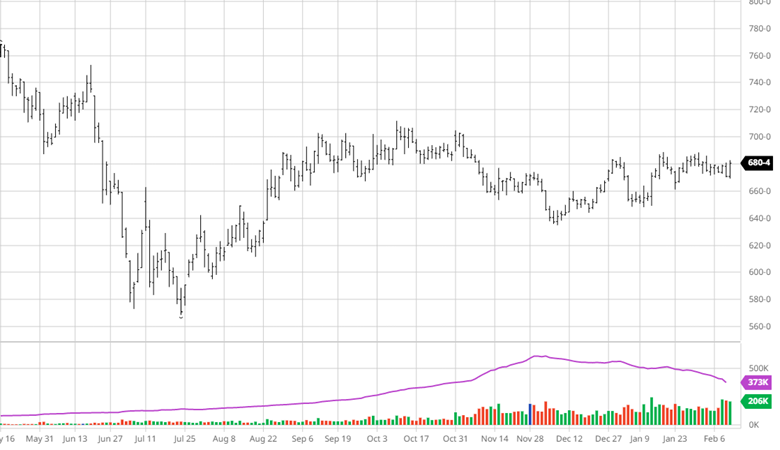

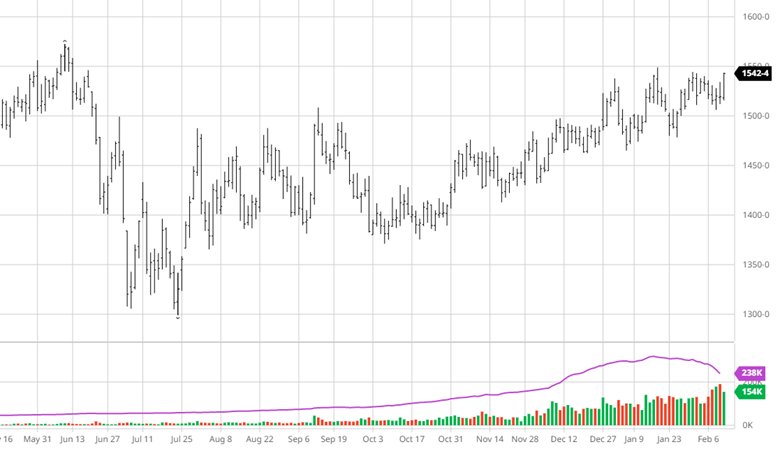

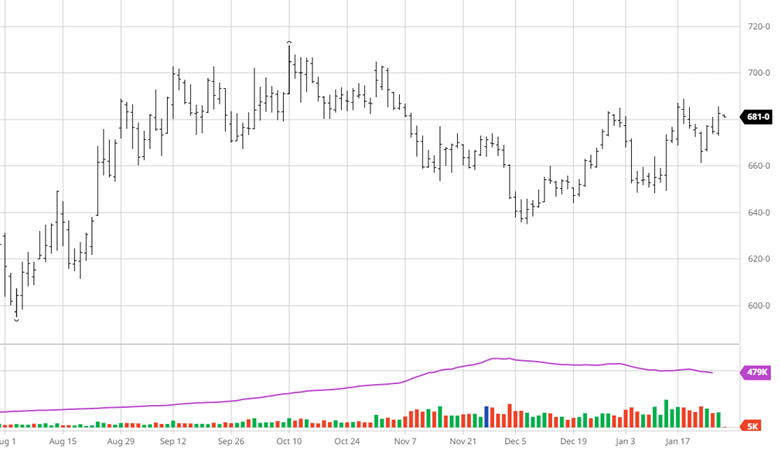

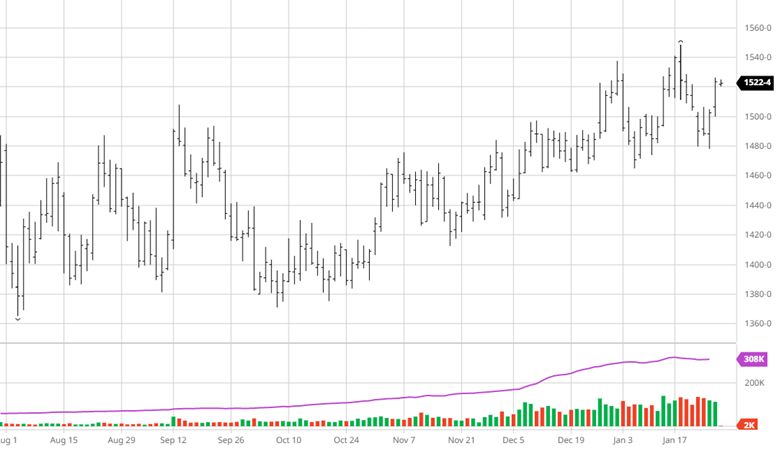

Commentary:

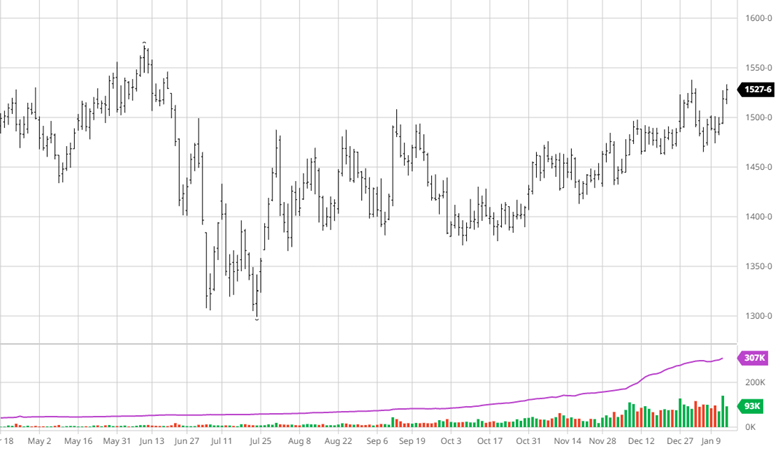

The market just experienced a long needed buy round. It started as a fill in and turned into a fill up. The buy side had the futures to lean on so many stepped up their buying. The problem with that was the fact that futures fell quicker than expected and now there is more wood out there than needed. You throw the Euro wood into the mix, and we have more wood chasing too few dollars again. In traders’ terms “the market lost the bid again.”

Economic:

The key to housing fundamentals is labor. We went all through the teen years without enough skilled labor. Finally, prices were forced up enough to allow wages to rise and get the needed labor. We have not seen any layoffs in the home building sector so far. That is a sign of confidence on the home builder’s side. Today we are all data dependent. The builders are not seeing big downturn in the numbers but its early.

Technical:

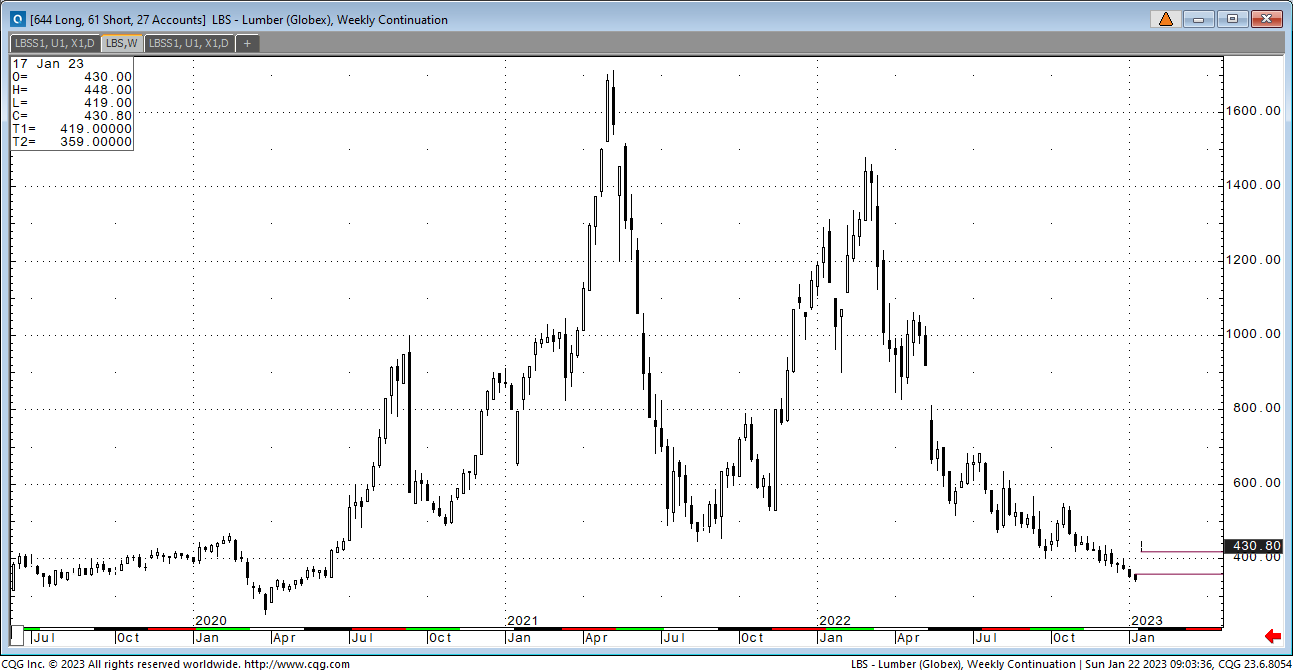

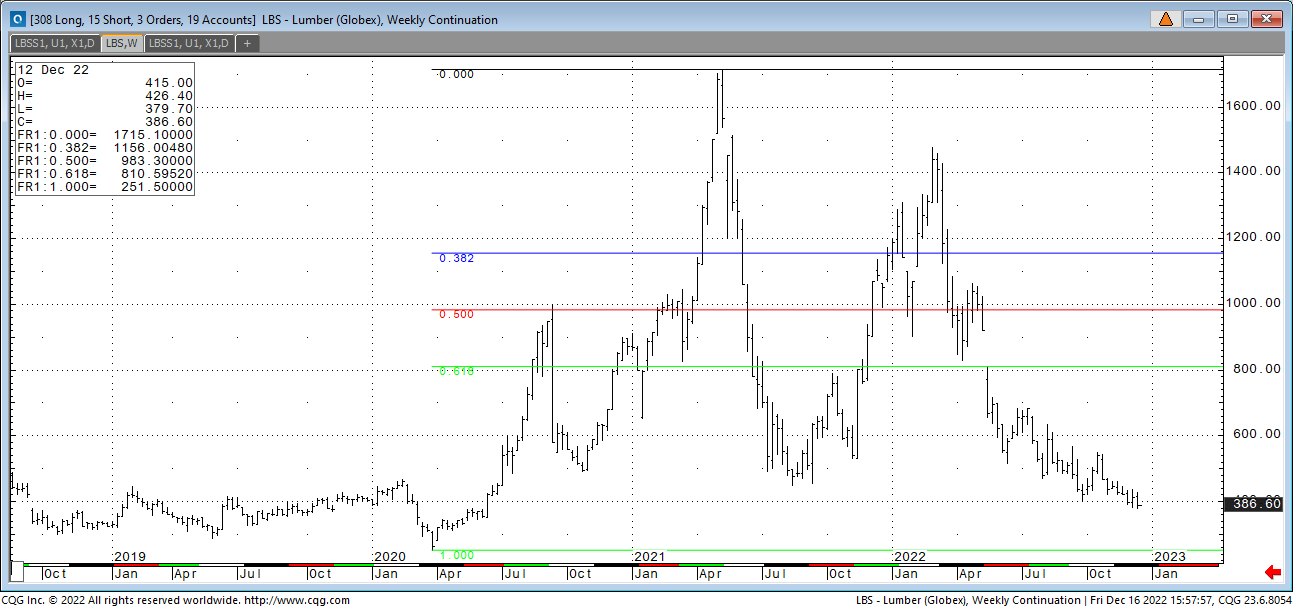

It is hard to believe but the week gap left by the expiration is coming back into play. That gap is 419 to 344. Please remember the last time I talked about the gap the market rallied $100. This time I don’t think the timing is right for a rally. The downside channel comes in at 379.50. The expiration pushed the market over the channel not market conditions. This area has become relevant again today but is also now defined as cheap.

The market of the past few months reminds me of the typical “controlled burn” markets of the past. You have to hold inventory because the spikes are quick and violent. We are back to the first buy is good and then not. The difference on this one is there just may be a premium to sell in futures to stop the bleeding. That’s what just occurred. The other positive is now futures are headed for a deep discount allowing forward pricing again. That is a controlled burn. There is a path to mitigate risk and invest.

CFTC Commitment of Traders report still delayed!!

NEW CONTRACT:

Lumber Futures Volume & Open Interest

CFTC Commitments of Traders Long Report

https://www.cftc.gov/dea/futures/other_lf.htm

Lumber & Wood Pulp Options

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

312-761-2636