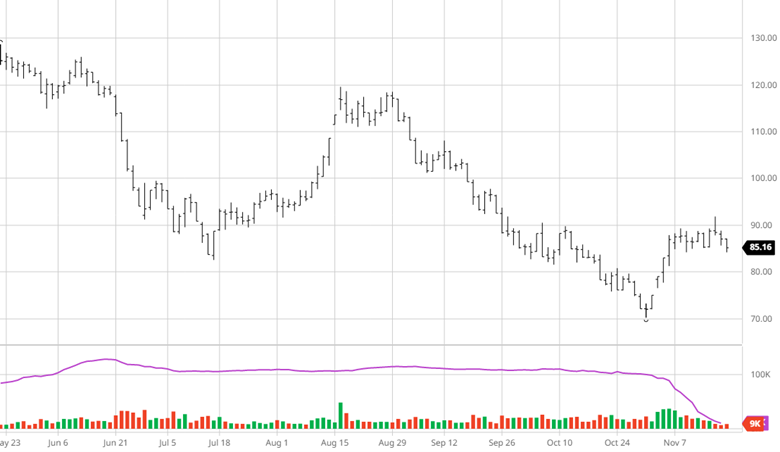

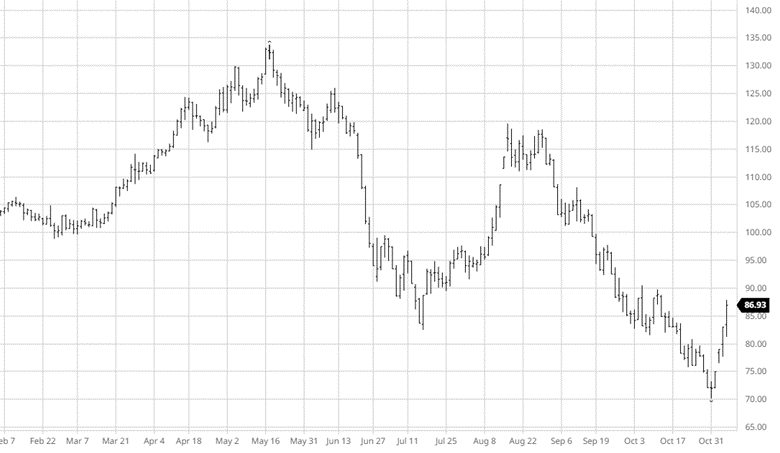

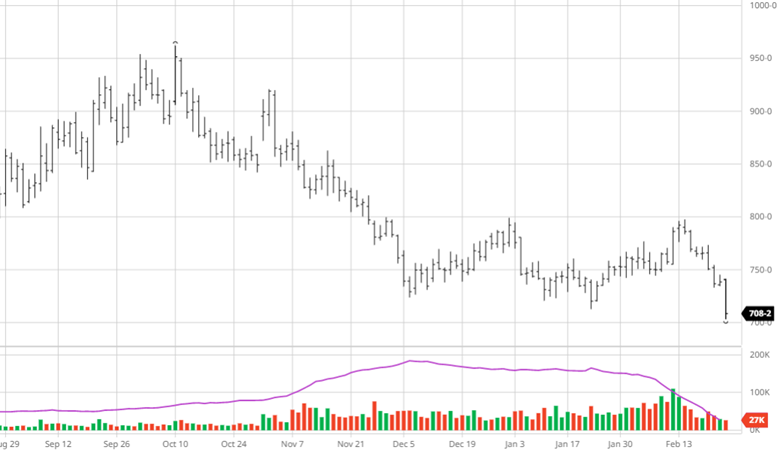

Wheat has struggled the last two weeks after pushing up against the $8.00 mark before falling all the way to $7.08 to end the week. Wheat has moved lower as Russia is selling their wheat the cheapest of anyone, with Egypt purchasing 240,000 tonnes this week. Russia selling their wheat cheaper to gain market share and get money to continue to fund their war on Ukraine. Funds were also sellers this week on the news as they expect Russia to get business as long as countries are saving money. The Ag Forum released estimates for wheat of 49.5 million acres and a trend yield of 49.2 bu/ac. This news combined with Russia were bearish but with first notice day approaches we could see calmer trade than the past few days soon.

Cotton

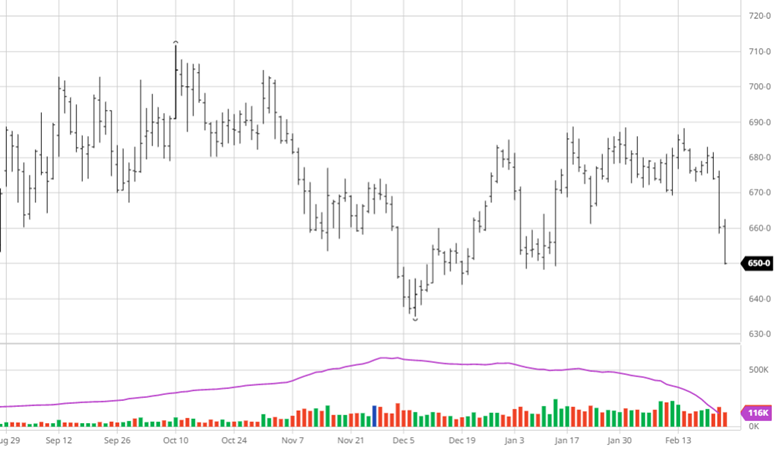

The cotton story has not changed much as the supply/demand story has not changed. There is both a lack of demand and a supply surplus here in the US, which has led to less imports of cotton goods. With the potential recession looming the lack of current demand mixed with that does not paint a great picture for cotton as it continues to trade on the lower end of its recent range.

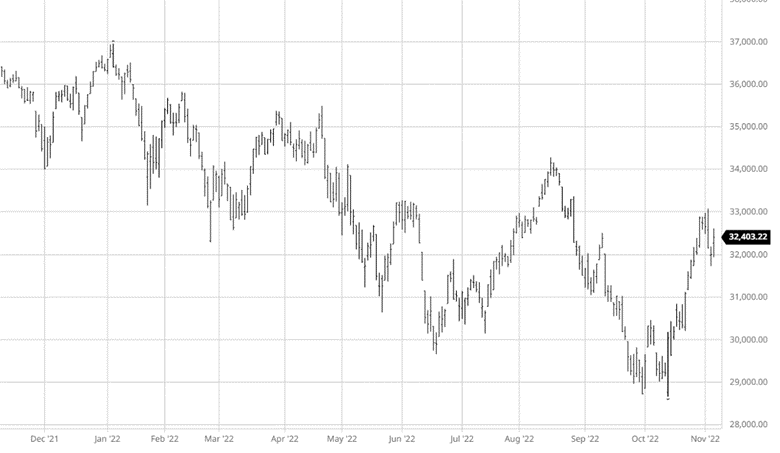

Equity Markets

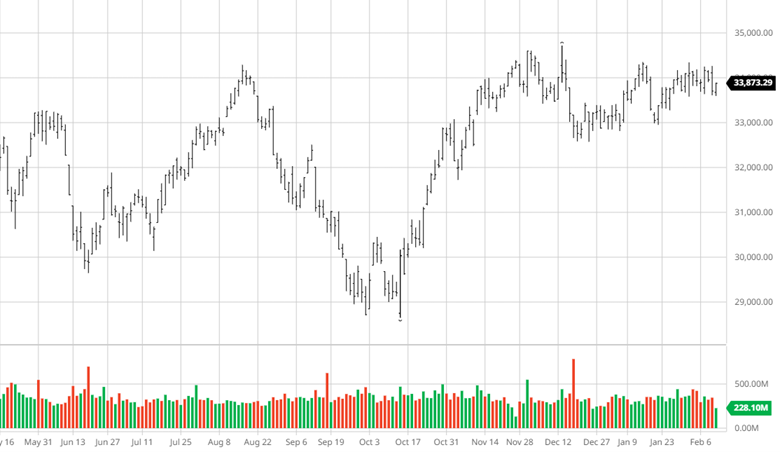

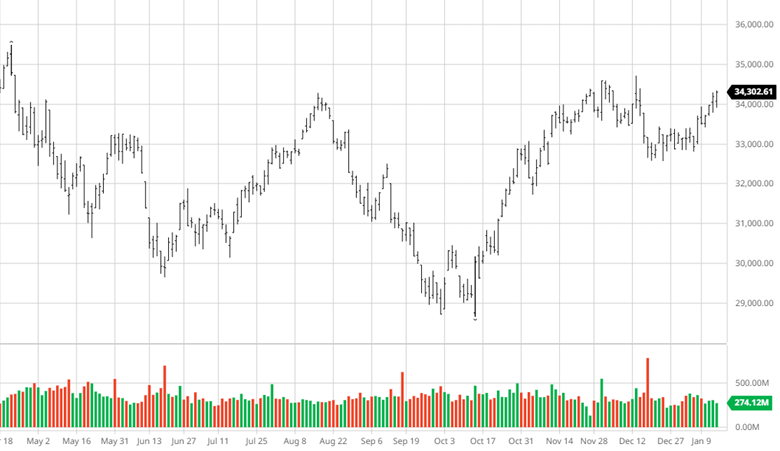

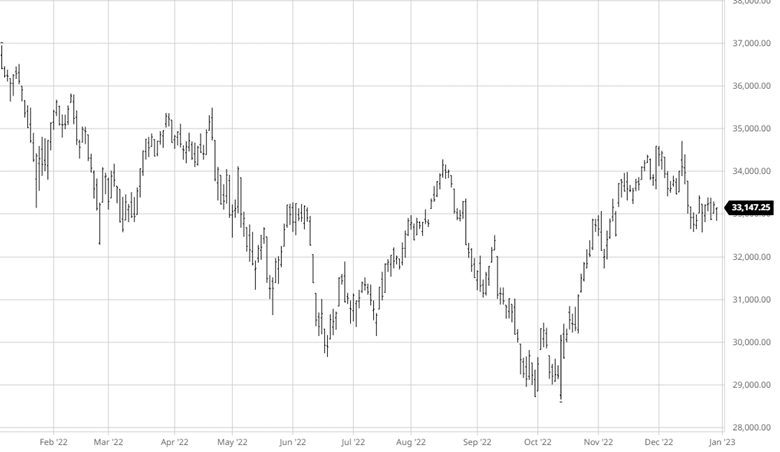

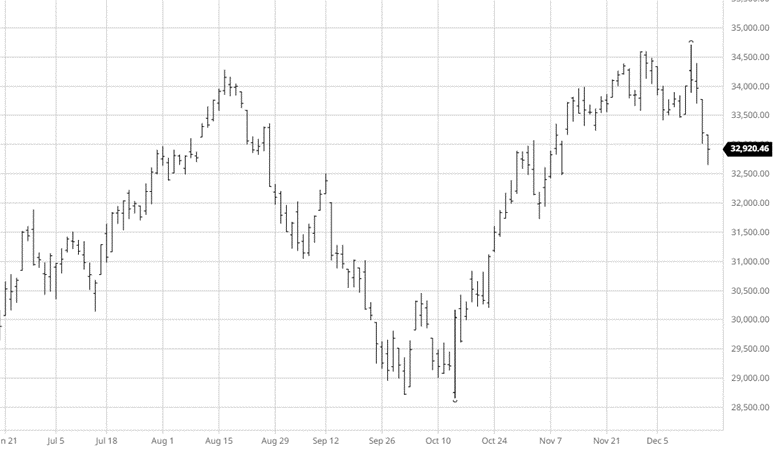

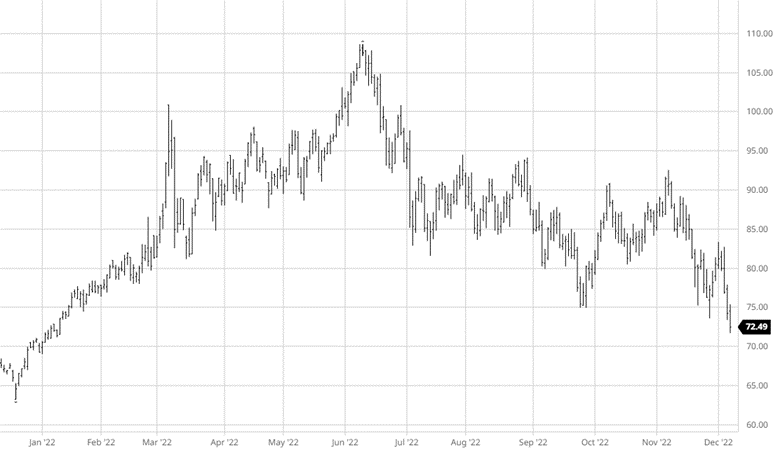

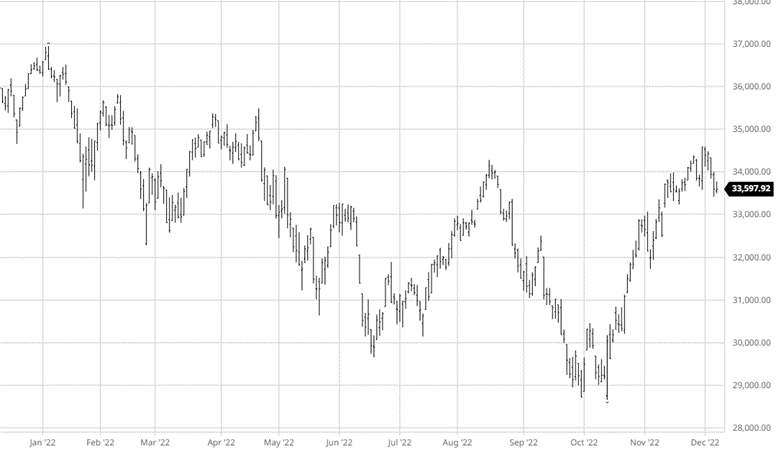

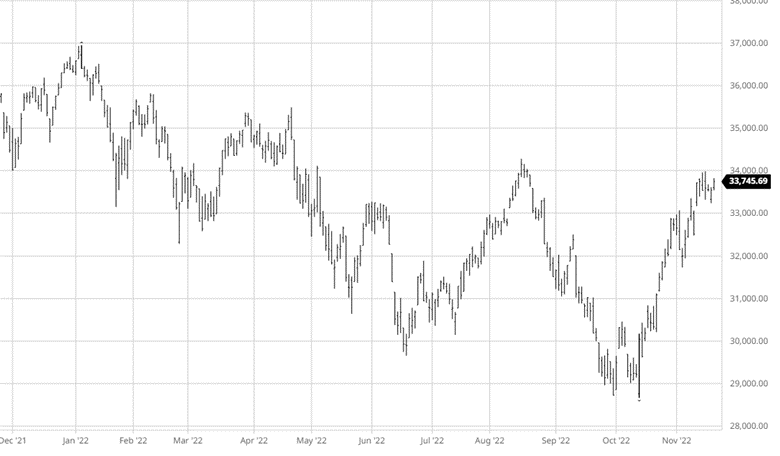

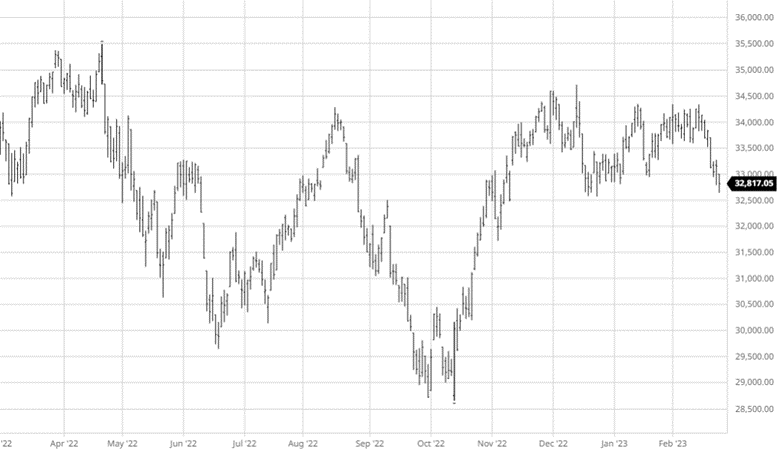

Equity Markets were down this week as economic data keeps coming in supporting higher rates. Inflation is sticking around and earnings are mixed as February will post big losses across the major indexes. Many market commentors still believe we are heading lower from several different factors including the Fed, inflation, layoffs, valuations and more. Continue to keep an eye on the strengthening USD.

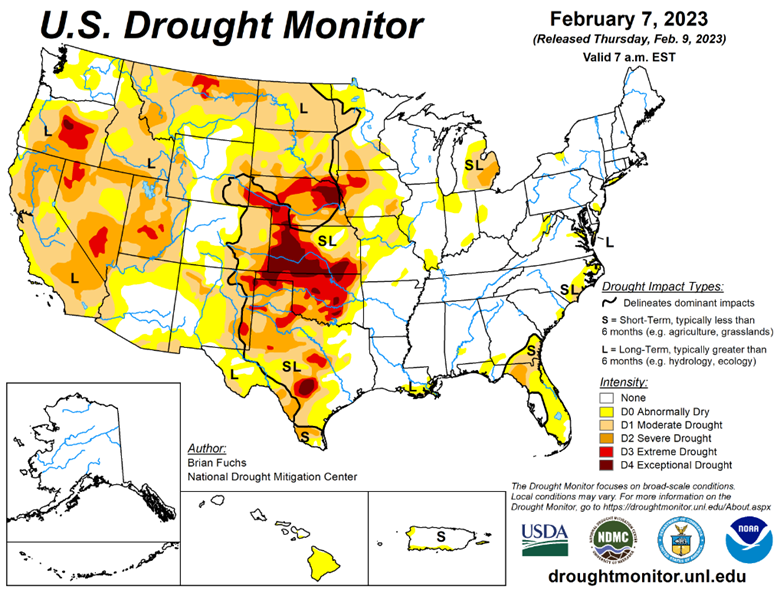

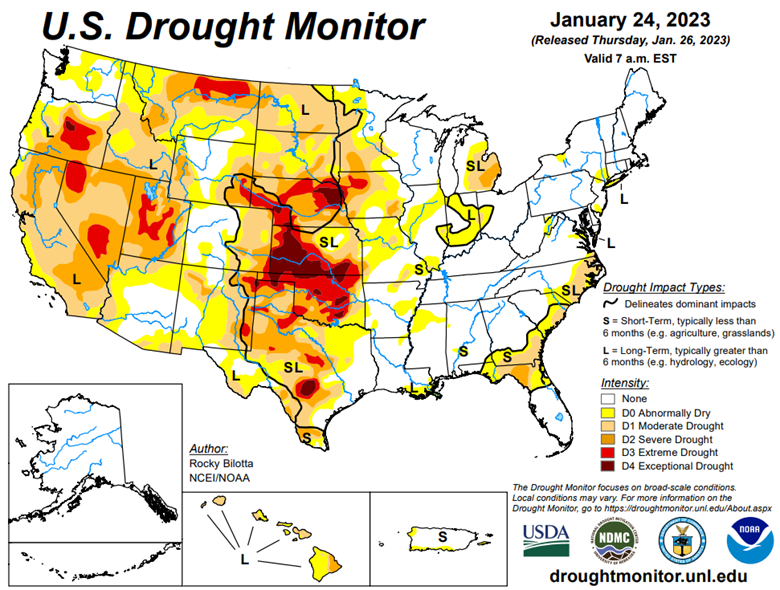

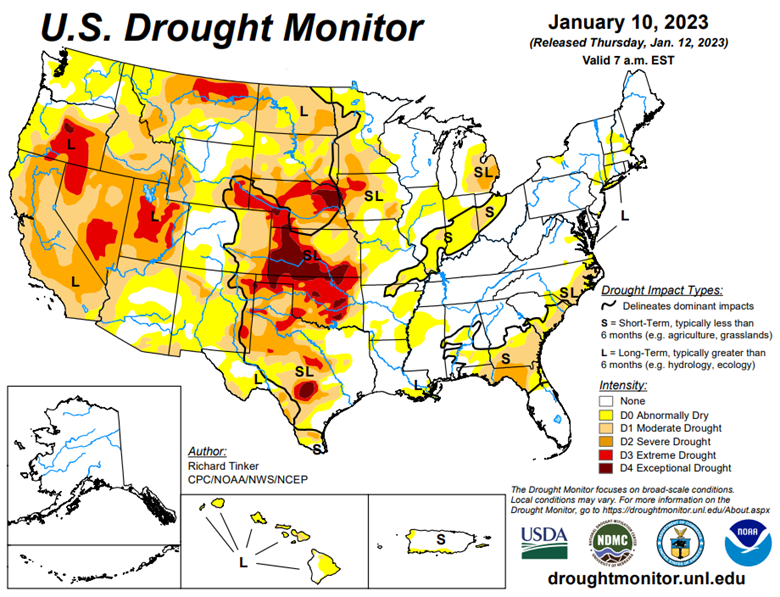

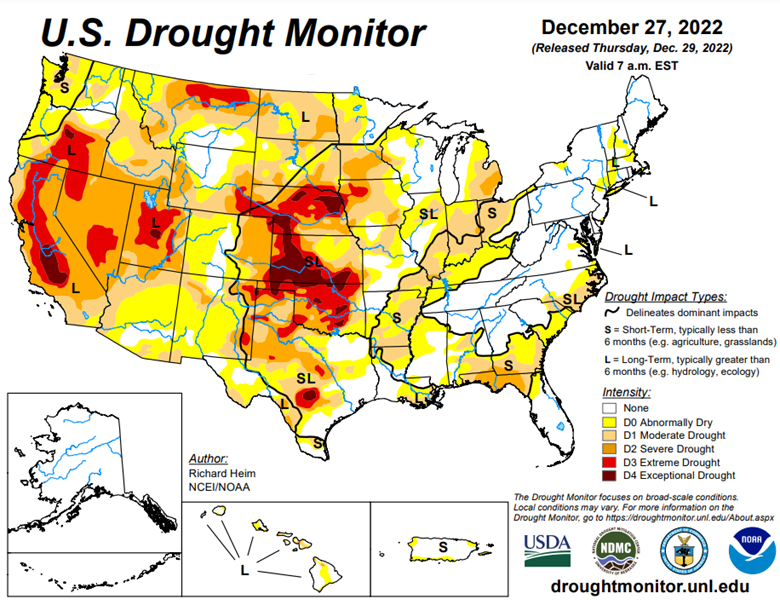

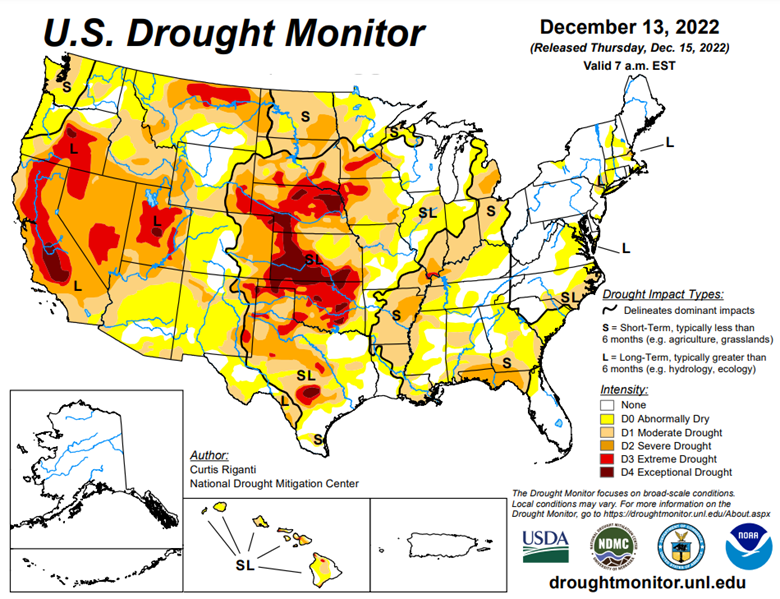

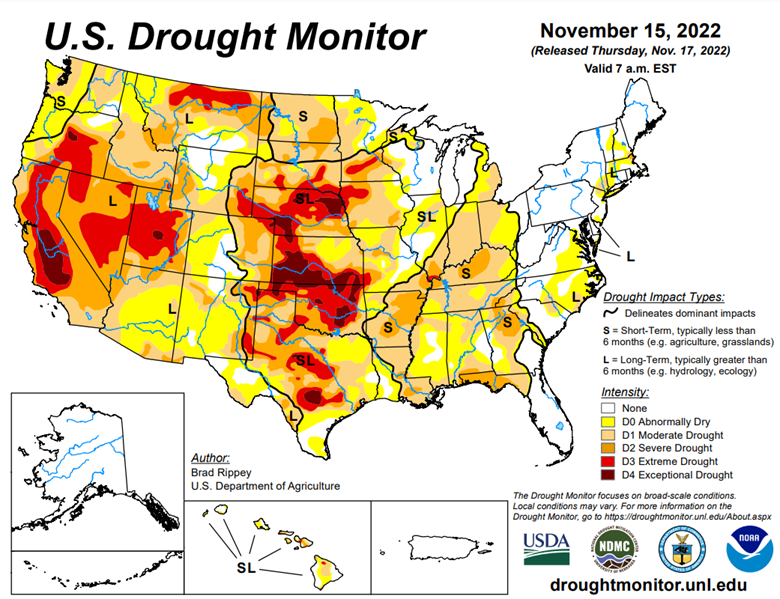

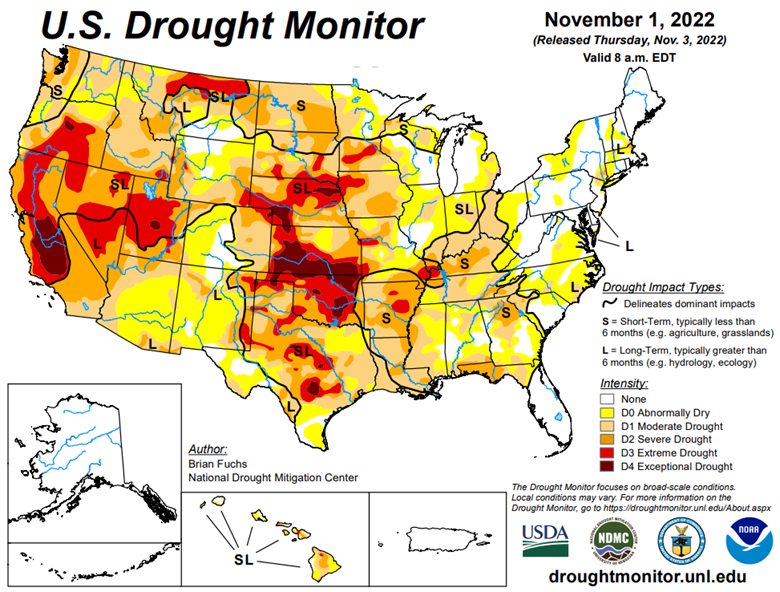

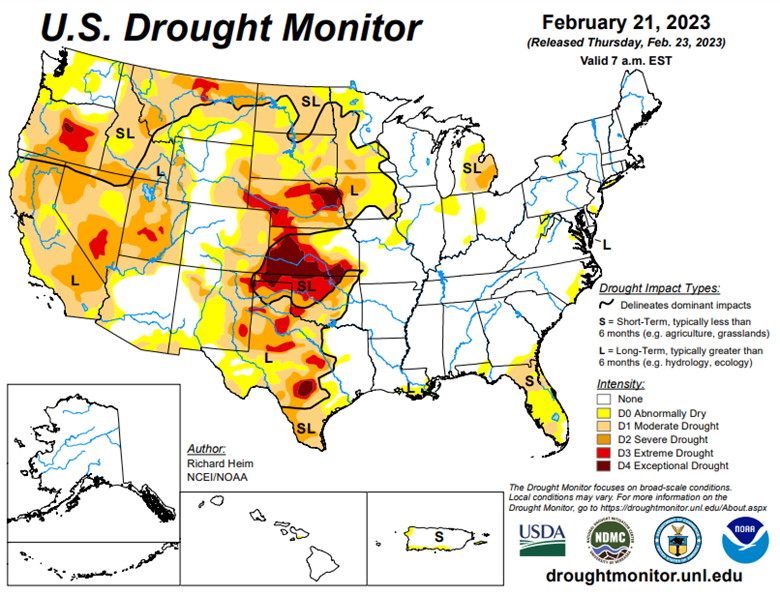

Drought Monitor

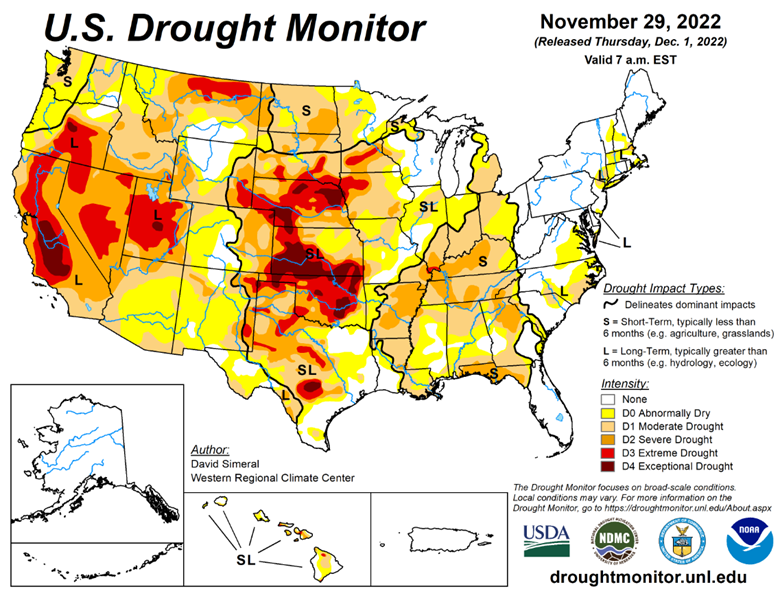

Eastern corn belt has gotten plenty of moisture so far this winter with the western corn belt needing more heading into the spring.

Podcast

With every new year, there are new opportunities, and there’s no better time to dive deeply into the stock market and tax-saving strategies for 2023 than now. In our latest episode of the Hedged Edge, we’re joined by Tim Webb, Chief Investment Officer and Managing Partner from our sister company, RCM Wealth Advisors. Tim is no stranger to advising institutions and agribusinesses where he has been implementing no-nonsense financial planning strategies and market investment disciplines to help Clients build and maintain wealth and reach financial goals since

Inside this jam-packed session, we’re taking a break from commodities, and talking about the world of equities, interest rates, tax savings, and business planning strategies. Plus, Jeff and Tim delve into a variety of topics like:

- The current state of the markets within the wealth management industry

- Is there a beacon of hope, or is it all doom and gloom for the markets?

- Other strategies to think about outside of the stock market and so much more!

Via Barchart.com

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.