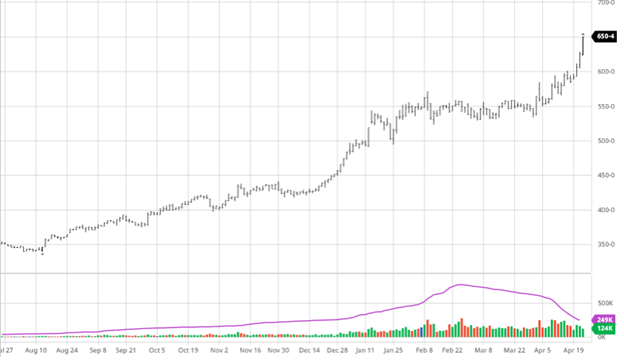

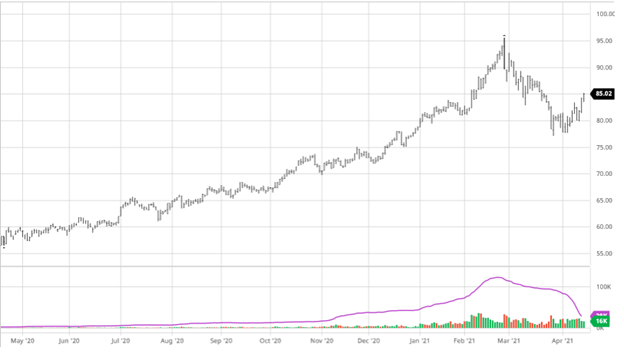

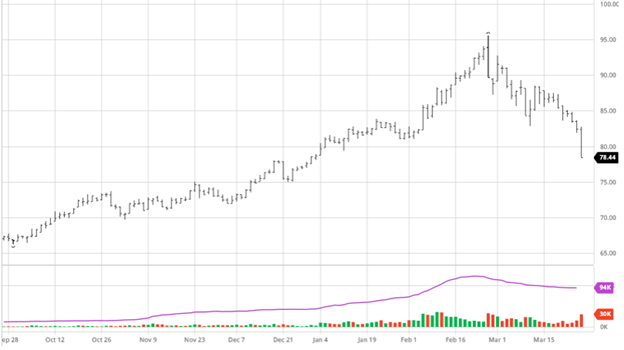

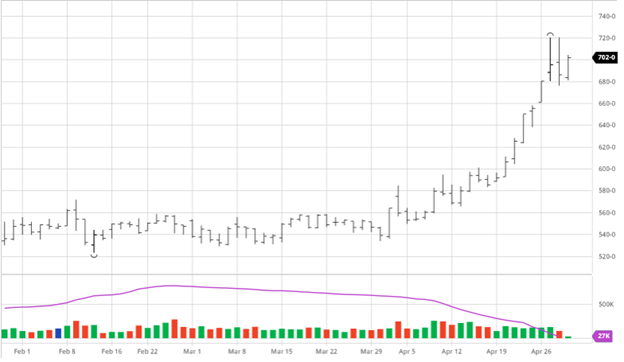

Volatility was the name of the game this week as many days saw wide trading ranges on both sides of unchanged. Looking at the chart below you can just how wide ranges the last few days have been. Despite the volatlity, the May contract settled squarely within the range as of Thursday. This volatility came about as we’ve faced a short squeeze on the front month May contract. Coming into the week, there were nearly 200,000 open contracts, as of this morning there are only 12,500 – presumably many were on the short side and needed to cover.

Regardless of what has caused the rally – higher prices is GREAT for the American Farmer!

For the July contract and new crop Dec, the markets followed the May higher this week and most April as South America’s struggles with drought conditions begin to be seen in yield estimates. Any rain after May 10th probably won’t be able to add must help this late in the game. As expected, exports were good this week but that has become the new normal. The epanded limits coming next week along with higher prices means we should probably expect volatility to hang around.

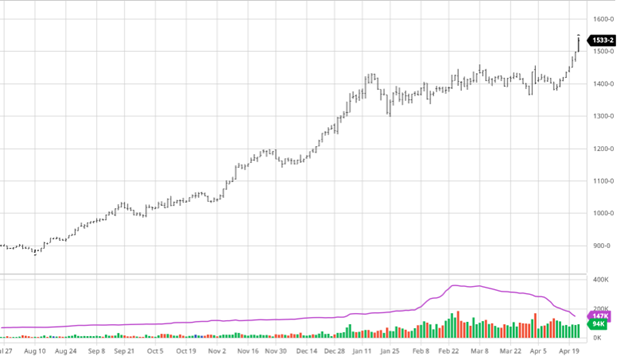

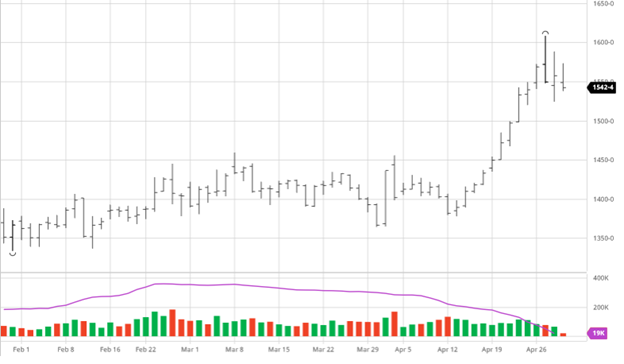

Soybeans had small gains on the week as they also traded in wide ranges in the May contract in addition to future months. The short squeeze has end users scrambling with physical delivery coming up. Along with beans rallying, we have seen basis improve in many areas as buyers try get what is left out of farmers bins. A growing consensus among traders is that continued strong US cash bids indicate that the stock numbers are lower than the USDA reports. Will the USDA adjust in the June report is a major question? Bean meal and oil have also rallied in the past couple weeks aiding to soybeans rise. The fundamental news around the market was less in focus this week with the May contract expiration causing for most of the volatility.

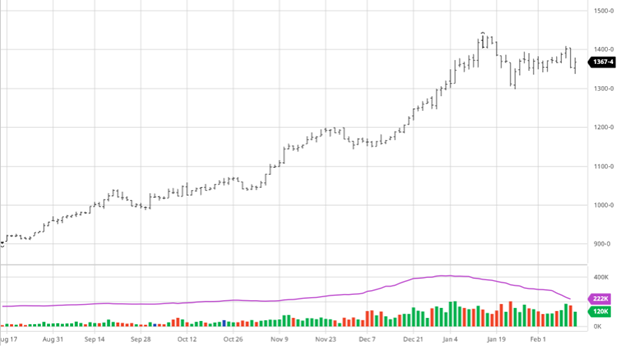

Dow Jones

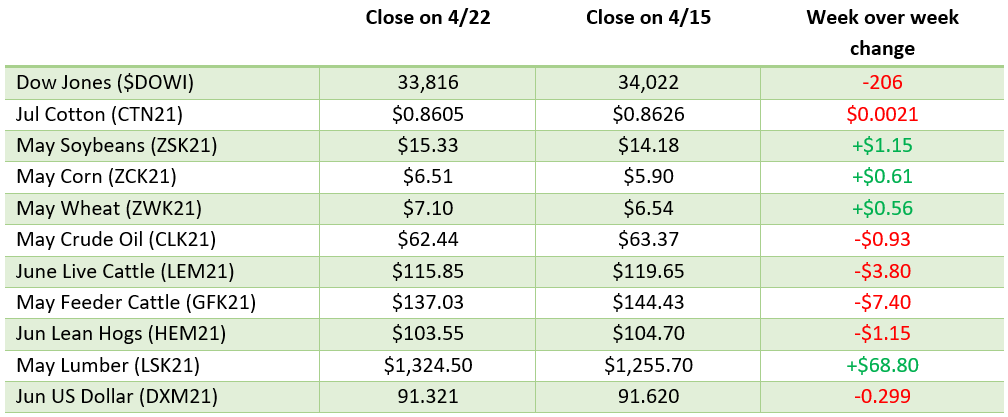

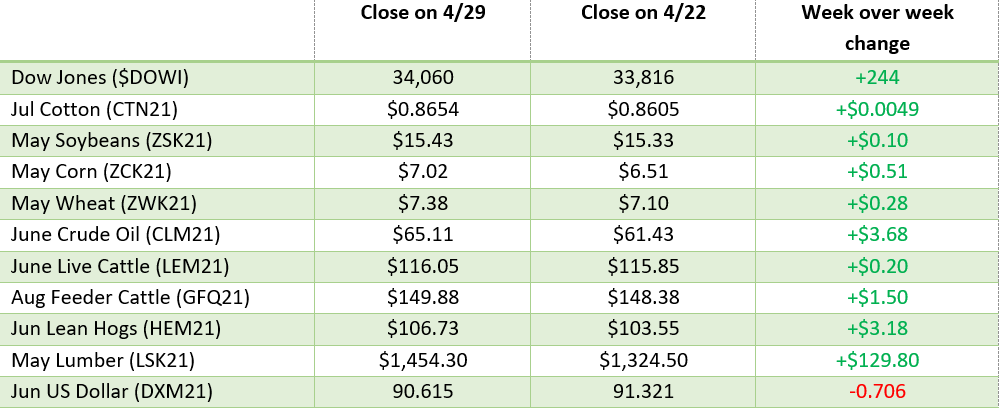

The Dow was up slightly on the week as more news about reopenings continue to roll in and President Biden gave his first speech to Congress. Vaccination rates continue to be strong in many cities and New York City announced this week they will lift all restrictions for reopening July 1st.

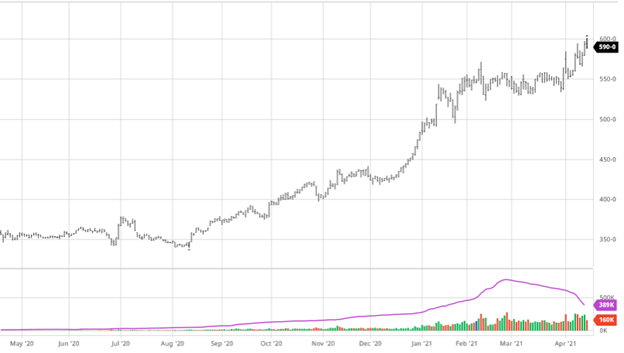

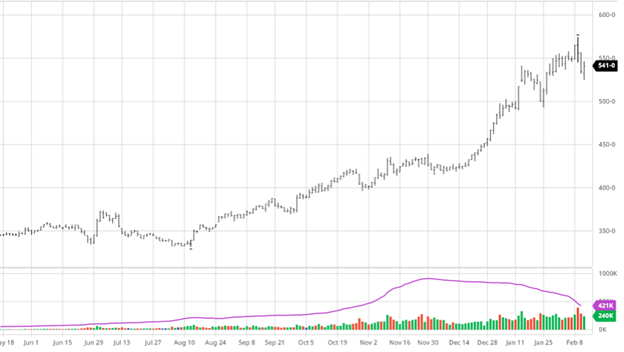

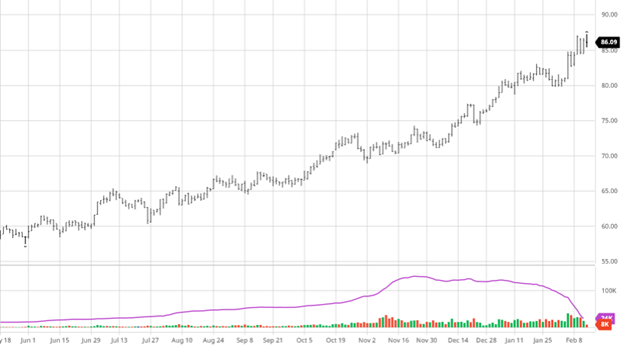

Lumber

Check out our recent post about the lumber market and what all has been going on.

Podcast

Check out or recent podcasts with guests Elaine Kub and Kyle Little. Elaine and Jeff discuss grain markets and trading grains while Kyle helps give insight into the Lumber markets and what has been going on.

https://rcmagservices.com/the-hedged-edge/

Other News

On Monday, daily trading limits will expand for our major markets with corn increased from 25 cents to 40 cents, beans from 70 to $1.00 and wheat from 40 to 45. The CBOT is not tipping their hand that they expect volatility this summer, the daily limit increases are largely due to the high prices to keep daily ranges in line with historic percentages of price.

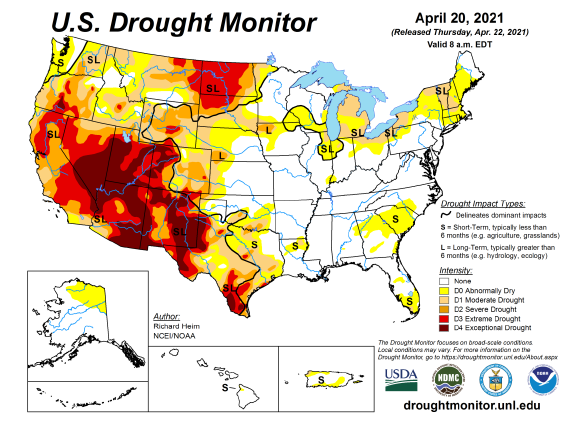

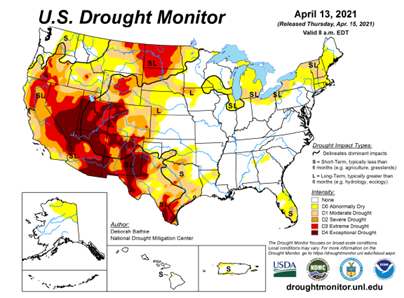

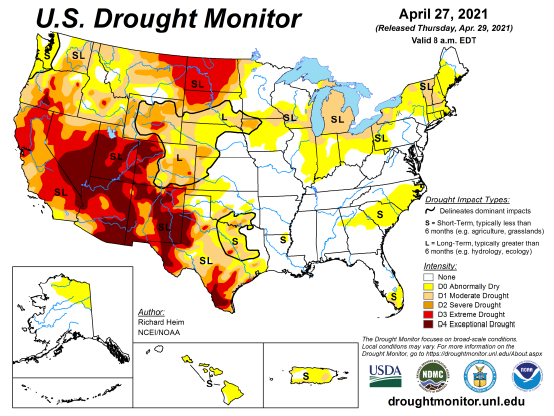

US Drought Monitor

The map below shows what areas are currently experiencing drought conditions across the US. Not much changed from last week. The rains in Texas will help alleviate some dryness in the area but will not solve their moisture issues. Some dryness has crept into Illinois and Indiana but nothing to worry about right now.

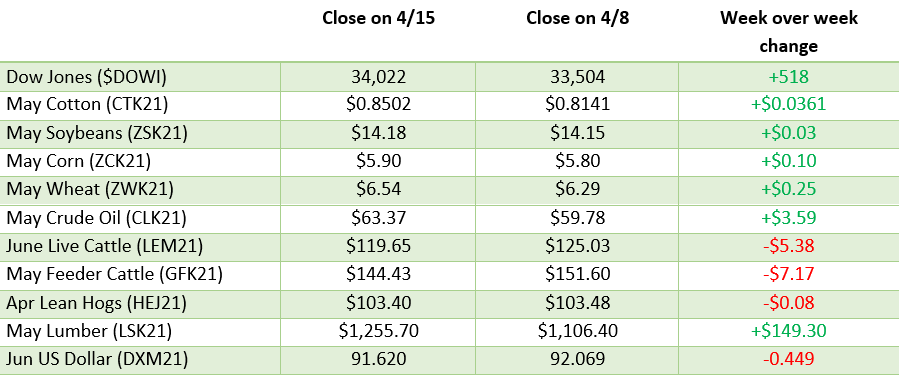

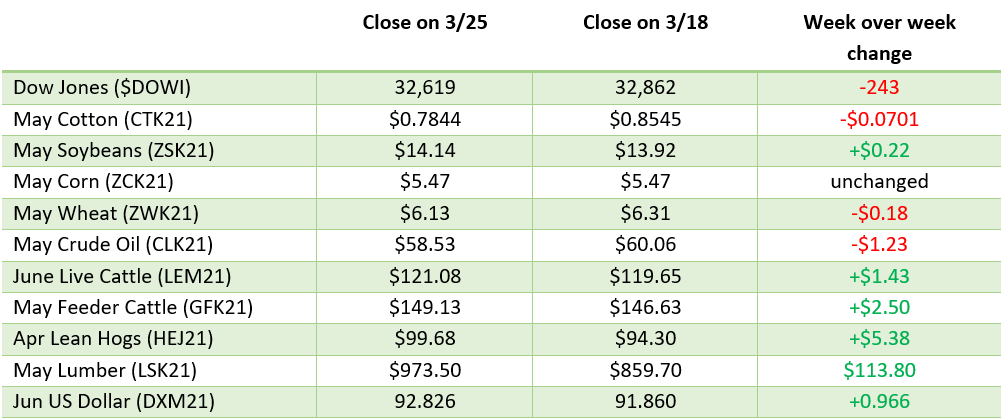

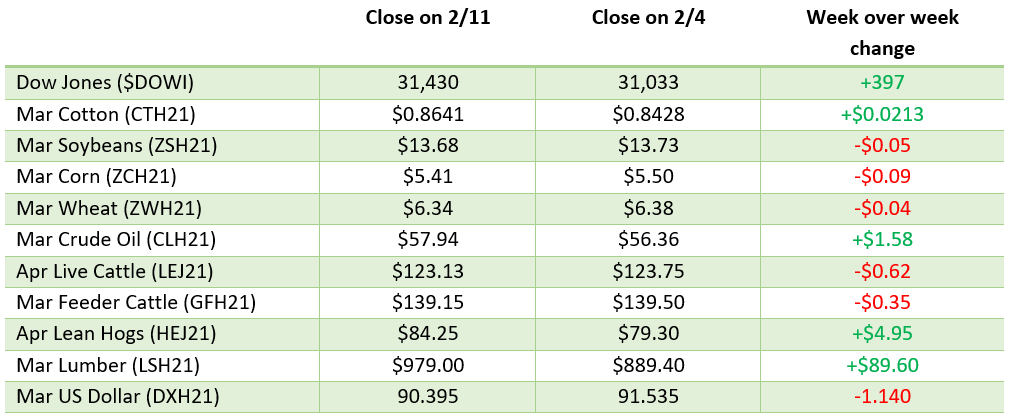

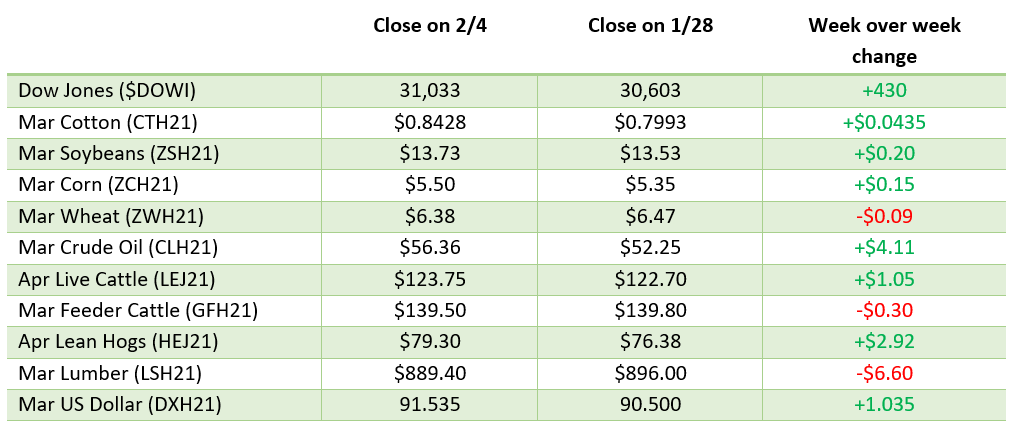

Weekly prices

Via Barchart.com