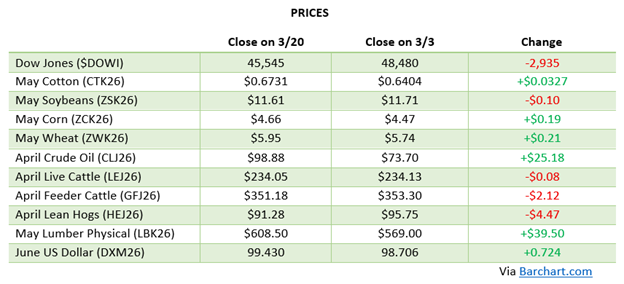

Recap:

Futures finished the week down $21. One notable development was in the COT report showing an increase of 924 industry longs. That puts the long hedge position at roughly 1,600 cars. That represents a meaningful amount of protection in place and should help dampen anxiety during periods of volatility. At the same time, short funds added 595 contracts, remaining committed to the lumber futures trade.

In a low-volume environment, positioning matters. The industry is actively managing risk by using futures to step away from the daily cash-market grind, while the funds continue to stay with a trade that has worked. Who is hedged—and who is pressing—will matter more as liquidity thins.

Unlike the October/Now NAWLA meetings, which often end with traders going gangbusters, the Montreal convention usually goes out with more of a whimper. That is largely seasonal. As the calendar turns toward May, near‑term needs begin to fade, and most buyers have already covered requirements for a while. The shift toward JIT purchasing changed that dynamic somewhat, but only at the margins.

In short, the discount should cap the selloff, but the overall tone suggests the market is waiting for the next buy program to emerge.

Technical:

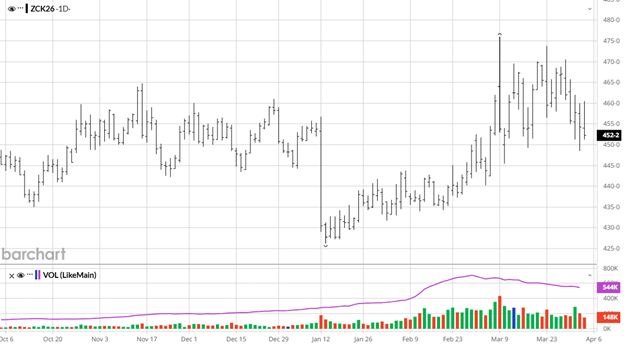

Momentum indicators are negative. The futures market is struggling to keep them positive. What I have noticed is that the trendlines are trending lower. The market is walking the support and resistance lines down each cycle. Each time futures trade above the resistance line, it is followed by a sharp break. Today, the industry is using those breaks to hedge future needs. It becomes an efficient derivative tool, and that creates neutrality.

Daily Bulletin:

https://www.cmegroup.com/daily_bulletin/current/Section23_Lumber_Options.pdf

Southern Yellow Pine:

https://www.cmegroup.com/markets/agriculture/lumber-and-softs/southern-yellow-pine.volume.html

The Commitment of Traders:

https://www.cftc.gov/dea/futures/other_lf.htm

About the Leonard Report:

The Leonard Lumber Report is a column that focuses on the lumber futures market’s highs and lows and everything else in between. Our very own, Brian Leonard, risk analyst, will provide weekly commentary on the industry’s wood product sectors.

Brian Leonard

bleonard@rcmam.com

312-761-263

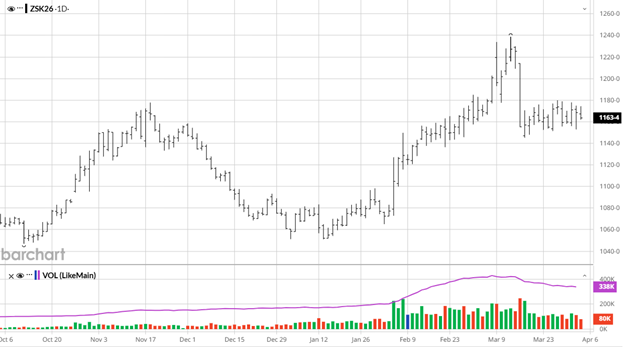

Soybeans have struggled to find sustained strength even after the March 31st USDA reports, which confirmed expectations for increased U.S. acreage and relatively comfortable stocks levels. The larger planting outlook reinforces the idea of ample new crop supplies, especially when paired with ongoing pressure from South America’s record production. While periodic rallies have been driven by energy market spillover and inflation concerns, the lack of consistent export demand, particularly from China, and fading optimism around biofuel policy have kept the market defensive. Overall, the USDA data solidified a more bearish supply outlook, leaving soybeans reliant on external market strength rather than supportive fundamentals. Talks between president Trump and China’s president Xi will be watched under a microscope if they end up happening after already being delayed with the conflict in Iran continuing.

Soybeans have struggled to find sustained strength even after the March 31st USDA reports, which confirmed expectations for increased U.S. acreage and relatively comfortable stocks levels. The larger planting outlook reinforces the idea of ample new crop supplies, especially when paired with ongoing pressure from South America’s record production. While periodic rallies have been driven by energy market spillover and inflation concerns, the lack of consistent export demand, particularly from China, and fading optimism around biofuel policy have kept the market defensive. Overall, the USDA data solidified a more bearish supply outlook, leaving soybeans reliant on external market strength rather than supportive fundamentals. Talks between president Trump and China’s president Xi will be watched under a microscope if they end up happening after already being delayed with the conflict in Iran continuing.