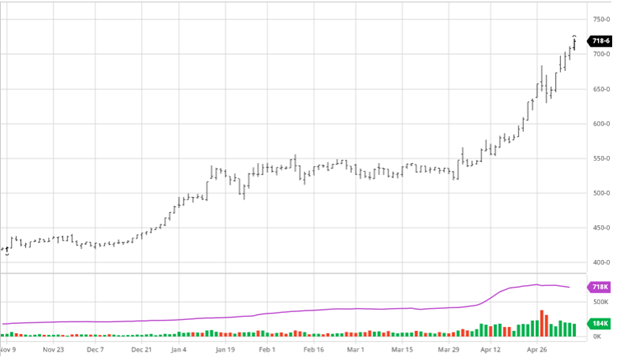

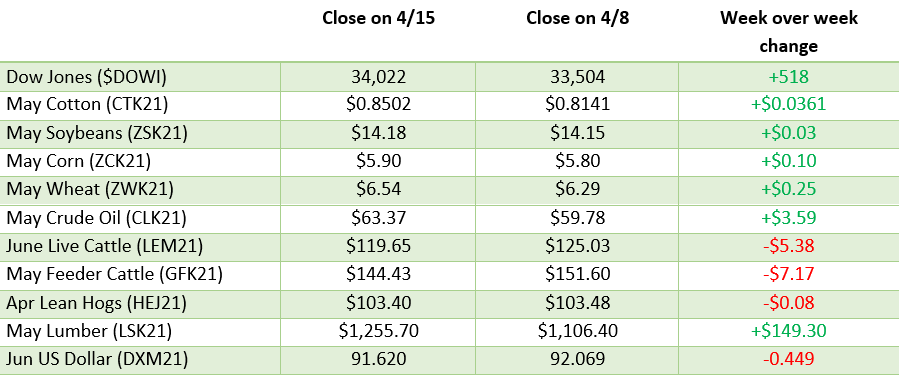

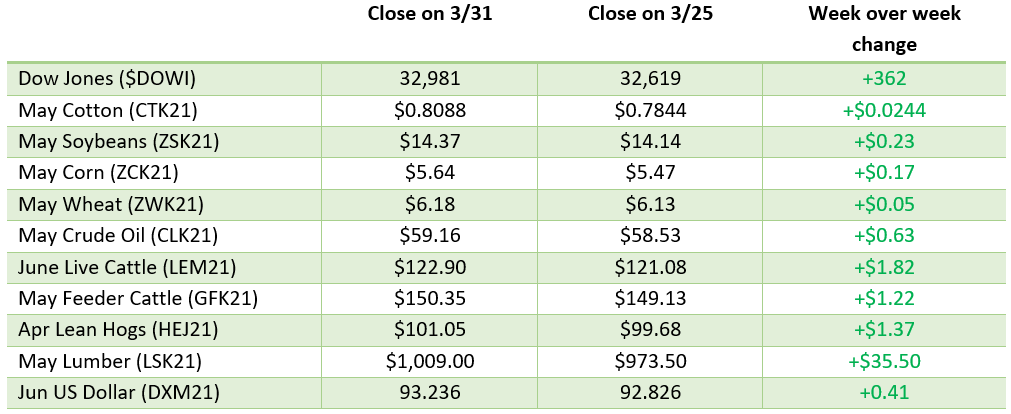

Corn finally had a day with a major pullback as it tested the new expanded limits on Thursday. This move comes after a slightly bearish crop report along with a lackluster trade following it. After the impressive run to this point it makes sense why speculators would take profits and hedgers would begin to manage their risk for this year as we begin to get better picture from the planting starts data. For the bulls, much of Brazil’s safrinha crop will go another 10-14 days without rain continuing to stress the crop. This week the US’ corn crop was seen as being 67% planted with more progress being made thanks to favorable weather. How the week finishes will be important for the bulls and bears to keep momentum on their side. In this week’s USDA report the 21/22 US ending stocks came in at 1.507 billion bushels (estimates were around 1.36 billion) and world 21/22 ending stocks at 292.3 million metric tons. The USDA and WASDE think demand rationing is coming as it cut US exports and increased ending stocks despite a record export and shipping pace.

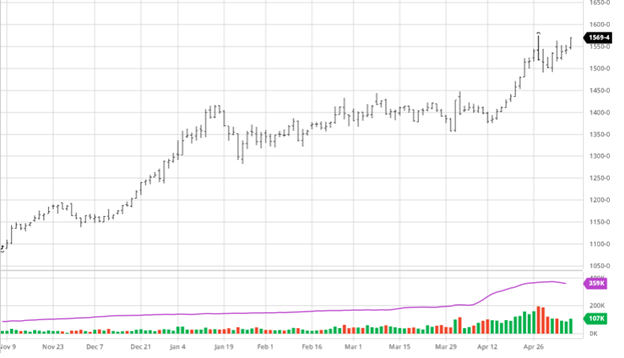

Soybeans, despite the big losses suffered on Thursday, finished the week above where they were last week. Beans were down over 80 cents at one point during trading on Thursday before large end user demand rallied prices 30 cents of the lows to show some support. We knew that expanding the daily limits would allow for more volatility but that does not make what has happened this week any easier to get comfortable with. In this week’s USDA report the 21/22 US ending stocks came in at 140 million bushels, slightly above estimates, with world ending stocks coming in at 91.1 million metric tonnes. The 20/21 US bean stocks were 120 million bushels, by starting at 140 million bushels there is not much room for error to be adjusted down without being tight on ending stocks. To finish at these levels export cuts are expected to come in.

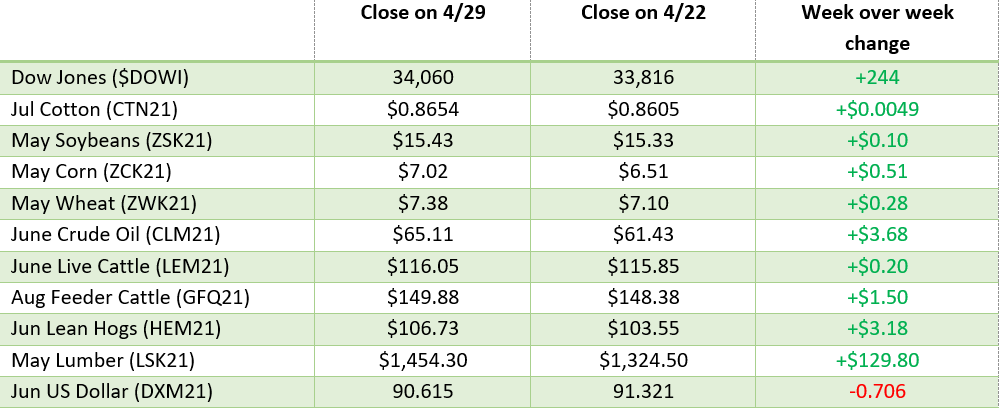

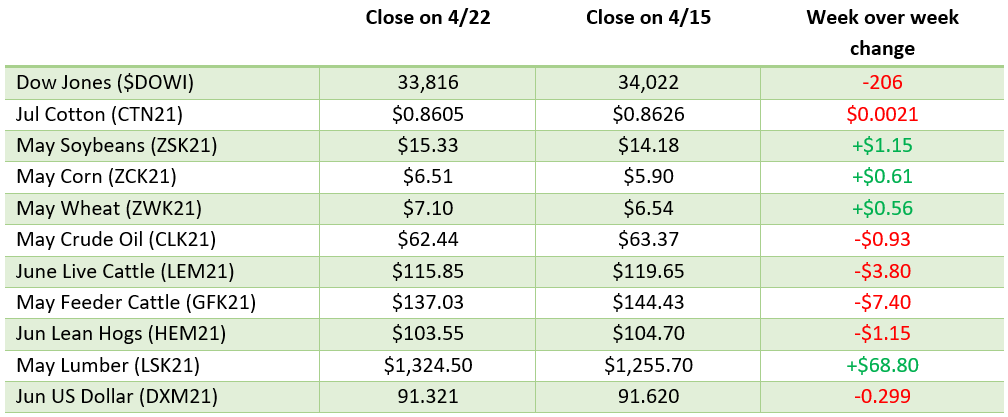

Dow Jones

The Dow was down on the week along with other major averages as a correction has hit the market this week. The Nasdaq, S&P 500, and Russell 2000 were all down along with the DOW this week showing widespread market weakness and selling hitting all sectors.

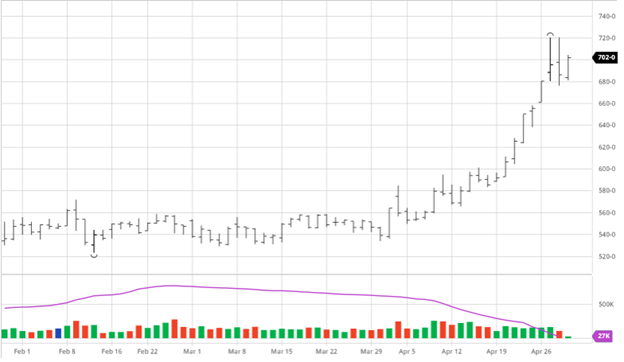

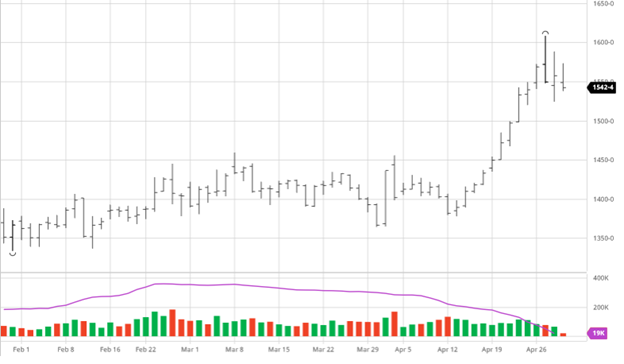

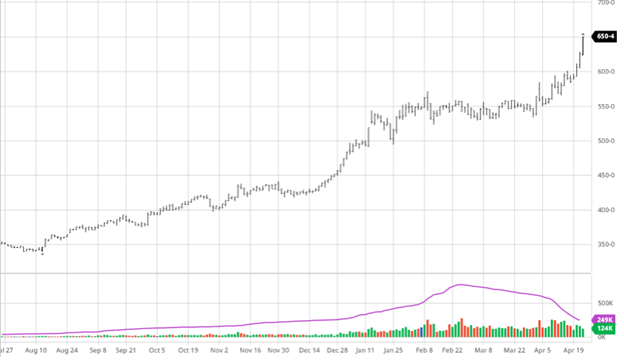

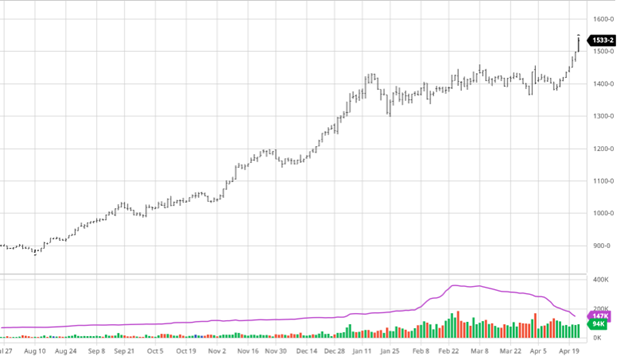

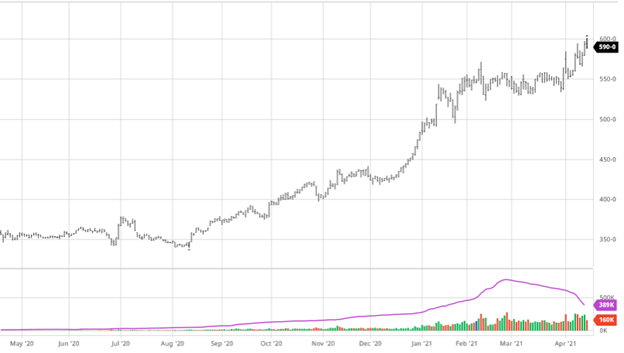

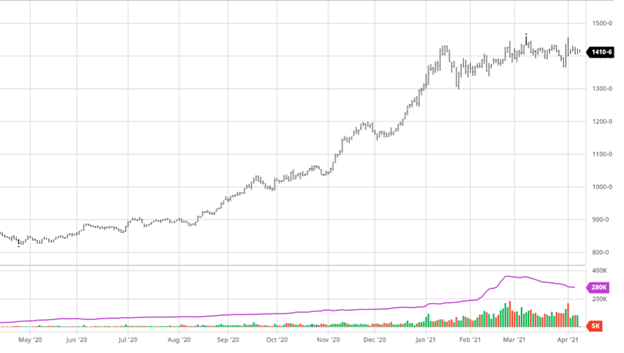

Lumber

Check out our recent post about the lumber market and what all has been going on.

Podcast

Check out our recent podcast with Dr. Greg Willoughby: We’re talking with Greg in the new episode about being a “plant doctor”, weather patterns, GMO & organic produce, crop history, technical advances, level 201 education on agronomy, the agronomy equation, Helena Agri, soil biology, American v European agriculture, Greg’s early background in livestock, and the advancement of native plants to modern produce.

https://rcmagservices.com/the-hedged-edge/

Other News

A major bridge over the Mississippi River in Memphis, TN was shut down this week for traffic both over and under it as a major crack/break in the structure was discovered. This backed up hundreds of barges in the Mississippi with no alternate route until it reopened Friday morning.

The CDC announced this week that vaccinated Americans can go about most activities without having to wear a mask or social distance in a welcome announcement for people who have been wanting to get back out and about like normal times.

The Colonial Pipeline hack had many Americans scrambling desperately to fill up their cars and spare tanks, because if there is one thing Americans are great at it is over reacting. The hack caused a disruption in the distribution to many states but was opened back up after only a couple days but the shortages will persist for a little bit of time in some areas.

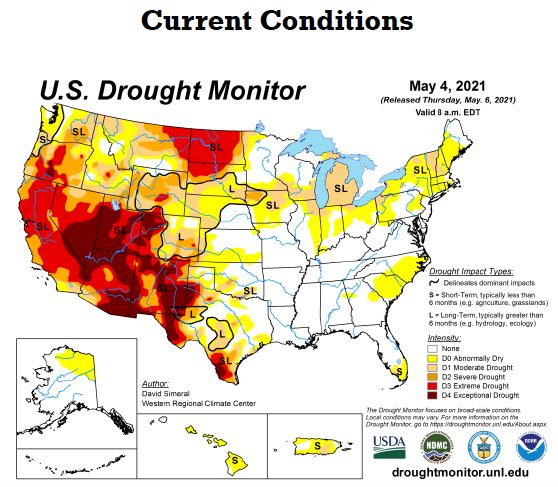

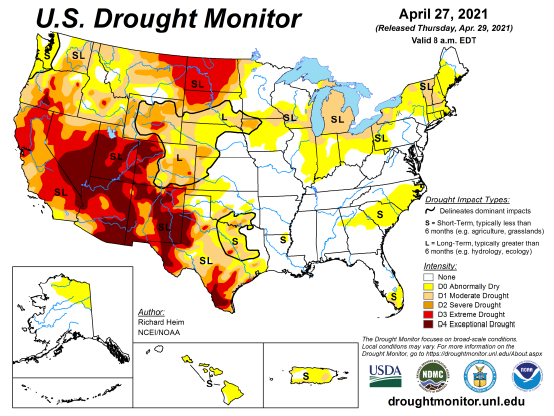

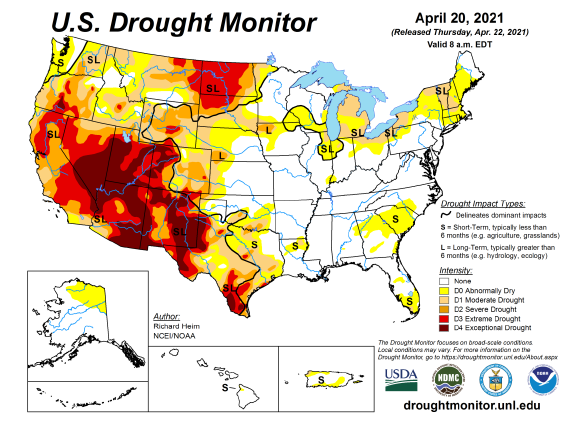

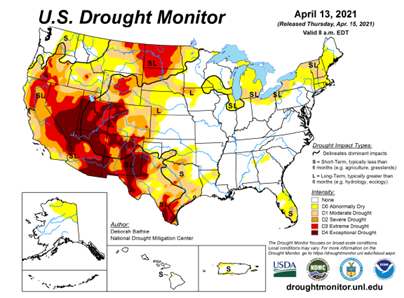

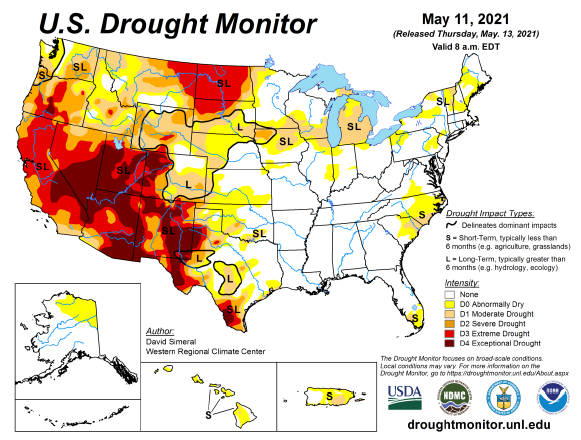

US Drought Monitor

The map below shows this week’s drought conditions across the US. Some areas have gotten rain this week that will help relieve some of the areas highlighted below.

Via Barchart.com