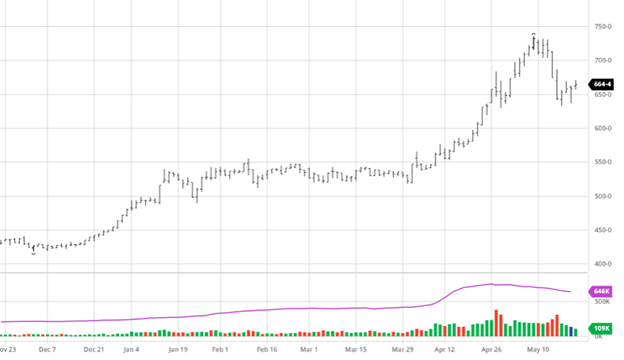

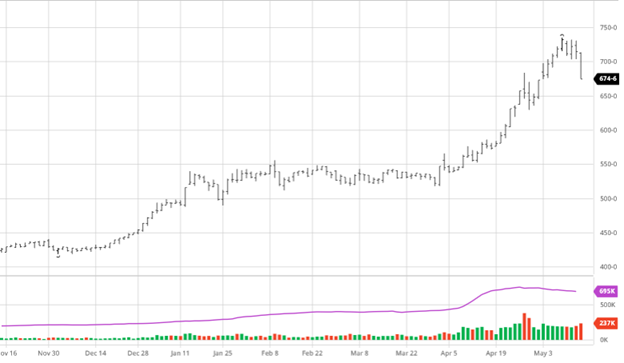

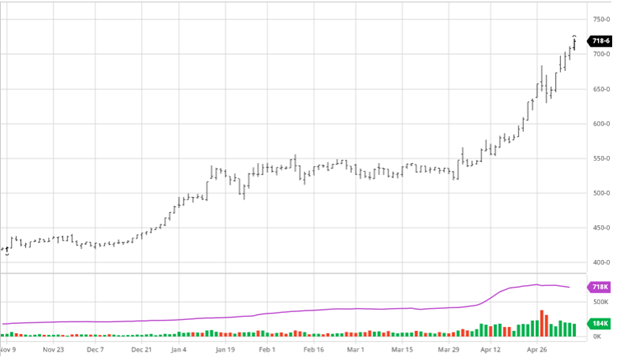

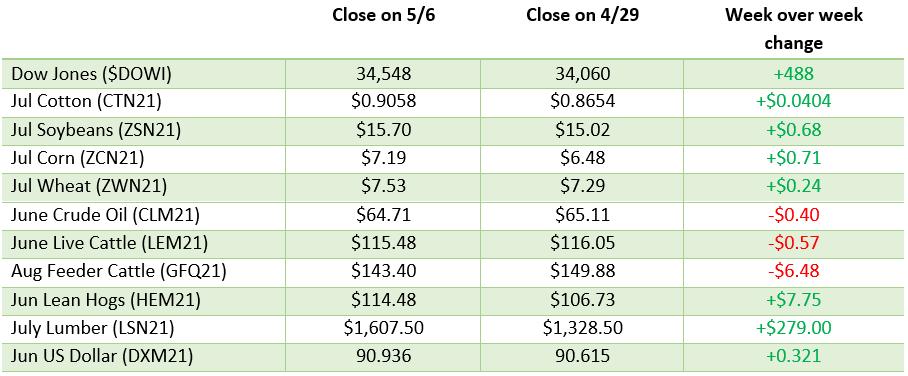

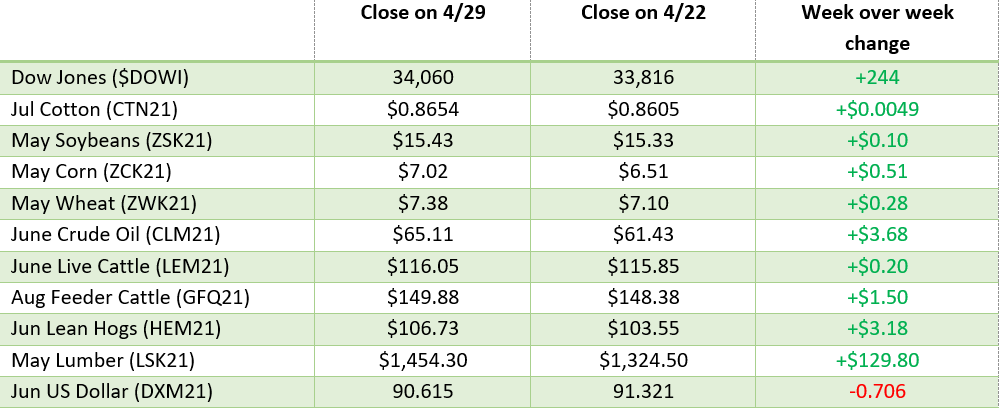

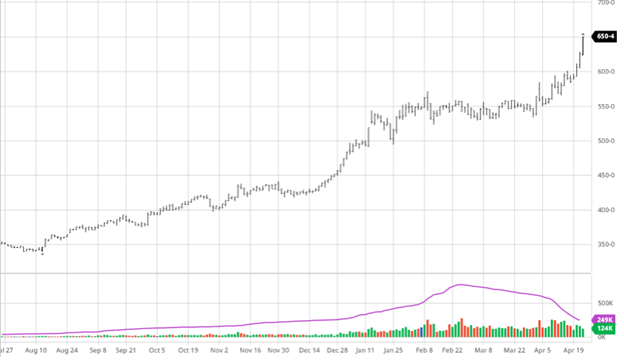

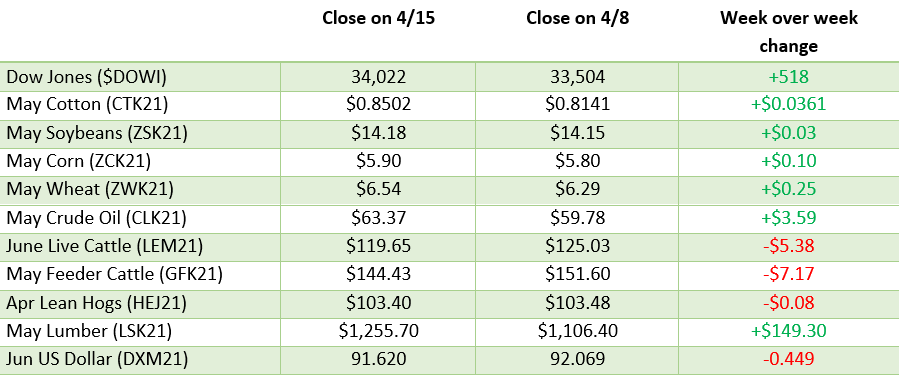

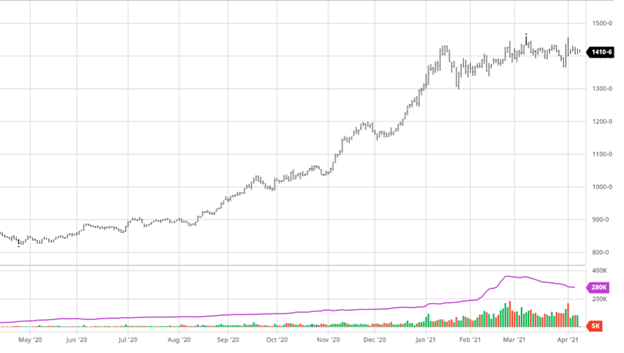

Volatility was the story this week as you can see the dip and bounce back over the last few days in the chart below. Surprisingly it was not the funds alone that triggered the selloff but rather a more balanced mix of funds, commercials, and farmer selling – in short – it appears to have been a bit of profit taking into the end of the month.

Corn had strong exports this week with no major cancellations (despite rumors to start the week). While these rumors of a cancellation dropped prices aggressively, the subsequent large sales of new crop corn to China, following the dip, ended up saving China quite a bit of money while also rebounding our markets. Seller beware when China is the main buyer.

The weekly ethanol grind was 294MGa and well above the weekly pace needed to meet the annual USDA estimate. Corn was seen as being 91% planted to start the week along with great weather across most of the US heading into Memorial Day weekend.

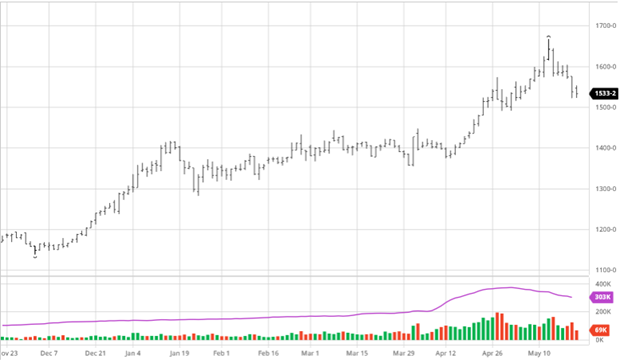

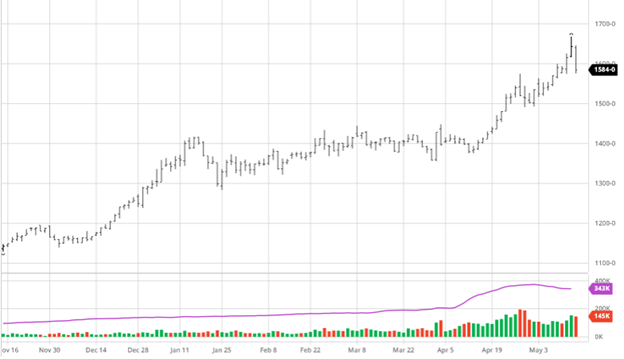

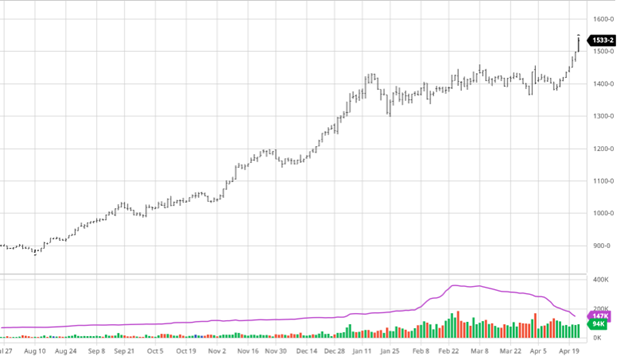

Soybeans made small gains on the week with lower volatility than corn but similar price movement. Exports were solid in old crop beans giving the bulls some momentum to work with heading into the weekend. Exports were strong again this week, which is a welcome sign after slowing the last couple. The soybean crop was seen as about 80% planted at the start of the week as progress continues across the country. The recent loses have made US commodities competitive again in the world market allowing for some stronger demand into the end of the year. Once we get on the other side of Memorial Day the June weather outlook will start to be important as most of the crop will be in the ground and some already well into growing.

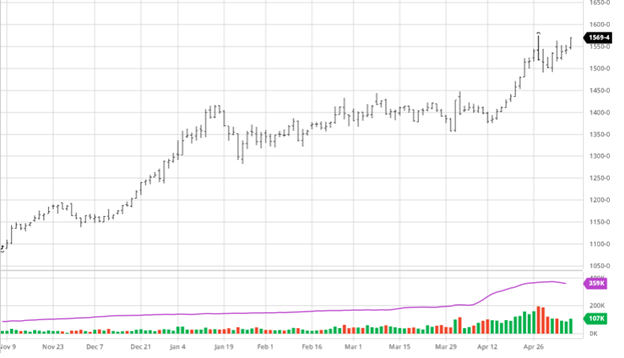

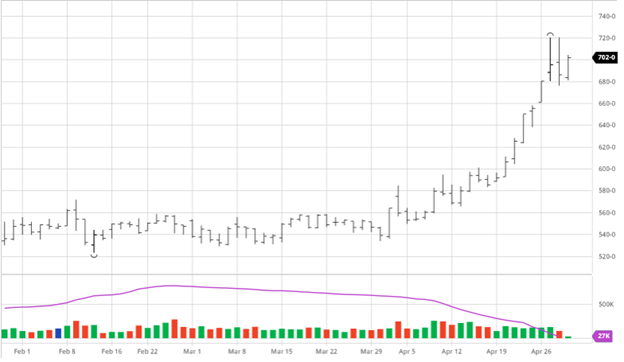

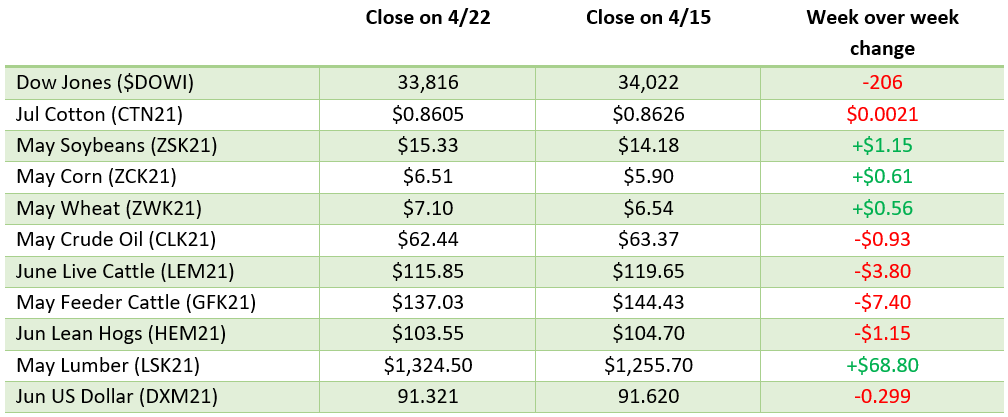

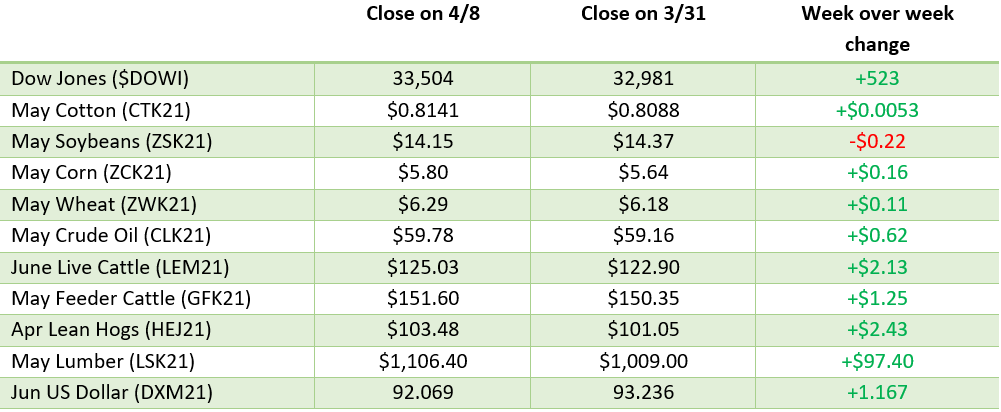

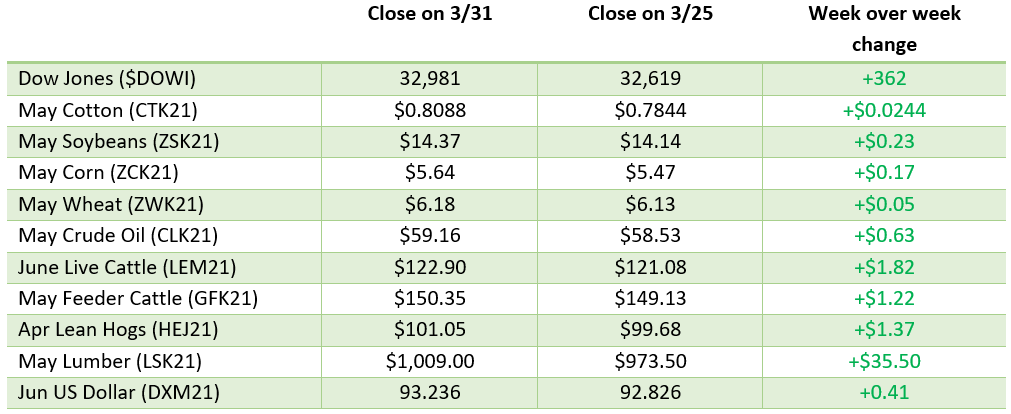

Dow Jones

The Dow and other indexes gained on the week with improving opening conditions and support for some of the major market players in the S&P. Republicans and Democrats continue to work on their versions of the infrastructure plan the Biden White House wants to pass.

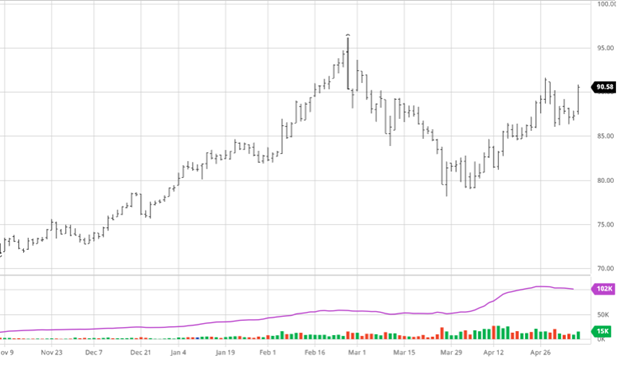

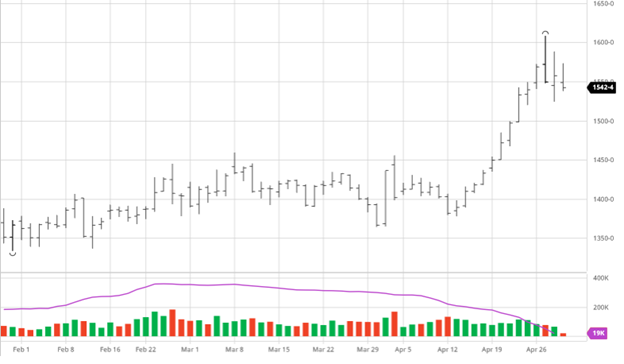

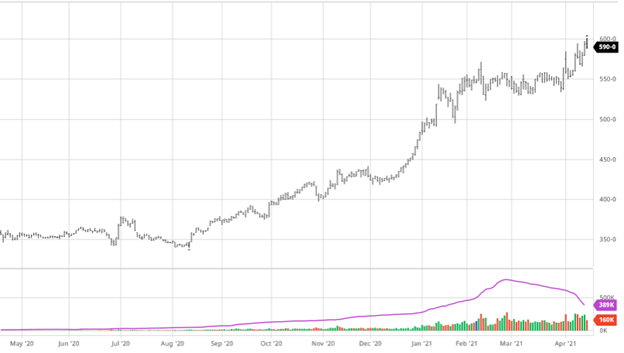

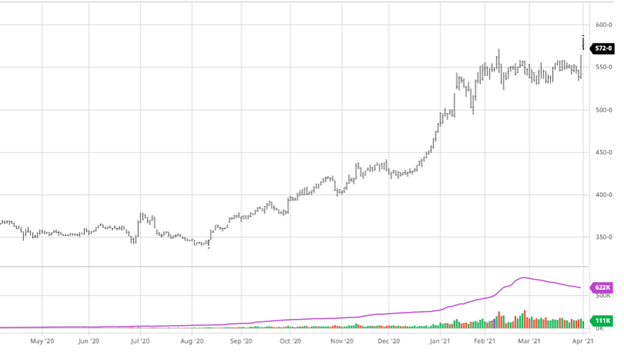

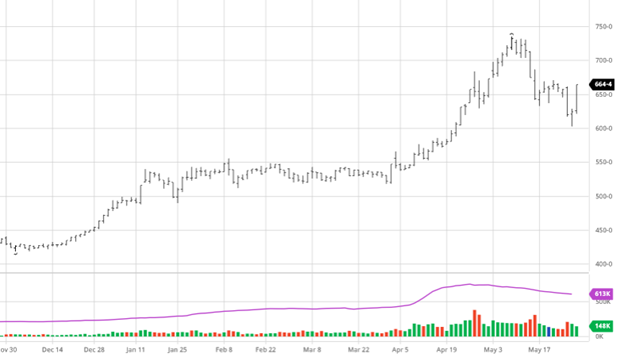

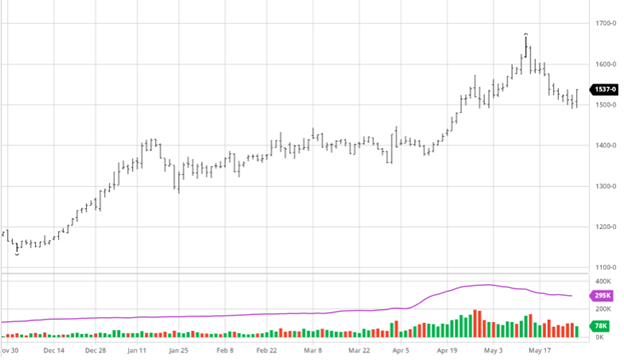

Lumber

Check out our recent post about the lumber market and what all has been going on.

Podcast

Check out our recent podcast with Dr. Greg Willoughby: We’re talking with Greg in the new episode about being a “plant doctor”, weather patterns, GMO & organic produce, crop history, technical advances, level 201 education on agronomy, the agronomy equation, Helena Agri, soil biology, American v European agriculture, Greg’s early background in livestock, and the advancement of native plants to modern produce.

https://rcmagservices.com/the-hedged-edge/

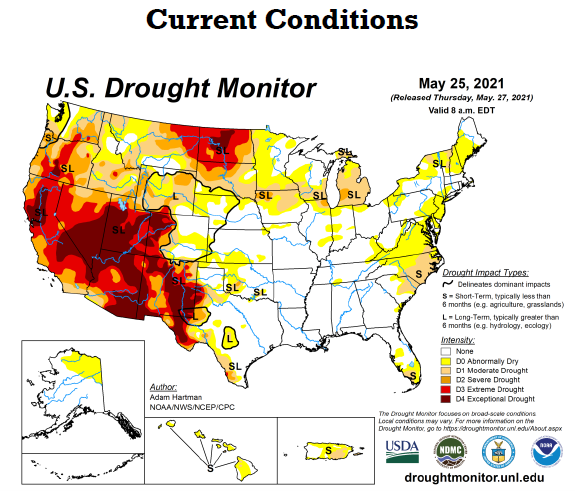

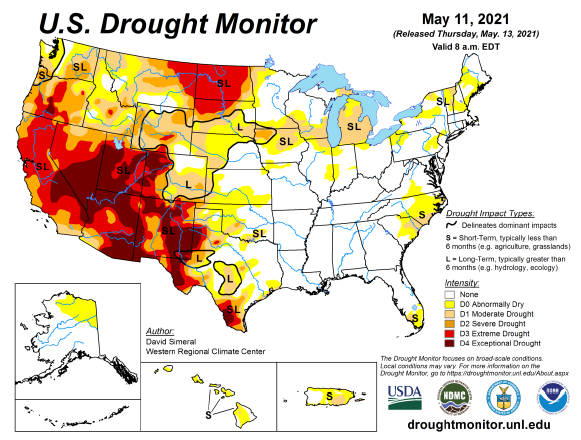

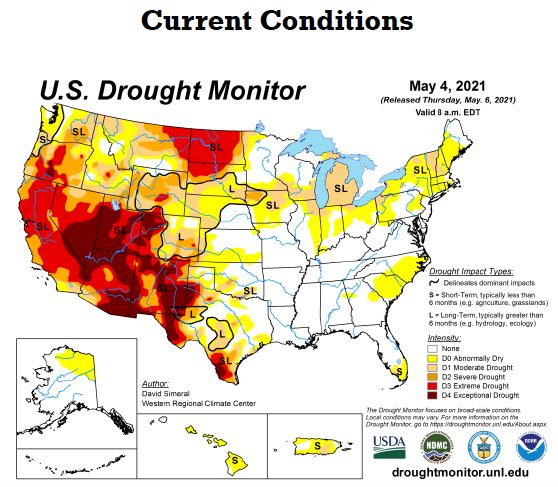

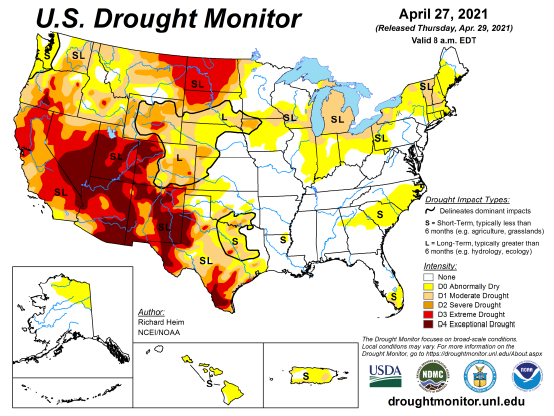

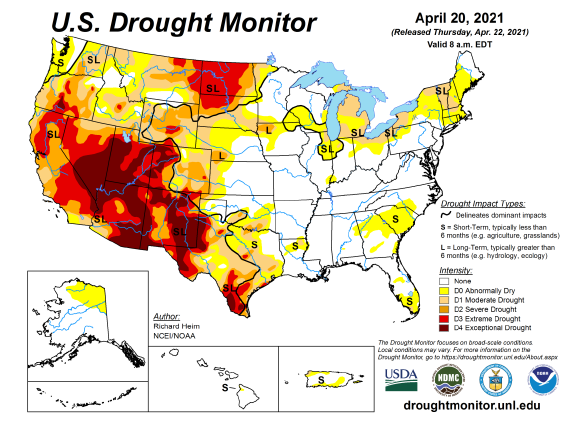

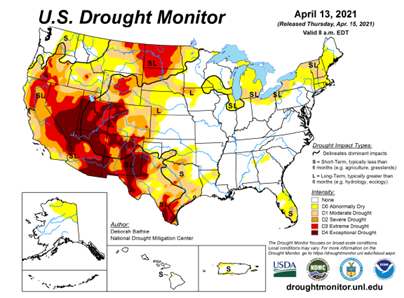

US Drought Monitor

The map below shows this week’s drought conditions across the US. Many areas across the corn belt received rain over the week while others, like the Dakotas and Michigan, remain dry.