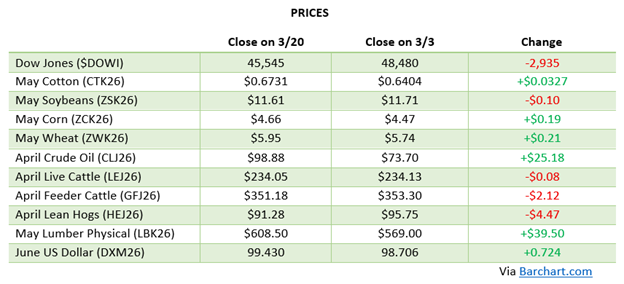

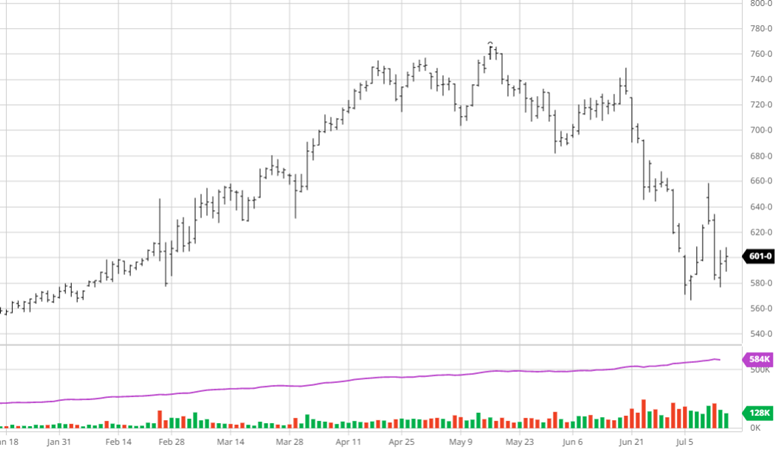

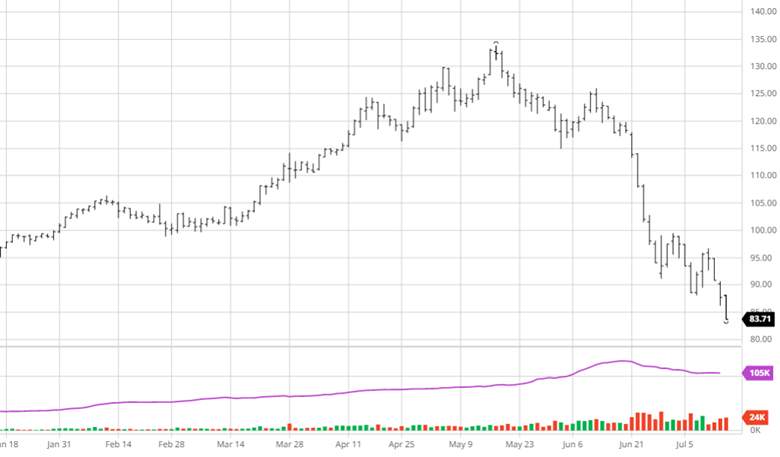

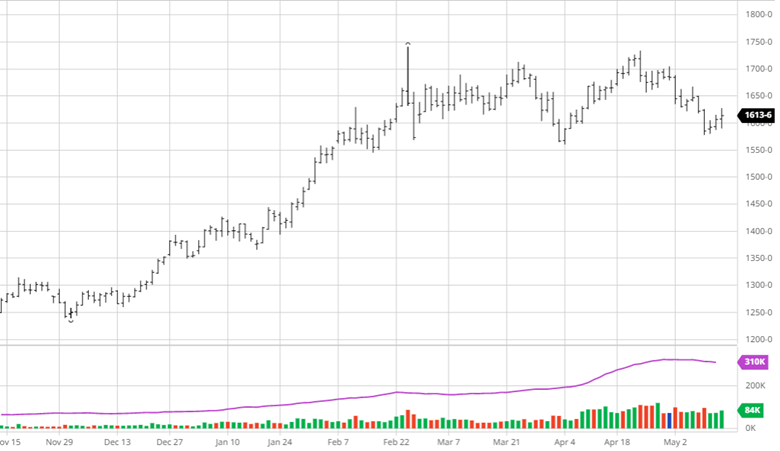

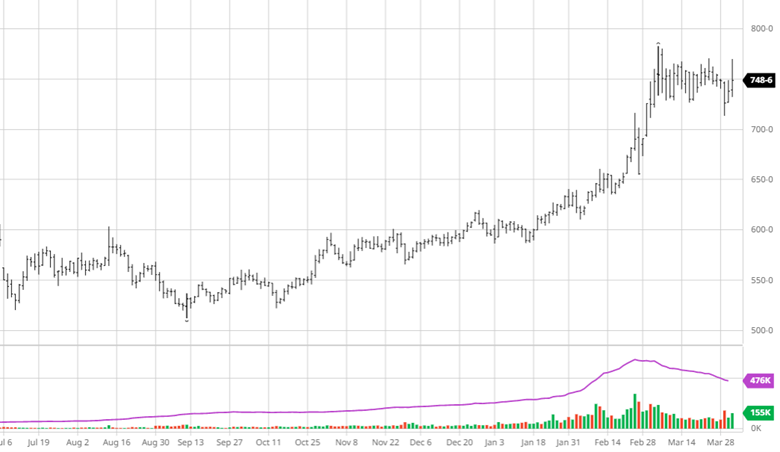

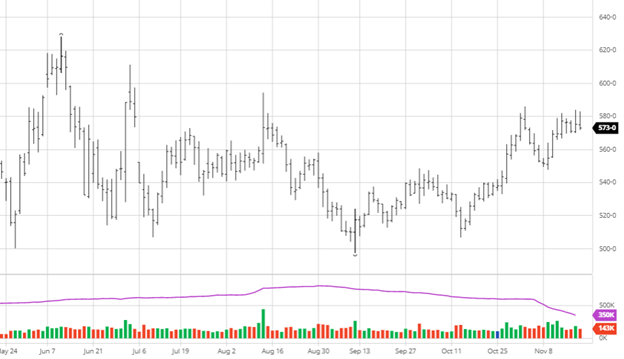

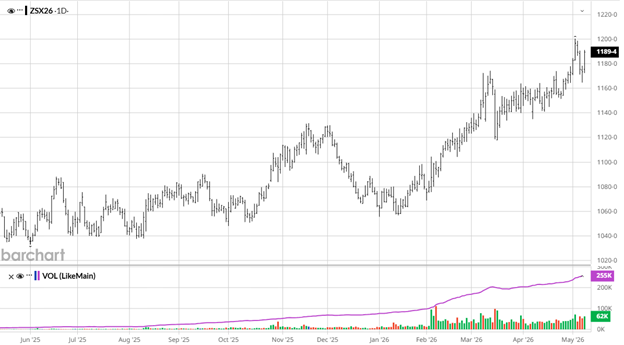

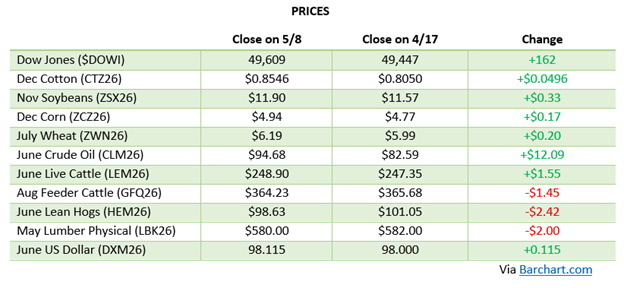

Corn has been a tale of two forces over the past three weeks. Coming off the euphoria of Iran’s Strait of Hormuz reopening announcement on April 17th, markets initially attempted to stabilize, but that news seemed short-lived as volatility in the middle east kept markets volatile. With the war premium in and out of the market, it has been trying to trade both geopolitical news and fundamentals, and those fundamentals remain heavy. U.S. ending stocks at 2.127 billion bushels, the highest in seven years, kept a ceiling on any sustained rally, and fast planting progress added some pressure. The USDA’s crop progress report showed nationwide corn plantings at 38% planted. Exports remain strong as the potential for a smaller US crop with higher fertilizer costs keep buyers in the market at these price levels. December corn popped above $5 for a couple days but quickly fell back as it fell with crude on peace talks. Geopolitical events are hard to predict, especially with this White House, so if you get the opportunity for profitable sales, it would be something worth considering because if crude drops back to $70-80/barrel and we have another record/near record crop it will be hard to hold these levels or move higher.

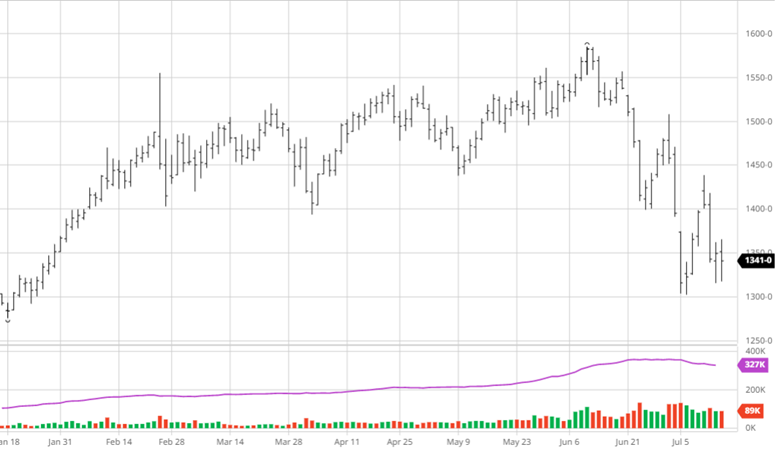

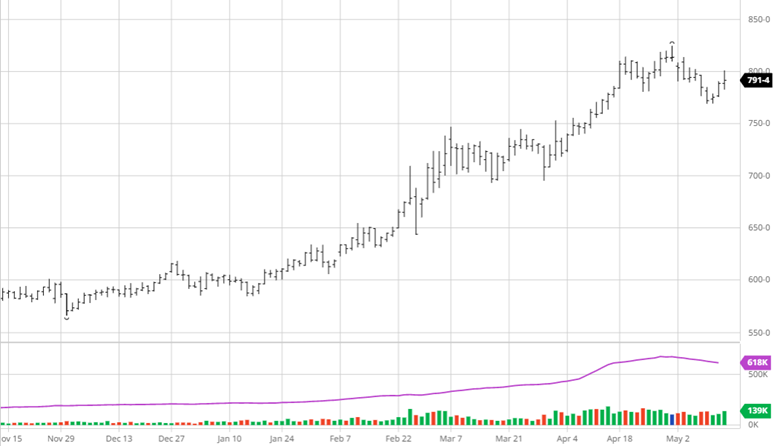

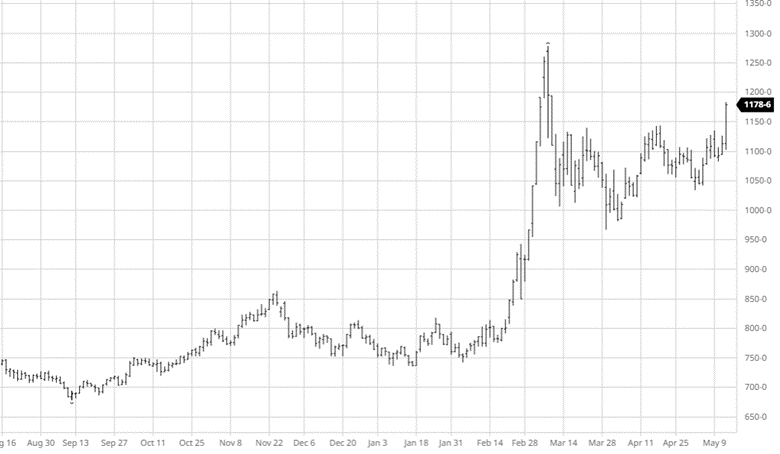

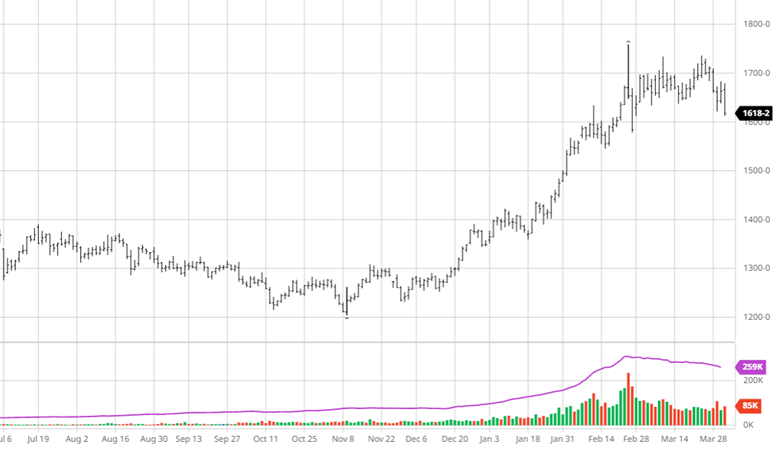

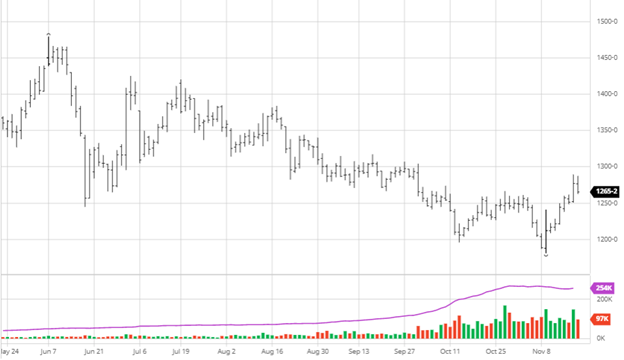

The market continues to wait for a fresh demand catalyst, and the one most closely watched, a potential resumption of Chinese buying linked to a Trump-Xi summit, has been repeatedly delayed amid ongoing Iran conflict negotiations, but appears to be on for this month. The bullish case for soybeans continues to rest on crush economics. Board crush margins holding above $3 per bushel are exceptional by historical standards and are supporting the nearby contracts. NOPA March crush are expected to far exceed year-ago levels, underscoring the strength of domestic demand for meal and oil. Brazil’s Conab raised its 2025/26 soybean production estimate once more to 6.582 billion bushels, and May shipment estimates from Brazil’s Anec were raised to 533.8 million bushels, peak export season for the world’s largest shipper. That supply overhang remains the key obstacle to a sustained rally with South America having such a large crop. Beans planted were at 33% for the week of May 4th, slightly lower than expected but still very strong for this time of year.

The market continues to wait for a fresh demand catalyst, and the one most closely watched, a potential resumption of Chinese buying linked to a Trump-Xi summit, has been repeatedly delayed amid ongoing Iran conflict negotiations, but appears to be on for this month. The bullish case for soybeans continues to rest on crush economics. Board crush margins holding above $3 per bushel are exceptional by historical standards and are supporting the nearby contracts. NOPA March crush are expected to far exceed year-ago levels, underscoring the strength of domestic demand for meal and oil. Brazil’s Conab raised its 2025/26 soybean production estimate once more to 6.582 billion bushels, and May shipment estimates from Brazil’s Anec were raised to 533.8 million bushels, peak export season for the world’s largest shipper. That supply overhang remains the key obstacle to a sustained rally with South America having such a large crop. Beans planted were at 33% for the week of May 4th, slightly lower than expected but still very strong for this time of year.

Equity Markets

Equity Markets

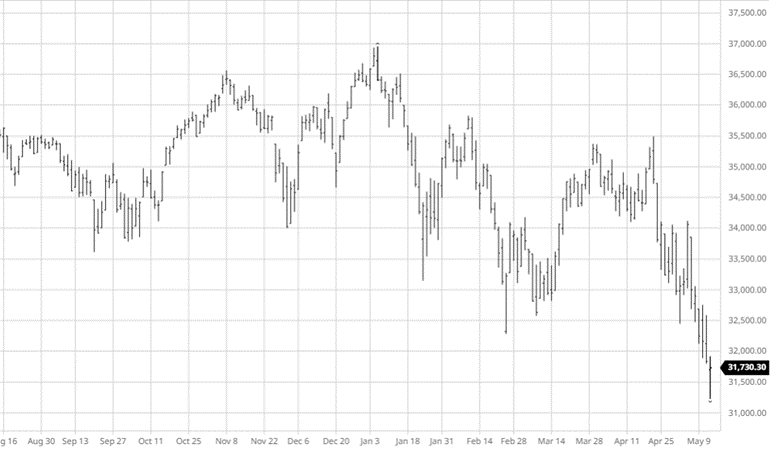

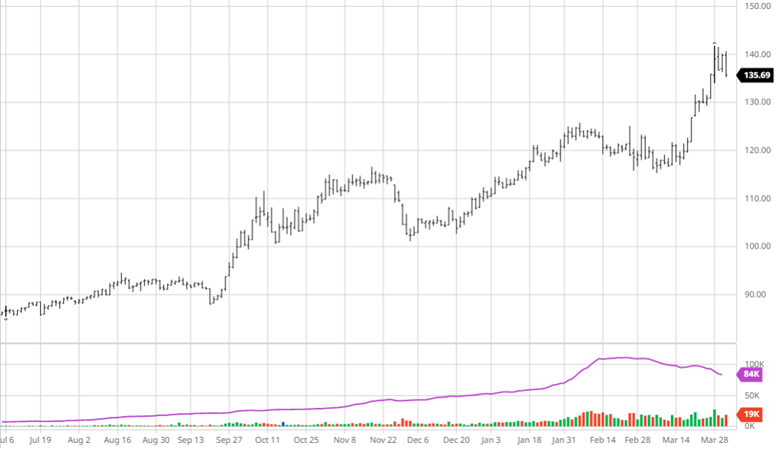

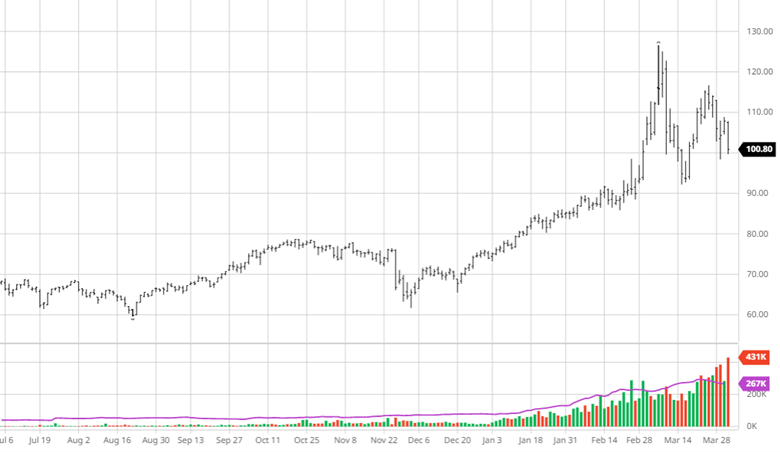

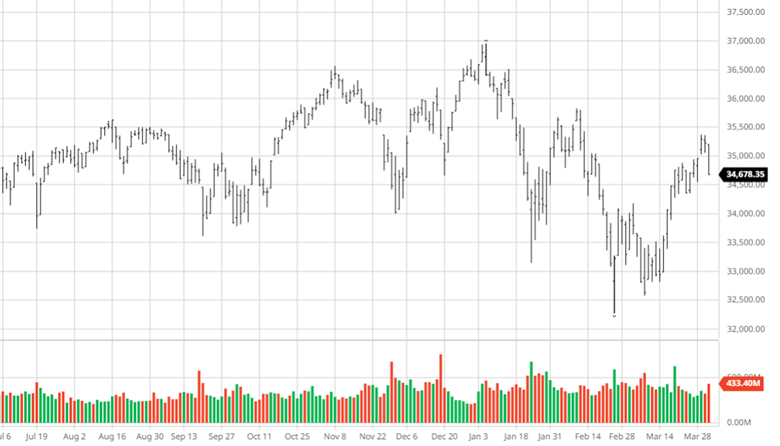

Equity markets continue to make new highs on the back of the AI trade with names like Micron, SanDisk and Western Digital screaming higher and other tech names having a very strong April with the NASDAQ Index up over 15% in the month. Big players such as Google, Meta, and Amazon reported in the last 2 weeks with mixed results but the markets moved higher.

Energy Markets

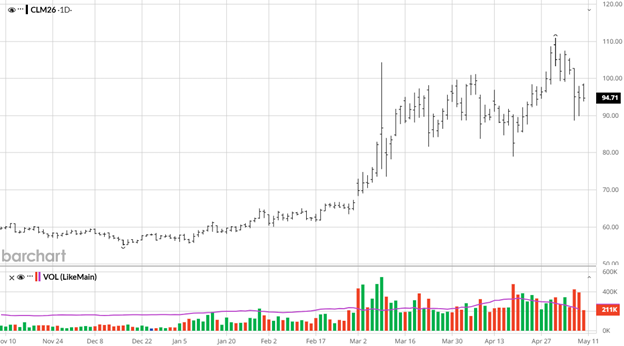

Energy has remained the dominant macro force across all commodity markets, though the price action has been far more volatile and two-directional compared to the one-way crude rally seen earlier in the spring. This push-pull between ceasefire hopes and renewed escalation threats has created a volatile and headline-driven energy market. For ag producers, the primary implication is that fertilizer cost relief remains partial and uncertain. Diesel costs have come down from peak levels but are not back to pre-war norms, and nitrogen prices, which spiked nearly 40% during the war, have only partially retreated.

Other News

– Cotton has continued its run higher on demand from overseas buyers with alternative fibers such as polyester needing oil for production. Growers can be profitable at these levels so having a hedging strategy where you protect the downside but can still participate in any further upside is very important.

– EPA finalized 2026–2027 Renewable Fuel Standard volumes at record highs, a development that could meaningfully increase ethanol demand and provide a long-term supportive floor under corn prices.

– Iran is reportedly evaluating a U.S. peace proposal that includes a full reopening of the Strait of Hormuz by both sides. Markets expect Iran’s formal response in coming days, making this the single most important macro event in the near-term commodity outlook.

– The May 12th USDA WASDE report will include the first official 2026/27 production forecasts for all major crops. Given the wheat situation in the Plains and uncertainty around corn acres, this report has the potential to be a significant market mover across the complex.

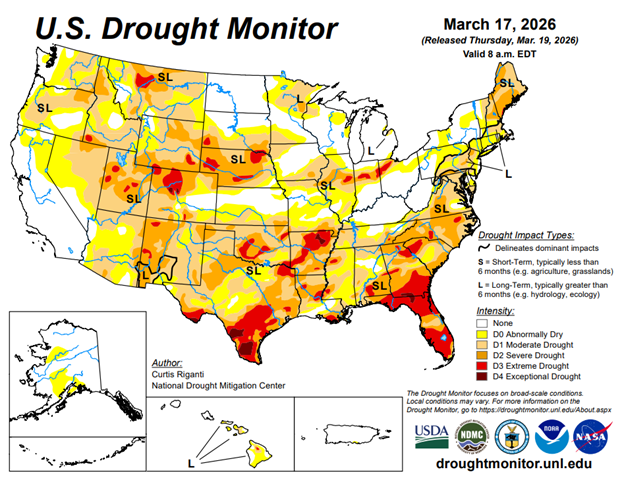

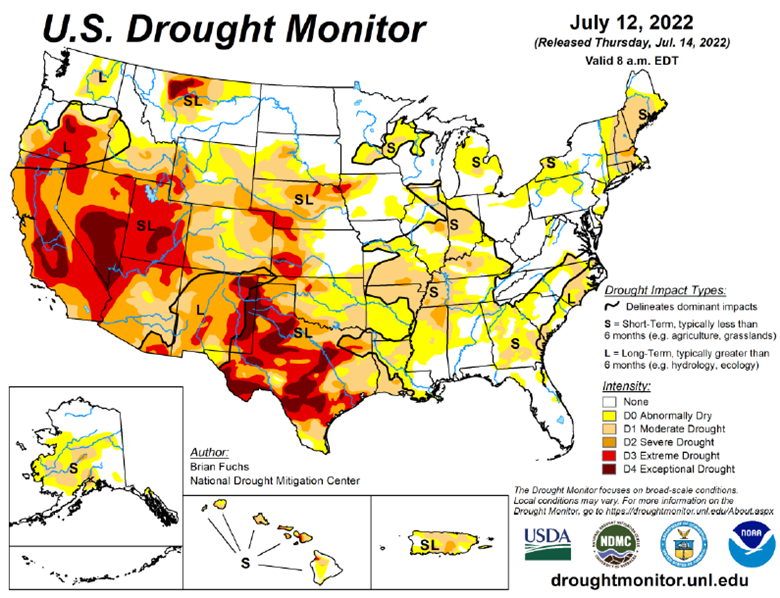

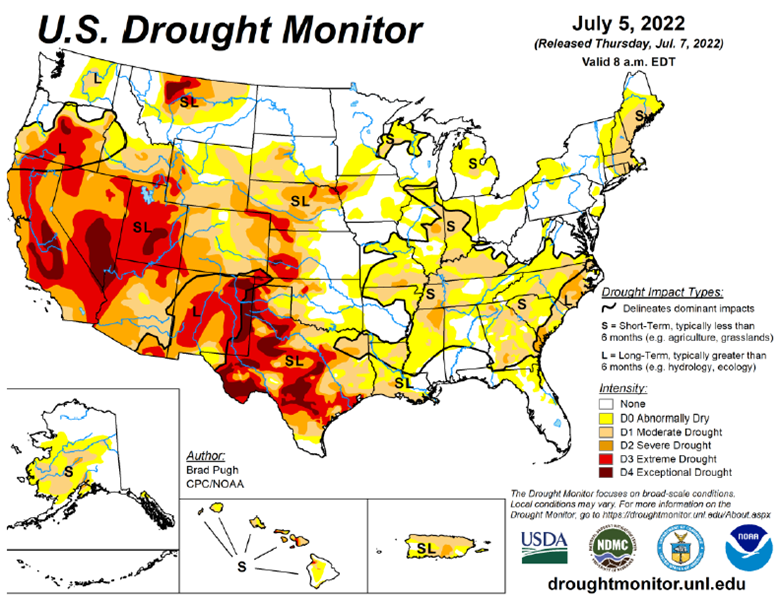

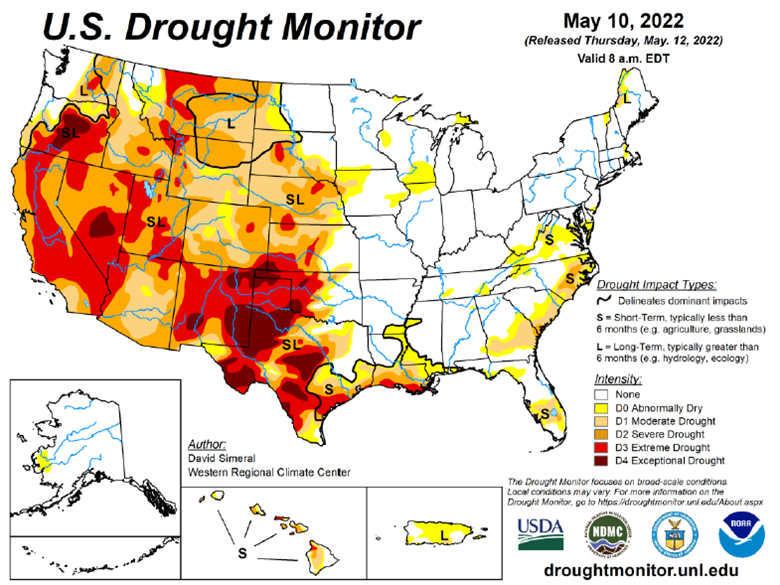

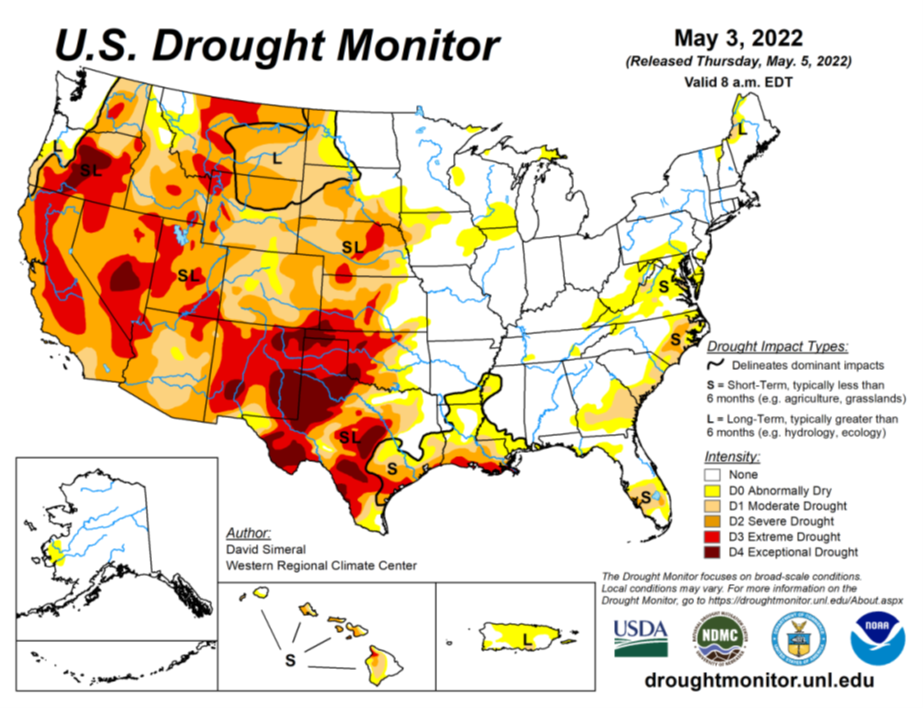

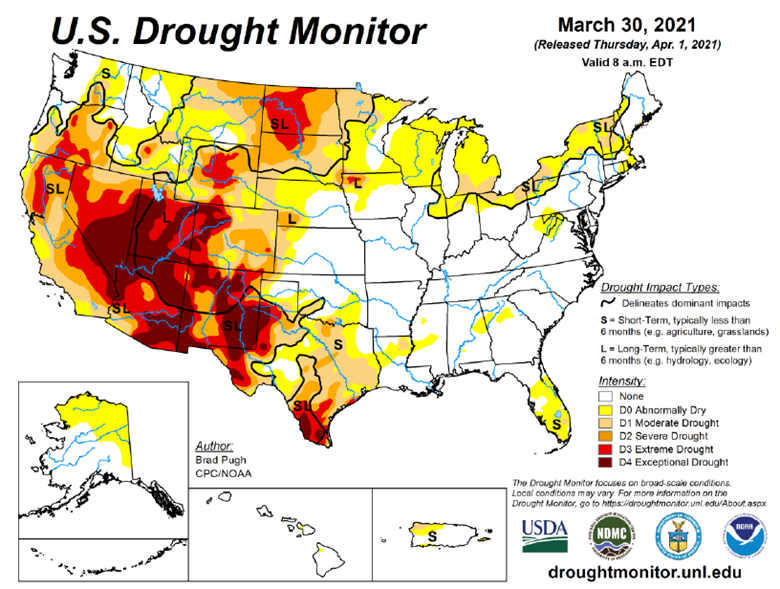

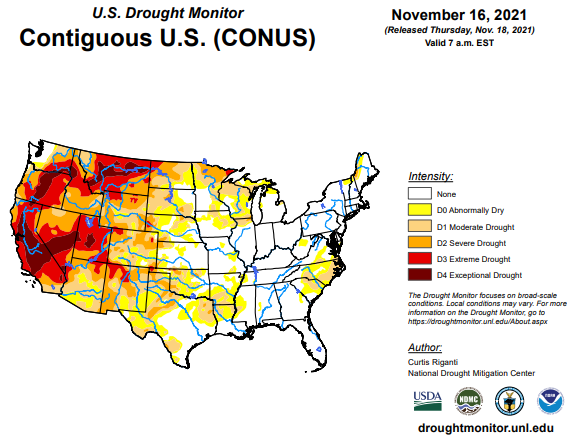

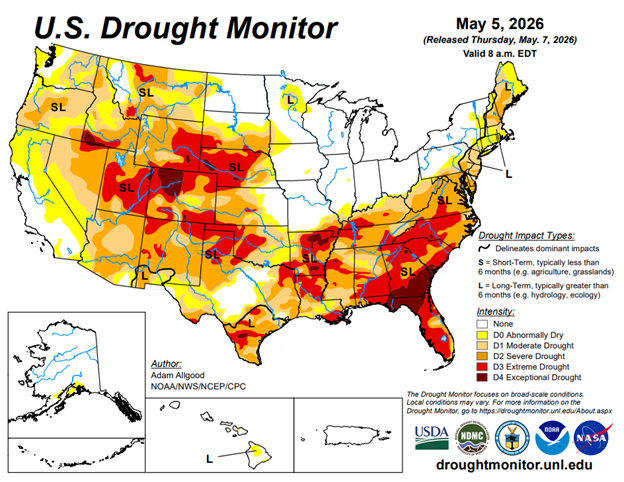

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today+

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.