Commentary:

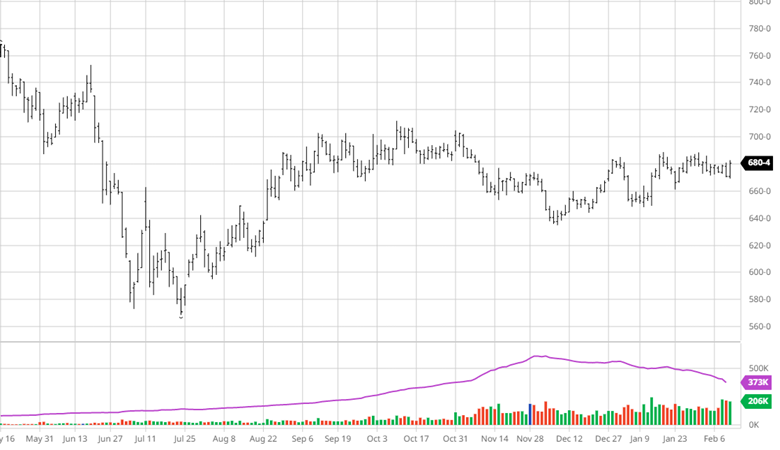

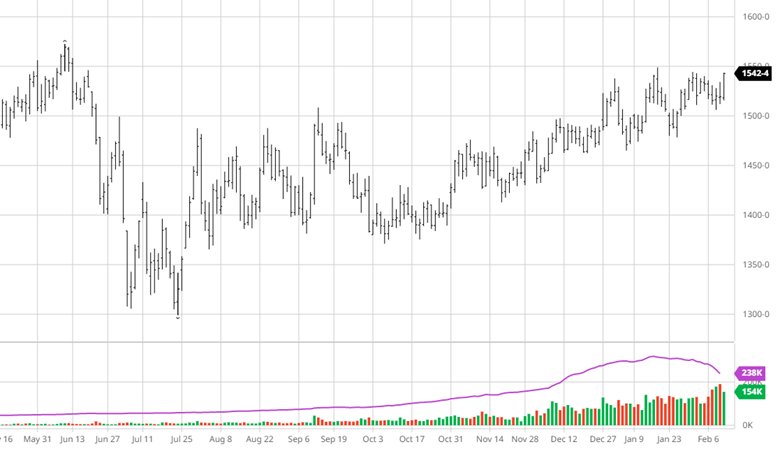

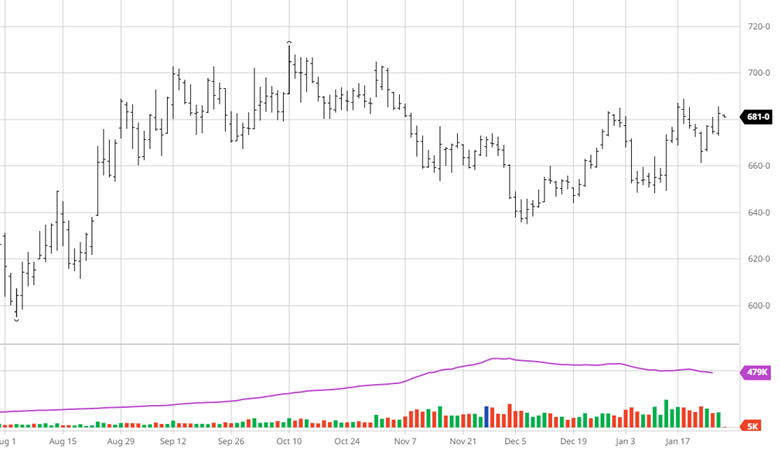

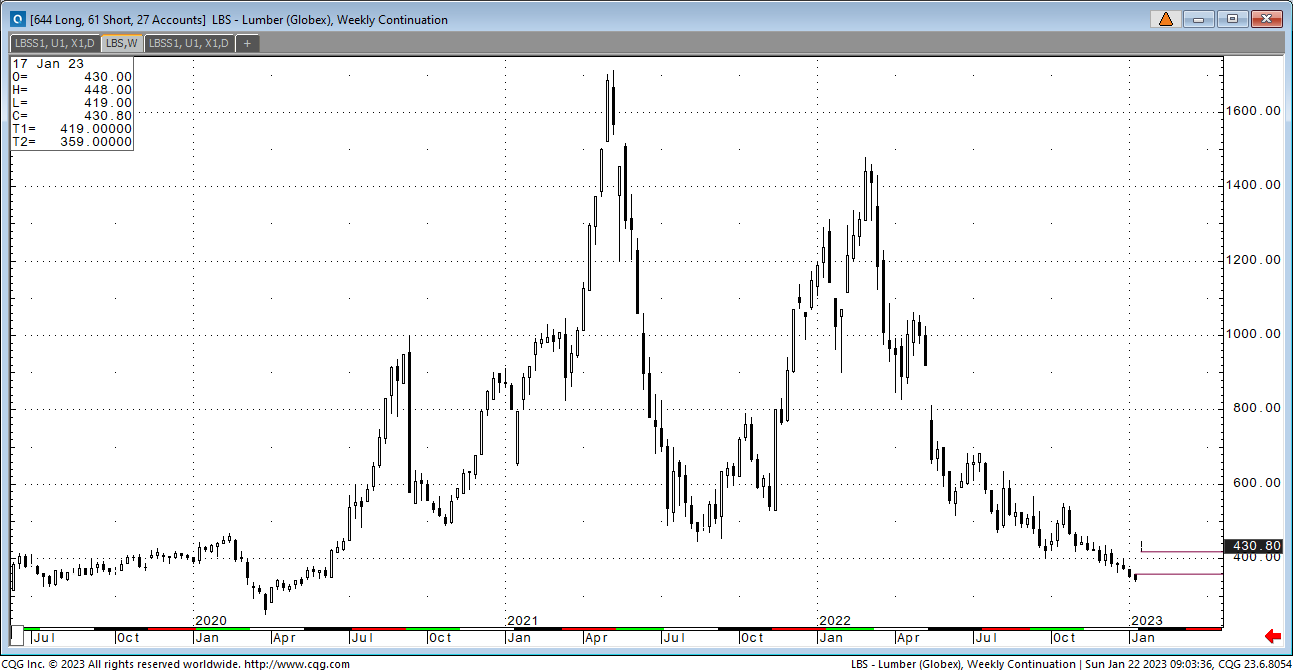

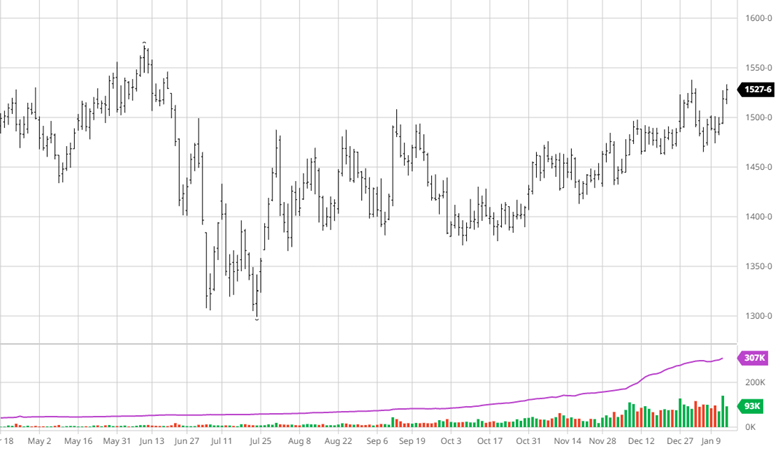

There is still too much wood out there. This week the euro traders had to not only deal with a soft market but also with the basis wood getting cheaper daily. Add to the mix that every Friday those with contract wood start off in the negative and you get this extreme malaise. With the amount of construction going on out there the market is either telling us the slowdown will be drastic or we are undervalued. Neither will be answered anytime soon so for today the market is the true indicator. Futures are on day 13 of this sell off. The rally lasted 16 days so the market could be close to bottoming. The resiliency of futures the last few days in light of all the algo selling pressure tells me it is close. What the bounce will look like is anyone’s guess, but the conditions are for a better grind higher market into the spring and not a spike up from the low. So, prepare for the spike and how for the grind.

Economic:

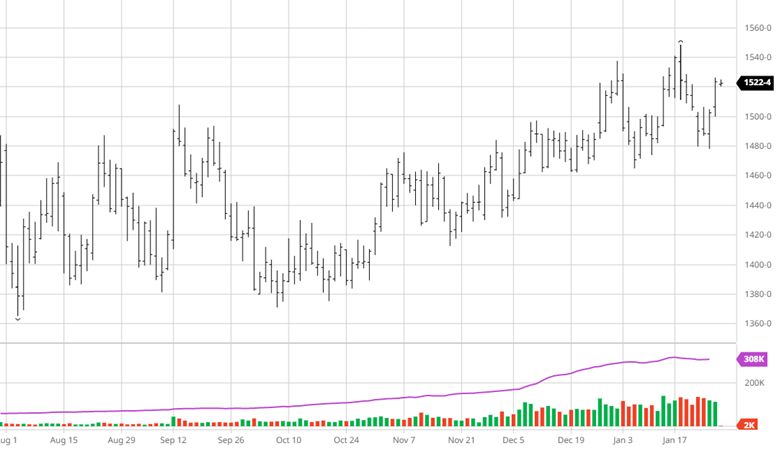

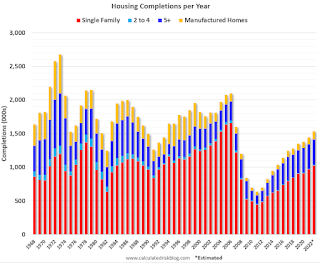

The housing starts report this week added to the confusion already lingering throughout the industry. Today multifamily units under construction are at the highest level since 1973. Combined single and multifamily there are 1.7 million units under construction. That number bumps up against the record. These are seasonally adjusted numbers. That said, there is near record construction going on with a third of the country dormant because of winter. When digging down into the numbers one must wonder with construction at this pace are we really under built? Rents are sticky, so I would expect that pace to remain in place while single families continue to fall off. The construction dynamics bare some resemblance to the housing market in 2004-2005. That is when the housing bubble burst. The housing sector was in a bear market well before the 2009 economic meltdown. The pace of today’s construction will lead to an overbuilt industry at some point. In a year from now we will not have 1.7 million units under construction. Now let us add to the confusion. The fact is today there are 1.7 million units under construction and that makes $382 way too cheap.

Technical:

March futures objective is for the January settlement of $344. The gap will be closed at $359.00 but the market is searching for value and that is the last expiration. The fact that the market is headed back to that area is troubling long-term. It indicates that $344 wasn’t a onetime fluke. It was considered a value the first time down and now is the area of rebuilding. The next rally up may just have to correct back again to this area. Momentum is oversold and a correction is coming but the market is not stair stepping higher yet. My only hope is that it isn’t a continuation of the stair stepping lower mode. In any case these are good levels to own wood going into the spring.

Below are the option links to the new contract. Please take a look at the quote page for options.

Calendar Page: https://www.cmegroup.com/markets/agriculture/lumber-and-softs/lumber.calendar.options.html#optionProductId=10192

CFTC Commitment of Traders report still delayed!!

NEW CONTRACT:

Lumber Futures Volume & Open Interest

CFTC Commitments of Traders Long Report

https://www.cftc.gov/dea/futures/other_lf.htm

Lumber & Wood Pulp Options

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636