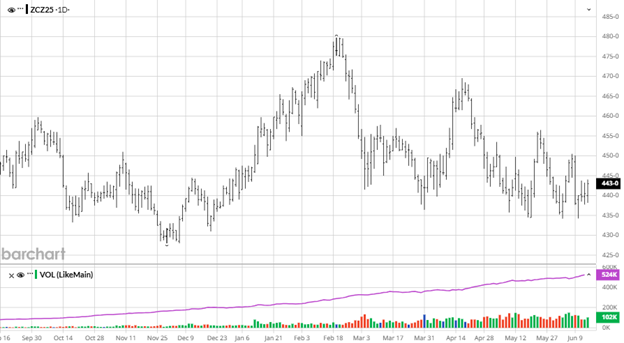

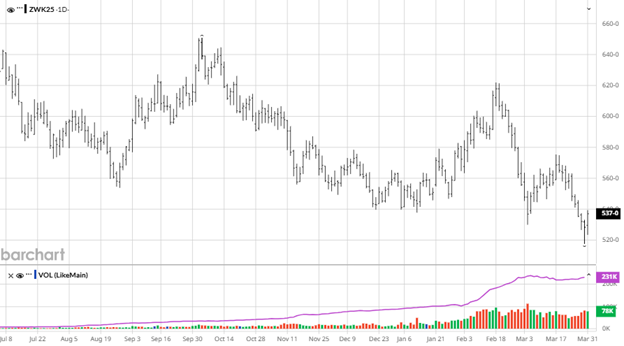

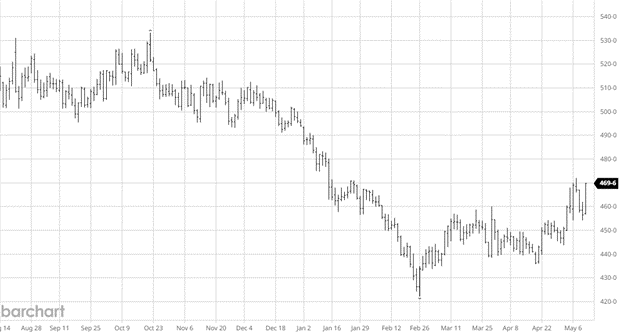

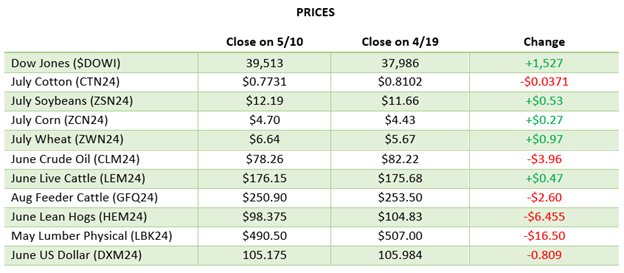

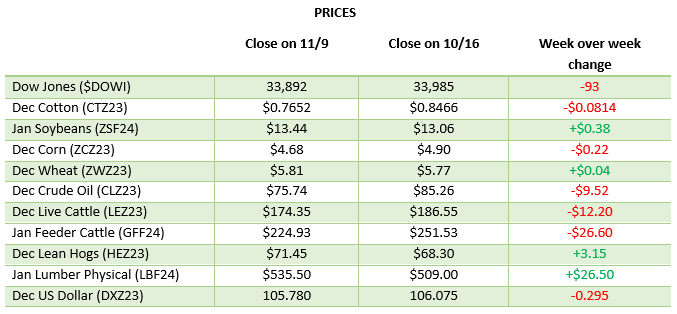

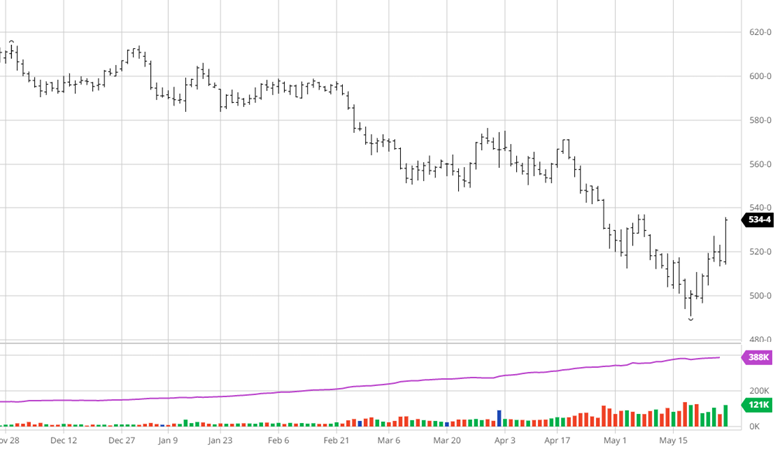

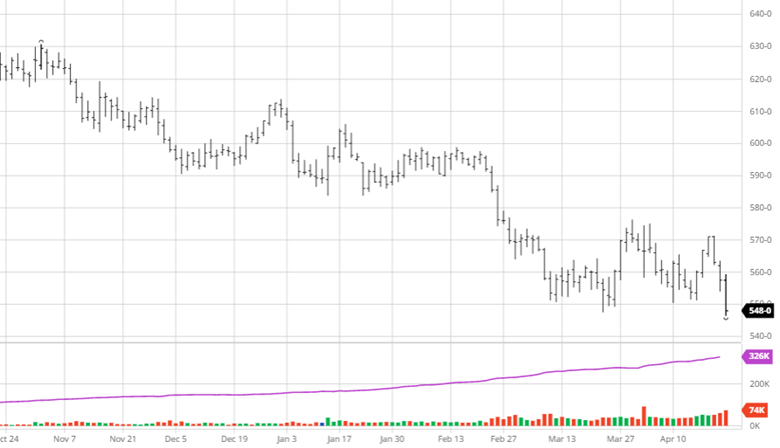

Corn has continued to trade range-bound between $4.10 and $4.30 with a nice recent run to the top of the range. Follow through buying to push towards $4.50 will be needed as harvest heads toward a finish and the large supply coming out of the fields. All crops got a boost after positive news from Secretary Bessent over the weekend saying China will be buying US soybeans (and assume other commodities as well). The market still has downside risk with a large US crop and global economic issues that for now are not flashing major warning signals but the market has been recession warry since the tariffs went into place in April.

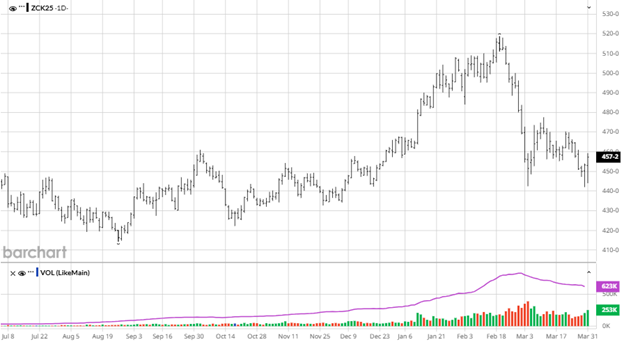

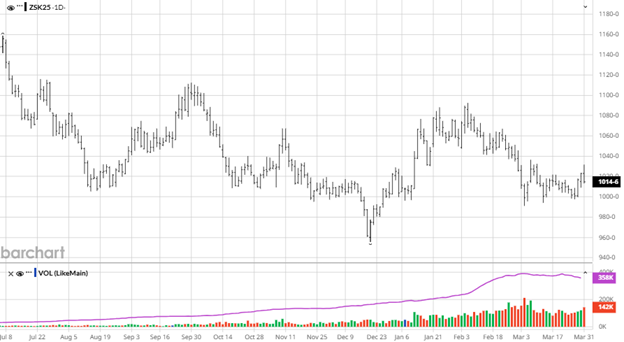

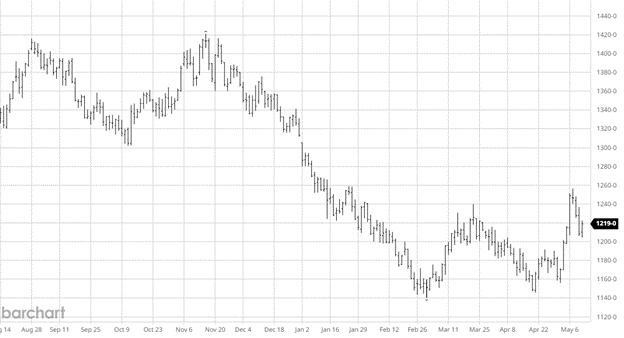

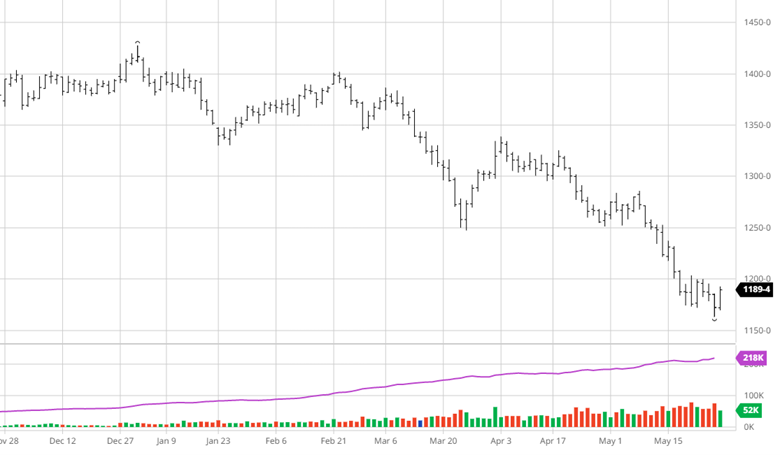

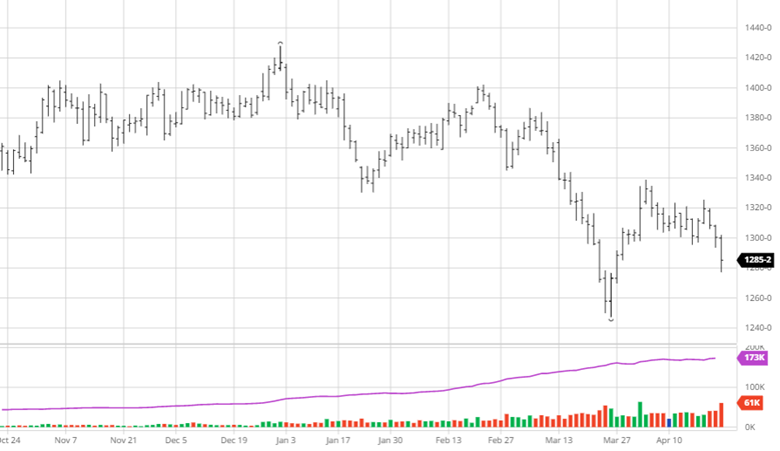

Beans continued their recent rally with positive news on US and China trade relations from Secretary Bessent. We will need to see these soybean purchases from China come to fruition without any more escalations that could put this progress at risk. With the continued Government shutdown the lack of information to trade from the USDA will make private reports the main news.

Beans continued their recent rally with positive news on US and China trade relations from Secretary Bessent. We will need to see these soybean purchases from China come to fruition without any more escalations that could put this progress at risk. With the continued Government shutdown the lack of information to trade from the USDA will make private reports the main news.

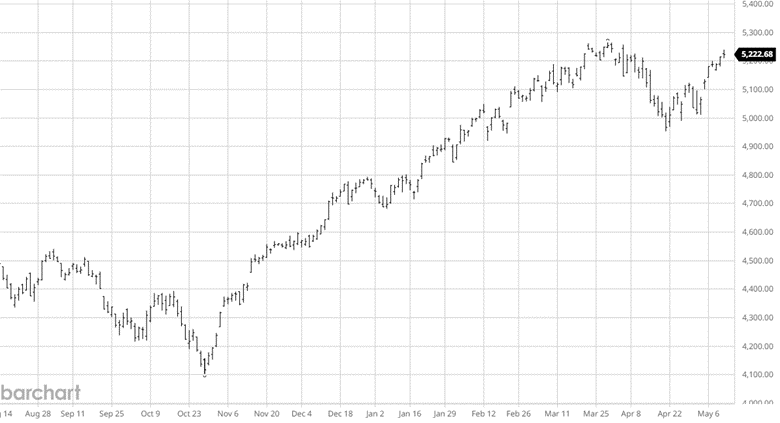

Equity Markets

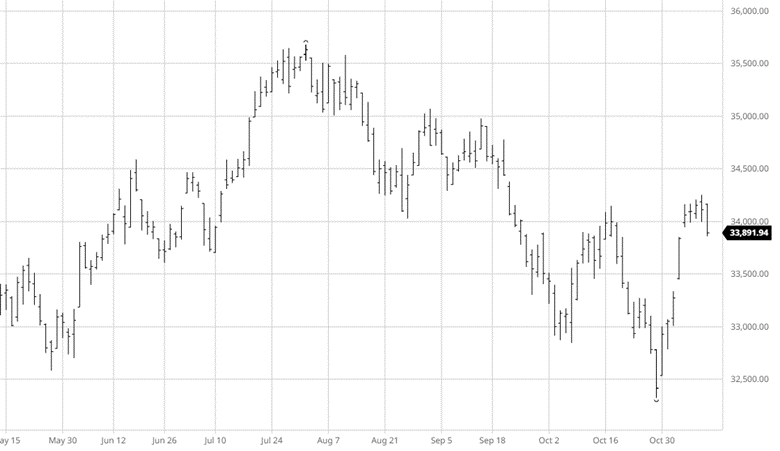

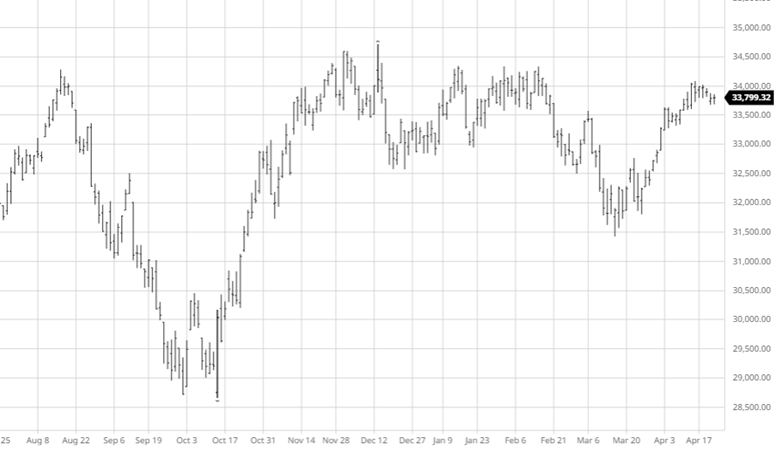

Equity markets continue to move higher after a recent dip as Gold has fallen off its recent highs but equities, lead by AI and tech, continue to climb higher with 2 months left in the year.

Other News

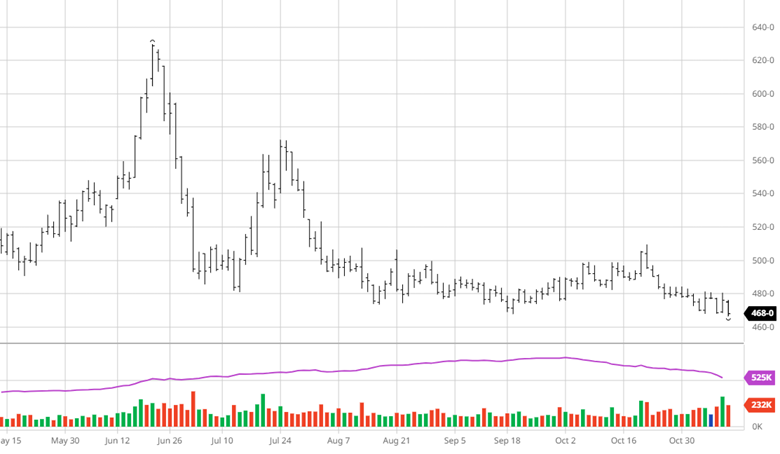

- Cattle futures have fallen quickly off record highs as question marks around the USDA and white house about how they want to address high beef prices continue.

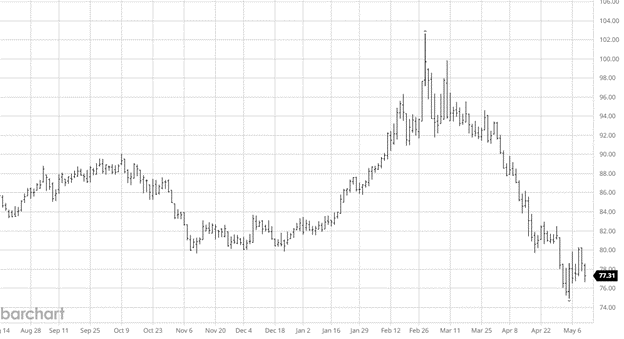

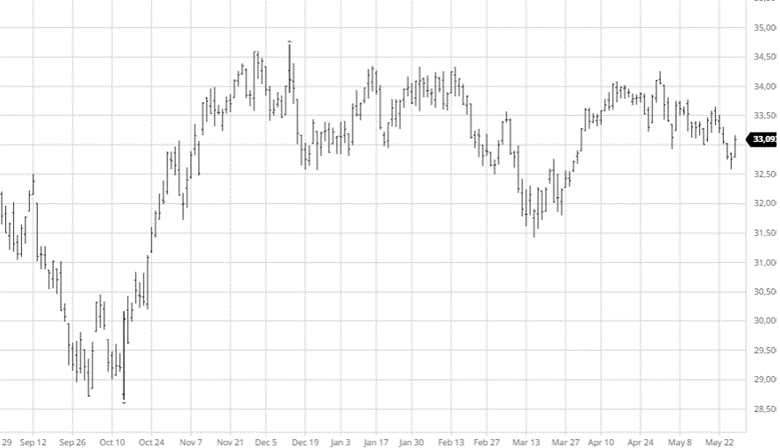

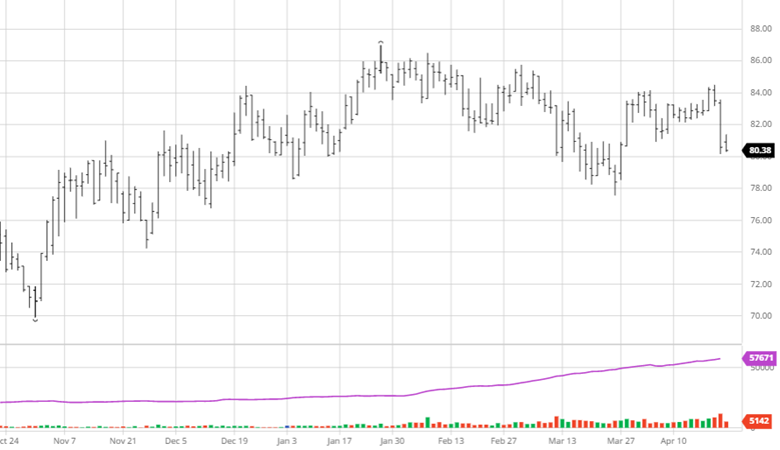

- Cotton remains quiet with no major news to get it out of the mid 60 cent range.

- The government shutdown continues.

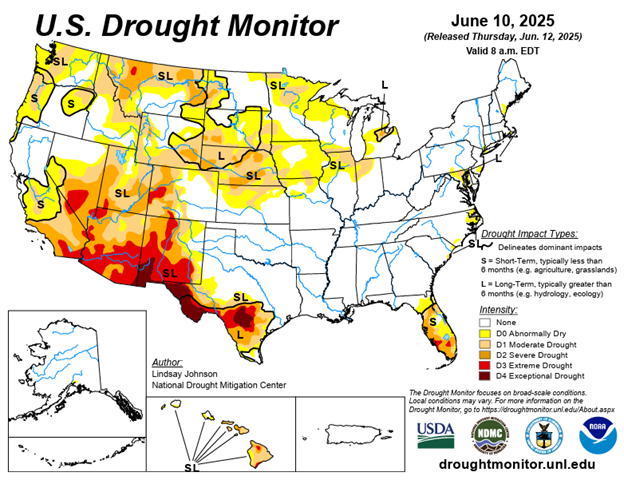

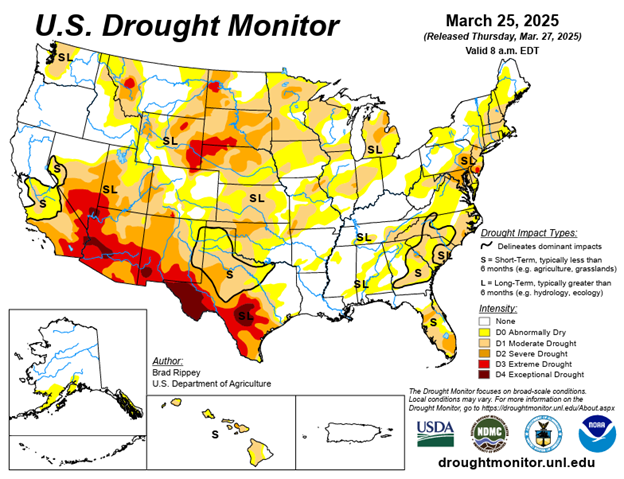

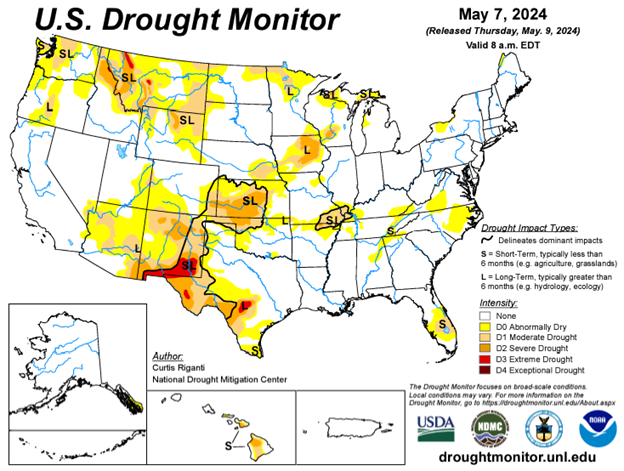

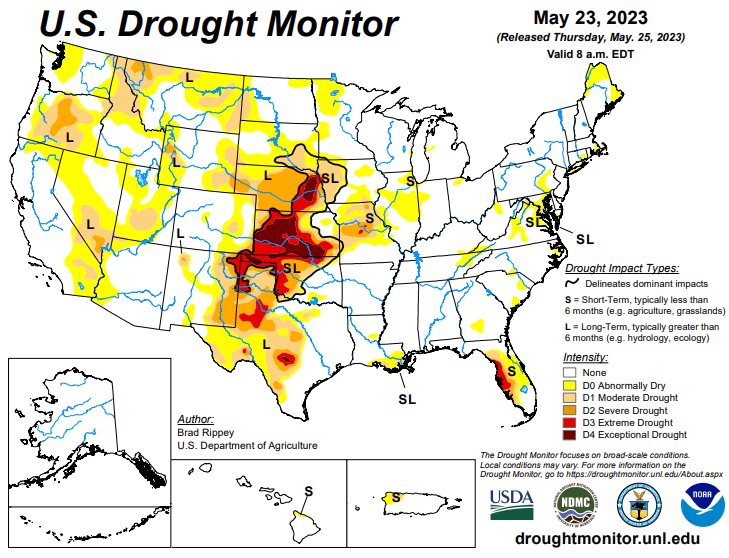

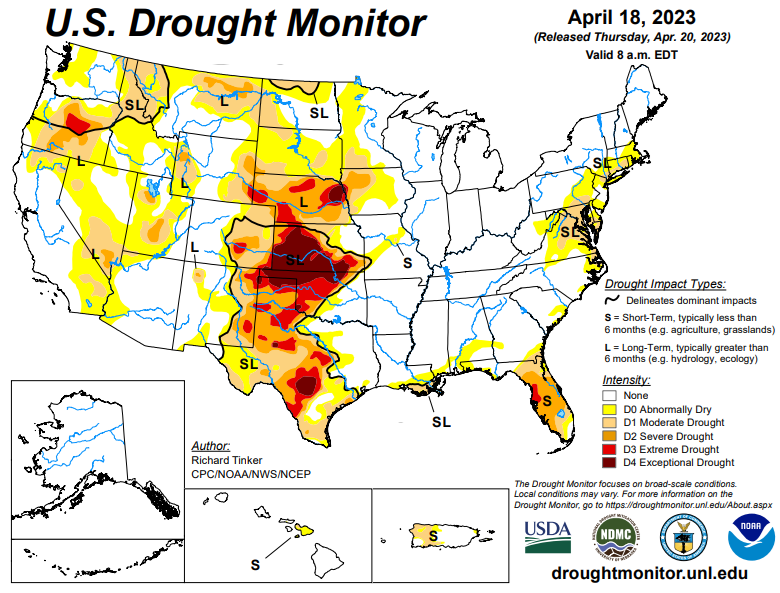

Drought Monitor

Here is the most recent drought monitor as harvest rolls on.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers — Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.

Check it Out: