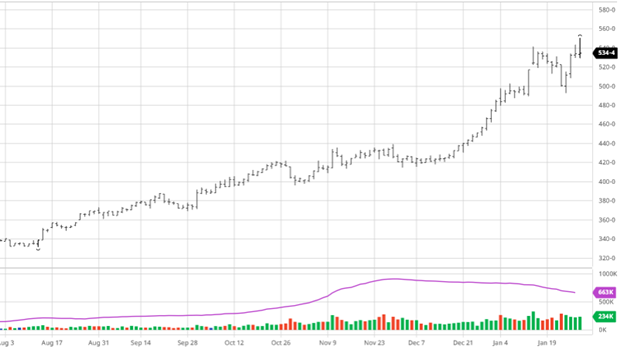

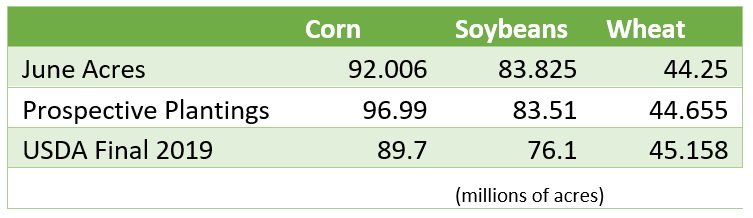

The USDA Acreage report was released this week and was bullish for corn. Planted acres came in @ 92.70 million acres, which was below the average estimate of 93.787 million. June 1st stocks were also slightly lower than estimates coming in at 4.112 billion bushels. For the second year in a row the USDA came out with less planted acres than pre-report estimates. There was also a note at the start of the report saying there are still 2.18 million acres intended to be planted during the survey time of May 29-June 17. This means that the 92.70 million number may end up being lower as odds are not all the 2.18 million acres got planted. This combined with the lower stocks gave corn a big boost as Dec’ 21 futures went limit up post report.

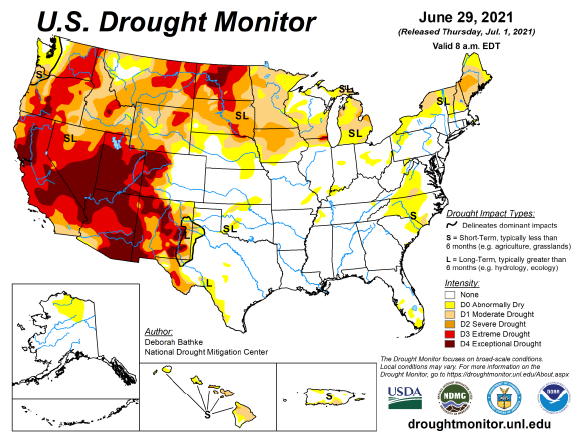

This is the last major market moving report (historically) of the summer, which means we are now in a weather market for the time being. The upper Midwest is still very dry and needs relief as you can see in the drought monitor chart at the bottom.

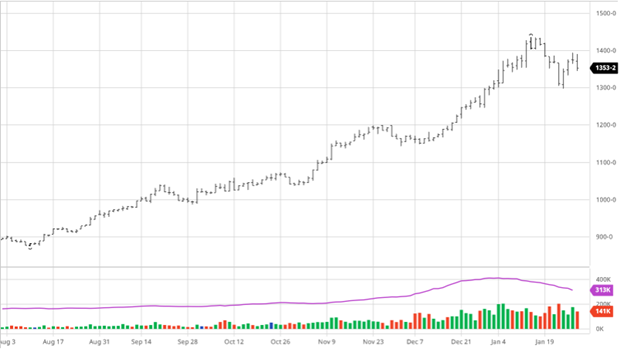

Soybeans, like corn, saw big gains following the release of the acreage report. Planted acres came in at 87.6 million acres, below the average estimate of 88.955 million. The June 1st stocks were also lower than estimates coming in at 767 million bushels, 20 million lower than the average estimate. Beans had a similar post report reaction to corn because the bullishness of the numbers were similar. With acres and stocks both being smaller than anticipated this will put pressure on the crop and weather during August will be very important for not only the crop but also the price.

Wheat had a neutral report but followed corn and soybeans higher after. Wheat looks to be forming a bottom on the charts but July weather is still critical for the plains/Canadian wheat crop. Wheat struggled lower on Thursday as they had their own trade and did not follow the lead of corn and soybeans. Weather this month will be important for the crop as we are also in a weather market for wheat too.

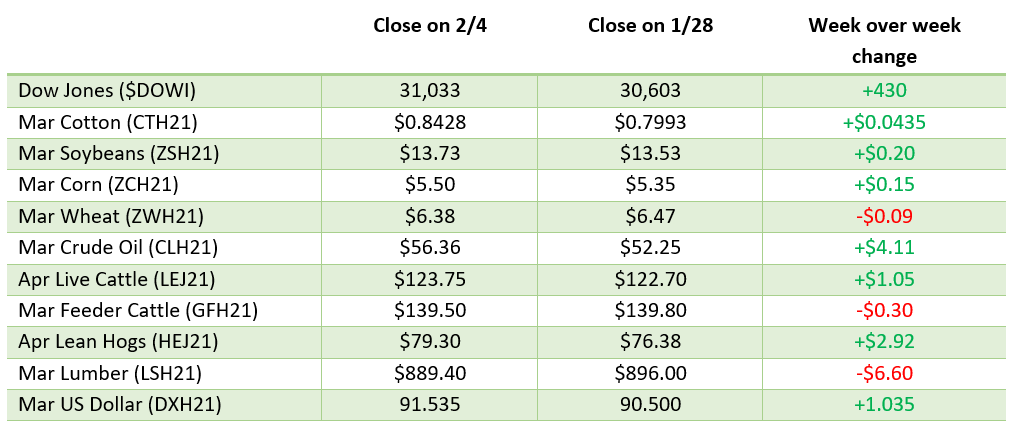

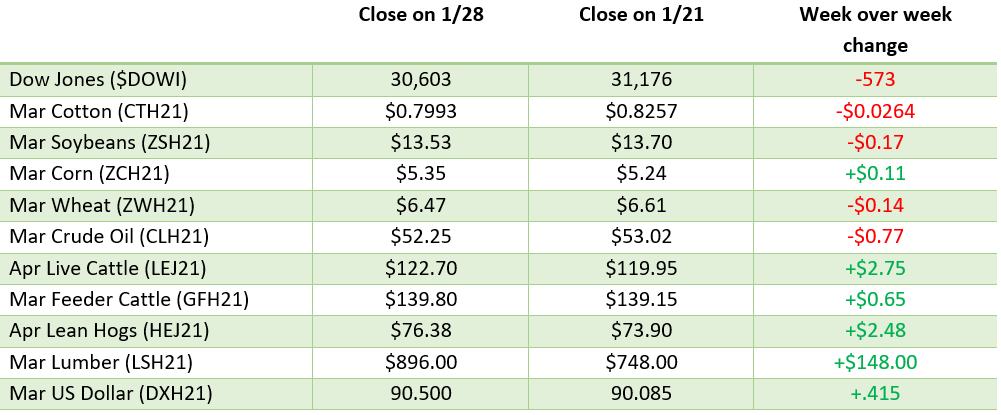

Dow Jones

The Dow gained on the week as all major indexes had a good week as trade continues to be getting back to normal following the covid lockdown of the last year. The Dow closed out the month strong after seeing major weakness the first half of June.

Lumber

Lumber prices have continued their slide down and are back in the 700s after trading into the mid 1700s in early May. The pressure on the market looks to continue as the downturn has been sharp.

Podcast

Check out our recent podcast with Dr. Greg Willoughby: We’re talking with Greg in the new episode about being a “plant doctor”, weather patterns, GMO & organic produce, crop history, technical advances, level 201 education on agronomy, the agronomy equation, Helena Agri, soil biology, American v European agriculture, Greg’s early background in livestock, and the advancement of native plants to modern produce.

https://rcmagservices.com/the-hedged-edge/

US Drought Monitor

The map below shows current drought conditions and the continued problems in the upper Midwest and continued sever drought in the western US.

Via Barchart.com