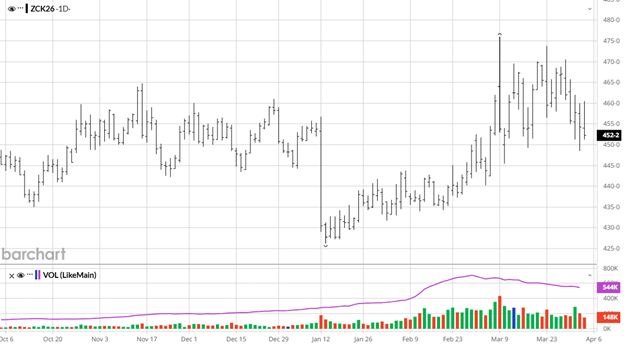

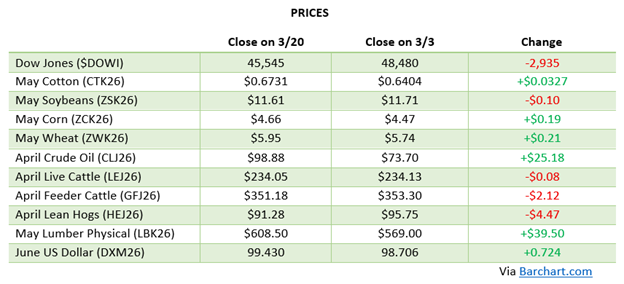

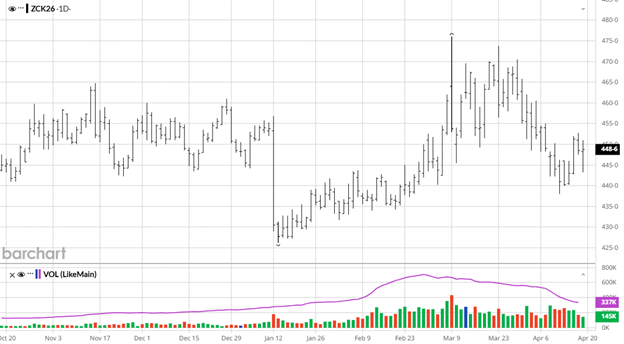

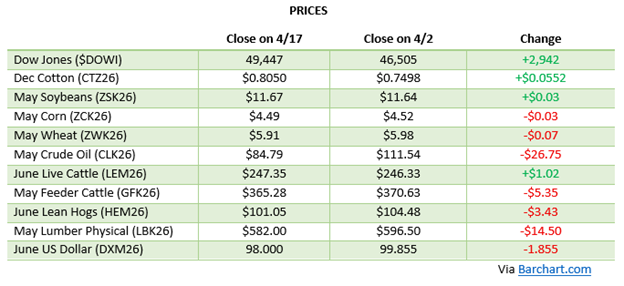

Corn spent the start of April grinding lower, posting a fourth consecutive weekly loss by April 10th as the April WASDE reinforced a burdensome supply narrative. The USDA left U.S. ending stocks essentially unchanged at 2.127 billion bushels, the highest in seven years, and global stocks came in above trade expectations at 294.81 million metric tons. A two week ceasefire between the U.S. and Iran, announced April 7th, removed much of the war premium that had propped up prices since March, as easing Strait of Hormuz concerns pulled crude oil sharply lower and dragged corn along with it. July futures slid to a fresh four-week low near $4.40, completing a nearly 62% retracement from the March 9th highs. The past week saw stabilization and a modest recovery. Faster than expected planting progress, U.S. corn planting reached 5% completion as of April 13th, slightly ahead of last year’s pace, combined with firming eastern Corn Belt basis and Mexico securing a large forward purchase of 12.4 million bushels helped steady sentiment. The old crop market remains locked in a congestion zone between $4.45 and $4.55 on May futures, with the 200-day moving average serving as key support. Speculators have been trimming their long positions aggressively, as shown in the latest CFTC Commitment of Traders reports, leaving the market less vulnerable to a large liquidation event but also with less upside fuel until a fresh catalyst emerges as money allocators reposition to the equity markets.

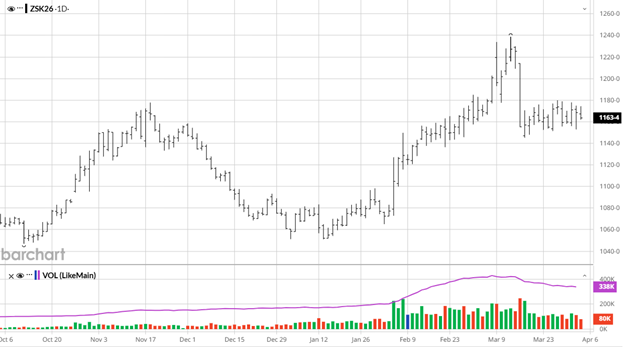

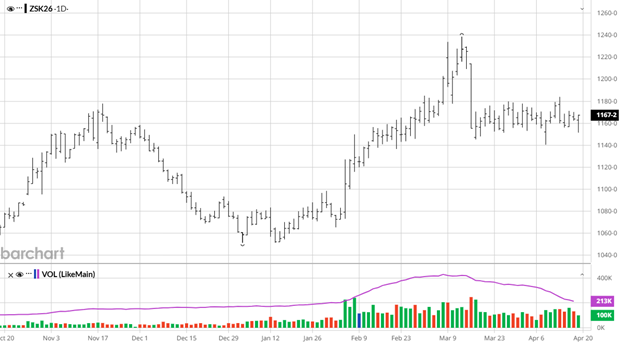

Soybeans have largely remained in a sideways grind, trading between $11.50 and $11.83 on July futures for most of the last 2 weeks. The April WASDE showed U.S. ending stocks unchanged at 350 million bushels with adjustments netting to zero, crush estimates raised while exports were trimmed by the same amount. The season-average price forecast was nudged 10 cents higher to $10.30 per bushel. Brazil’s CONAB raised its 2025/26 soybean production estimate again, this time to 6.582 billion bushels, keeping the global supply backdrop heavy and capping any sustained rallies. On the positive side, strong domestic crush margins, board crush pushing above $3 per bushel, have been the primary support story for the complex. NOPA March crush is expected to come in well above year-ago levels when reported. U.S. planting progress debuted at 6% complete as of April 13th, ahead of the 2% five-year average, with Mississippi and Tennessee leading at 39% and 36%, respectively. The market is waiting for a significant new headline to break out of the current range. Talks between President Trump and China’s President Xi, which were delayed amid the Iran conflict, remain a key watch item as any resumption of Chinese buying interest could quickly change the demand narrative for U.S. soybeans.

Soybeans have largely remained in a sideways grind, trading between $11.50 and $11.83 on July futures for most of the last 2 weeks. The April WASDE showed U.S. ending stocks unchanged at 350 million bushels with adjustments netting to zero, crush estimates raised while exports were trimmed by the same amount. The season-average price forecast was nudged 10 cents higher to $10.30 per bushel. Brazil’s CONAB raised its 2025/26 soybean production estimate again, this time to 6.582 billion bushels, keeping the global supply backdrop heavy and capping any sustained rallies. On the positive side, strong domestic crush margins, board crush pushing above $3 per bushel, have been the primary support story for the complex. NOPA March crush is expected to come in well above year-ago levels when reported. U.S. planting progress debuted at 6% complete as of April 13th, ahead of the 2% five-year average, with Mississippi and Tennessee leading at 39% and 36%, respectively. The market is waiting for a significant new headline to break out of the current range. Talks between President Trump and China’s President Xi, which were delayed amid the Iran conflict, remain a key watch item as any resumption of Chinese buying interest could quickly change the demand narrative for U.S. soybeans.

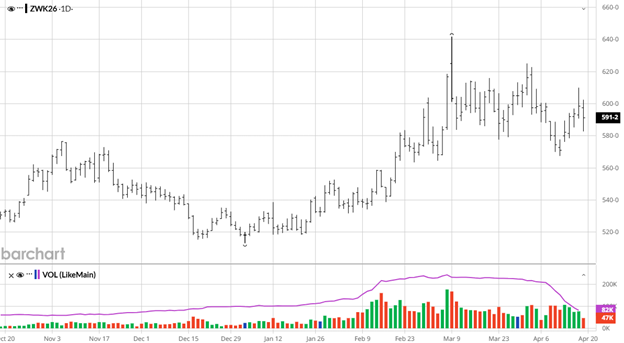

Wheat has done better the last couple of weeks, with Kansas City HRW futures rallying on the back of deteriorating U.S. crop conditions and persistent drought in the Southern Plains. USDA’s April 14th crop progress report showed just 34% of the winter wheat crop rated good-to-excellent, down a full 13 percentage points from a year ago, with 32% of the crop rated poor or very poor. Oklahoma and the Texas Panhandle remained in severe to extreme drought, and the recent widespread rain systems have largely missed the driest areas. Concerns about the long-term fertilizer supply disruptions caused by the Iran conflict have added a structural premium, with funds holding a record long position in spring wheat and a growing net long in Kansas City HRW. July HRW futures jumped nearly 20 cents on April 14th alone, reaching their highest settlement since March 31st at $6.36. Chicago SRW July futures also pushed above $6.00. The market sold off modestly to end the week but held the bulk of its gains. Longer-range forecasts suggest late April could bring more favorable moisture to parts of the Plains, which could temper upside. For now, weather, drought maps, and the weekly crop condition ratings are the primary price drivers.

Equity Markets

Equity markets have moved from deep stress to new record highs over this two-week stretch, tracking the Iran ceasefire developments closely. When Trump announced the two-week pause in operations on April 7th, the Dow Jones Industrial Average surged 1,325 points, its best single session since April 2025, while the S&P 500 gained 2.5% to 6,782. Through the balance of the period, stocks continued recovering as investors grew increasingly optimistic about a lasting peace deal, with the S&P 500 recouping all losses accumulated since the start of the conflict. The run to new highs has been impressive with the NASDAQ having a positive day for 14 straight days.

Energy Markets

Energy markets have continued to be volatile over the past couple of weeks but the news of ceasefire and opening of the Strait of Hormuz. While the cease-fire does not mean the conflict is over, if good news continues to come out of Washington oil prices will fall. The ceasefire dynamics have already meaningfully reduced fertilizer cost fears and energy-linked inflation expectations.

Other News

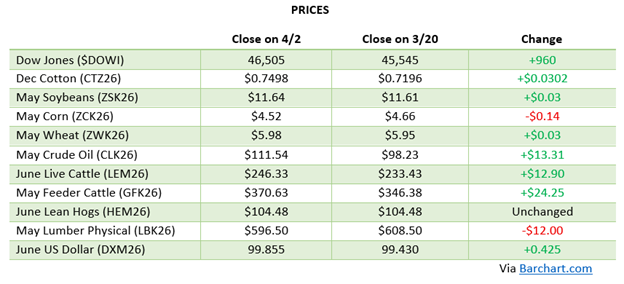

- Cotton has been one of the most compelling commodity stories of the period, with July futures pushing to a nearly two-year high and new crop cotton reaching $0.80 in the Dec contract. The move has been supported by a combination of bullish factors: elevated crude oil prices increasing polyester production costs and driving synthetic fiber substitution back toward natural cotton, a weaker U.S. dollar, and persistent drought in key U.S. growing regions stretching from the Texas Panhandle westward. The USDA April WASDE raised global production by 900,000 bales while also lifting consumption by 560,000 bales, leaving the net balance slightly tightened.

- USDA’s April WASDE raised the season-average farm price for wheat 5 cents to $5.00/bu, corn 5 cents to $4.15/bu, and soybeans 10 cents to $10.30/bu.

- The Trump administration called out fertilizer giant Mosaic for idling two Brazilian plants, with Deputy Agriculture Secretary Stephen Vaden publicly questioning the timing as global fertilizer supplies face war-related disruptions.

- A new survey found that only 60% of U.S. corn farmers have secured their nitrogen needs for the 2026 crop year, a reflection of the input cost uncertainty created by the Iran conflict.

- Brazil’s CONAB raised its 2025/26 total corn crop estimate to 139.6 MMT (5.5 billion bushels), maintaining a heavy Southern Hemisphere supply backdrop.

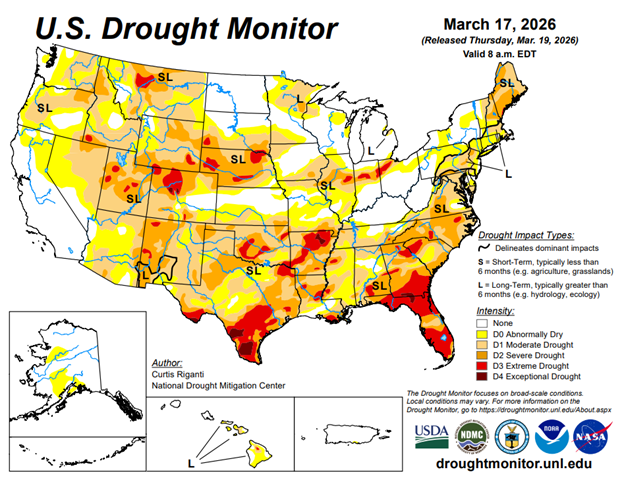

Drought Monitor

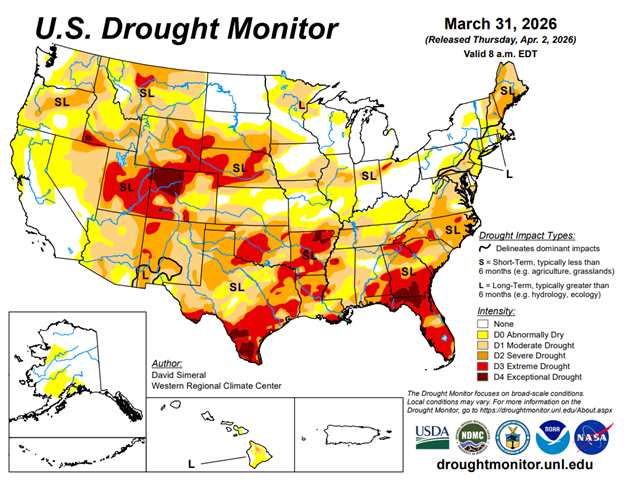

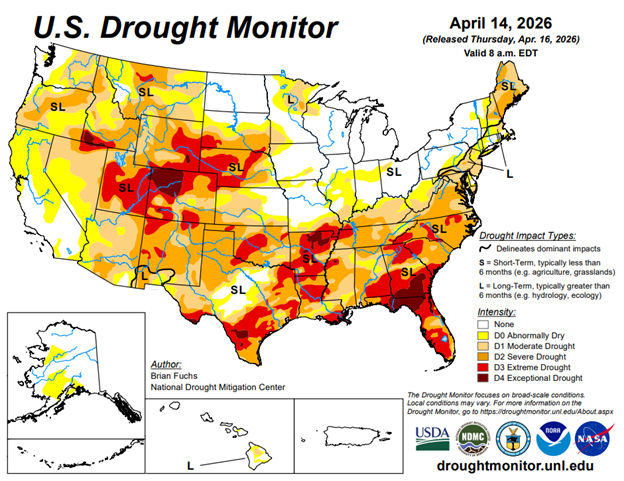

Here is the most recent drought monitor. With planting starting later this spring, we need rain in a lot of places in March.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.