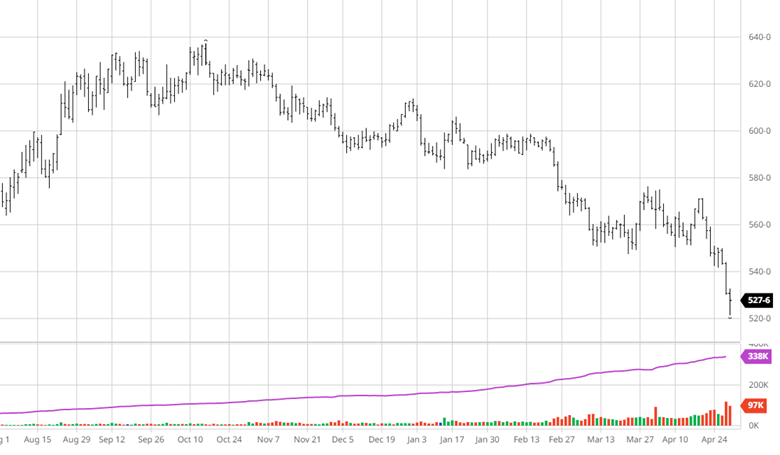

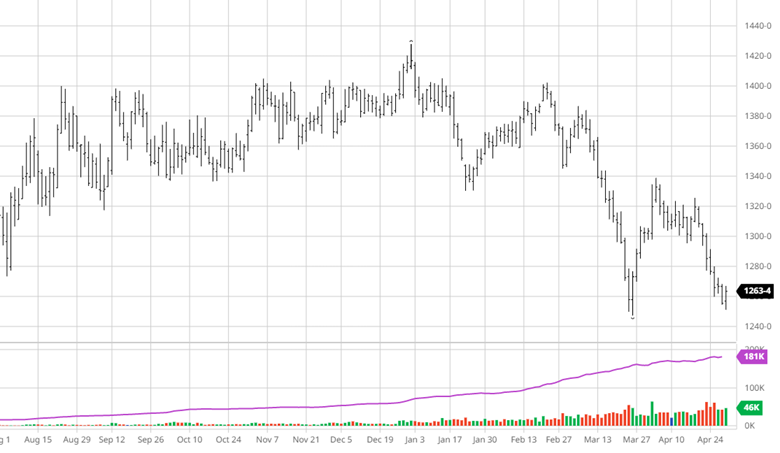

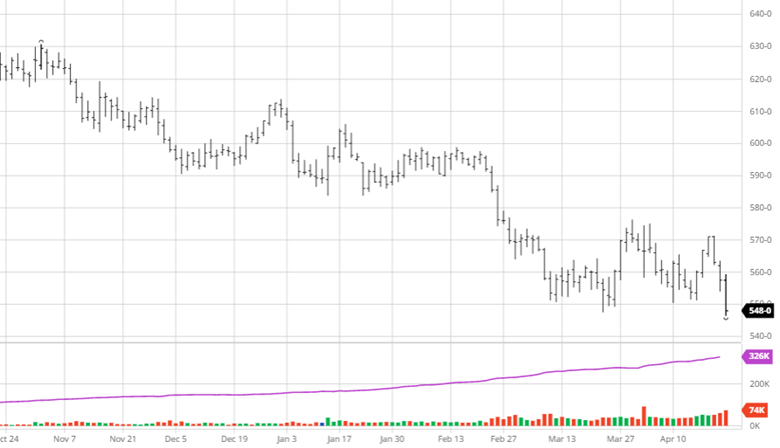

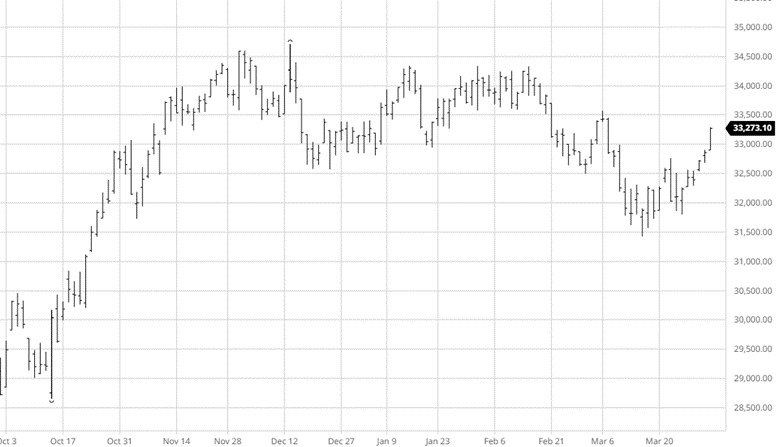

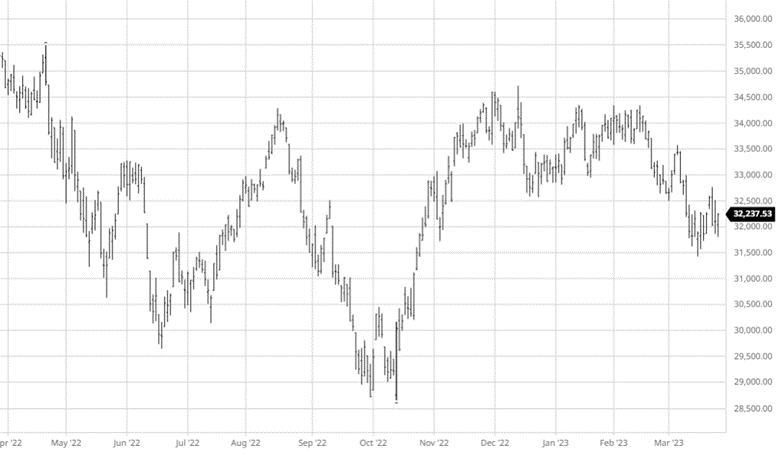

All markets, regardless if it is a commodity or equity, will telegraph a change in their trend. The lumber market is one of the easiest markets to predict. It only takes 10 or 12 missteps before you are right. In the few months of 2023, we have gone from expecting a sideways give-it-back market to looking for a recession, and finally, it getting positive. We are now back to the sideways thought process as an industry. The key facts are that the housing sector didn’t get as bad as we thought, but that better-than-expected business didn’t help prices. The demand has not cleaned up the excess supply. May 1st. looks much different than we had thought back on January 1st. or does it?

Are the wholesalers feeding on their young? Yes. Are the buyers locking in jobs at $700 and beating up distribution for another $30? Yes. Is it true that all euro wholesalers can only go out after dark? Yes. We are where we expected to be at this point. The problems on the supply side are working themselves out. It is just looming micro issues now. These micro-dynamic issues should not control pricing, but in this small industry, they do. The industry’s macro dynamics do not look bad. They are just very slow-moving. The macro issue of logs. The macro issue of reduced production, no infrastructure replacement, and the macro issue of costs are all factors that determine the price on a timeline never defined. All we have is Elliot Wave to help.

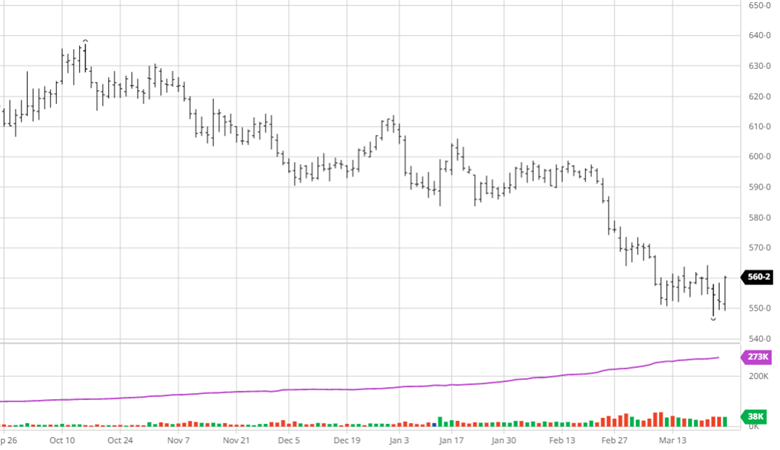

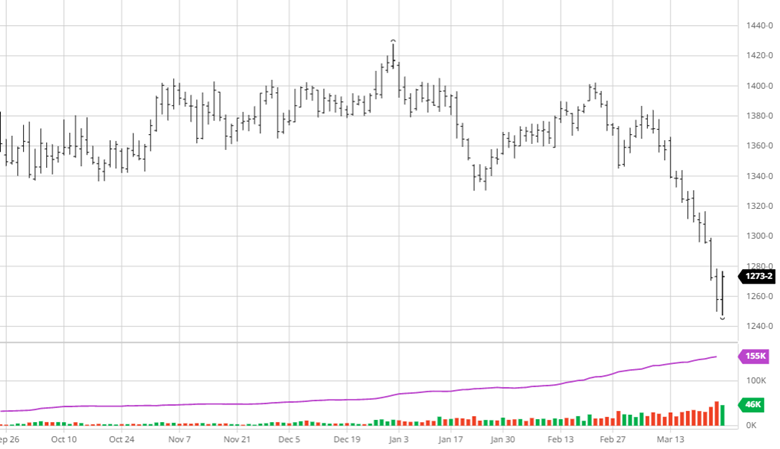

The main technical read today is the long-term Elliot Wave. The pattern consists of a 1 down in August of 2021, a 2 up in August of 2022, and now a wave 3 down which has not been defined yet. I’m confirming that completion is somewhere between here and May 15th. for 2 reasons. First is that we tend to make our new lows somewhere around expiration and the fact that the next expiration is a delivered price. We need to put an asterisk next to Wave 3 as it might be artificial. I’m not recommending buying July because Wave 3 is in, just defining a bottom.

There have been two very successful strategies for the first 4 months of the year. The first is straight out of futures 101, the basis trade. No one wanted to waste their time making $20 on a basis trade. Today those same naysayers are hoping they don’t lose $20. If you did the basis in LBK rolled it to LBRK and then to July you picked up $50 of basis. Really…. The other success has been the strategy that is older than dirt. Counter those with wood in a falling market and counter them aggressively. There is a rhythm to this market. We have been in a lower high and lower lows cycle that could be shifting to flat highs and higher lows. That brings the “Don’t be the second guy into the Pool” syndrome back into play again.

The one way a market telegraphs a change is through the news. This industry has gone from reports of shutdowns to extensions of those shutdowns. Today’s news is about how many guys showed up late for work. The Beaks of the world are telling us that more of the same is in front of us.

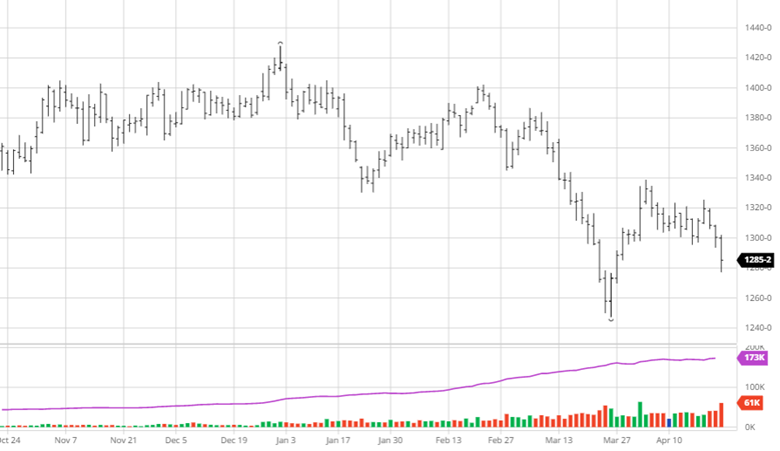

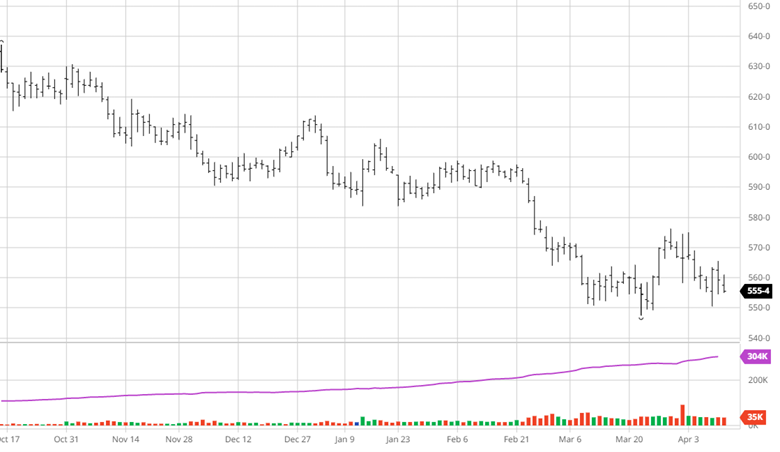

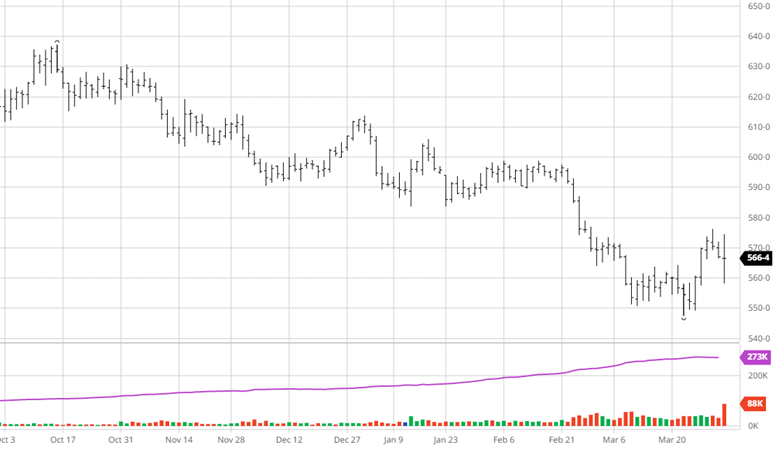

Lumber Futures Volume & Open Interest

CFTC Commitments of Traders Long Report

https://www.cftc.gov/dea/futures/other_lf.htm

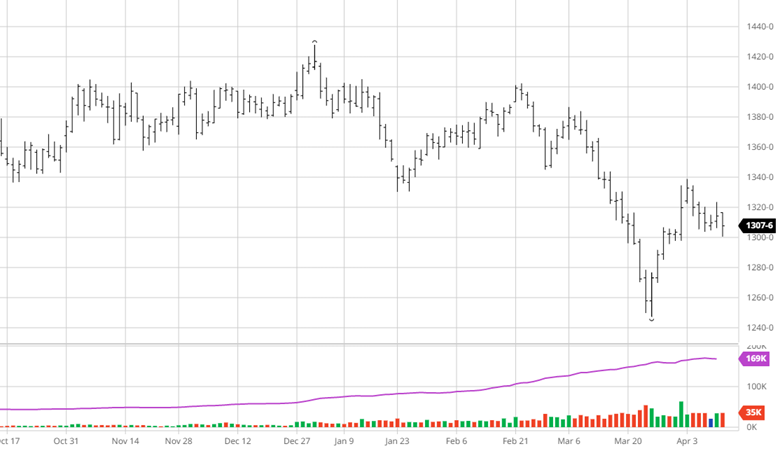

Lumber & Wood Pulp Options

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-2636