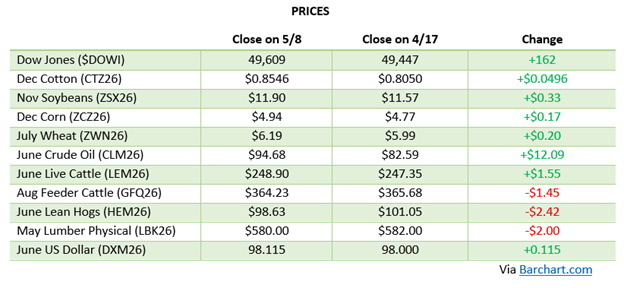

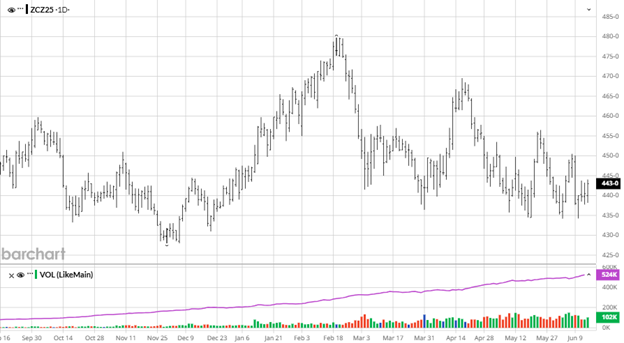

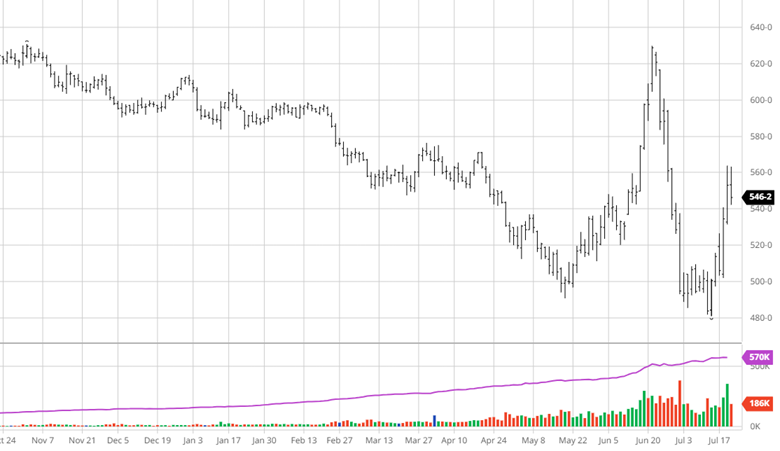

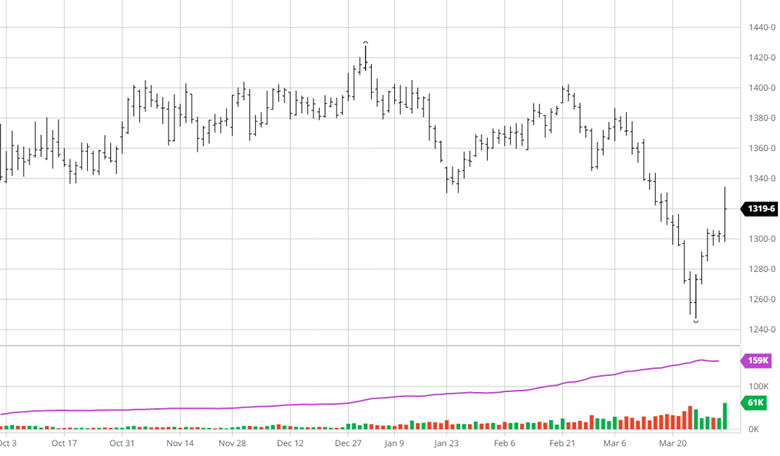

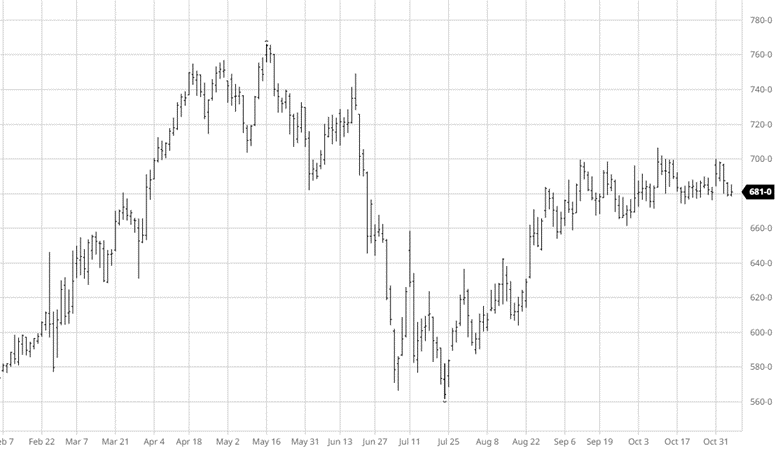

Corn spent the last two weeks trying to carve out a bottom after the brutal three-week stretch of fund liquidation that ran from Memorial Day into mid-month. Managed Money had been selling aggressively, and while that pace finally cooled, the selling pressure left December corn defending the $4.40 area with the season-average farm price forecast sitting right on top of the market. The catalysts that drove the spring rally have all moved the wrong way: planting weather has been close to ideal, crop establishment across the Corn Belt has been excellent, and crude oil has continued to leak lower as the Iran peace framework has firmed up. With old-crop ending stocks comfortable at 2.145 billion bushels and the new-crop balance sheet described by USDA as essentially unchanged, there has simply been no fresh bullish fuel to pull the funds back to the buy side.

Corn spent the last two weeks trying to carve out a bottom after the brutal three-week stretch of fund liquidation that ran from Memorial Day into mid-month. Managed Money had been selling aggressively, and while that pace finally cooled, the selling pressure left December corn defending the $4.40 area with the season-average farm price forecast sitting right on top of the market. The catalysts that drove the spring rally have all moved the wrong way: planting weather has been close to ideal, crop establishment across the Corn Belt has been excellent, and crude oil has continued to leak lower as the Iran peace framework has firmed up. With old-crop ending stocks comfortable at 2.145 billion bushels and the new-crop balance sheet described by USDA as essentially unchanged, there has simply been no fresh bullish fuel to pull the funds back to the buy side.

From here, the entire complex is positioning ahead of the June 30th Planted Acreage and Grain Stocks reports, which is far and away the next major scheduled event. Any meaningful deviation from the March Prospective Plantings number, especially given how much chatter there has been about corn acres slipping on elevated fertilizer costs, has the potential to move this market hard in either direction. The other watch item is the calendar itself: as we push toward pollination in July, the weather forecast carries more and more weight, and a hot, dry ridge building over the Corn Belt is the kind of thing that could put a weather premium back into a market that has very little of one priced in right now.

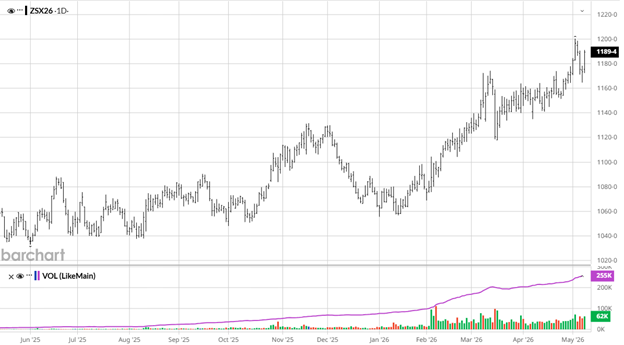

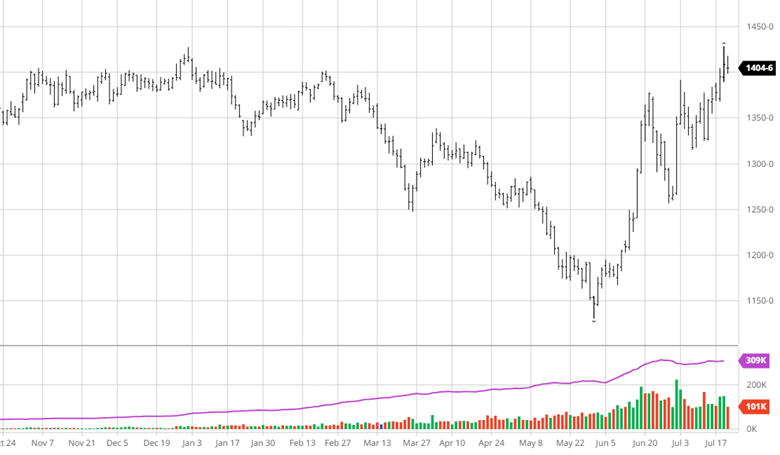

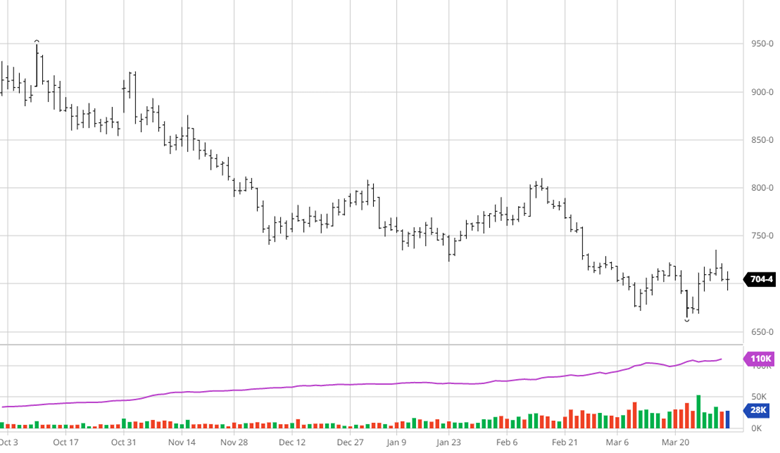

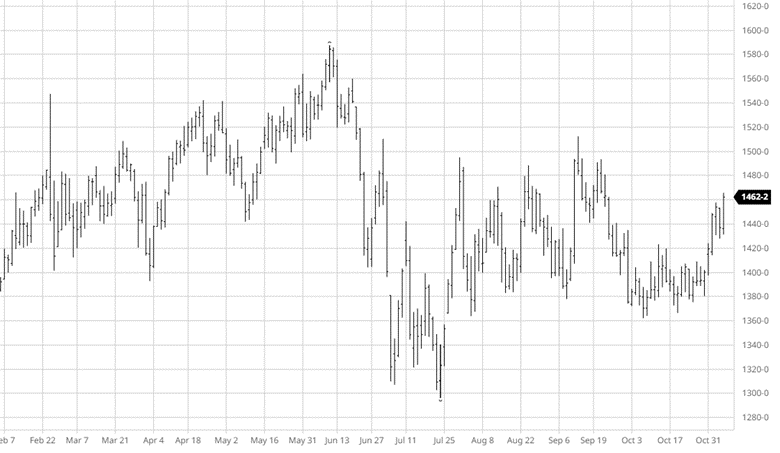

Soybeans have once again been the more resilient half of the row-crop trade, holding up better than corn even as the same fund liquidation wave washed through the complex. July beans have been hovering in the $11.15 to $11.30 neighborhood, leaning on the tighter fundamental backdrop the May WASDE established, namely that 2026/27 ending stocks projection of just 310 million bushels and the booming crush demand story behind it. Board crush margins north of $3 per bushel remain historically strong and continue to do the heavy lifting on the demand side, with the RFS volumes finalized at record highs providing a structural floor under soybean oil. The drag remains the supply side: planting is all but wrapped up at well over 90% complete, Brazil is sitting on another enormous crop, and U.S. export shipments are still running behind last year’s pace. The long-delayed Trump-Xi meeting remains the wildcard that could flip the demand narrative overnight if a framework actually materializes, but the market has been burned enough times waiting on that headline that it is no longer paying up for it. Like corn, beans are squarely focused on what the June 30th acreage figure does to the new-crop picture.

Soybeans have once again been the more resilient half of the row-crop trade, holding up better than corn even as the same fund liquidation wave washed through the complex. July beans have been hovering in the $11.15 to $11.30 neighborhood, leaning on the tighter fundamental backdrop the May WASDE established, namely that 2026/27 ending stocks projection of just 310 million bushels and the booming crush demand story behind it. Board crush margins north of $3 per bushel remain historically strong and continue to do the heavy lifting on the demand side, with the RFS volumes finalized at record highs providing a structural floor under soybean oil. The drag remains the supply side: planting is all but wrapped up at well over 90% complete, Brazil is sitting on another enormous crop, and U.S. export shipments are still running behind last year’s pace. The long-delayed Trump-Xi meeting remains the wildcard that could flip the demand narrative overnight if a framework actually materializes, but the market has been burned enough times waiting on that headline that it is no longer paying up for it. Like corn, beans are squarely focused on what the June 30th acreage figure does to the new-crop picture.

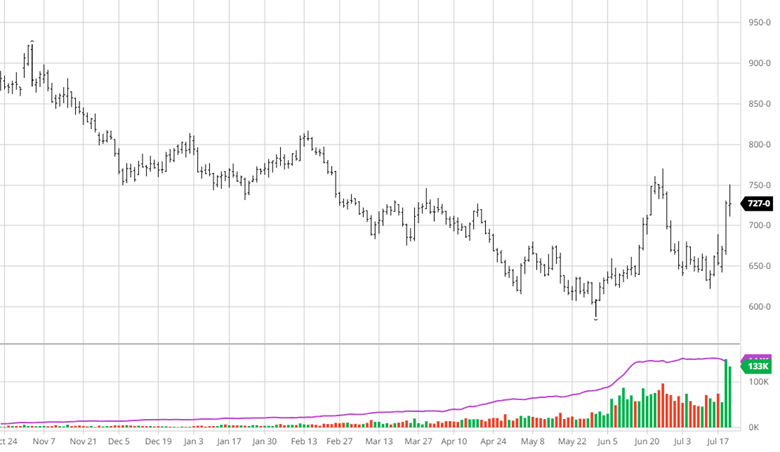

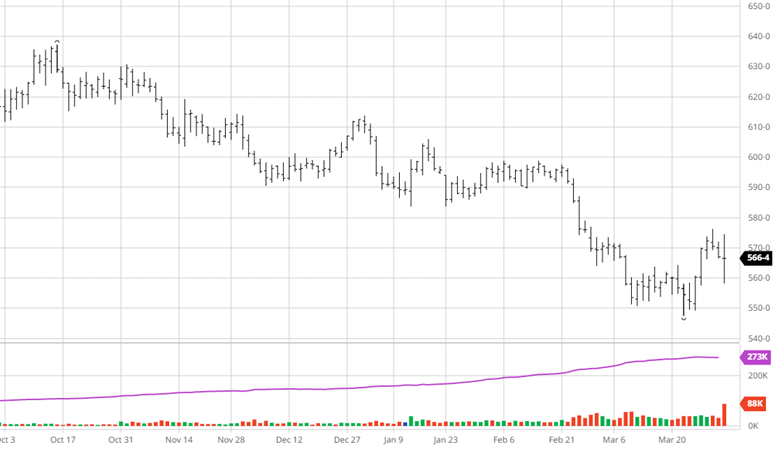

Wheat has continued the slide that began once it touched multi-year highs back in mid-May on the historically small U.S. winter wheat crop. The pullback has been driven by harvest pressure now that combines are rolling across the Southern Plains, timely late-May and early-June rains that pulled crop conditions up off the worst-case scenario, and funds booking profits after an extended run. July Chicago SRW has worked down into the high $5.80s and July KC HRW has slid into the low $6.30s. The important thing to remember is that nothing about the supply story has actually changed, this is still projected to be the smallest domestic wheat harvest since 1965, so the question is whether harvest lows are in or whether the seasonal pressure has more to run. Watch the pace of harvest results, spring wheat conditions in the Northern Plains, and whether the recent rains were enough to truly stabilize the HRW crop or just a temporary reprieve.

Wheat has continued the slide that began once it touched multi-year highs back in mid-May on the historically small U.S. winter wheat crop. The pullback has been driven by harvest pressure now that combines are rolling across the Southern Plains, timely late-May and early-June rains that pulled crop conditions up off the worst-case scenario, and funds booking profits after an extended run. July Chicago SRW has worked down into the high $5.80s and July KC HRW has slid into the low $6.30s. The important thing to remember is that nothing about the supply story has actually changed, this is still projected to be the smallest domestic wheat harvest since 1965, so the question is whether harvest lows are in or whether the seasonal pressure has more to run. Watch the pace of harvest results, spring wheat conditions in the Northern Plains, and whether the recent rains were enough to truly stabilize the HRW crop or just a temporary reprieve.

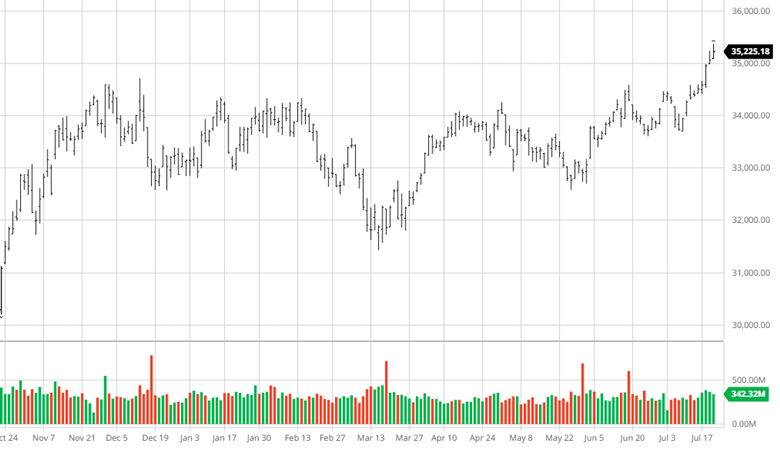

Equity Markets

Equity markets have extended their remarkable run, with the major indexes pushing to fresh records even as volatility has picked up and some of the high-flying AI names have seen sharp, fast bouts of profit-taking. The dominant tension remains inflation: with price data still running hot, a growing share of investors now believes the Fed’s next move could be a rate hike before year-end rather than another cut, a notable shift in expectations. For now, the AI trade and strong earnings tone have been enough to keep dip-buyers in control, but the market feels increasingly two-sided after such a long stretch of one-way gains.

Energy Markets

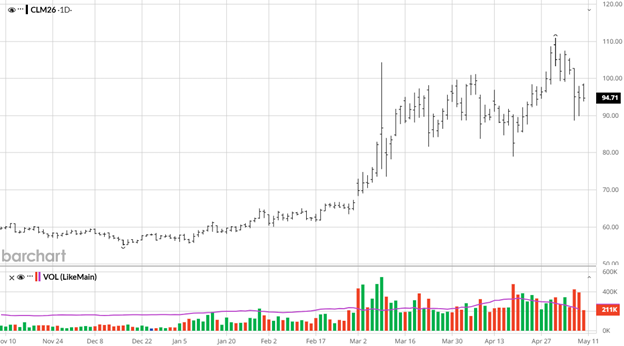

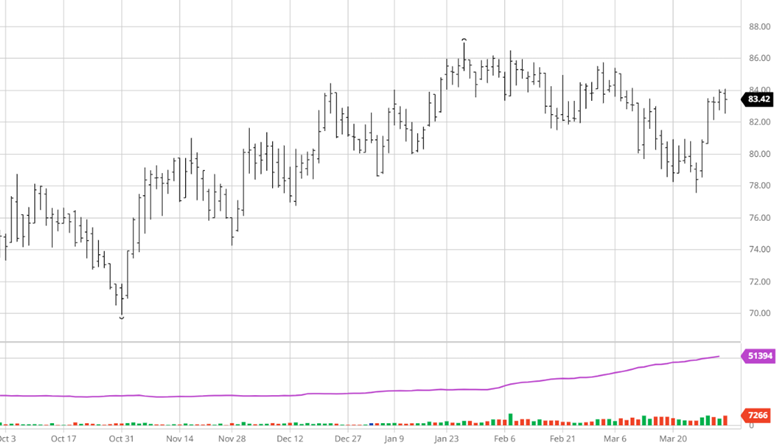

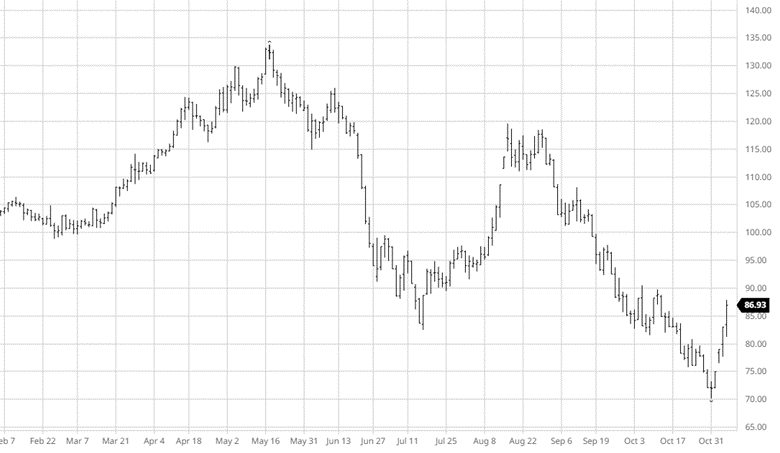

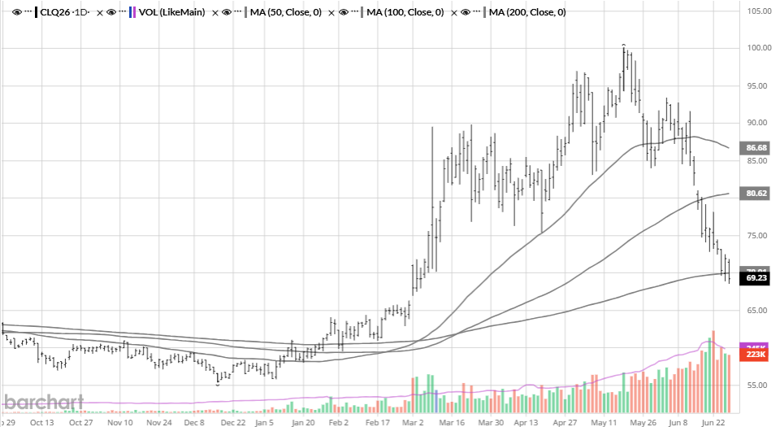

Crude oil has remained the single most important variable for the entire ag complex, and the direction has been lower. WTI has continued to retreat from its spring highs above $110 per barrel as the Iran peace negotiations have progressed, with the apparent Memorandum of Understanding to wind down the Middle East conflict taking crude back below $85 to close out the prior period and keeping pressure on prices since. The reopening of the Strait of Hormuz to international shipping is reportedly part of the framework, and if that holds, the war premium that propped up the grain complex this spring continues to bleed out. The practical takeaway for producers is that fertilizer cost relief is finally becoming more than partial, nitrogen and diesel have eased off their wartime peaks, though prices are not yet all the way back to pre-conflict norms.

Other News

– The June 30th USDA Planted Acreage and Grain Stocks reports are the dominant near-term event for the entire complex. With so much debate over whether high fertilizer costs trimmed corn acres from the March intentions, and whether beans picked up the difference, any surprise in the final acreage figures will be a significant market mover heading into July.

– The New World screwworm situation in Texas continues to be monitored after its first mention in the WASDE narrative last month, a reminder that animal agriculture is carrying its own emerging risks alongside the geopolitical backdrop.

– Cotton has continued to drift with the broader commodity complex as crude has retreated, peeling away some of the energy-driven premium that had made natural fiber more attractive versus petroleum-based synthetics. Producers who can lock in profitable margins at current levels while keeping upside participation should continue to evaluate their hedging options.

– Any concrete movement on a Trump-Xi meeting remains the most important demand-side wildcard for soybeans. A genuine resumption of Chinese buying would change the bean story quickly, but the market has stopped pricing it in until it actually happens.

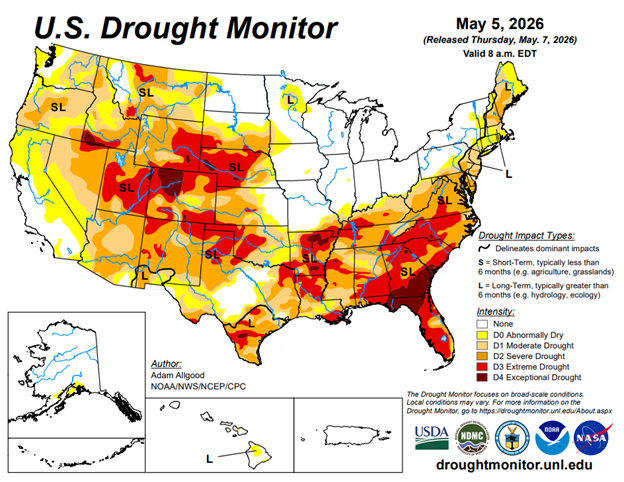

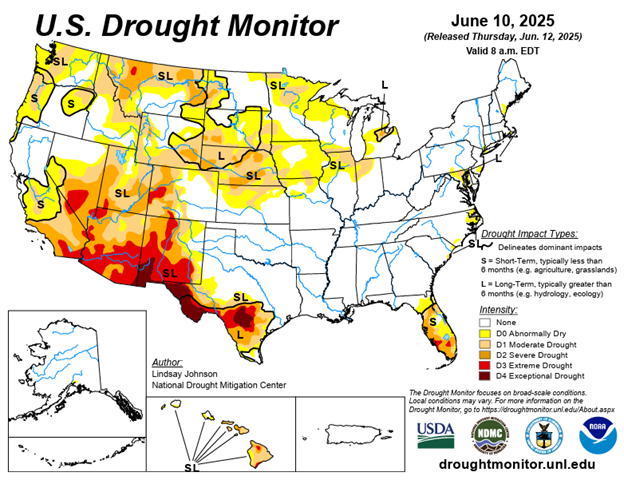

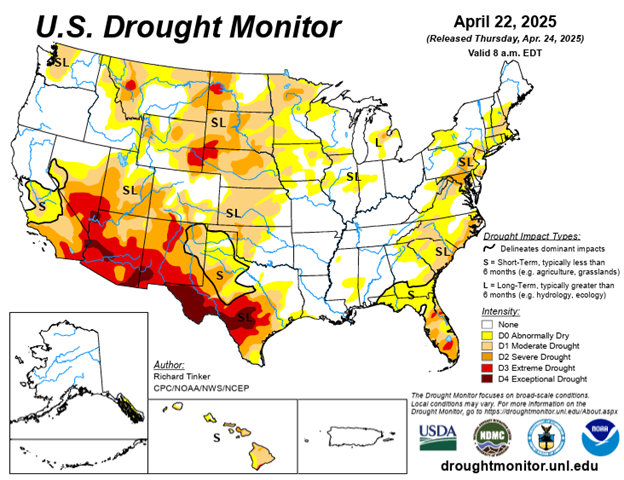

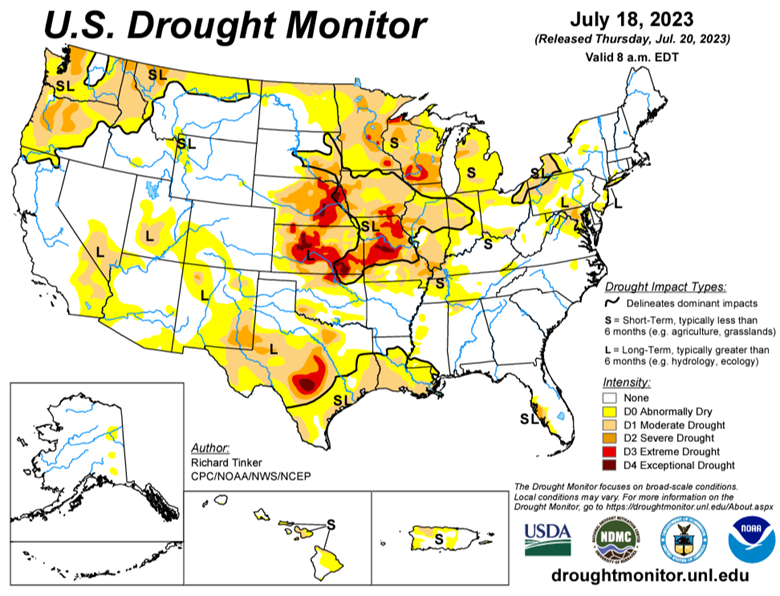

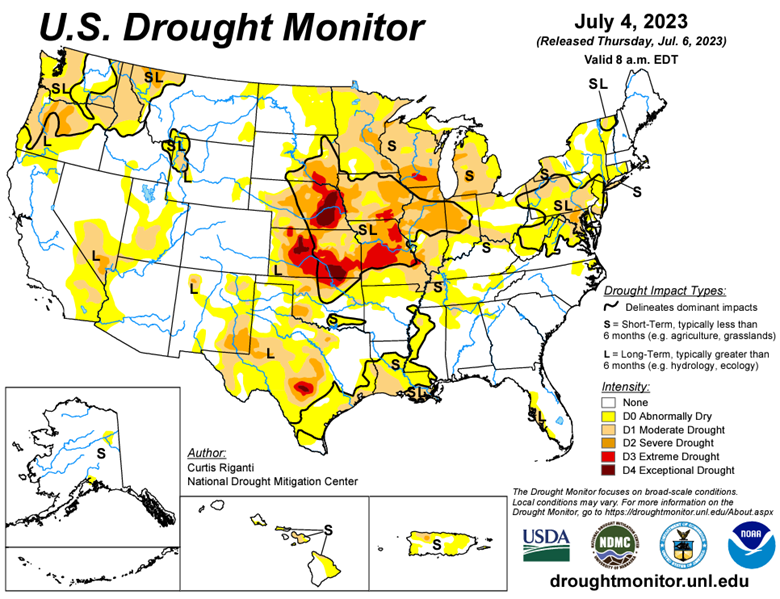

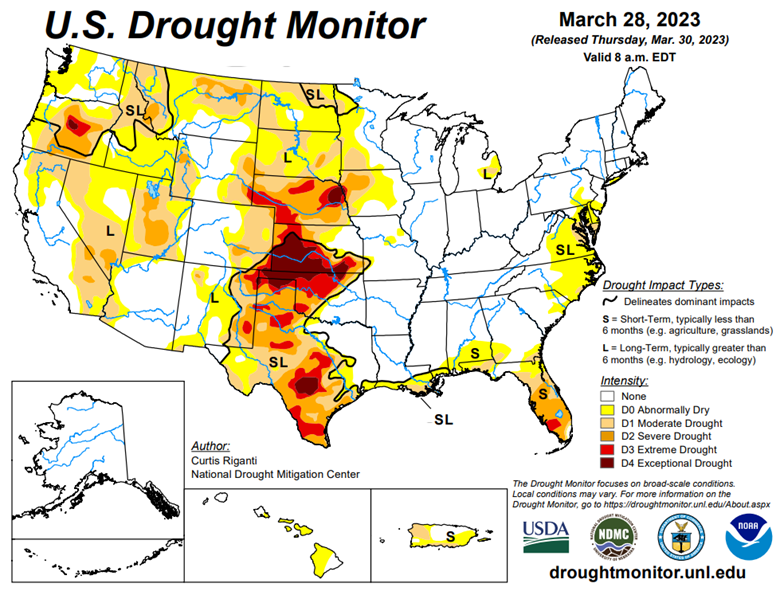

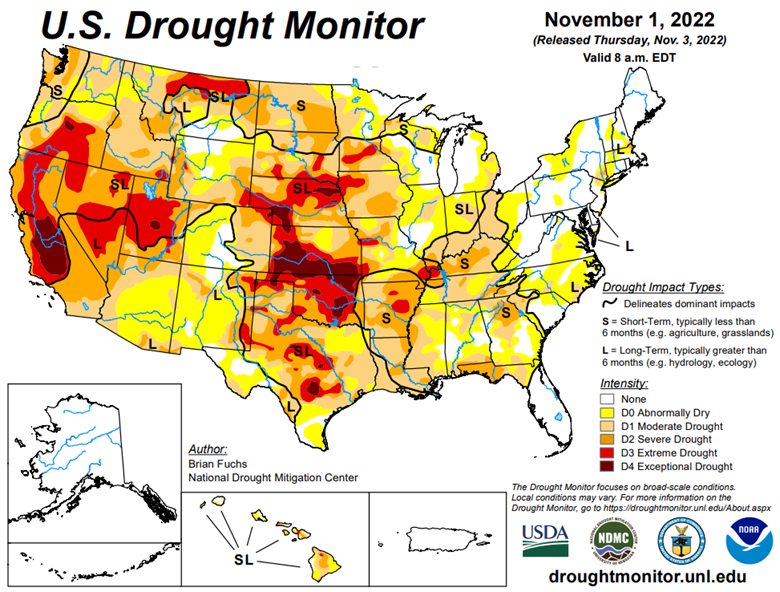

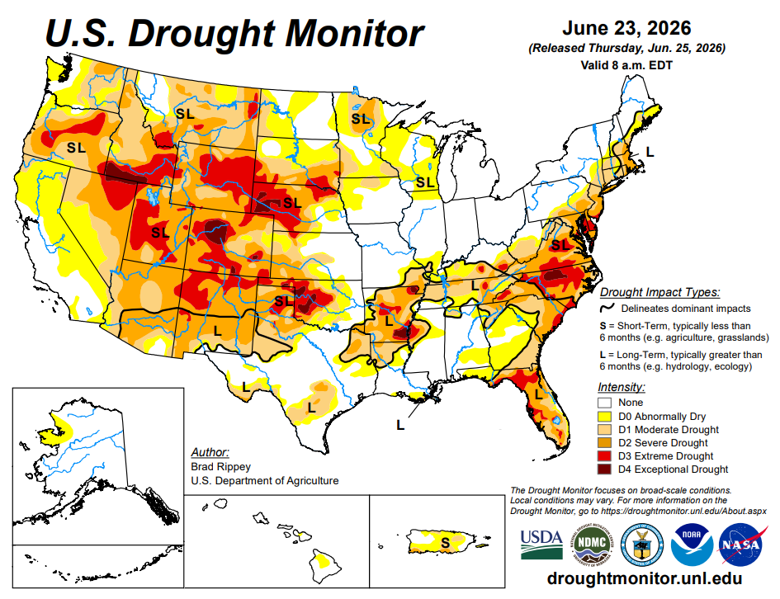

Drought Monitor

Here is the most recent drought monitor.

Contact an Ag Specialist Today

Whether you’re a producer, end-user, commercial operator, RCM AG Services helps protect revenues and control costs through its suite of hedging tools and network of buyers/sellers.

Contact Ag Specialist Brady Lawrence today at 312-858-4049 or blawrence@rcmam.com.